|

|

市場調査レポート

商品コード

1532312

ソフトウェア定義型自動車市場- 世界および地域別分析:用途別、SDVタイプ別、E/Eアーキテクチャ別、車両タイプ別、車両自律性別、オファリング別、地域別 - 分析と予測(2024年~2034年)Software Defined Vehicle Market - A Global and Regional Analysis: Focus on Application, SDV Type, E/E Architecture, Vehicle Type, Vehicle Autonomy, Offering, and Region - Analysis and Forecast, 2024-2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ソフトウェア定義型自動車市場- 世界および地域別分析:用途別、SDVタイプ別、E/Eアーキテクチャ別、車両タイプ別、車両自律性別、オファリング別、地域別 - 分析と予測(2024年~2034年) |

|

出版日: 2024年08月13日

発行: BIS Research

ページ情報: 英文 100 Pages

納期: 1~5営業日

|

全表示

- 概要

- 目次

ソフトウェア定義型自動車の市場規模は、様々な市場促進要因に後押しされ、著しい成長を遂げています。

楽観的シナリオでは、2024年の市場規模は3,448億米ドルと評価され、CAGR 17.82%で拡大し、2034年には1兆7,767億米ドルに達すると予測されています。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2024年~2034年 |

| 2024年の評価額 | 3,448億米ドル |

| 2034年の予測 | 1兆7,767億米ドル |

| CAGR | 17.82% |

ソフトウェア定義型自動車(SDV:Software-Defined Vehicle)分野の台頭により、自動車業界は革命的な変化を遂げつつあります。今や、ハードウェアだけでなくソフトウェアが自動車を制御し、定義しています。このパラダイムの変化により、より柔軟で頻繁な更新が可能になり、遠隔操作による機能向上も可能になっています。SDVは、モノのインターネット(IoT)、機械学習(ML)、人工知能(AI)などの最先端技術を利用して、より安全で賢く、効率的な車両を実現します。OTA(Over-the-Air)アップグレードや機能拡張を通じて、メーカーはハードウェアとソフトウェア開発のサイクルを切り離すことができ、より迅速なイノベーションとより優れた消費者体験を実現できます。これは、SDVの考え方によって可能になります。

SDV市場の急速な拡大には、数多くの変数が寄与しています。主な原動力の1つは、複雑なソフトウェアシステムに依存するコネクテッドカーや自律走行車に対するニーズの高まりです。SDVの採用は、インフォテインメント、安全性、利便性の向上に対する消費者の期待の高まりによってさらに促進されています。さらに、電気自動車(EV)を選ぶ人が増えるにつれて、バッテリーの性能、エネルギー効率、統合充電ソリューションを制御するための高度なソフトウェアに対する需要が高まっています。もう1つの重要な問題は、自動車業界において、ソフトウェアとデジタルサービスが提供価値の中心となる、サービス指向アーキテクチャへの移行が進んでいることです。クラウドコンピューティング、人工知能、強力なサイバーセキュリティフレームワークの革新は、この移行を可能にし、安全で信頼性の高い車両運用を保証します。

SDV市場は、北米と欧州で最も速いペースで成長しています。これは、大規模な自動車メーカーとITビジネスが存在し、強固な技術エコシステムがあり、自動車の研究開発に多額の投資が行われているためです。北米、特に米国が市場をリードしているのは、自律走行車の市場開拓における革新的な役割、多額のベンチャーキャピタルからの資金調達、有利な規制の枠組みがあるためです。欧州はそのすぐ後塵を拝しており、英国やドイツなどの国々がコネクテッドカーや電気自動車のプログラムをリードしています。これらの地域の成長は、老舗の自動車大手の存在、厳しい排出基準、持続可能性の重視によってさらに加速しています。

当レポートでは、世界のソフトウェア定義型自動車市場について調査し、市場の概要とともに、用途別、SDVタイプ別、E/Eアーキテクチャ別、車両タイプ別、車両自律性別、オファリング別、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

第1章 市場:業界の展望

- 動向:現在および将来の影響評価

- サプライチェーンの概要

- R&Dレビュー

- 規制状況

- ステークホルダー分析

- 主要な世界的イベントの影響分析

- 市場力学の概要

第2章 ソフトウェア定義型自動車市場(用途別)

- 用途のセグメンテーション

- 用途の概要

- ソフトウェア定義型自動車市場(SDVタイプ別)

- ソフトウェア定義型自動車市場(用途別)

