|

|

市場調査レポート

商品コード

1399752

欧州の防衛部門向け没入型リアリティ市場の分析・予測:2023-2033年Europe Immersive Reality for Defense Market - Analysis and Forecast, 2023-2033 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 欧州の防衛部門向け没入型リアリティ市場の分析・予測:2023-2033年 |

|

出版日: 2023年12月28日

発行: BIS Research

ページ情報: 英文 98 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

欧州の防衛部門向け没入型リアリティの市場規模は、2022年の6億3,000万米ドルから、予測期間中に18.72%の成長率で推移し、2033年には41億3,000万米ドルの規模に成長すると予測されています。

防衛部門向け没入型リアリティの市場は、訓練、シミュレーション、作戦の有効性を向上させる革新的な技術ソリューションに対するニーズの高まりに後押しされ、防衛・軍事産業における重要な領域として急速に発展しています。

防衛部門向け没入型リアリティは、軍事技術の更新の原動力であり、旧来の防衛パラダイムを一新する多様な技術・用途を提供します。軍事機関や軍隊が増大する脅威や作戦上の障害に直面する中で、没入型リアリティの導入は可能性の限界を押し広げる態勢を整えています。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2023-2033年 |

| 2023年評価 | 7億4,000万米ドル |

| 2033年予測 | 41億3,000万米ドル |

| CAGR | 18.72% |

没入型リアリティ技術は、訓練、シミュレーション、運用効率の向上など多くの利点を提供し、防衛用途の展望を急速に変えつつあります。これらの最先端システムは、費用対効果、臨場感、多彩な機能により、現代の防衛活動に欠かせないものとなっています。高度な訓練とシミュレーションは、防衛部門における没入型リアリティのもっとも一般的な用途の2つです。兵士は、仮想現実 (VR) や拡張現実 (AR) デバイスを使用して、安全かつ制御された環境で、現実的な戦闘シナリオに取り組み、能力を完成させ、戦術的な専門知識を構築することができます。これは訓練コストを削減するだけでなく、軍人のパフォーマンスを向上させます。

訓練以外にも、没入型リアリティは任務の計画や実行にも役立ちます。HUDやARシステムは、兵士、パイロット、指揮官にリアルタイムの情報を提供し、戦場での状況認識や意思決定を向上させるために活用されます。さらに、没入型リアリティは遠隔操作やドローンの操縦において極めて重要な役割を果たしています。オペレーターはVRヘッドセットを通じて戦場に没入し、無人車両やドローンを精密かつ正確に操縦することができます。

当レポートでは、欧州の防衛部門向け没入型リアリティの市場を調査し、市場の背景・概要、市場成長への各種影響因子の分析、特許の動向、各種プログラム、市場規模の推移・予測、各種区分・主要国別の詳細分析、競合情勢、主要企業の分析などをまとめています。

市場の分類

セグメンテーション1:用途別

- 3Dモデリング

- シミュレーション&トレーニング

- メンテナンス&モニタリング

- 状況認識

セグメンテーション2:国別

- フランス

- ドイツ

- ロシア

- 英国

- その他

セグメンテーション3:タイプ別

- 拡張現実 (AR)

- 仮想現実 (VR)

- 複合現実 (MR)

目次

エグゼクティブサマリー

調査範囲

第1章 市場

- 業界の展望

- 防衛部門向け没入型リアリティ:概要

- 進行中のプログラムと今後のプログラム

- 没入型リアリティの未来的な動向

- スタートアップと投資の情勢

- サプライチェーン分析

- 特許分析

- 事業力学

- 事業促進要因

- 事業上の課題

- 事業戦略

- 経営戦略

- 事業機会

第2章 欧州

- 防衛部門向け没入型リアリティ (地域別)

- 欧州

- 市場

- 用途

- 製品

- 欧州 (国別)

第3章 競合ベンチマーキング・企業プロファイル

- 競合ベンチマーキング

- Bohemia Interactive Simulations

- Indra Sistemas, S.A.

- Thales Group

- Varjo

- その他の主要企業プロファイル

- データ予測・モデリングの要素

List of Figures

- Figure 1: Immersive Reality for Defense Market, $Billion, 2022-2033

- Figure 2: Immersive Reality for Defense (by Application), $Million, 2022 and 2033

- Figure 3: Immersive Reality for Defense Market (by Type), $Million, 2022 and 2033

- Figure 4: Immersive Reality for Defense Market (by Region), $Billion, 2033

- Figure 5: Supply Chain Analysis

- Figure 6: Immersive Reality for Defense Market, Business Dynamics

- Figure 7: Share of Key Market Developments, January 2021-September 2023

- Figure 8: Competitive Benchmarking of Key Players

- Figure 9: Research Methodology

- Figure 10: Top-Down and Bottom-Up Approach

- Figure 11: Assumptions and Limitations

List of Tables

- Table 1: Startups and Investments, 2021-2023

- Table 2: Patents, January 2021-September 2023

- Table 3: Mergers and Acquisitions, January 2021-September 2023

- Table 4: Partnerships, Collaborations, Agreements, and Contracts, January 2021-September 2023

