|

|

市場調査レポート

商品コード

1445389

データセンター用冷媒市場 - 世界および地域の分析:製品・用途・サプライチェーン分析・国別分析・予測 (2023~2032年)Data Center Refrigerant Market - A Global and Regional Analysis: Focus on Product, Application, Supply-Chain Analysis, and Country Analysis - Analysis and Forecast, 2023-2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| データセンター用冷媒市場 - 世界および地域の分析:製品・用途・サプライチェーン分析・国別分析・予測 (2023~2032年) |

|

出版日: 2024年03月07日

発行: BIS Research

ページ情報: 英文 153 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

世界のデータセンター用冷媒の市場規模は、2022年の4億7,120万米ドルから、予測期間中は8.59%のCAGRで推移し、2032年には12億1,510万米ドルに成長すると予測されています。

世界のデータセンター用冷媒市場の成長は、データセンター数の増加とエネルギー効率の高いデータセンター運営に向けた政府の取り組みによって促進されると予測されています。また、政府の政策や財政支援により、データセンター施設内での環境に優しい冷媒の利用が奨励されています。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2023-2032年 |

| 2023年評価 | 5億3,320万米ドル |

| 2032年予測 | 12億1,510万米ドル |

| CAGR | 8.59% |

データセンター用冷媒市場のCAGRは8.59%であり、環境の持続可能性と運用効率の相乗効果が高まっていることを示しています。データセンターの世界での拡大が続く中、効率的な冷却ソリューションに対する需要が高まっています。冷媒はITインフラから熱を放散させ、最適な機能を維持する上で極めて重要な役割を果たしています。環境問題の高まりを受けて、地球温暖化やオゾン層破壊の可能性を低減した環境に優しい冷媒への移行が顕著になっています。

特に、ITや電気通信などの分野では、拡大するデジタルインフラをサポートするための堅牢で効率的な冷却ソリューションに対する需要の高まりに後押しされ、冷媒が幅広く使用されています。この成長により、最新施設の高密度コンピューティング環境に対応する高度な冷凍ソリューションの必要性が強調されています。

さらに、液体冷却が人気を得ています。液浸冷却や直接チップ冷却のような高度な冷却手法に不可欠な液冷は、エネルギー効率を高め、データセンターにおける環境への影響を最小限に抑えます。液体冷却の台頭は、持続可能性の目標に沿いつつ、運用上の要求を満たすソリューションに業界が傾倒していることを反映しています。

当レポートでは、世界のデータセンター用冷媒の市場を調査し、市場概要、市場影響因子の分析、市場規模の推移・予測、各種区分・地域別の詳細分析、競合情勢、主要企業の分析などをまとめています。

市場の分類

セグメンテーション1:産業別

- IT・電気通信

- 銀行

- 金融サービス・保険(BFSI)

- 研究・ヘルスケア

- 小売

- 製造

- その他

セグメンテーション2:データセンタータイプ別

- ハイパースケール

- コロケーション

- エッジデータセンター

- エンタープライズ

セグメンテーション3:冷媒タイプ別

- 従来型冷媒

- 液体冷却液

セグメンテーション4:冷却タイプ別

- 空冷

- 液冷

- フリークーリング

セグメンテーション5:展開別

- 設置/OEM

- アフターマーケット

セグメンテーション6:地域別

- 北米

- 欧州

- 英国

- 中国

- アジア太平洋および日本

- 南米

目次

エグゼクティブサマリー

第1章 市場

- 業界の展望

- 市場の定義

- データセンターの動向

- エコシステム/進行中のプログラム

- 事業力学

- 事業促進要因

- 事業上の課題

- 事業機会

- サプライチェーン分析

- 価格分析

第2章 用途別

- 業界

- データセンタータイプ

第3章 製品別

- 冷媒タイプ

- 従来型冷媒

- 液体冷却液

- 冷却タイプ

- 空冷

- 液冷

- フリークーリング

- 展開

- 取付・OEM

- アフターマーケット

第4章 地域

- 世界のデータセンターの展望

- 北米

- 欧州

- 英国

- 中国

- アジア太平洋と日本

- 南米

第5章 市場:競合ベンチマーキング・企業プロファイル

- 競合ベンチマーキング

- 企業プロファイル

- Honeywell International Inc.

- The Chemours Company

- Climalife

- Arkema

- Orbia

- DAIKIN INDUSTRIES, Ltd.