第3章 ソフトウェア定義型自動車市場(製品別)

- 製品セグメンテーション

- 製品概要

- ソフトウェア定義型自動車市場(車両タイプ別)

- ソフトウェア定義型自動車市場(車両自律性別)

- ソフトウェア定義型自動車市場(E/Eアーキテクチャ別)

- ソフトウェア定義型自動車市場(オファリング別)

第4章 ソフトウェア定義型自動車市場(地域別)

- ソフトウェア定義型自動車市場(地域別)

- 北米

- 欧州

- アジア太平洋

- その他の地域

第5章 企業プロファイル

- 今後の見通し

- 地理的評価

- 企業プロファイル

- Aptiv PLC

- Audi AG

- BMW Group

- Tesla

- Robert Bosch GmbH

- NVIDIA Corporation

- Qualcomm Technologies Inc.

- Marelli Holdings Co., Ltd.

- Continental AG

- Volkswagen Ag

- General Motors Company

- Stellantis NV

- BYD Company Limited

- Hyundai Motor Company

- Mercedes Benz Group AG

- その他

第6章 調査手法

Introduction to Software-Defined Vehicle Market

The software-defined vehicle market is undergoing significant growth, which is propelled by various key factors and market drivers. In an optimistic scenario, the market is evaluated at a valuation of $344.8 billion in 2024 and is projected to expand at a CAGR of 17.82% to reach $1,776.7 billion by 2034.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2024 - 2034 |

| 2024 Evaluation | $344.8 Billion |

| 2034 Forecast | $1,776.7 Billion |

| CAGR | 17.82% |

The automotive industry is undergoing a revolutionary change with the rise of the software-defined vehicle (SDV) sector. Software, rather than only hardware, is now controlling and defining vehicles. This paradigm change makes more flexibility, frequent updates, and improved functions that may be controlled remotely possible. SDVs use cutting-edge technology such as the Internet of Things (IoT), machine learning (ML), and artificial intelligence (AI) to create vehicles that are safer, smarter, and more efficient. Through over-the-air (OTA) upgrades and feature enhancements, manufacturers may decouple the cycles of hardware and software development, resulting in faster innovation and better consumer experiences. This is made possible by the SDV idea.

Numerous variables contribute to the SDV market's rapid expansion. One of the main drivers is the growing need for connected and autonomous cars, which depend on complex software systems to operate. The adoption of SDVs is further driven by consumers' increasing expectations for improved infotainment, safety, and convenience features. Additionally, as more people choose electric cars (EVs), the demand for sophisticated software to control battery performance, energy efficiency, and integrated charging solutions increases. Another important issue is the movement in the automotive industry toward a service-oriented architecture, where software and digital services are central to the value offered. Innovations in cloud computing, artificial intelligence, and strong cybersecurity frameworks make this transition possible and guarantee safe and dependable vehicle operations.

The SDV market has grown at the fastest rate in North America and Europe due to the presence of significant automotive manufacturers and IT businesses, robust technical ecosystems, and significant investments in automotive R&D. The market is led by North America, especially the U.S. because of its innovative role in the development of autonomous vehicles, significant venture capital funding, and advantageous regulatory framework. Europe is right behind, with nations such as the U.K. and Germany leading the way in connected and electric car programs. These regions' growth is further accelerated by the existence of well-established automotive titans, strict emission standards, and a strong emphasis on sustainability.

Furthermore, government programs are essential for supporting the SDV market. The expansion of the market in the U.S. is largely dependent on federal and state regulations that support electric and driverless vehicles as well as large financing for smart infrastructure initiatives. The European Union incentivizes car manufacturers to incorporate SDV technologies into their vehicles through its strict CO2 emission rules and extensive smart mobility policies, such as the European Green Deal. Aiming to dominate the electric and autonomous car sectors in Asia-Pacific, China's government is investing heavily in 5G infrastructure to facilitate vehicle-to-everything (V2X) connectivity, as well as providing large subsidies and tax breaks.

In conclusion, the software-defined vehicles (SDVs) market is poised for substantial growth and transformation in the coming years as the global automotive industry shifts toward digitalization and connectivity. With increasing consumer demand for advanced features, rapid technological advancements, and supportive government policies driving the adoption of SDVs, the demand for sophisticated software and integrated vehicle platforms is expected to soar, presenting unprecedented opportunities for stakeholders in the automotive ecosystem. As the automotive industry embraces software-defined vehicles as the future of transportation, the SDV market stands at the forefront of innovation, poised to redefine the driving experience. Together with fostering innovation, these government initiatives hasten the rollout of SDVs and ensure that regulatory frameworks keep pace with technological breakthroughs.