- Table 5: Immersive Reality for Defense Market (by Region), $Million, 2022-2033

- Table 6: Europe Immersive Reality for Defense Market (by Application), $Million, 2022-2033

- Table 7: Europe Immersive Reality for Defense Market (by Type), $Million, 2022-2033

- Table 8: U.K. Immersive Reality for Defense Market (by Application), $Million, 2022-2033

- Table 9: U.K. Immersive Reality for Defense Market (by Type), $Million, 2022-2033

- Table 10: Germany Immersive Reality for Defense Market (by Application), $Million, 2022-2033

- Table 11: Germany Immersive Reality for Defense Market (by Type), $Million, 2022-2033

- Table 12: France Immersive Reality for Defense Market (by Application), $Million, 2022-2033

- Table 13: France Immersive Reality for Defense Market (by Type), $Million, 2022-2033

- Table 14: Russia Immersive Reality for Defense Market (by Application), $Million, 2022-2033

- Table 15: Russia Immersive Reality for Defense Market (by Type), $Million, 2022-2033

- Table 16: Rest-of-Europe Immersive Reality for Defense Market (by Application), $Million, 2022-2033

- Table 17: Rest-of-Europe Immersive Reality for Defense Market (by Type), $Million, 2022-2033

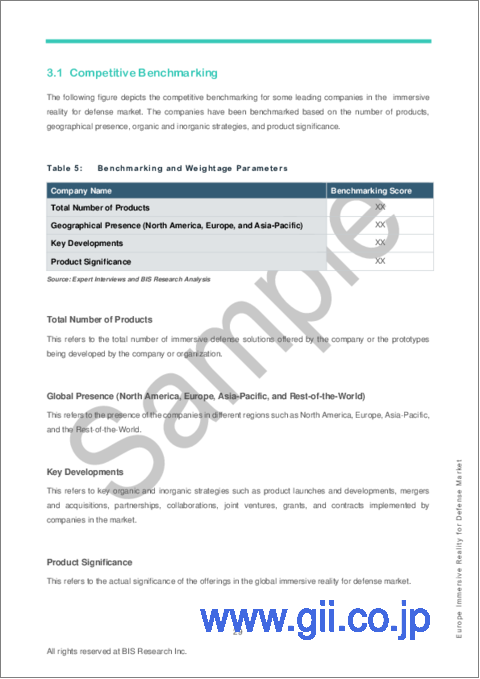

- Table 18: Benchmarking and Weightage Parameters

- Table 19: Bohemia Interactive Simulations: Product Portfolio

- Table 20: Bohemia Interactive Simulations: Mergers and Acquisitions

- Table 21: Bohemia Interactive Simulations: Partnerships, Collaborations, Agreements, and Contracts

- Table 22: Indra Sistemas, S.A.: Product Portfolio

- Table 23: Indra Sistemas, S.A.: Mergers and Acquisitions

- Table 24: Indra Sistemas, S.A.: Partnerships, Collaborations, Agreements, and Contracts

- Table 25: Thales Group: Product Portfolio

- Table 26: Thales Group: Mergers and Acquisitions

- Table 27: Varjo: Product Portfolio

- Table 28: Varjo: Partnerships, Collaborations, Agreements, and Contracts

- Table 29: Other Key Players Profile in the Immersive Reality for Defense Market

Introduction to Europe Immersive Reality for Defense Market

The Europe immersive reality for defense market is estimated to reach $4.13 billion by 2033 from $0.63 billion in 2022, at a growth rate of 18.72% during the forecast period 2023-2033. The field of immersive reality for defense applications is rapidly evolving as a critical domain within the defense and military industries, driven by the growing need for innovative technical solutions to improve training, simulation, and operational effectiveness. Immersive reality refers to a set of technologies that surround users/trainees in virtual settings, delivering a multimodal experience that can reproduce real-world scenarios with remarkable fidelity and immersion.

The field of immersive reality for defense applications is a driving force behind the change of military technologies, providing a diverse range of technologies and applications that challenge old defensive paradigms. As military agencies and armed forces continue to face increasing threats and operational obstacles, the incorporation of immersive reality is poised to push the boundaries of what is possible.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2023 - 2033 |

| 2023 Evaluation | $0.74 Billion |

| 2033 Forecast | $4.13 Billion |

| CAGR | 18.72% |

Market Introduction

Immersive reality technologies are rapidly transforming the landscape of defense applications, providing numerous advantages such as improved training, simulation, and operational efficiency. These cutting-edge systems are indispensable in modern defense operations due to their cost-effectiveness, realism, and varied functions. Advanced training and simulation are two of the most common applications of immersive reality in the defense sector. Soldiers can engage in realistic combat scenarios, perfect their abilities, and build tactical expertise in a safe and controlled environment using virtual reality (VR) and augmented reality (AR) devices. This not only cuts training expenses but also improves military personnel performance.

