てんかん治療薬市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Epilepsy Treatment Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766369

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

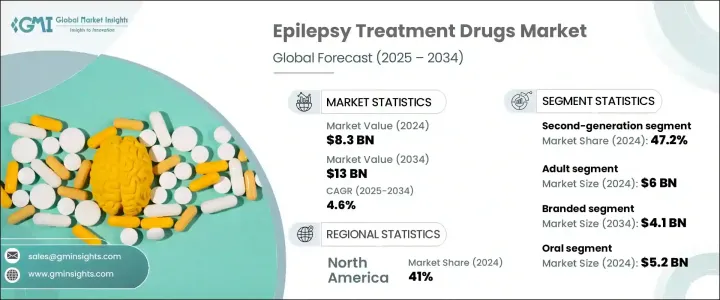

てんかん治療薬の世界市場規模は、2024年に83億米ドルとなり、CAGR 4.6%で成長し、2034年には130億米ドルに達すると推定されます。

てんかんの診断件数が世界的に着実に増加していることが、より効果的で利用しやすい治療オプションに対する需要を促進している主な要因の1つです。医薬品の技術革新、副作用の少ない新時代の抗てんかん薬の開発、治療アドヒアランスの向上などが、この増加傾向を支えています。神経学関連研究への政府・民間投資の増加、認知度の向上、検診率の上昇も市場拡大に寄与しています。

また、神経疾患に対してより脆弱な世界の高齢化人口の増加も、てんかん治療薬の需要をさらに高めると予想されます。医薬品開発企業は、より優れた忍容性、徐放性、患者のコンプライアンス向上を実現する治療薬を優先しています。このシフトは、新興国におけるヘルスケアインフラの改善や、主要市場における規制の合理化と相まって、イノベーションと製品採用に有利な環境を生み出しています。さらに、特に薬剤耐性てんかんに対する個別化医療戦略への移行は、治療成績を向上させ、長期的な市場成長の原動力となっています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 83億米ドル |

| 予測金額 | 130億米ドル |

| CAGR | 4.6% |

抗てんかん薬(AED)は抗けいれん薬とも呼ばれ、脳内の不規則な電気信号を安定させることで発作を予防し、てんかんの症状全般を改善します。薬剤クラス別に、市場は第一世代、第二世代、第三世代に分けられます。2024年には、第2世代AEDが世界市場の47.2%を占め、最大の売上シェアを占めています。このセグメントは2025年から2034年にかけてCAGR 4.6%で拡大すると予測されています。AEDが広く受け入れられている背景には、旧世代の治療薬に比べて薬物相互作用の発生率が低いこと、副作用プロファイルが改善されていること、患者のアドヒアランスが向上していることなどがあります。

製品タイプ別では、市場はブランド医薬品とジェネリック医薬品に分類されます。ブランド医薬品は2024年に26億米ドルを生み出し、2034年には41億米ドルに達すると予測されています。製薬会社は、薬物動態が改善され、副作用が少なく、治療効果が高いブランド治療薬の製造にますます力を入れるようになっています。特に従来の治療に反応しない患者の間で、新規治療に対するニーズが高まっていることも、ブランド抗てんかん薬の需要を押し上げています。

投与経路を分析すると、2024年には経口剤が52億米ドルを占め、最大のシェアを占めています。このセグメントは予測期間中にCAGR 4.9%で成長すると予測されています。経口剤は、その利便性、使いやすさ、投与スケジュールと患者の服薬アドヒアランスを向上させる徐放性製剤の導入などにより、好まれています。また、多様な経口製剤が入手可能であることも、先進国市場と新興国市場の両方での採用を加速させています。

市場は患者の属性に基づき、成人集団と小児集団に区分されます。2024年の市場規模は60億米ドルで成人がリードしており、2034年までCAGR 4.5%で拡大すると予測されています。成人におけるてんかん発症率の増加は、脳卒中、脳損傷、変性疾患などの加齢に関連した神経疾患と関連しています。その結果、信頼性が高く的を絞った治療アプローチに対する需要が高まっており、発作制御を改善するための多剤併用レジメンや長期療法が重視されるようになっています。

発作タイプによって、市場は焦点発作、全般発作、複合発作に区分されます。全般発作分野は2024年に25億米ドルを生み出し、2034年には40億米ドルに達すると推定されています。強直間代発作や欠神発作を含む全般発作の症例数が増加しており、より強固な治療ソリューションの必要性が高まっています。この動向は、神経学的研究のための政府資金の拡大、保険適用範囲の拡大、てんかん治療へのアクセス強化を目的とした政策イニシアチブによって支えられています。