- Dow

- M&I Materials Ltd

- Asetek, Inc. A/S

- 3M

- Cargill, Incorporated

第6章 調査手法

List of Figures

- Figure 1: Properties of Hydrogen, Fluorine, and Chlorine Refrigerants

- Figure 2: Phase-Out Schedules for HCFCs and HFCs

- Figure 3: Global Data Center Refrigerant Market, $Million, 2022-2032

- Figure 4: Global Data Center Refrigerant Market (by Industry), $Million, 2022 and 2032

- Figure 5: Global Data Center Refrigerant Market (by Data Center Type), $Million, 2022 and 2032

- Figure 6: Global Data Center Refrigerant Market (by Refrigerant Type), $Million, 2022 and 2032

- Figure 7: Global Data Center Refrigerant Market (by Cooling Type), $Million, 2022 and 2032

- Figure 8: Global Data Center Refrigerant Market (by Deployment), $Million, 2022 and 2032

- Figure 9: Global Data Center Refrigerant Market (by Region), 2022

- Figure 10: Scope Definition

- Figure 11: Hyperscale Data Center Capacity (by Region), MW, 2021

- Figure 12: Data Center Capacity Outlook (by Region), MW, 2021

- Figure 13: Anticipated Energy Consumption, by Data Center Types, TWh, 2023

- Figure 14: Power Flows in a typical Data Center:

- Figure 15: Pathway to Carbon Neutrality in Data Centers

- Figure 16: Key Factors for Assessing Infrastructure Cost in a Data Center Project

- Figure 17: CAPEX Comparison: Traditional Data Centers (TDC) Vs Carbon Neutral Data Centers (CNDC)

- Figure 18: Key Factors for Assessing Energy Cost in Data Center Project

- Figure 19: OPEX Comparison: Traditional Data Centers (TDC) Vs Carbon Neutral Data Centers (CNDC):

- Figure 20: Major Countries' Share of Total Installed Renewable Capacity, 2021

- Figure 21: Global Trend in Industrial Refrigeration

- Figure 22: Estimated Capital Expense for Various Data Center Cooling Technologies

- Figure 23: Some Criteria Followed by Data Centers while Choosing Refrigerants

- Figure 24: GWP and ODP of Most Common Refrigerants in Data Centers

- Figure 25: Estimated Worldwide 5G Adoption as a Share of Total Mobile Connections (Excluding IoT)

- Figure 26: Share of Global Data Center (by Country), 2022

- Figure 27: Water Utility and Wastewater Cost Comparison in Data Centers, 2021

- Figure 28: Cooling Efficiency and Water Usage of Data Center Cooling Technologies

- Figure 29: Energy Distribution in a Typical Data Center, 2022

- Figure 30: Evolution of Refrigerants from 1830 and Future Anticipations

- Figure 31: Data Center Web Traffic, Zettabytes per Year, 2016-2021

- Figure 32: Data Center pPue Analysis

- Figure 33: Supply Chain Analysis of Global Data Center Refrigerant Market

- Figure 34: Competitive Benchmarking Matrix

- Figure 35: Global Data Center Refrigerant Market: Research Methodology

- Figure 36: Data Triangulation

- Figure 37: Top-Down and Bottom-Up Approach

- Figure 38: Assumptions and Limitations

List of Tables

- Table 1: Advantages and Disadvantages of Non-PFAS Refrigerants

- Table 2: Key Consortium/Association in Data Center Refrigerant Industry

- Table 3: Regulations Impacting the Data Center Refrigerant Market

- Table 4: Government Initiatives and Impacts

- Table 5: Recent Developments by Leading Companies toward Data Center Cooling, 2019-2023

- Table 6: Key Companies and Developments toward Neural Networks in Data Centers

- Table 7: Key Companies Exploring Indirect Thermosyphon Cooling

- Table 8: Data Center Refrigerant Pricing

- Table 9: Global Data Center Refrigerant Market (by Region), $Million, 2022-2032

- Table 10: Honeywell International Inc.: Product Portfolio

- Table 11: The Chemours Company: Product Portfolio

- Table 12: Climalife: Product Portfolio

- Table 13: Arkema: Product Portfolio

- Table 14: Orbia: Product Portfolio

- Table 15: DAIKIN INDUSTRIES, Ltd.: Product Portfolio

- Table 16: Dow: Product Portfolio

- Table 17: M&I Materials Ltd: Product Portfolio

- Table 18: Asetek, Inc. A/S: Product Portfolio

- Table 19: 3M: Product Portfolio

- Table 20: Cargill, Incorporated: Product Portfolio

The Global Data Center Refrigerant Market Expected to Reach $1,215.1 Million by 2032