Aside from training, immersive reality is useful in mission planning and execution. HUDs and augmented reality systems are utilized to give real-time information to soldiers, pilots, and commanders, improving situational awareness and decision-making on the battlefield. Furthermore, immersive reality plays a pivotal role in remote operations and drone piloting. Operators can immerse themselves in the battlefield through VR headsets, controlling unmanned vehicles and drones with precision and accuracy.

Market Segmentation:

Segmentation 1: by Application

- 3D Modeling

- Simulation and Training

- Maintenance and Monitoring

- Situational Awareness

Segmentation 2: by Country

- France

- Germany

- Russia

- U.K.

- Rest-of-Europe

Segmentation 3: by Type

- Augmented Reality (AR)

- Virtual Reality (VR)

- Mixed Reality (MR)

How can this report add value to an organization?

Product/Innovation Strategy: The product segment helps the reader to understand the different types of immersive solutions available for defense deployment and their potential in Europe region.

Growth/Marketing Strategy: The Europe immersive reality for defense market has seen some major development by key players operating in the market, such as partnership, collaboration, and joint venture. The favored strategy for the collaboration between defense agencies and private players is primordially contracting the development and delivery of advanced materials and specialized composite components for space system applications.

Competitive Strategy: Key players in the Europe immersive reality for defense market have been analyzed and profiled in the study, inclusive of major segmentations and service offerings companies provide in the technology segments, respectively. Moreover, a detailed competitive benchmarking of the players operating in the immersive reality for defense market has been done to help the reader understand how players stack against each other, presenting a clear market landscape. Additionally, comprehensive competitive strategies such as partnerships, agreements, and collaborations will aid the reader in understanding the revenue pockets in the market.

Methodology: The research methodology design adopted for this specific study includes a mix of data collected from primary and secondary data sources. Both primary resources (key players, market leaders, and in-house experts) and secondary research (a host of paid and unpaid databases), along with analytical tools, are employed to build the predictive and forecast models.

Key Market Players and Competition Synopsis

The companies that are profiled have been selected based on thorough secondary research, which includes analyzing company coverage, product portfolio, market penetration, and insights that are gathered from primary experts.

Key Companies Profiled:

|

|

Table of Contents

Executive Summary

Scope of the Study

1. Markets

- 1.1. Industry Outlook

- 1.1.1. Immersive Reality for Defense Market: Overview

- 1.1.2. Ongoing and Upcoming Programs

- 1.1.2.1. U.S. Army's Squad Immersive Virtual Trainer (SiVT)

- 1.1.2.2. Remote Augmented Reality Maintenance Assistance (RARM-A)

- 1.1.2.3. Mixed and Immersive Reality Assessment Generation Engine (MIRAGE)

- 1.1.2.4. Virtual Battlespace Simulation (VBS) Training and Military Operations in Urbanized Terrain (MOUT) Training

- 1.1.3. Futuristic Trends in Immersive Reality

- 1.1.3.1. Neuromorphic Computing

- 1.1.3.2. Brain-Computer Interface (BCI) in Immersive Reality Solutions

- 1.1.3.3. Immersive Synthetic Training Environment (STE)

- 1.1.3.4. Tactical Augmented Reality (TAR)

- 1.1.3.5. Virtual Squad Training System (VSTS)

- 1.1.3.6. Artificial Intelligence (AI) Integration in AR-Based Military Simulations

- 1.1.4. Startups and Investment Landscape

- 1.1.5. Supply Chain Analysis

- 1.1.6. Patent Analysis

- 1.2. Business Dynamics

- 1.2.1. Business Drivers

- 1.2.1.1. Increasing Need for Training with Enhanced Situational and Spatial Awareness toward Increased Soldier Lethality

- 1.2.1.2. Development toward Multi-Domain Operations (MDO) Army by 2035

- 1.2.2. Business Challenges

- 1.2.2.1. Tackling Cybersickness and Information Overload

- 1.2.2.2. Security Concerns in Immersive Solutions

- 1.2.3. Business Strategies

- 1.2.3.1. Mergers and Acquisitions

- 1.2.4. Corporate Strategies

- 1.2.4.1. Partnerships, Collaborations, Agreements, and Contracts

- 1.2.5. Business Opportunities

- 1.2.5.1. Advancements toward Next-Generation Command and Control (C2) System Platforms

- 1.2.5.2. Development of Glass Box Systems

- 1.2.1. Business Drivers

2. Europe

- 2.1. Immersive Reality for Defense Market (by Region)

- 2.2. Europe

- 2.2.1. Market

- 2.2.1.1. Key Players in Europe

- 2.2.1.2. Business Drivers

- 2.2.1.3. Business Challenges

- 2.2.2. Application

- 2.2.2.1. Europe Immersive Reality for Defense Market (by Application)

- 2.2.3. Product

- 2.2.3.1. Europe Immersive Reality for Defense Market (by Type)

- 2.2.4. Europe (by Country)

- 2.2.4.1. U.K.