Market Segmentation:

Segmentation 1: by Application

- Powertrain Control

- Advanced Driver-Assistance Systems (ADAS)

- Autonomous Driving

- Infotainment and Connectivity

- Telematics

- Vehicle Management

- Others

Segmentation 2: by SDV Type

- SDV

- Semi-SDV

Segmentation 3: by Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

Segmentation 4: by Vehicle Autonomy

- Level 1

- Level 2

- Level 3

- Level 4

- Level 5

Segmentation 5: by E/E Architecture

- Distributed Architecture

- Domain Centralized Architecture

- Zonal Control Architecture

Segmentation 6: by Offering

- Software

- Hardware

- Services

Segmentation 7: by Region

- North America

- Europe

- Asia-Pacific

- Rest-of-the-World

How can this report add value to an organization?

Product/Innovation Strategy: The global software defined vehicle market has been extensively segmented based on various categories, such as application, SDV type, vehicle type, vehicle autonomy, and offering. This can help readers get a clear overview of which segments account for the largest share and which ones are well-positioned to grow in the coming years.

Competitive Strategy: A detailed competitive benchmarking of the players operating in the global software defined vehicle market has been done to help the reader understand how players stack against each other, presenting a clear market landscape. Additionally, comprehensive competitive strategies such as partnerships, agreements, and collaborations will aid the reader in understanding the untapped revenue pockets in the market.

Key Market Players and Competition Synopsis

The companies that are profiled have been selected based on thorough secondary research, which includes analyzing company coverage, product portfolio, market penetration, and insights gathered from primary experts.

Some of the prominent companies in this market are:

- Aptiv PLC

- Tesla

- Robert Bosch GmbH

- Qualcomm Technologies Inc.

- Continental AG

Key Questions Answered in this Report:

- What are the main factors driving the demand for software-defined vehicles?

- What are the major patents filed by the companies active in the global software-defined vehicle market?

- Which are the key players in the global software-defined vehicle market, and what are their respective market shares?

- What are the strategies adopted by the key companies to gain a competitive edge in the global software-defined vehicle market?

- What is the futuristic outlook for the global software-defined vehicle market in terms of growth potential?

- What is the current estimation of the global software-defined vehicle market, and what growth trajectory is projected from 2024 to 2034?

- Which application and product segments are expected to lead the market over the forecast period 2024-2034?

- Which regions demonstrate the highest adoption rates for the global software-defined vehicle market, and what factors contribute to their leadership?

Table of Contents

Executive Summary

Scope and Definition

Market/Product Definition

Key Questions Answered

Analysis and Forecast Note

1. Markets: Industry Outlook

- 1.1 Trends: Current and Future Impact Assessment

- 1.2 Supply Chain Overview

- 1.2.1 Value Chain Analysis

- 1.2.2 Pricing Forecast

- 1.3 R&D Review

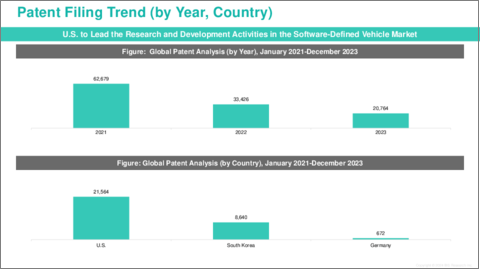

- 1.3.1 Patent Filing Trend by Country, by Company

- 1.4 Regulatory Landscape

- 1.5 Stakeholder Analysis

- 1.5.1 Use Case

- 1.5.2 End User and Buying Criteria

- 1.6 Impact Analysis for Key Global Events

- 1.7 Market Dynamics Overview

- 1.7.1 Market Drivers

- 1.7.2 Market Restraints

- 1.7.3 Market Opportunities

2. Software Defined Vehicle Market (by Application)

- 2.1 Application Segmentation

- 2.2 Application Summary

- 2.3 Software Defined Vehicle Market (by SDV Type)

- 2.3.1 SDV

- 2.3.2 Semi-SDV

- 2.4 Software Defined Vehicle Market (by Application)

- 2.4.1 Autonomous Driving

- 2.4.2 Infotainment and Connectivity

- 2.4.3 Vehicle Management

- 2.4.4 Advanced Driver-Assistance Systems (ADAS)