Introduction to Global Data Center Refrigerant Market

The global data center refrigerant market is expected to grow from $471.2 million in 2022 to $1,215.1 million by 2032, at a CAGR of 8.59% during the forecast period 2023-2032. The growth of the global data center refrigerant market is anticipated to be fueled by the rising quantity of data centers and governmental efforts toward energy-efficient data center operations. Additionally, governmental policies and financial support encourage the utilization of environment-friendly refrigerants within data center facilities.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2023 - 2032 |

| 2023 Evaluation | $533.2 Million |

| 2032 Forecast | $1,215.1 Million |

| CAGR | 8.59% |

Market Introduction

Data center refrigerant market, with an impressive CAGR of 8.59%, demonstrates an increasing synergy between environmental sustainability and operational efficiency. Amidst the ongoing global expansion of data centers, there is a heightened demand for efficient cooling solutions. Refrigerants play a pivotal role in dissipating heat from IT infrastructure, thereby maintaining optimal functionality. In response to escalating environmental concerns, there is a notable transition towards eco-friendly refrigerants characterized by reduced global warming and ozone depletion potentials.

Notably, sectors such as IT and Telecom find extensive use of refrigerants, spurred by the escalating demand for robust and efficient cooling solutions to support the expanding digital infrastructure. This growth emphasizes the need for advanced refrigeration solutions that cater to the high-density computing environments of modern facilities.

Additionally, liquid cooling fluids are gaining traction. Integral to advanced cooling methodologies like immersion and direct-to-chip cooling, they enhance energy efficiency and minimize environmental impact in data centers. Their rising prominence reflects the industry's inclination towards solutions meeting operational demands while aligning with sustainability goals.

Adherence to government regulations, such as the Kigali Amendment to the Montreal Protocol, underscores the industry's sustainability commitment. This is crucial as organizations strive to reduce carbon footprints and optimize resource use. The transition to eco-friendly refrigerants and advanced cooling technology is pivotal, particularly in high-demand sectors like IT and Telecom, aligning with a broader move towards sustainability in modern data center operations.

Industry Impact

The industry impact of data center refrigerants is profound, influencing both environmental sustainability and operational efficiency. With the escalating number of data centers globally, the demand for efficient cooling systems is paramount. Refrigerants, crucial components in these systems, play a pivotal role in managing heat generated by critical IT infrastructure. As regulations tighten and environmental concerns escalate, there's a notable shift toward eco-friendly refrigerants with reduced global warming potential and ozone depletion potential. This transition from traditional to modern refrigerants reflects a commitment to mitigating environmental impact while optimizing energy usage. Furthermore, innovative cooling methodologies such as immersion and direct-to-chip cooling are gaining traction, promising enhanced energy efficiency and reduced carbon footprints. Thus, the industry's adoption of eco-friendly refrigerants underscores a strategic imperative toward sustainability and operational excellence in data center operations.

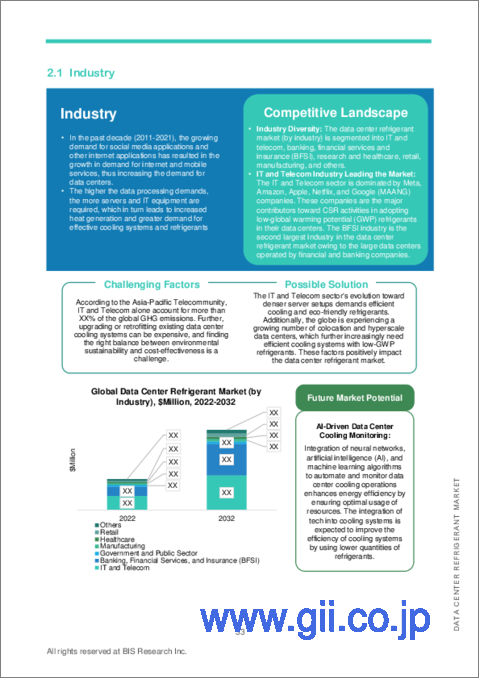

Market Segmentation:

Segmentation 1: by Industry

- IT and Telecom

- Banking

- Financial Services and Insurance (BFSI)

- Research and Healthcare

- Retail

- Manufacturing

- Others

IT and Telecom Segment to Lead the Global Data Center Refrigerant Market (by Industry)

In the IT and telecommunications sector, Meta, Amazon, Apple, Netflix, and Google (MAANG) corporations hold significant position. These entities stand out as primary participants in corporate social responsibility (CSR) endeavors, particularly in the adoption of refrigerants with low global warming potential (GWP) within their data centers. The Banking, Financial Services, and Insurance (BFSI) sector is quickly emerging as a significant force in the data center refrigerant market, ranking as the second largest. This is due to the extensive network of large data centers operated by banking and financial institutions.

Segmentation 2: by Data Center Type

- Hyperscale

- Colocation

- Edge Data Center

- Enterprise

Hyperscale Data Centers to Lead the Global Data Center Refrigerant Market (by Data Center Type)

Hyperscale data centers are at the forefront of transforming extensive data centers into environmentally sustainable entities. They are pioneering the exploration of eco-friendly cooling techniques, with carbon dioxide (CO2) emerging as a prominent refrigerant choice. In contrast, edge data centers strategically positioned near users to minimize data processing latency typically adhere to conventional cooling methodologies. The adoption of environment-friendly refrigerants varies and is influenced by factors such as facility size and operator preferences. With sustainability gaining prominence and regulatory measures becoming more stringent, there's a potential for edge data centers to transition toward refrigerants with lower global warming potential (GWP), aligning with prevailing industry trends.

Segmentation 3: by Refrigerant Type

- Conventional Refrigerants

- Liquid Cooling Fluids

Liquid Cooling Fluids to Lead the Global Data Center Refrigerant Market (by Refrigerant Type)

Liquid cooling fluids are gaining traction in the data center refrigerant market due to their efficient heat dissipation properties. These fluids offer superior cooling capabilities, especially in high-density computing environments, minimizing the risk of overheating and enhancing energy efficiency. As data centers strive for sustainability and regulatory compliance, liquid cooling fluids present an eco-friendly alternative with reduced environmental impact, positioning them as a key contender in the evolving landscape of data center refrigerants.

Segmentation 4: by Cooling Type

- Air Cooling

- Liquid Cooling

- Free Cooling

Air Cooling Leading the Global Data Center Refrigerant Market (by Cooling Type)

Air cooling remains a prominent choice in the data center refrigerant market, valued for its simplicity and widespread adoption. This method utilizes air as the primary cooling medium, circulating it through the data center to dissipate heat generated by IT equipment. Despite challenges such as limited scalability and energy inefficiency, air cooling remains favored in many data center setups due to its familiarity and cost-effectiveness. However, advancements in liquid cooling and environmental concerns may prompt gradual shifts toward more efficient refrigeration technologies.

Segmentation 5: by Deployment

- Installation/OEM

- Aftermarket

Installation/OEM to Lead the Global Data Center Refrigerant Market Market (by Deployment)

Original equipment manufacturers (OEMs) lead the data center refrigerant market. OEMs specialize in designing and manufacturing cooling systems tailored to data center specifications. With expertise in integrating refrigeration solutions seamlessly into data center infrastructure, they offer comprehensive support from initial setup to ongoing maintenance. This ensures optimal performance and reliability of refrigerant systems. As data centers increasingly prioritize efficiency and sustainability, OEMs play a pivotal role in providing innovative and eco-friendly cooling solutions tailored to evolving demand in the market.

Segmentation 6: by Region

- North America

- Europe

- U.K.

- China

- Asia-Pacific and Japan

- South America

North America Region to Lead the Global Data Center Refrigerant Market (by Region)

North America emerges as a frontrunner in the data center refrigerant market, driven by its robust infrastructure and technological advancements. With a high concentration of data centers across the region, including major tech hubs, North America holds a significant market share. Factors such as stringent environmental regulations and the push toward energy efficiency further propel the adoption of eco-friendly refrigerants. As the region continues to prioritize innovation and sustainability, North America remains a key influencer in shaping the trajectory of the data center refrigerant industry.

Recent Developments in the Data Center Refrigerant Market

- In May 2022, Intel announced its commitment to invest $700.0 million in a new research and development facility focused on designing cutting-edge immersion liquid cooling solutions and other technologies tailored for data center applications.

