|

|

市場調査レポート

商品コード

1422242

欧州の2D材料市場:分析と予測(2022年~2031年)Europe 2D Materials Market: Analysis and Forecast, 2022-2031 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 欧州の2D材料市場:分析と予測(2022年~2031年) |

|

出版日: 2024年02月09日

発行: BIS Research

ページ情報: 英文 128 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

欧州の2D材料の市場規模(英国を除く)は、2022年の7,790万米ドルから2031年には5億2,800万米ドルに達すると予測され、予測期間の2022年~2031年のCAGRは23.7%になるとみられています。

2D材料の需要増は、複合材料やコーティング、エネルギー貯蔵デバイス、エレクトロニクス、半導体、医薬品、自動車など、さまざまな産業からの需要増が原動力になると予想されます。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2022年~2031年 |

| 2022年評価 | 7,790万米ドル |

| 2031年予測 | 5億2,800万米ドル |

| CAGR | 23.7% |

欧州の2D材料市場は現在、大きな成長局面を迎えています。この拡大の主な要因は、燃料電池自動車の採用が増加していることに加え、同大陸全域で脱炭素化と汚染防止への取り組みが重視されていることです。さらに、エレクトロニクス分野における透明導電膜(TCF)のニーズの高まりとともに、さまざまなエンドユーザー産業からの2D材料に対する高い需要が、欧州の2D材料市場の成長をさらに後押ししています。

さらに、ナノ材料に向けた世界の動向は欧州市場に好影響を与え、市場拡大を促進すると予想されます。また、太陽光発電やスポーツ用品などの用途で2D材料が利用されていることも、欧州における2D材料の需要拡大に寄与しています。

当レポートでは、欧州の2D材料市場について調査し、市場の概要とともに、エンドユーザー別、材料タイプ別、国別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

調査範囲

第1章 市場

- 業界の展望

- ビジネスダイナミクス

- スタートアップの情勢

第2章 地域

- 欧州

- 市場

- 用途

- 製品

- 欧州(国別)

- 英国

- 市場

- 用途

- 製品

第3章 市場-競合ベンチマーキングと企業プロファイル

- 競合ベンチマーキング

- 競合マトリックス

- 主要企業の材料タイプ別の製品マトリックス

- 主要企業の市場シェア分析、2021年

- 企業プロファイル

- Thomas Swan & Co. Ltd.

- Ossila Ltd

- 2D Materials Pte Ltd.

- Blackleaf

- BASF SE

- AVANZARE INNOVACION TECNOLOGICA S.L.

- Layer One

- 2-D Tech

- Smena

第4章 調査手法

List of Figures

- Figure 1: Europe 2D Materials Market, $Million, 2021, 2022, and 2031

- Figure 2: Europe 2D Materials Market (by End User), $Million, 2021 and 2031

- Figure 3: Europe 2D Materials Market (by Material Type), $Million, 2021 and 2031

- Figure 4: 2D Materials Market (by Region), $Million, 2021 and 2031

- Figure 5: Fuel Cell Electric Vehicle Fleets

- Figure 6: Advantages of Employing Graphene in Fuel Cells

- Figure 7: Advantages of Graphene and Derivatives in Fuel Cell Applications

- Figure 8: Importance of Graphene in Achieving Sustainability Goals

- Figure 9: Different Types of 2D Materials as Efficient ECR Electrocatalysts

- Figure 10: Supply Chain Analysis of the 2D Materials Market

- Figure 11: Automotive Production, Units, 2019-2021

- Figure 12: Billing of Semiconductor Industry, $Billion, 2018-2022

- Figure 13: Difference Between Bulk Materials and Nano Materials

- Figure 14: Comparison Analysis Between Graphene and TMDCs

- Figure 15: Different Methodologies of 2D Materials

- Figure 16: Different Applications of Graphene/Mxene Composite in Medical Field

- Figure 17: Smart Nanomaterials Market Snapshot

- Figure 18: Clean Energy Investment in the Net Zero Pathway, $Trillion, 2016-2050