販売チャネルでは、病院薬局、小売薬局、オンライン薬局が主要なセグメントです。小売薬局は2024年に23億米ドルの収益を獲得し、予測期間中にCAGR 4.9%を記録すると予想されています。特に低・中所得国において、費用対効果の高いジェネリック医薬品が小売の場で入手可能になりつつあり、てんかん患者がより手頃な価格でてんかんを管理できるようになっています。さらに、保険適用や補助金制度により、患者が小売店を通じて必要な医薬品を入手しやすくなっています。

地域別では、北米が2024年のシェア41%で世界のてんかん治療薬市場を牽引しました。米国は、高い認知度、整備されたヘルスケアシステム、高度な神経学的治療への患者アクセスを改善するための一貫した取り組みにより、同年の売上高に31億米ドルを貢献しました。米国市場は前年比着実な成長を示しており、2021年の28億米ドルから2023年には30億米ドル、2024年には31億米ドルに達します。同地域におけるてんかんの有病率の増加は、有利な規制条件や世界の製薬企業の存在と相まって、市場開拓を後押しし続けています。

業界の大手企業は、患者の転帰を改善し、ヘルスケアシステムにおけるてんかんの全体的な負担を軽減することを目指し、先進的な製剤や併用療法に積極的に投資しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- てんかんの有病率の上昇

- 研究開発活動への投資の増加

- てんかんの新しい治療への需要の高まり

- 意識の高まりと早期診断

- 業界の潜在的リスク&課題

- 抗てんかん薬に伴う副作用

- 特許の有効期限

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 米国[食品医薬品局(FDA)]

- カナダ(カナダ保健省規制)

- 欧州

- アジア太平洋地域

- 日本(PMDA)

- 中国(NMPA)

- インド(CDSCO)

- オーストラリア(TGA)

- 北米

- パイプライン分析

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:薬剤クラス別、2021年~2034年

- 主要動向

- 第一世代

- 第二世代

- 第三世代

第6章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- ブランド

- ジェネリック医薬品

第7章 市場推計・予測:投与経路別、2021年~2034年

- 主要動向

- 経口

- 鼻腔

- 注射

- 直腸

第8章 市場推計・予測:年齢別、2021年~2034年

- 主要動向

- 小児

- 成人

第9章 市場推計・予測:発作タイプ別、2021年~2034年

- 主要動向

- 局所発作

- 全身発作

- 複合発作

第10章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 病院薬局

- 小売薬局

- オンライン薬局

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- AbbVie

- Bausch Health Companies

- Dr. Reddy’s Laboratories

- Eisai

- GSK

- Jazz Pharmaceuticals

- Lupin Pharmaceuticals

- Neurelis

- Novartis

- Pfizer

- Sanofi

- SK Biopharmaceuticals

- Sumitomo Pharma

- Sun Pharmaceutical Industries

- UCB

目次

The Global Epilepsy Treatment Drugs Market was valued at USD 8.3 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 13 billion by 2034. The steady rise in epilepsy diagnoses globally is one of the key factors driving demand for more effective and accessible treatment options. Pharmaceutical innovations, the development of new-age anti-epileptic drugs with fewer side effects, and enhanced treatment adherence are all supporting this upward trend. Growing government and private investments in neurology-related research, alongside increasing awareness and screening rates, are contributing to the expanding market.

The rising global aging population-more vulnerable to neurological disorders-is also expected to further elevate the demand for epilepsy medications. Drug developers are prioritizing therapies that offer better tolerability, sustained release, and improved patient compliance. This shift, paired with improved healthcare infrastructure in developing nations and streamlined regulatory pathways in key markets, is creating a favorable environment for innovation and product adoption. Moreover, the transition toward more personalized medicine strategies, particularly for drug-resistant epilepsy, is improving treatment outcomes and driving long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.3 Billion |

| Forecast Value | $13 Billion |

| CAGR | 4.6% |

Anti-epileptic drugs (AEDs), also referred to as anticonvulsants, work by stabilizing irregular electrical signals in the brain, helping to prevent seizures and manage the overall symptoms of epilepsy. Based on drug class, the market is divided into first-generation, second-generation, and third-generation drugs. In 2024, second-generation AEDs accounted for the largest revenue share, contributing 47.2% to the global market. This segment is forecasted to expand at a CAGR of 4.6% from 2025 to 2034. Their broader acceptance is attributed to lower incidences of drug interactions, improved side effect profiles, and better patient adherence compared to older-generation therapies.