- 2.2.4.1.1. Market

- 2.2.4.1.1.1. Key Players in the U.K.

- 2.2.4.1.2. Application

- 2.2.4.1.2.1. U.K. Immersive Reality for Defense Market (by Application)

- 2.2.4.1.3. Product

- 2.2.4.1.3.1. U.K. Immersive Reality for Defense Market (by Type)

- 2.2.4.1.1. Market

- 2.2.4.2. Germany

- 2.2.4.2.1. Market

- 2.2.4.2.1.1. Key Players in Germany

- 2.2.4.2.2. Application

- 2.2.4.2.2.1. Germany Immersive Reality for Defense Market (by Application)

- 2.2.4.2.3. Product

- 2.2.4.2.3.1. Germany Immersive Reality for Defense Market (by Type)

- 2.2.4.2.1. Market

- 2.2.4.3. France

- 2.2.4.3.1. Market

- 2.2.4.3.1.1. Key Players in France

- 2.2.4.3.2. Application

- 2.2.4.3.2.1. France Immersive Reality for Defense Market (by Application)

- 2.2.4.3.3. Product

- 2.2.4.3.3.1. France Immersive Reality for Defense Market (by Type)

- 2.2.4.3.1. Market

- 2.2.4.4. Russia

- 2.2.4.4.1. Market

- 2.2.4.4.1.1. Key Players in Russia

- 2.2.4.4.2. Application

- 2.2.4.4.2.1. Russia Immersive Reality for Defense Market (by Application)

- 2.2.4.4.3. Product

- 2.2.4.4.3.1. Russia Immersive Reality for Defense Market (by Type)

- 2.2.4.4.1. Market

- 2.2.4.5. Rest-of-Europe

- 2.2.4.5.1. Application

- 2.2.4.5.1.1. Rest-of-Europe Immersive Reality for Defense Market (by Application)

- 2.2.4.5.2. Product

- 2.2.4.5.2.1. Rest-of-Europe Immersive Reality for Defense Market (by Type)

- 2.2.4.5.1. Application

- 2.2.4.1. U.K.

- 2.2.1. Market

3. Competitive Benchmarking and Company Profiles

- 3.1. Competitive Benchmarking

- 3.2. Bohemia Interactive Simulations

- 3.2.1. Company Overview

- 3.2.1.1. Role of Bohemia Interactive Simulations in the Immersive Reality for Defense Market

- 3.2.1.2. Customers

- 3.2.1.3. Product Portfolio

- 3.2.2. Business Strategies

- 3.2.2.1. Mergers and Acquisitions

- 3.2.3. Corporate Strategies

- 3.2.3.1. Partnerships, Collaborations, Agreements, and Contracts

- 3.2.4. Analyst View

- 3.2.1. Company Overview

- 3.3. Indra Sistemas, S.A.

- 3.3.1. Company Overview

- 3.3.1.1. Role of Indra Sistemas, S.A. in the Immersive Reality for Defense Market

- 3.3.1.2. Customers

- 3.3.1.3. Product Portfolio

- 3.3.2. Business Strategies

- 3.3.2.1. Mergers and Acquisitions

- 3.3.3. Corporate Strategies

- 3.3.3.1. Partnerships, Collaborations, Agreements, Investments, and Contracts

- 3.3.4. Analyst View

- 3.3.1. Company Overview

- 3.4. Thales Group

- 3.4.1. Company Overview

- 3.4.1.1. Role of Thales Group in the Immersive Reality for Defense Market

- 3.4.1.2. Customers

- 3.4.1.3. Product Portfolio

- 3.4.2. Business Strategies

- 3.4.2.1. Mergers and Acquisitions

- 3.4.3. Analyst View

- 3.4.1. Company Overview

- 3.5. Varjo

- 3.5.1. Company Overview

- 3.5.1.1. Role of Varjo in the Immersive Reality for Defense Market

- 3.5.1.2. Customers

- 3.5.1.3. Product Portfolio

- 3.5.2. Corporate Strategies

- 3.5.2.1. Partnerships, Collaborations, Agreements, and Contracts

- 3.5.3. Analyst View

- 3.5.1. Company Overview

- 3.6. Other Key Player Profiles

- 3.7. Factors for Data Prediction and Modeling