|

|

市場調査レポート

商品コード

1776232

欧州の難治性てんかん治療市場:分析・予測 (2025~2035年)Europe Refractory Epilepsy Treatment Market: Analysis and Forecast, 2025-2035 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 欧州の難治性てんかん治療市場:分析・予測 (2025~2035年) |

|

出版日: 2025年07月25日

発行: BIS Research

ページ情報: 英文 60 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

欧州の難治性てんかん治療の市場規模は、2024年の13億4,320万米ドルから、予測期間中はCAGR 6.98%で推移し、2035年には28億2,280万米ドルに達すると予測されています。

欧州における難治性てんかん治療のパラダイムは、より個別化され、各患者の臨床プロファイル、遺伝子マーカー、ライフスタイルの選択を活用するものへと変化しつつあります。欧州の医療提供者は、従来の"one-size-fits-all"アプローチを超えて、ゲノミクス、分子診断学、高度なデータ解析の開発を組み合わせることで、オーダーメイドの治療計画を立てることができます。発作制御の改善と副作用の低減に加え、この精密な技術は、高価な試行錯誤の投薬も最小限に抑えます。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2025-2035 |

| 2025年評価 | 14億2,430万米ドル |

| 2035年予測 | 28億2,280万米ドル |

| CAGR | 6.98% |

欧州医薬品庁 (EEA) による厳格な規制、国境を越えた臨床登録システム、欧州の強力なバイオバンクインフラが、新たな抗てんかん薬の検証やバイオマーカーの開発を加速させています。予測アルゴリズムを活用して薬剤耐性のある患者を早期に特定することで、神経調節療法や標的医薬品によるタイムリーな介入が可能になっています。また、学術機関、てんかん専門クリニック、ライフサイエンス業界のイノベーターの協力が、西欧・中欧・東欧全体に広がる精密神経学ネットワークのもとで、より正確な予後予測、早期診断、最適化された治療経路の実現を促しています。これにより、患者の転帰が改善され、費用対効果の高い医療提供が可能になることが期待されています。

欧州の難治性てんかん治療市場は急速に変化しており、医療従事者や医療システムは、第一選択薬で発作のコントロールができない患者に対し、より個別化された技術主導の治療へとシフトしています。この市場には、先進的な医薬品、神経調節デバイス、新興バイオ医薬品などが含まれており、欧州全体600万人いると推定されるてんかん患者の約30%が薬剤耐性を有していることが特徴です。難治性てんかんがもたらす深刻な臨床的・経済的負担への認識が高まっていることから、早期の発見と介入を可能にする革新的な治療法や診断ツールへの投資が促進されています。

次世代の抗てんかん薬 (カンナビジオールをベースとした補助療法薬や新規分子化合物) や発作コントロールの新たな手段を提供する神経調節技術 (深部脳刺激[DBS]、迷走神経刺激[VNS]、応答性神経刺激[RNS]など) は、重要な市場セグメントとなっています。EUの医療機器規則 (MDR) やEMAによる厳格な監督体制が安全性と有効性を高い水準で確保し、また、西欧における充実した償還制度や中東欧諸国での医療支出の増加が導入の後押しとなっています。

また、分子診断、AIを活用した予測アルゴリズム、ゲノムプロファイリングといった技術進歩が、精密医療の道を拓き、試行錯誤的な投薬を減らし、治療成果の向上に寄与しています。ただし課題も残されています。専門てんかんセンターの不足、高額な治療費、地域ごとの医療アクセスの格差などが、市場拡大の妨げとなっています。それでも、臨床の専門家、バイオ医薬品企業、学術研究ネットワークの連携が、より集中的かつ効果的な介入の基盤を築いており、難治性てんかん治療は、欧州における神経疾患領域の中でも注目すべき重要分野の一つとなりつつあります。

市場の分類:

セグメンテーション1:地域別

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他

当レポートでは、欧州の難治性てんかん治療の市場を調査し、主要動向、市場影響因子の分析、パイプラインの動向、市場規模の推移・予測、各種区分・地域/主要国別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

目次

エグゼクティブサマリー

範囲と定義

第1章 市場:業界展望

- 主要なトレンド

- 難治性てんかん治療市場の動向

- 難治性てんかん治療のための新たな標的療法

- ビジネス戦略

- 企業戦略

- 市場機会

- スタートアップの情勢

- エコシステムにおける主要なスタートアップ

- パイプライン薬:難治性てんかん治療

- 動向

- 難治性てんかん治療のための新たな標的療法

- 市場力学

- 動向、促進要因、課題、機会:現在および将来の影響評価

- 市場促進要因

- 市場抑制要因

- 市場機会

- 市場の課題

第2章 地域

- 地域サマリー

- 欧州

- 地域概要

- 市場成長の原動力

- 市場課題

- ドイツ

- フランス

- イタリア

- スペイン

- 英国

- その他

第3章 市場:競合ベンチマーキングと企業プロファイル

- Biocodex-SP

- GSK plc.

