|

|

市場調査レポート

商品コード

1526816

スマートハーベスト市場- 世界および地域別分析:用途別、製品別、地域別 - 分析と予測(2024年~2033年)Smart Harvest Market - A Global and Regional Analysis: Focus on Application, Product, and Region - Analysis and Forecast, 2024-2033 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| スマートハーベスト市場- 世界および地域別分析:用途別、製品別、地域別 - 分析と予測(2024年~2033年) |

|

出版日: 2024年08月06日

発行: BIS Research

ページ情報: 英文 152 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

世界のスマートハーベストの市場規模は、2023年の47億2,950万米ドルから2033年には109億2,770万米ドルに達し、予測期間の2024年~2033年のCAGRは8.34%になると予測されています。

スマートハーベスト市場は飛躍的な成長を遂げようとしています。持続可能な農業への世界の移行と農業における先端技術の統合に伴い、最先端のスマートハーベストソリューションに対するかつてない需要が生じています。人工知能や機械学習を含む技術の進歩は、収穫プロセスに革命をもたらし、比類のない精度と効率を提供します。さらに、持続可能な農業の推進と食料安全保障の確保を目的とした世界の政府のイニシアティブの高まりが、スマートハーベスト技術への実質的な投資を促進すると予想されます。これは、ベンダーが収穫能力の限界を押し広げるために絶えず革新し、最終的に世界中の農業慣行における生産性、効率性、持続可能性の向上を確実にするダイナミックな情勢を作り出しています。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2024年~2033年 |

| 2024年評価 | 53億1,410万米ドル |

| 2033年予測 | 109億2,770万米ドル |

| CAGR | 8.34% |

スマートハーベスト市場には、自動化とデータ主導の意思決定を通じて収穫プロセスを最適化するように設計された最先端の農業技術や手法が含まれます。この市場には、ロボットハーベスター、スマートハーベスター、ダイナミックモニタリングソフトウェアなどの先進システムが組み込まれており、これらが一体となって農作業の効率、精度、持続可能性を向上させる。人工知能(AI)、機械学習、リアルタイム分析を活用することで、スマートハーベスト・ソリューションは、労働力不足、作物収量の変動、資源管理などの重大な問題に取り組みます。

スマートハーベスト市場は、労働コストと人的労力を最小限に抑えながら生産性を向上させる必要性によって急速に進展しています。この市場では、センサーやドローンの統合とともに、自律型収穫機の使用が増加しています。これらの技術的進歩は、不適切な収穫による作物ロスの増加や人件費の高騰といった問題を軽減するのに役立っています。とはいえ、市場は先端技術の高額な費用や新興国での普及率の遅れといった課題に直面しています。こうした障害にもかかわらず、研究や技術開発に多額の資金を提供するなど、持続可能な農業と食糧安全保障を推進する政府の取り組みが成長を後押ししています。さらに、小規模農場向けに設計されたスケーラブルな収穫技術のイントロダクションは、先進的なソリューションをより身近なものにし、市場の拡大をさらに後押ししています。

当レポートでは、世界のスマートハーベスト市場について調査し、市場の概要とともに、用途別、製品別、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

第1章 市場

- 動向:現在および将来の影響評価

- サプライチェーンの概要

- 研究開発レビュー

- 規制状況

- ステークホルダー分析

- 市場力学:概要

- 市場における主要製品のアーキテクチャ/技術比較

第2章 用途

- 用途のセグメンテーション

- 用途の概要

- 世界のスマートハーベスト市場(事業サイト別)

- 用途のセグメンテーション

- 用途の概要

- 世界のスマートハーベスト市場(作物タイプ別)

第3章 製品

- 製品セグメンテーション

- 製品概要

- 世界のスマートハーベスト市場(製品別)

第4章 地域

- 地域別概要

- 促進要因と抑制要因

- 北米

- 欧州

- アジア太平洋

- その他の地域

第5章 市場-競合ベンチマーキングと企業プロファイル

- 今後の見通し

- 地理的評価

- Agrobot

- Dogtooth Technologies Limited

- FFRobotics

- OCTINION

- Harvest CROO Robotics LLC

- Advanced Farm Technologies, Inc.

- MetoMotion

- Mycionics Inc.

- Tortuga Agricultural Technologies, Inc.

- Organifarms GmbH

- Tevel Aerobotics Technologies

- AVL Motion B.V.