- In November 2022, Google announced plans for the advancement of a novel data center cooling system, which harnesses waste heat generated by servers to fuel the cooling infrastructure. This innovative system remains in its preliminary stages of development.

- In June 2021, Microsoft inaugurated its eco-friendly datacenter region in Arizona. The Arizona-based datacenters will employ adiabatic cooling, a method that eliminates water usage for cooling during over half of the year.

Demand - Drivers and Limitations

Market Demand Drivers

The global surge in digital services, cloud computing, and data storage demands has fueled the proliferation of data center infrastructure, including hyperscale facilities deployed worldwide. Edge computing advancements have accelerated data processing for technologies such as IoT and 5G. Concurrently, environmental consciousness has prompted companies to prioritize sustainability, with giants such as Google and Microsoft committing to carbon-neutral operations. Collaborations such as BMW's partnership with EcoDC underscore this shift, leveraging green data centers for computational needs. Apple's CSR initiatives highlight the industry's progress toward carbon neutrality. To align with sustainability goals, data centers increasingly adopt energy-efficient, low-GWP refrigerants, driving market growth. As water-based cooling predominates in data centers, water usage effectiveness (WUE) emerges as a crucial metric, especially amid rising global water consumption. Combining WUE with power usage effectiveness (PUE) provides insights into facility efficiency, urging data centers to optimize water utilization for sustainable operations.

Market Restraints

Despite its promising growth trajectory, the data center refrigerant market faces several restraints. One significant challenge is the regulatory landscape, with stringent regulations and compliance requirements impacting the adoption of certain refrigerants. Additionally, the initial investment costs associated with upgrading or retrofitting existing data center cooling systems with eco-friendly refrigerants can be prohibitive for some organizations. Technical challenges, such as compatibility issues with existing infrastructure and concerns about performance and reliability, also hinder widespread adoption. Moreover, the lack of awareness and expertise in selecting and implementing suitable refrigerant solutions poses a barrier to market expansion. Addressing these restraints would be crucial for unlocking the full potential of the data center refrigerant market and driving sustainable growth in the future.

Market Opportunities

Neural network implementations are revolutionizing data center cooling by enabling real-time analysis of temperature and environmental data, leading to precise control and significant energy savings. Meanwhile, indirect thermosyphon cooling utilizes dielectric liquids to dissipate heat from electronic components efficiently. Investments in data center cooling innovations, driven by the demand for sustainability, are exemplified by initiatives such as COOLERCHIPS, aiming to reduce cooling power usage. NVIDIA Corporation received funding to develop a Green Refrigerant Compact Hybrid System, while tech giants such as Facebook and Google also invest heavily in optimizing cooling processes. Data centers' substantial energy consumption and carbon emissions underscore the urgency for sustainable practices, aligning with initiatives such as the European Green Deal for carbon-neutral data centers by 2030. Amidst the growth in data center installations driven by cloud computing and IoT, efficiency improvements in cooling are imperative to meet escalating demand while mitigating environmental impact.

How can this report add value to an organization?

Product/ Innovation Strategy: In the data center refrigerant market, a strategic focus on innovation drives product development. Collaborate with industry leaders to introduce eco-friendly refrigerants and advanced cooling technologies, meeting evolving regulatory standards. Leverage data analytics for real-time monitoring, optimizing cooling efficiency, and reducing environmental impact while ensuring operational excellence.

Growth/ Marketing Strategy: Utilize targeted marketing campaigns highlighting eco-friendly benefits and energy savings. Forge partnerships with data center operators and OEMs to expand reach and offer comprehensive solutions. Continuously innovate to stay ahead in the competitive landscape.

Competitive Strategy: Emphasizing differentiation and value proposition will be crucial for success in the market. Conduct thorough market analysis to identify niche segments and competitive advantages and position products accordingly. Forge alliances with key stakeholders and offer customizable solutions to meet diverse customer needs effectively.

Key Market Players and Competition Synopsis

The companies that are profiled in the data center refrigerant market have been selected based on inputs gathered from primary experts and analyzing company coverage, product portfolio, and market penetration.

Some of the prominent names in the market are:

- Honeywell International Inc.

- The Chemours Company

- Climalife

- Arkema

- Orbia

- DAIKIN INDUSTRIES, Ltd.