- Figure 19: Numerous Types of Applications for Graphene Conductive Films

- Figure 20: Numerous Types of Non-Graphene Materials and their Usage in Different Applications

- Figure 21: Research Methodology

- Figure 22: Top-Down and Bottom-Up Approach

- Figure 23: 2D Materials Market: Influencing Factors

- Figure 24: Assumptions and Limitations

List of Tables

- Table 1: Consortiums and Associations

- Table 2: Regulatory/Certification Bodies

- Table 3: List of Government Programs for 2D Materials Market

- Table 4: List of Programs by Research Institutions and Universities

- Table 5: Key Product Developments

- Table 6: Key Market Developments

- Table 7: Key Mergers and Acquisitions

- Table 8: Key Partnerships and Joint Ventures

- Table 9: 2D Materials Market (by Region), Tons, 2021-2031

- Table 10: 2D Materials Market (by Region), $Million, 2021-2031

- Table 11: Europe 2D Materials Market (by End User), Tons, 2021-2031

- Table 12: Europe 2D Materials Market (by End User), $Million, 2021-2031

- Table 13: Europe 2D Materials Market (by Material Type), Tons, 2021-2031

- Table 14: Europe 2D Materials Market (by Material Type), $Million, 2021-2031

- Table 15: Germany 2D Materials Market (by End User), Tons, 2021-2031

- Table 16: Germany 2D Materials Market (by End User), $Million, 2021-2031

- Table 17: Germany 2D Materials Market (by Material Type), Tons, 2021-2031

- Table 18: Germany 2D Materials Market (by Material Type), $Million, 2021-2031

- Table 19: France 2D Materials Market (by End User), Tons, 2021-2031

- Table 20: France 2D Materials Market (by End User), $Million, 2021-2031

- Table 21: France 2D Materials Market (by Material Type), Tons, 2021-2031

- Table 22: France 2D Materials Market (by Material Type), $Million, 2021-2031

- Table 23: Italy 2D Materials Market (by End User), Tons, 2021-2031

- Table 24: Italy 2D Materials Market (by End User), $Million, 2021-2031

- Table 25: Italy 2D Materials Market (by Material Type), Tons, 2021-2031

- Table 26: Italy 2D Materials Market (by Material Type), $Million, 2021-2031

- Table 27: Spain 2D Materials Market (by End User), Tons, 2021-2031

- Table 28: Spain 2D Materials Market (by End User), $Million, 2021-2031

- Table 29: Spain 2D Materials Market (by Material Type), Tons, 2021-2031

- Table 30: Spain 2D Materials Market (by Material Type), $Million, 2021-2031

- Table 31: Rest-of-Europe 2D Materials Market (by End User), Tons, 2021-2031

- Table 32: Rest-of-Europe 2D Materials Market (by End User), $Million, 2021-2031

- Table 33: Rest-of-Europe 2D Materials Market (by Material Type), Tons, 2021-2031

- Table 34: Rest-of-Europe 2D Materials Market (by Material Type), $Million, 2021-2031

- Table 35: U.K. 2D Materials Market (by End User), Tons, 2021-2031

- Table 36: U.K. 2D Materials Market (by End User), $Million, 2021-2031

- Table 37: U.K. 2D Materials Market (by Material Type), Tons, 2021-2031

- Table 38: U.K. 2D Materials Market (by Material Type), $Million, 2021-2031

- Table 39: Product Matrix for Key Companies, By Material Type

- Table 40: Market Shares of Key Companies, 2021

“The Europe 2D Materials Market (excluding U.K.) Expected to Reach $528.0 Million by 2031.”