- 2.4.5 Telematics

- 2.4.6 Powertrain Control

- 2.4.7 Others

3. Software Defined Vehicle Market (by Product)

- 3.1 Product Segmentation

- 3.2 Product Summary

- 3.3 Software Defined Vehicle Market (by Vehicle Type)

- 3.3.1 Passenger Vehicles

- 3.3.2 Commercial Vehicles

- 3.4 Software Defined Vehicle Market (by Vehicle Autonomy)

- 3.4.1 Level 1

- 3.4.2 Level 2

- 3.4.3 Level 3

- 3.4.4 Level 4

- 3.4.5 Level 5

- 3.5 Software Defined Vehicle Market (by E/E Architecture)

- 3.5.1 Distributed Architecture

- 3.5.2 Domain Centralized Architecture

- 3.5.3 Zonal Control Architecture

- 3.6 Software Defined Vehicle Market (by Offering)

- 3.6.1 Software

- 3.6.2 Hardware

- 3.6.3 Services

4. Software Defined Vehicle Market (by Region)

- 4.1 Software Defined Vehicle Market (by Region)

- 4.2 North America

- 4.2.1 Regional Overview

- 4.2.2 Driving Factors for Market Growth

- 4.2.3 Factors Challenging the Market

- 4.2.4 Application

- 4.2.5 Product

- 4.2.6 U.S.

- 4.2.6.1 Market by Application

- 4.2.6.2 Market by Product

- 4.2.7 Canada

- 4.2.7.1 Market by Application

- 4.2.7.2 Market by Product

- 4.2.8 Mexico

- 4.2.8.1 Market by Application

- 4.2.8.2 Market by Product

- 4.3 Europe

- 4.3.1 Regional Overview

- 4.3.2 Driving Factors for Market Growth

- 4.3.3 Factors Challenging the Market

- 4.3.4 Application

- 4.3.5 Product

- 4.3.6 Germany

- 4.3.6.1 Market by Application

- 4.3.6.2 Market by Product

- 4.3.7 France

- 4.3.7.1 Market by Application

- 4.3.7.2 Market by Product

- 4.3.8 U.K.