- LivaNova PLC

- Novartis AG

- UCB S.A.

第4章 調査手法

List of Figures

- Figure 1: Europe Refractory Epilepsy Treatment Market (by Scenario), $Million, 2024, 2028, and 2035

- Figure 2: Europe Refractory Epilepsy Treatment Market, 2024-2035

- Figure 3: Timeline of Drugs Launched for Refractory Epilepsy Treatment

- Figure 4: Europe Refractory Epilepsy Treatment Market Snapshot

- Figure 5: Refractory Epilepsy Treatment Market, $Million, 2024 and 2035

- Figure 6: Europe Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 7: Germany Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 8: France Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 9: Italy Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 10: Spain Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 11: U.K. Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 12: Rest-of-Europe Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 13: Inclusion and Exclusion

- Figure 14: Data Triangulation

- Figure 15: Top-Down and Bottom-Up Approach

- Figure 16: Assumptions and Limitations

List of Tables

- Table 1: Market Snapshot

- Table 2: Recent Investments in Refractory Epilepsy Treatment

- Table 3: Key Development in Seizure Management by Key Companies

- Table 4: Start-ups and Investment Landscape

- Table 5: Pipeline Drugs and its Clinical Trial Phase

- Table 6: Recent Investments in Refractory Epilepsy Treatment

- Table 7: Major Development in the Refractory Epilepsy Treatment Market

- Table 8: Major Development in Refractory Epilepsy Treatment Market

- Table 9: Major Drugs and Their Indication

- Table 10: Major Devices Used in the Refractory Epilepsy Treatment Market

- Table 11: Refractory Epilepsy Treatment Market (by Regio), $Million, 2023-2035

- Table 12: Europe Refractory Epilepsy Treatment Market (By Country), $Million, 2023-2035

This report can be delivered in 2 working days.

Introduction to Europe Refractory Epilepsy Treatment Market

The Europe refractory epilepsy treatment market is projected to reach $2,822.8 million by 2035 from $1,343.2 million in 2024, growing at a CAGR of 6.98% during the forecast period 2025-2035. The paradigm for treating refractory epilepsy in Europe is changing to one that is more individualised and makes use of each patient's clinical profile, genetic markers, and lifestyle choices. Beyond the conventional ""one-size-fits-all"" approach, European healthcare providers can create customised treatment plans by combining developments in genomics, molecular diagnostics, and advanced data analytics. In addition to improving seizure control and lowering side effects, this precise technique also minimises expensive trial-and-error dosing.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2025 - 2035 |

| 2025 Evaluation | $1,424.3 Million |

| 2035 Forecast | $2,822.8 Million |

| CAGR | 6.98% |

The European Medicines Agency's strict regulations, cross-border clinical registries, and Europe's strong biobanking infrastructure are helping to validate new antiseizure drugs and speed up the development of biomarkers. Timely intervention with neuromodulation or targeted pharmaceuticals is made possible by the early detection of drug-resistant patients using prediction algorithms. Collaboration between academic institutions, speciality epilepsy clinics, and life-science innovators promises more precise prognoses, earlier diagnoses, and optimised treatment pathways as precision neurology networks spread throughout Western, Central, and Eastern Europe. This will ultimately improve patient outcomes and drive cost-effective care.

Market Introduction

The market for refractory epilepsy treatments in Europe is rapidly changing as medical professionals and healthcare systems shift towards more individualised, technologically driven care for individuals whose seizures are still uncontrollable with first-line treatments. The market, which includes advanced pharmaceuticals, neuromodulation devices, and emerging biologics, is characterised by drug-resistant cases, which affect approximately 30% of the estimated 6 million individuals with epilepsy on the continent. Investment in innovative treatments and diagnostic tools that facilitate earlier detection and intervention is being driven by growing awareness of the significant clinical and financial burden of refractory epilepsy.