- Fieldwork Robotics

- AMB Rousset

- Deere & Company

第6章 調査手法

List of Figures

- Figure 1: Global Smart Harvest Market (by Region), $Million, 2024, 2028, and 2033

- Figure 2: Global Smart Harvest Market (by Site of Operation), $Million, 2024, 2028, and 2033

- Figure 3: Global Smart Harvest Market (by Crop Type), $Million, 2024, 2028, and 2033

- Figure 4: Global Smart Harvest Market (by Product), $Million, 2024, 2028, and 2033

- Figure 5: Global Smart Harvest Market, Recent Developments

- Figure 6: Supply Chain and Risks within the Supply Chain

- Figure 7: Global Smart Harvest Market, Global Pricing Snapshot, by Product, $/Unit, 2024, 2028, and 2033

- Figure 8: Patent Analysis (by Country), January 2021 and December 2023

- Figure 9: Patent Analysis (by Company), January 2021 and December 2023

- Figure 10: U.S. Smart Harvest Market, $Million, 2023-2033

- Figure 11: Canada Smart Harvest Market, $Million, 2023-2033

- Figure 12: Mexico Smart Harvest Market, $Million, 2023-2033

- Figure 13: Germany Smart Harvest Market, $Million, 2023-2033

- Figure 14: France Smart Harvest Market, $Million, 2023-2033

- Figure 15: Italy Smart Harvest Market, $Million, 2023-2033

- Figure 16: Spain Smart Harvest Market, $Million, 2023-2033

- Figure 17: U.K. Smart Harvest Market, $Million, 2023-2033

- Figure 18: Rest-of-Europe Smart Harvest Market, $Million, 2023-2033

- Figure 19: China Smart Harvest Market, $Million, 2023-2033

- Figure 20: Japan Smart Harvest Market, $Million, 2023-2033

- Figure 21: South Korea Smart Harvest Market, $Million, 2023-2033

- Figure 22: India Smart Harvest Market, $Million, 2023-2033

- Figure 23: Rest-of-Asia-Pacific Smart Harvest Market, $Million, 2023-2033

- Figure 24: Middle East and Africa Smart Harvest Market, $Million, 2023-2033

- Figure 25: South America Smart Harvest Market, $Million, 2023-2033

- Figure 26: Strategic Initiatives, 2021-2023

- Figure 27: Share of Strategic Initiatives, 2021-2023

- Figure 28: Data Triangulation

- Figure 29: Top-Down and Bottom-Up Approach

- Figure 30: Assumptions and Limitations

List of Tables

- Table 1: Market Snapshot

- Table 2: Smart Harvest Market, Opportunities across Regions

- Table 3: Impact Analysis of Market Navigating Factors, 2023-2033

- Table 4: Technical Parameters Comparison for Smart Harvesters

- Table 5: Global Smart Harvest Market (by Region), $Million, 2023-2033

- Table 6: North America Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 7: North America Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 8: North America Smart Harvest Market (by Product), $Million, 2023-2033

- Table 9: U.S. Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 10: U.S. Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 11: U.S. Smart Harvest Market (by Product), $Million, 2023-2033

- Table 12: Canada Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 13: Canada Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 14: Canada Smart Harvest Market (by Product), $Million, 2023-2033

- Table 15: Mexico Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 16: Mexico Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 17: Mexico Smart Harvest Market (by Product), $Million, 2023-2033

- Table 18: Europe Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 19: Europe Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 20: Europe Smart Harvest Market (by Product), $Million, 2023-2033

- Table 21: Germany Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 22: Germany Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 23: Germany Smart Harvest Market (by Product), $Million, 2023-2033

- Table 24: France Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 25: France Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 26: France Smart Harvest Market (by Product), $Million, 2023-2033

- Table 27: Italy Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 28: Italy Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 29: Italy Smart Harvest Market (by Product), $Million, 2023-2033

- Table 30: Spain Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 31: Spain Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 32: Spain Smart Harvest Market (by Product), $Million, 2023-2033

- Table 33: U.K. Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 34: U.K. Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 35: U.K. Smart Harvest Market (by Product), $Million, 2023-2033

- Table 36: Rest-of-Europe Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 37: Rest-of-Europe Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 38: Rest-of-Europe Smart Harvest Market (by Product), $Million, 2023-2033

- Table 39: Asia-Pacific Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 40: Asia-Pacific Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 41: Asia-Pacific Smart Harvest Market (by Product), $Million, 2023-2033

- Table 42: China Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 43: China Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 44: China Smart Harvest Market (by Product), $Million, 2023-2033

- Table 45: Japan Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 46: Japan Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 47: Japan Smart Harvest Market (by Product), $Million, 2023-2033

- Table 48: South Korea Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 49: South Korea Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 50: South Korea Smart Harvest Market (by Product), $Million, 2023-2033

- Table 51: India Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 52: India Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 53: India Smart Harvest Market (by Product), $Million, 2023-2033