- Dow

- M&I Materials Ltd

- Asetek, Inc. A/S

- 3M

- Cargill, Incorporated

Table of Contents

Executive Summary

1 Markets

- 1.1 Industry Outlook

- 1.1.1 Market Definition

- 1.1.2 Data Center Trends

- 1.1.2.1 Data Center Capacities: Current and Future

- 1.1.2.2 Data Center Power Consumption Scenario

- 1.1.2.3 Impact of Carbon-Neutral Data Center (CNDC) Operations on Data Center Refrigerant Market

- 1.1.2.3.1 Current and Future Scenario for CNDC

- 1.1.2.3.2 Alternative Solutions to Current HVAC Systems Used in Data Centers

- 1.1.2.3.3 Cost Analysis

- 1.1.2.3.3.1 Capital Expenditure (CAPEX)

- 1.1.2.3.3.1.1 Infrastructure Cost

- 1.1.2.3.3.2 Operational Expenditure (OPEX)

- 1.1.2.3.3.2.1 Energy Cost

- 1.1.2.3.4 Key Countries to Focus

- 1.1.2.4 Impact of United Nations Intergovernmental Panel on Climate Change on Data Center Market

- 1.1.2.4.1 Impact Assessment of United Intergovernmental Panel on Climate Change (IPCC)'s report

- 1.1.2.5 Impact of PFAS Refrigerant Ban on the Global Data Center Cooling Outlook

- 1.1.2.5.1 Alternative Cooling Solutions to PFAS Refrigerants

- 1.1.2.5.2 Advantages and Disadvantages of Non-PFAS Refrigerants

- 1.1.2.6 Data Center Cooling Strategies

- 1.1.2.6.1 Upcoming Data Center Refrigerant Concepts

- 1.1.2.7 Refrigerant Selection Criteria

- 1.1.2.8 Other Industrial Trends

- 1.1.2.8.1 HPC Cluster Developments

- 1.1.2.8.2 Blockchain Initiatives

- 1.1.2.8.3 Super Computing

- 1.1.2.8.4 5G and 6G Developments

- 1.1.2.8.5 Impact of Server/Rack Density

- 1.2 Ecosystem/Ongoing Programs

- 1.2.1 Consortiums and Associations

- 1.2.2 Important Regulations

- 1.2.3 Government Initiatives and Impacts

- 1.3 Business Dynamics

- 1.3.1 Business Drivers

- 1.3.1.1 Expanding Data Center Industry

- 1.3.1.1.1 Data Center Investment Landscape

- 1.3.1.1.1.1 Key Regional Data Center Investment Trend (2022-2023)

- 1.3.1.1.1 Data Center Investment Landscape

- 1.3.1.2 Sustainable Development Efforts and CSR Activities

- 1.3.1.2.1 The Green IT Cube

- 1.3.1.3 Growing Adoption of Alternate Cooling Solutions for Improved Water Usage Efficiency

- 1.3.1.4 Need for High Energy Efficiency

- 1.3.1.1 Expanding Data Center Industry

- 1.3.2 Business Challenges

- 1.3.2.1 Phasing out of PFAS Refrigerants

- 1.3.2.2 Intense Market Competition from Diverse Cooling Technology

- 1.3.2.3 Rapid Adoption of Refrigerants over Air Cooling Driven by its Advantages

- 1.3.2.3.1 Leading Hyperscale Data Centre Operators to Have a Huge Impact on Market Adoption

- 1.3.3 Business Opportunities

- 1.3.3.1 AI and Neural Network Implementation to Optimize Cooling

- 1.3.3.2 Growing Traction for Indirect Thermosyphon Cooling

- 1.3.3.3 Increase in Investments toward Data Center Cooling Innovations

- 1.3.3.4 Growing Utilization of Advanced Refrigerants to Meet Environmental Targets

- 1.3.3.5 Resurgence of Air-Cooled Chillers

- 1.3.1 Business Drivers

- 1.4 Supply Chain Analysis

- 1.5 Pricing Analysis

2 By Application

- 2.1 Industry

- 2.2 Data Center Type

3 By Product

- 3.1 Refrigerant Type

- 3.1.1 Conventional Refrigerants

- 3.1.2 Liquid Cooling Fluids

- 3.2 Cooling Type

- 3.2.1 Air Cooling

- 3.2.2 Liquid Cooling

- 3.2.3 Free Cooling

- 3.3 Deployment

- 3.3.1 Installation/OEM

- 3.3.2 Aftermarket

4 Regions

- 4.1 Global Data Center Outlook

- 4.2 North America

- 4.2.1 U.S.