Next-generation antiseizure drugs (like cannabidiol-based adjuncts and novel molecular entities) and neuromodulation technologies (like deep brain stimulation (DBS), vagus nerve stimulation (VNS), and responsive neurostimulation (RNS)) that provide alternate methods of controlling seizures are important market segments. While strict EU Medical Device Regulation (MDR) and EMA oversight guarantee high levels of safety and efficacy, adoption is being aided by Western Europe's favourable reimbursement environment and Central and Eastern Europe's growing healthcare spending.

Molecular diagnostics, AI-powered predictive algorithms, and genomic profiling are some of the technological advancements that are enabling precision treatment paths, decreasing trial-and-error prescribing, and increasing patient outcomes. However, obstacles still exist: a lack of specialised epilepsy centres, high therapeutic costs, and unequal access across regions impede expansion. However, cooperation between clinical experts, biopharma firms, and academic research networks is creating the foundation for more focused, successful interventions and making the treatment of refractory epilepsy a crucial area of attention within the larger neurology industry in Europe.

Market Segmentation:

Segmentation 1: By Region

- Europe

- Germany

- U.K.

- France

- Italy

- Spain

- Rest-of-Europe

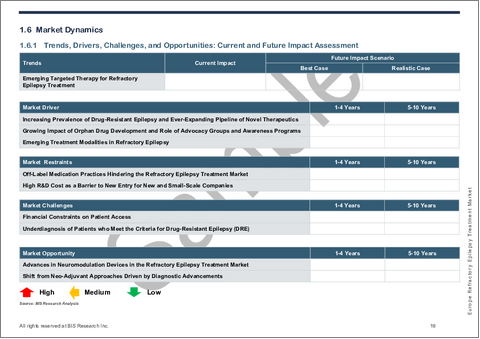

Europe Refractory Epilepsy Treatment Market Trends, Drivers and Challenges

Trends

- Rising uptake of neuromodulation therapies (Vagus Nerve Stimulation, Responsive Neurostimulation, Deep Brain Stimulation) alongside pharmacologic options

- Growth in cannabidiol (CBD)-based and other novel adjunctive medications following EU approvals

- Expansion of precision medicine approaches, including genetic profiling to tailor treatment regimens

- Increased use of tele-health and remote monitoring platforms for treatment adherence and seizure tracking

Drivers

- Persistent unmet need: ~30% of epilepsy patients remain drug-resistant despite multiple AED trials

- Strong R&D pipeline and strategic partnerships between pharma and device manufacturers

- Supportive reimbursement frameworks and increasing healthcare budgets in many European countries

- Patient advocacy and greater disease awareness driving early specialist referrals

Challenges

- High cost of advanced therapies and unequal access across Western versus Eastern Europe

- Complex regulatory environment for novel biologics and devices under EU MDR

- Limited number of specialized epilepsy centers and trained multidisciplinary teams

- Variability in national treatment guidelines and slow adoption of cutting-edge options in some markets

How can this report add value to an organization?

Product/Innovation Strategy: The report offers in-depth insights into the latest technological advancements in refractory epilepsy treatment, enabling organizations to drive innovation and develop cutting-edge products tailored to market needs.

Growth/Marketing Strategy: By providing comprehensive market analysis and identifying key growth opportunities, the report equips organizations with the knowledge to craft targeted marketing strategies and expand their market presence effectively.

Competitive Strategy: The report includes a thorough competitive landscape analysis, helping organizations understand their competitors' strengths and weaknesses and allowing them to strategize effectively to gain a competitive edge in the market.

Regulatory and Compliance Strategy: It provides updates on evolving regulatory frameworks, approvals, and industry guidelines, ensuring organizations stay compliant and accelerate market entry for new Refractory Epilepsy Treatment solutions.

Investment and Business Expansion Strategy: By analyzing market trends, funding patterns, and partnership opportunities, the report assists organizations in making informed investment decisions and identifying potential M&A opportunities for business growth.

Key Market Players and Competition Synopsis

Profiled companies have been selected based on inputs gathered from primary experts, as well as analyzing company coverage, product portfolio, and market penetration.

Some prominent names established in this market are:

- UCB S.A.

- Novartis AG

- LivaNova PLC

- GSK plc.