- Table 54: Rest-of-Asia-Pacific Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 55: Rest-of-Asia-Pacific Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 56: Rest-of-Asia-Pacific Smart Harvest Market (by Product), $Million, 2023-2033

- Table 57: Rest-of-the-World Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 58: Rest-of-the-World Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 59: Rest-of-the-World Smart Harvest Market (by Product), $Million, 2023-2033

- Table 60: Middle East and Africa Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 61: Middle East and Africa Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 62: Middle East and Africa Smart Harvest Market (by Product), $Million, 2023-2033

- Table 63: South America Smart Harvest Market (by Site of Operation), $Million, 2023-2033

- Table 64: South America Smart Harvest Market (by Crop Type), $Million, 2023-2033

- Table 65: South America Smart Harvest Market (by Product), $Million, 2023-2033

- Table 66: Market Share, Robotic Harvester Manufacturers, 2023

- Table 67: Market Share, Smart Harvester Manufacturers, 2023

Smart Harvest Market Overview

The global smart harvest market is projected to reach $10,927.7 million by 2033 from $4,729.5 million in 2023, growing at a CAGR of 8.34% during the forecast period 2024-2033.

The smart harvest market is poised for exponential growth. With the global transition toward sustainable agriculture and the integration of advanced technologies in farming, an unprecedented demand for cutting-edge smart harvest solutions arises. Technological advancements, including artificial intelligence and machine learning, are set to revolutionize harvesting processes, offering unparalleled accuracy and efficiency. Furthermore, escalating governmental initiatives worldwide aimed at promoting sustainable agriculture and ensuring food security are expected to drive substantial investments in smart harvest technologies. This creates a dynamic landscape wherein vendors continually innovate to push the boundaries of harvesting capabilities, ultimately ensuring enhanced productivity, efficiency, and sustainability in agricultural practices worldwide.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2024 - 2033 |

| 2024 Evaluation | $5,314.1 Million |

| 2033 Forecast | $10,927.7 Million |

| CAGR | 8.34% |

Introduction to Smart Harvest

The smart harvest market includes cutting-edge agricultural technologies and methods designed to optimize the harvesting process through automation and data-driven decision-making. This market incorporates advanced systems such as robotic harvesters, smart harvesters, and dynamic monitoring software, which together improve the efficiency, precision, and sustainability of agricultural operations. By utilizing artificial intelligence (AI), machine learning, and real-time analytics, smart harvest solutions tackle significant issues such as labor shortages, crop yield variability, and resource management.

Market Introduction

The smart harvest market is rapidly advancing, driven by the need to enhance productivity while minimizing labor costs and human effort. This market is experiencing increased use of autonomous harvesting equipment, along with the integration of sensors and drones. These technological advancements help mitigate issues such as rising crop losses due to improper harvesting and the high cost of labor. Nonetheless, the market faces challenges such as the high expense of advanced technologies and the slow adoption rate in developing countries. Despite these obstacles, government initiatives promoting sustainable agriculture and food security, including significant funding for research and technology development, are propelling growth. Moreover, the introduction of scalable harvesting technologies designed for small-scale farms is making advanced solutions more accessible, further boosting market expansion.

Industrial Impact

The smart harvest market has a profound impact on the agricultural industry, driving significant advancements in productivity, efficiency, and sustainability. The integration of cutting-edge technologies, such as artificial intelligence (AI), machine learning, and advanced robotics, is revolutionizing traditional harvesting processes. These technologies enable precise and efficient harvesting, reducing labor costs and minimizing crop losses. Additionally, real-time analytics and data-driven decision-making enhance resource management and yield optimization. The global emphasis on sustainable agriculture and food security is further propelling the adoption of smart harvest solutions, with substantial governmental investments fostering innovation and market growth. This technological shift not only addresses labor shortages and resource challenges but also positions the agricultural sector for long-term sustainability and resilience. Consequently, the smart harvest market is poised to reshape the industrial landscape, driving economic growth and ensuring food security for future generations.

Market Segmentation

Segmentation 1: by Site of Operation

- On Field

- Controlled Environment

- Greenhouses

- Indoor Farms

On-Field to Lead the Market (by Site of Operation)

Smart harvest technologies are revolutionizing on-field agricultural practices with advanced robotics and AI, enhancing efficiency and precision in crop harvesting. Utilizing automated machinery and sophisticated sensors, these innovations reduce labor costs and improve yield and quality. Key market players are developing autonomous harvesters and integrating smart sensors and drones to optimize operations. This shift addresses labor shortages and supports sustainable farming by minimizing waste and maximizing resources. The on-field application of these technologies drives market growth, driven by the demand for increased productivity and higher-quality produce.