- 4.3.8.1 Market by Application

- 4.3.8.2 Market by Product

- 4.3.9 Spain

- 4.3.9.1 Market by Application

- 4.3.9.2 Market by Product

- 4.3.10 Rest-of-Europe

- 4.3.10.1 Market by Application

- 4.3.10.2 Market by Product

- 4.4 Asia-Pacific

- 4.4.1 Regional Overview

- 4.4.2 Driving Factors for Market Growth

- 4.4.3 Factors Challenging the Market

- 4.4.4 Application

- 4.4.5 Product

- 4.4.6 China

- 4.4.6.1 Market by Application

- 4.4.6.2 Market by Product

- 4.4.7 Japan

- 4.4.7.1 Market by Application

- 4.4.7.2 Market by Product

- 4.4.8 South Korea

- 4.4.8.1 Market by Application

- 4.4.8.2 Market by Product

- 4.4.9 Rest-of-Asia-Pacific

- 4.4.9.1 Market by Application

- 4.4.9.2 Market by Product

- 4.5 Rest-of-the-World

- 4.5.1 Regional Overview

- 4.5.2 Driving Factors for Market Growth

- 4.5.3 Factors Challenging the Market

- 4.5.4 Application

- 4.5.5 Product

- 4.5.6 Middle East and Africa

- 4.5.6.1 Market by Application

- 4.5.6.2 Market by Product

- 4.5.7 South America

- 4.5.7.1 Market by Application

- 4.5.7.2 Market by Product

5. Companies Profiled

- 5.1 Next Frontiers

- 5.2 Geographic Assessment

- 5.3 Company Profiles

- 5.3.1 Aptiv PLC

- 5.3.1.1 Overview

- 5.3.1.2 Top Products/Product Portfolio

- 5.3.1.3 Top Competitors

- 5.3.1.4 Target Customers

- 5.3.1.5 Key Personnel

- 5.3.1.6 Analyst View

- 5.3.1.7 Market Share

- 5.3.2 Audi AG

- 5.3.2.1 Overview

- 5.3.2.2 Top Products/Product Portfolio

- 5.3.2.3 Top Competitors

- 5.3.2.4 Target Customers

- 5.3.2.5 Key Personnel

- 5.3.2.6 Analyst View

- 5.3.2.7 Market Share

- 5.3.3 BMW Group

- 5.3.3.1 Overview

- 5.3.3.2 Top Products/Product Portfolio

- 5.3.3.3 Top Competitors

- 5.3.3.4 Target Customers

- 5.3.3.5 Key Personnel

- 5.3.3.6 Analyst View

- 5.3.3.7 Market Share

- 5.3.4 Tesla

- 5.3.4.1 Overview

- 5.3.4.2 Top Products/Product Portfolio

- 5.3.4.3 Top Competitors

- 5.3.4.4 Target Customers

- 5.3.4.5 Key Personnel

- 5.3.4.6 Analyst View

- 5.3.4.7 Market Share

- 5.3.5 Robert Bosch GmbH

- 5.3.5.1 Overview

- 5.3.5.2 Top Products/Product Portfolio

- 5.3.5.3 Top Competitors

- 5.3.5.4 Target Customers

- 5.3.5.5 Key Personnel

- 5.3.5.6 Analyst View

- 5.3.5.7 Market Share

- 5.3.6 NVIDIA Corporation

- 5.3.6.1 Overview

- 5.3.6.2 Top Products/Product Portfolio

- 5.3.6.3 Top Competitors

- 5.3.6.4 Target Customers

- 5.3.6.5 Key Personnel

- 5.3.6.6 Analyst View

- 5.3.7.7 Market Share

- 5.3.7 Qualcomm Technologies Inc.

- 5.3.7.1 Overview

- 5.3.7.2 Top Products/Product Portfolio

- 5.3.7.3 Top Competitors

- 5.3.7.4 Target Customers

- 5.3.7.5 Key Personnel

- 5.3.7.6 Analyst View

- 5.3.7.7 Market Share

- 5.3.8 Marelli Holdings Co., Ltd.

- 5.3.8.1 Overview

- 5.3.8.2 Top Products/Product Portfolio

- 5.3.8.3 Top Competitors

- 5.3.8.4 Target Customers

- 5.3.1 Aptiv PLC

- 5.3.8..5 Key Personnel

- 5.3.8.6 Analyst View

- 5.3.8.7 Market Share

- 5.3.9 Continental AG

- 5.3.9.1 Overview

- 5.3.9.2 Top Products/Product Portfolio

- 5.3.9.3 Top Competitors

- 5.3.9.4 Target Customers

- 5.3.9.5 Key Personnel

- 5.3.9.6 Analyst View

- 5.3.9.7 Market Share

- 5.3.10 Volkswagen Ag

- 5.3.10.1 Overview

- 5.3.10.2 Top Products/Product Portfolio

- 5.3.10.3 Top Competitors

- 5.3.10.4 Target Customers

- 5.3.10.5 Key Personnel

- 5.3.10.6 Analyst View

- 5.3.10.7 Market Share

- 5.3.11 General Motors Company

- 5.3.11.1 Overview

- 5.3.11.2 Top Products/Product Portfolio

- 5.3.11.3 Top Competitors

- 5.3.11.4 Target Customers

- 5.3.11.5 Key Personnel

- 5.3.11.6 Analyst View

- 5.3.11.7 Market Share

- 5.3.12 Stellantis NV

- 5.3.12.1 Overview

- 5.3.12.2 Top Products/Product Portfolio

- 5.3.12.3 Top Competitors

- 5.3.12.4 Target Customers

- 5.3.12.5 Key Personnel

- 5.3.12.6 Analyst View

- 5.3.12.7 Market Share

- 5.3.13 BYD Company Limited

- 5.3.13.1 Overview

- 5.3.13.2 Top Products/Product Portfolio

- 5.3.13.3 Top Competitors

- 5.3.13.4 Target Customers

- 5.3.13.5 Key Personnel

- 5.3.13.6 Analyst View

- 5.3.13.7 Market Share

- 5.3.14 Hyundai Motor Company

- 5.3.14.1 Overview

- 5.3.14.2 Top Products/Product Portfolio

- 5.3.14.3 Top Competitors

- 5.3.14.4 Target Customers

- 5.3.14.5 Key Personnel

- 5.3.14.6 Analyst View

- 5.3.14.7 Market Share

- 5.3.15 Mercedes Benz Group AG

- 5.3.15.1 Overview

- 5.3.15.2 Top Products/Product Portfolio

- 5.3.15.3 Top Competitors

- 5.3.15.4 Target Customers

- 5.3.15.5 Key Personnel

- 5.3.15.6 Analyst View

- 5.3.15.7 Market Share

- 5.3.16 Other Key Players