- Biocodex-SP

Table of Contents

Executive Summary

Scope and Definition

1 Market: Industry Outlook

- 1.1 Major Trend

- 1.2 Trend in Refractory Epilepsy Treatment Market

- 1.2.1 Emerging Targeted Therapy for Refractory Epilepsy Treatment

- 1.2.2 Business Strategies

- 1.2.2.1 Product Developments

- 1.2.2.2 Market Developments

- 1.2.3 Corporate Strategies

- 1.2.3.1 Partnerships and Joint Ventures

- 1.2.4 Market Opportunities

- 1.2.4.1 Advances in Neuromodulation Devices in the Refractory Epilepsy Treatment Market

- 1.2.4.2 Shift from Neo-Adjuvant Approaches Driven by Diagnostic Advancements

- 1.3 Start-Ups Landscape

- 1.3.1 Key Start-Ups in the Ecosystem

- 1.4 Pipeline Drugs, Refractory Epilepsy Treatment

- 1.5 Trends

- 1.5.1 Emerging Targeted Therapy for Refractory Epilepsy Treatment

- 1.6 Market Dynamics

- 1.6.1 Trends, Drivers, Challenges, and Opportunities: Current and Future Impact Assessment

- 1.6.2 Market Drivers

- 1.6.2.1 Increasing Prevalence of Drug-resistant Epilepsy and Ever-expanding Pipeline of Novel Therapeutics

- 1.6.2.2 Growing Impact of Orphan Drug Development and Role of Advocacy Groups and Awareness Programs

- 1.6.2.3 Emerging Treatment Modalities in Refractory Epilepsy

- 1.6.3 Market Restraints

- 1.6.3.1 Off-Label Medication Practices Hindering the Refractory Epilepsy Treatment Market

- 1.6.3.2 High R&D Cost as a Barrier to New Entry for New and Small-Scale Companies

- 1.6.4 Market Opportunities

- 1.6.4.1 Advances in Neuromodulation Devices in the Refractory Epilepsy Treatment Market

- 1.6.4.2 Shift from Neo-Adjuvant Approaches Driven by Diagnostic Advancements

- 1.6.5 Market Challenges

- 1.6.5.1 Financial Constraints on Patient Access

- 1.6.5.2 Underdiagnosis of Patients who Meet the Criteria for Drug-Resistant Epilepsy (DRE)

2 Region

- 2.1 Regional Summary

- 2.2 Europe

- 2.2.1 Regional Overview

- 2.2.2 Driving Factors for Market Growth

- 2.2.3 Factors Challenging the Market

- 2.2.4 Germany

- 2.2.5 France

- 2.2.6 Italy

- 2.2.7 Spain

- 2.2.8 U.K.

- 2.2.9 Rest-of-Europe

3 Markets - Competitive Benchmarking & Company Profiles

- 3.1 Biocodex-SP

- 3.1.1 Overview

- 3.1.2 Top Products/Product Portfolio

- 3.1.3 Top Competitors

- 3.1.4 Target Customers

- 3.1.5 Strategic Positioning and Market Impact

- 3.1.6 Analyst View

- 3.1.7 Pipeline and Research Initiatives

- 3.2 GSK plc.

- 3.2.1 Overview

- 3.2.2 Top Products/Product Portfolio

- 3.2.3 Top Competitors

- 3.2.4 Target Customers

- 3.2.5 Strategic Positioning and Market Impact

- 3.2.6 Analyst View

- 3.2.7 Research Initiatives

- 3.3 LivaNova PLC

- 3.3.1 Overview

- 3.3.2 Top Products/Product Portfolio

- 3.3.3 Top Competitors

- 3.3.4 Target Customers

- 3.3.5 Strategic Positioning and Market Impact

- 3.3.6 Analyst View

- 3.3.7 Research Initiatives

- 3.4 Novartis AG

- 3.4.1 Overview

- 3.4.2 Top Products/Product Portfolio

- 3.4.3 Top Competitors

- 3.4.4 Target Customers

- 3.4.5 Strategic Positioning and Market Impact

- 3.4.6 Analyst View

- 3.4.7 Pipeline and Research Initiatives

- 3.5 UCB S.A.

- 3.5.1 Overview

- 3.5.2 Top Products/Product Portfolio

- 3.5.3 Top Competitors

- 3.5.4 Target Customers

- 3.5.5 Strategic Positioning and Market Impact

- 3.5.6 Analyst View

- 3.5.7 Pipeline and Research Initiative

4 Research Methodology

- 4.1 Data Sources

- 4.1.1 Primary Data Sources

- 4.1.2 Secondary Data Sources

- 4.1.3 Inclusion and Exclusion

- 4.1.4 Data Triangulation

- 4.2 Market Estimation and Forecast