Introduction to Europe 2D Materials Market

The Europe 2D materials market (excluding U.K.) is projected to reach $528.0 million by 2031 from $77.9 million in 2022, growing at a CAGR of 23.7% during the forecast period 2022-2031. The rising demand for 2D materials is expected to be driven by increased demand from various industries including composites and coatings, energy storage devices, electronics, semiconductors, pharmaceuticals, automotive, and more.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2022 - 2031 |

| 2022 Evaluation | $77.9 Million |

| 2031 Forecast | $528.0 Million |

| CAGR | 23.7% |

Market Introduction

The 2D materials market in Europe is currently experiencing a phase of significant growth. This expansion is primarily attributed to the increasing adoption of fuel cell vehicles, coupled with a growing emphasis on decarbonization and pollution control initiatives across the continent. Moreover, the high demand for 2D materials from various end-user industries, along with the surging need for transparent conductive films (TCF) within the electronics sector, is further propelling the growth of the Europe 2D materials market.

Additionally, the global trend towards nanomaterials is expected to have a positive impact on the Europe market, fostering its expansion. The utilization of 2D materials in applications such as photovoltaics and sports equipment is also contributing to the rising demand for these materials within Europe.

Market Segmentation:

Segmentation 1: by End User

- Composite and Coatings

- Energy Storage Devices

- Electronics

- Semiconductor

- Pharmaceuticals

- Automobiles

- Others

Segmentation 2: by Material Type

- Graphene

- Black Phosphorous

- Transition Metal Dichalcogenides

- Mxene

- Hexagonal boron nitride

- Others

electrical and thermal conductivity.

Segmentation 3: by Country

- Germany

- France

- Italy

- Spain

- Rest-of-Europe

How can this report add value to an organization?

Product/Innovation Strategy: The product segment helps the reader to understand the different material types involved in 2D materials. Moreover, the study provides the reader with a detailed understanding of the Europe 2D materials market based on the end user (composite and coatings, energy storage devices, electronics, semiconductors, pharmaceuticals, automobiles, and others). 2D materials are gaining traction in end-user industries on the back of sustainability concerns and their high durability properties. They are also being used for controlling greenhouse gas (GHG) emissions.

Growth/Marketing Strategy: The Europe 2D materials market has seen major development by key players operating in the market, such as business expansions, partnerships, collaborations, mergers and acquisitions, and joint ventures. The favored strategy for the companies has been product developments, business expansions, and acquisitions to strengthen their position in the Europe 2D materials market.

Competitive Strategy: Key players in the Europe 2D materials market analyzed and profiled in the study involve 2D materials manufacturers and the overall ecosystem. Moreover, a detailed competitive benchmarking of the players operating in the Europe 2D materials market has been done to help the reader understand how players stack against each other, presenting a clear market landscape. Additionally, comprehensive competitive strategies such as partnerships, agreements, acquisitions, and collaborations will aid the reader in understanding the untapped revenue pockets in the market.

Table of Contents

Executive Summary

Scope of the Study

1. Markets

- 1.1. Industry Outlook

- 1.1.1. Trends: Current and Future

- 1.1.1.1. Increasing Demand of 2D Materials for Hydrogen Fuel Cells in Electric Vehicles

- 1.1.1.2. Increasing Preference of 2D Materials to Lessen the Pollutants

- 1.1.2. Supply Chain Analysis

- 1.1.3. Ecosystem of 2D Materials Market

- 1.1.3.1. Consortiums and Associations

- 1.1.3.2. Regulatory/Certification Bodies

- 1.1.3.3. Government Programs

- 1.1.3.4. Programs by Research Institutions and Universities

- 1.1.4. Impact of COVID-19 on 2D Materials Market

- 1.1.4.1. Impact of COVID-19 on Automotive Industry

- 1.1.4.2. Impact of COVID-19 on Semiconductor Industry

- 1.1.4.3. Impact of COVID-19 on Energy Storage Devices

- 1.1.4.4. Impact of COVID-19 on Health Care Industry

- 1.1.5. Impact of Semiconductor Crisis on 2D Materials Market

- 1.1.6. Comparative Analysis Between Bulk Materials and Nano Materials

- 1.1.7. Comparative Analysis Between Transition Metal Dichalcogenides (TMDCs) and Graphene