In terms of product type, the market is categorized into branded and generic drugs. Branded drugs generated USD 2.6 billion in 2024 and are projected to reach USD 4.1 billion by 2034. Pharmaceutical firms are increasingly focusing on producing branded treatments with improved pharmacokinetics, fewer adverse reactions, and greater therapeutic benefits. The rising need for novel treatments, especially among individuals who do not respond to conventional therapies, is also driving the demand for branded anti-epileptic medications.

When analyzing the route of administration, oral formulations held the largest share in 2024, accounting for USD 5.2 billion. This segment is projected to grow at a CAGR of 4.9% over the forecast period. Oral medications are preferred due to their convenience, ease of use, and the introduction of extended-release versions that improve dosage scheduling and patient adherence. The availability of diverse oral formulations is also accelerating adoption in both developed and emerging markets.

Based on patient demographics, the market is segmented into adult and pediatric populations. The adult segment led with a market value of USD 6 billion in 2024 and is expected to expand at a CAGR of 4.5% through 2034. The increasing incidence of epilepsy among adults is linked to age-related neurological conditions such as strokes, brain injuries, and degenerative disorders. As a result, the demand for reliable and targeted treatment approaches is rising, with a growing emphasis on multi-drug regimens and long-term therapy for improved seizure control.

According to seizure type, the market is segmented into focal seizures, generalized seizures, and combined seizures. The generalized seizure segment generated USD 2.5 billion in 2024 and is estimated to reach USD 4 billion by 2034. A rising number of generalized seizure cases, including tonic-clonic and absence seizures, is prompting the need for more robust therapeutic solutions. This trend is being supported by greater government funding for neurological research, insurance coverage expansions, and policy initiatives aimed at enhancing access to epilepsy care.

In terms of distribution channels, hospital pharmacies, retail pharmacies, and online pharmacies are the major segments. Retail pharmacies captured USD 2.3 billion in revenue in 2024 and are expected to register a CAGR of 4.9% during the forecast period. The growing availability of cost-effective generic drugs in retail settings, especially in low- and middle-income countries, is helping patients manage epilepsy more affordably. Additionally, insurance coverage and subsidy programs are making it easier for patients to access essential medications via retail outlets.

Regionally, North America led the global epilepsy treatment drugs market with a 41% share in 2024. The U.S. alone contributed USD 3.1 billion in revenue that year, driven by high awareness, well-developed healthcare systems, and consistent efforts to improve patient access to advanced neurological treatments. The U.S. market has shown steady year-on-year growth, moving from USD 2.8 billion in 2021 to USD 3 billion in 2023 and reaching USD 3.1 billion in 2024. The increasing prevalence of epilepsy in the region, coupled with favorable regulatory conditions and the presence of global pharmaceutical leaders, continues to push market development.

Major industry players are actively investing in advanced formulations and combination therapies, aiming to enhance patient outcomes and reduce the overall burden of epilepsy on healthcare systems.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Drug class

- 2.2.2 Type

- 2.2.3 Route of administration

- 2.2.4 Age group

- 2.2.5 Seizure type

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of epilepsy

- 3.2.1.2 Increasing investments in research and development activities

- 3.2.1.3 Increasing demand for novel treatment for epilepsy

- 3.2.1.4 Growing awareness and early diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Adverse effects associated with the antiepileptic drugs

- 3.2.2.2 Patent expiration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. [Food and Drug Administration (FDA)]

- 3.4.1.2 Canada (Health Canada Regulation)

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan (PMDA)

- 3.4.3.2 China (NMPA)

- 3.4.3.3 India (CDSCO)

- 3.4.3.4 Australia (TGA)

- 3.4.1 North America

- 3.5 Pipeline analysis

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 First-generation

- 5.3 Second-generation

- 5.4 Third-generation

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Branded

- 6.3 Generics

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Nasal

- 7.4 Injectable

- 7.5 Rectal

Chapter 8 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pediatric

- 8.3 Adult

Chapter 9 Market Estimates and Forecast, By Seizure Type, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Focal seizure

- 9.3 Generalized seizure

- 9.4 Combined seizure

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Hospital pharmacies

- 10.3 Retail pharmacies

- 10.4 Online pharmacies

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 AbbVie

- 12.2 Bausch Health Companies

- 12.3 Dr. Reddy’s Laboratories

- 12.4 Eisai

- 12.5 GSK

- 12.6 Jazz Pharmaceuticals

- 12.7 Lupin Pharmaceuticals

- 12.8 Neurelis

- 12.9 Novartis

- 12.10 Pfizer

- 12.11 Sanofi

- 12.12 SK Biopharmaceuticals

- 12.13 Sumitomo Pharma

- 12.14 Sun Pharmaceutical Industries

- 12.15 UCB

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日