- 4.2.2 Rest of North America

- 4.3 Europe

- 4.3.1 Germany

- 4.3.2 Netherlands

- 4.3.3 France

- 4.3.4 Scandinavia

- 4.3.5 Rest of Europe

- 4.4 U.K.

- 4.5 China

- 4.6 Asia Pacific and Japan

- 4.6.1 Japan

- 4.6.2 Australia

- 4.6.3 India

- 4.6.4 Singapore

- 4.6.5 Rest of Asia Pacific

- 4.7 South America

- 4.7.1 Brazil

5 Markets - Competitive Benchmarking & Company Profiles

- 5.1 Competitive Benchmarking

- 5.2 Company Profiles

- 5.2.1 Honeywell International Inc.

- 5.2.1.1 Company Overview

- 5.2.1.2 Product Portfolio

- 5.2.1.3 Analyst View

- 5.2.1.3.1 Regions of Growth:

- 5.2.2 The Chemours Company

- 5.2.2.1 Company Overview

- 5.2.2.2 Product Portfolio

- 5.2.2.3 Analyst View

- 5.2.2.3.1 Regions of Growth:

- 5.2.3 Climalife

- 5.2.3.1 Company Overview

- 5.2.3.2 Product Portfolio

- 5.2.3.3 Analyst View

- 5.2.3.3.1 Regions of Growth:

- 5.2.4 Arkema

- 5.2.4.1 Company Overview

- 5.2.4.2 Product Portfolio

- 5.2.4.3 Analyst View

- 5.2.4.3.1 Regions of Growth:

- 5.2.5 Orbia

- 5.2.5.1 Company Overview

- 5.2.5.2 Product Portfolio

- 5.2.5.3 Analyst View

- 5.2.5.3.1 Regions of Growth:

- 5.2.6 DAIKIN INDUSTRIES, Ltd.

- 5.2.6.1 Company Overview

- 5.2.6.2 Product Portfolio

- 5.2.6.3 Customer Profile

- 5.2.6.3.1 Target Customer Segments

- 5.2.6.3.2 Key Clients

- 5.2.6.4 Analyst View

- 5.2.6.4.1 Regions of Growth:

- 5.2.7 Dow

- 5.2.7.1 Company Overview

- 5.2.7.2 Product Portfolio

- 5.2.7.3 Customer Profile

- 5.2.7.3.1 Target Customer Segments

- 5.2.7.4 Analyst View

- 5.2.7.4.1 Regions of Growth:

- 5.2.8 M&I Materials Ltd

- 5.2.8.1 Company Overview

- 5.2.8.2 Product Portfolio

- 5.2.8.3 Customer Profile

- 5.2.8.3.1 Target Customer Segments

- 5.2.8.4 Analyst View

- 5.2.8.4.1 Regions of Growth:

- 5.2.9 Asetek, Inc. A/S

- 5.2.9.1 Company Overview

- 5.2.9.2 Product Portfolio

- 5.2.9.3 Customer Profile

- 5.2.9.3.1 Target Customer Segments

- 5.2.9.4 Analyst View

- 5.2.9.4.1 Regions of Growth:

- 5.2.10 3M

- 5.2.10.1 Company Overview

- 5.2.10.2 Product Portfolio

- 5.2.10.3 Customer Profile

- 5.2.10.3.1 Target Customer Segments

- 5.2.10.3.2 Key Clients

- 5.2.10.4 Analyst View

- 5.2.10.4.1 Regions of Growth:

- 5.2.11 Cargill, Incorporated

- 5.2.11.1 Company Overview

- 5.2.11.2 Product Portfolio

- 5.2.11.3 Customer Profile

- 5.2.11.3.1 Target Customer Segments

- 5.2.11.4 Analyst View

- 5.2.11.4.1 Regions of Growth:

- 5.2.1 Honeywell International Inc.

6 Research Methodology

- 6.1 Data Sources

- 6.1.1 Primary Data Sources

- 6.1.2 Secondary Data Sources

- 6.1.3 Data Triangulation

- 6.2 Market Estimation and Forecast

- 6.2.1 Factors for Data Prediction and Modelling