- 1.1.8. Methodologies of 2D Materials

- 1.1.9. Significant Advancements in Graphene and Other 2D Materials

- 1.1.10. Emergence of Hybrid Technology

- 1.1.11. Recent Investments Made in 2D Materials

- 1.1.12. Emerging Start-Up Companies of 2D Materials

- 1.1.13. Snapshot of Smart Nanomaterials Market

- 1.1.1. Trends: Current and Future

- 1.2. Business Dynamics

- 1.2.1. Business Drivers

- 1.2.1.1. Growing Adoption of 2D materials in Energy Storage

- 1.2.1.2. Strong Growth of 2D Materials in the Healthcare Industry

- 1.2.1.3. Growing Demand of Transparent Conductive Films (TCF) in Electronic Industry

- 1.2.2. Business Challenges

- 1.2.2.1. Lack of Large-Scale Production of High-Quality Graphene

- 1.2.2.2. High Cost of Production

- 1.2.3. Business Strategies

- 1.2.3.1. Product Developments

- 1.2.3.2. Market Developments

- 1.2.4. Corporate Strategies

- 1.2.4.1. Mergers and Acquisitions

- 1.2.4.2. Partnerships and Joint Ventures

- 1.2.5. Business Opportunities

- 1.2.5.1. Expanding Market of Nanomaterials for Easily accessible Electric Vehicles

- 1.2.5.2. Increasing Opportunities for Non-Graphene 2D Materials

- 1.2.1. Business Drivers

- 1.3. Start-Up Landscape

- 1.3.1. Key Start-Ups in the Ecosystem

2. Regions

- 2.1. Europe

- 2.1.1. Market

- 2.1.1.1. Key Producers and Suppliers in Europe

- 2.1.1.2. Business Drivers

- 2.1.1.3. Business Challenges

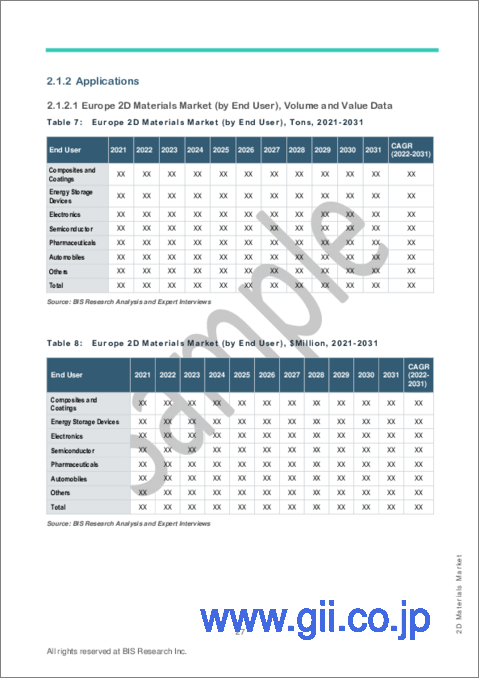

- 2.1.2. Applications

- 2.1.2.1. Europe 2D Materials Market (by End User), Volume and Value Data

- 2.1.3. Products

- 2.1.3.1. Europe 2D Materials Market (by Material Type), Volume and Value Data

- 2.1.4. Europe (by Country)

- 2.1.4.1. Germany

- 2.1.4.1.1. Market

- 2.1.4.1.1.1. Buyer Attributes

- 2.1.4.1.1.2. Key Producers and Suppliers in Germany

- 2.1.4.1.1.3. Regulatory Landscape

- 2.1.4.1.1.4. Business Drivers

- 2.1.4.1.1.5. Business Challenges

- 2.1.4.1.2. Applications

- 2.1.4.1.2.1. Germany 2D Materials Market (by End User), Volume and Value Data

- 2.1.4.1.3. Products

- 2.1.4.1.3.1. Germany 2D Materials Market (by Material Type), Volume and Value Data

- 2.1.4.1.1. Market

- 2.1.4.2. France

- 2.1.4.2.1. Market

- 2.1.4.2.1.1. Buyer Attributes

- 2.1.4.2.1.2. Key Producers and Suppliers in France

- 2.1.4.2.1.3. Regulatory Landscape

- 2.1.4.2.1.4. Business Drivers

- 2.1.4.2.1.5. Business Challenges

- 2.1.4.2.2. Applications

- 2.1.4.2.2.1. France 2D Materials Market (by End User), Volume and Value Data

- 2.1.4.2.3. Products

- 2.1.4.2.3.1. France 2D Materials Market (by Material Type), Volume and Value Data

- 2.1.4.2.1. Market

- 2.1.4.3. Italy

- 2.1.4.3.1. Market

- 2.1.4.3.1.1. Buyer Attribute

- 2.1.4.3.1.2. Key Producers and Suppliers in Italy

- 2.1.4.3.1.3. Regulatory Landscape

- 2.1.4.3.1.4. Business Drivers

- 2.1.4.3.1.5. Business Challenges

- 2.1.4.3.2. Applications

- 2.1.4.3.2.1. Italy 2D Materials Market (by End User), Volume and Value Data

- 2.1.4.3.3. Products

- 2.1.4.3.3.1. Italy 2D Materials Market (by Material Type), Volume and Value Data

- 2.1.4.3.1. Market

- 2.1.4.4. Spain

- 2.1.4.4.1. Market

- 2.1.4.4.1.1. Buyer Attributes

- 2.1.4.4.1.2. Key Producers and Suppliers in Spain

- 2.1.4.4.1.3. Regulatory Landscape

- 2.1.4.4.1.4. Business Drivers

- 2.1.4.4.1.5. Business Challenges

- 2.1.4.4.2. Applications

- 2.1.4.4.2.1. Spain 2D Materials Market (by End User), Volume and Value Data

- 2.1.4.4.3. Products

- 2.1.4.4.3.1. Spain 2D Materials Market (by Material Type), Volume and Value Data

- 2.1.4.4.1. Market

- 2.1.4.5. Rest-of-Europe (RoE)

- 2.1.4.5.1. Market

- 2.1.4.5.1.1. Buyer Attributes

- 2.1.4.5.1.2. Key Producers and Suppliers in Rest-of-Europe

- 2.1.4.5.1.3. Business Drivers

- 2.1.4.5.1.4. Business Challenges

- 2.1.4.5.2. Applications

- 2.1.4.5.2.1. Rest-of-Europe 2D Materials Market (by End User), Volume and Value Data

- 2.1.4.5.3. Products

- 2.1.4.5.3.1. Rest-of-Europe 2D Materials Market (by Material Type), Volume and Value Data

- 2.1.4.5.1. Market

- 2.1.4.1. Germany

- 2.1.1. Market

- 2.2. U.K.

- 2.2.1. Market

- 2.2.1.1. Buyer Attributes

- 2.2.1.2. Key Producers and Suppliers in the U.K.

- 2.2.1.3. Regulatory Landscape

- 2.2.1.4. Business Drivers

- 2.2.1.5. Business Challenges

- 2.2.2. Applications

- 2.2.2.1. U.K. 2D Materials Market (by End User), Volume and Value Data

- 2.2.3. Products

- 2.2.3.1. U.K. 2D Materials Market (by Material Type), Volume and Value Data

- 2.2.1. Market

3. Markets - Competitive Benchmarking & Company Profiles

- 3.1. Competitive Benchmarking

- 3.1.1. Competitive Position Matrix

- 3.1.2. Product Matrix for Key Companies, By Material Type

- 3.1.3. Market Share Analysis of Key Companies, 2021

- 3.2. Company Profiles

- 3.2.1. Thomas Swan & Co. Ltd.

- 3.2.1.1. Company Overview

- 3.2.1.1.1. Role of Thomas Swan & Co. Ltd. in the 2D Materials Market

- 3.2.1.1.2. Product Portfolio

- 3.2.1.1.3. Production Sites

- 3.2.1.2. Corporate Strategies

- 3.2.1.2.1. Partnerships, Collaborations, and Joint Ventures

- 3.2.1.3. Analyst View

- 3.2.1.1. Company Overview

- 3.2.2. Ossila Ltd

- 3.2.2.1. Company Overview

- 3.2.2.1.1. Role of Ossila Ltd in the 2D Materials Market

- 3.2.2.1.2. Product Portfolio

- 3.2.2.1.3. Production Sites

- 3.2.2.2. Analyst View

- 3.2.2.1. Company Overview

- 3.2.3. 2D Materials Pte Ltd.

- 3.2.3.1. Company Overview

- 3.2.3.1.1. Role of 2D Materials Pte Ltd. in the 2D Materials Market

- 3.2.3.1.2. Product Portfolio

- 3.2.3.1.3. Production Sites

- 3.2.3.2. Business Strategies

- 3.2.3.2.1. Product Developments

- 3.2.3.3. Corporate Strategies

- 3.2.3.3.1. Partnerships, Collaborations, and Joint Ventures

- 3.2.3.4. Analyst View

- 3.2.3.1. Company Overview

- 3.2.4. Blackleaf

- 3.2.4.1. Company Overview

- 3.2.4.1.1. Role of Blackleaf in the 2D Materials Market

- 3.2.4.1.2. Product Portfolio

- 3.2.4.1.3. Production Sites

- 3.2.4.2. Analyst View

- 3.2.4.1. Company Overview

- 3.2.5. BASF SE

- 3.2.5.1. Company Overview

- 3.2.5.1.1. Role of BASF SE in the 2D Materials Market

- 3.2.5.1.2. Product Portfolio

- 3.2.5.1.3. Production Sites

- 3.2.5.2. R&D Analysis

- 3.2.5.3. Analyst View

- 3.2.5.1. Company Overview

- 3.2.6. AVANZARE INNOVACION TECNOLOGICA S.L.

- 3.2.6.1. Company Overview

- 3.2.6.1.1. Role of AVANZARE INNOVACION TECNOLOGICA S.L. in the 2D Materials Market

- 3.2.6.1.2. Product Portfolio

- 3.2.6.1.3. Production Sites

- 3.2.6.2. Business Strategies

- 3.2.6.2.1. Market Development

- 3.2.6.3. Analyst View

- 3.2.6.1. Company Overview

- 3.2.7. Layer One

- 3.2.7.1. Company Overview

- 3.2.7.1.1. Role of Layer One in the 2D Materials Market

- 3.2.7.1.2. Product Portfolio

- 3.2.7.1.3. Production Sites

- 3.2.7.2. Business Strategies

- 3.2.7.2.1. Market Development

- 3.2.7.3. Analyst View

- 3.2.7.1. Company Overview

- 3.2.8. 2-D Tech

- 3.2.8.1. Company Overview

- 3.2.8.1.1. Role of 2-D Tech in the 2D Materials Market

- 3.2.8.1.2. Product Portfolio

- 3.2.8.1.3. Production Sites

- 3.2.8.2. Corporate Strategies

- 3.2.8.2.1. Market Development

- 3.2.8.3. Analyst View

- 3.2.8.1. Company Overview

- 3.2.9. Smena

- 3.2.9.1. Company Overview

- 3.2.9.1.1. Role of Smena in the 2D Materials Market

- 3.2.9.1.2. Product Portfolio

- 3.2.9.1.3. Production Sites

- 3.2.9.2. Analyst View

- 3.2.9.1. Company Overview

- 3.2.1. Thomas Swan & Co. Ltd.

4. Research Methodology

- 4.1. Primary Data Sources

- 4.2. BIS Data Sources

- 4.3. Assumptions and Limitations