Segmentation 2: by Crop Type

- Grain Crops

- Fruits and Vegetables

- Others

Grain Crops to Hold the Largest Share in the Market (by Crop Type)

Grain crops dominate the smart harvest market, driven by smart harvesting solutions such as autonomous combines and precision agriculture tools. Utilizing AI, IoT, and GPS, these technologies optimize harvesting through real-time monitoring, precise yield mapping, and efficient resource allocation. This reduces labor costs and enhances output quality. Leading agricultural tech companies are heavily investing in R&D to address labor shortages and sustainability challenges in grain farming. The demand for higher efficiency and productivity propels the adoption of smart harvest technologies, solidifying grain crops as the market's leading segment.

Segmentation 3: by Product

- Robotic Harvester

- Smart Harvester

- Self-Propelled

- Tractor Mounted

- Harvest Dynamic Monitoring

Smart Harvester to Lead the Market (by Product)

Smart harvesters, including tractor-mounted and self-propelled models, are revolutionizing agriculture by enhancing efficiency and productivity with AI, IoT, and GPS technologies. These machines optimize harvesting, enable precise crop selection, and reduce labor costs. Tractor-mounted models offer cost-effective flexibility for smaller farms, while self-propelled versions provide high efficiency for large-scale operations. Significant industry investment in R&D is driving innovation to meet the demand for precision agriculture. Consequently, smart harvesters are essential in modern farming, boosting yields, improving crop quality, and supporting sustainable practices.

Segmentation 4: by Region

- North America

- Europe

- Asia-Pacific

- Rest-of-the-World

Europe Region to Lead the Market (by Region)

Europe leads the smart harvest market, driven by technological advancements and the demand for efficient agricultural practices. Robust infrastructure supports IoT, AI, and robotics integration, boosting productivity and resource management. Germany, the U.K., and France spearhead this growth through significant R&D investments, supportive government policies, technological innovations, and farmer education on smart harvesting benefits. Key growth drivers include labor shortages, the need for precision agriculture, and sustainability goals. Strategic collaborations between tech firms and agricultural businesses further propel market expansion.

Recent Developments in Smart Harvest Market

- In July 2022, the Washington Tree Fruit Research Commission granted funding to Advanced Farm Technologies, Inc. to aid in the development of a robotic apple harvester.

- In November 2023, Organifarms GmbH and EBZ Group announced a partnership. EBZ Group's expertise provides Organifarms GmbH with ideal opportunities to scale its picking robots.

- In February 2024, Deere & Company unveiled the S7 Series of combines, a new series of harvesters engineered for enhanced efficiency, superior harvest quality, and user-friendly operation.

Demand - Drivers, Restraints, and Opportunities

Market Demand Driver - The Need for Maximizing Productivity while Reducing Labor Costs and Human Effort

The imperative to maximize productivity while minimizing labor costs and human effort is a key driver in the smart harvest market. Modern agricultural operations face significant challenges, including labor shortages and increasing operational costs. Smart harvest technologies, such as autonomous harvesters, precision agriculture tools, and integrated IoT systems, offer innovative solutions to these issues. By leveraging AI and real-time analytics, these technologies enable precise and efficient harvesting, reducing the dependency on manual labor. Autonomous systems can operate continuously, improving overall productivity and ensuring optimal use of resources. Additionally, smart harvest solutions enhance crop quality by accurately identifying the optimal time for harvesting, thereby reducing waste and increasing marketable yield. Investment in these technologies is not only a strategic response to labor market constraints but also a pathway to sustainable farming practices.

Market Restraint - High-Cost Factor Hindering the Growth of the Market

The high cost of smart harvest technologies remains a significant barrier to market growth. Advanced systems, including autonomous harvesters, precision agriculture tools, and integrated IoT solutions, require substantial upfront investment. This financial burden can be prohibitive, especially for small to mid-sized farms with limited capital. Additionally, the costs associated with ongoing maintenance, software updates, and operator training further strain financial resources. While large agricultural enterprises may absorb these expenses, smaller operations struggle to justify the investment against their narrow profit margins.

Moreover, the return on investment (ROI) for these technologies, although promising in the long term, can be slow to materialize, deterring widespread adoption. To address these challenges, stakeholders must explore financing options such as government subsidies, grants, and innovative leasing models.

Market Opportunity - Government Initiatives to Promote Sustainable Agriculture and Food Security

Government initiatives play a pivotal role in promoting sustainable agriculture and food security, thereby driving the growth of the smart harvest market. Numerous governments worldwide are introducing policies and funding programs aimed at encouraging the adoption of advanced agricultural technologies. These initiatives often include subsidies, grants, and tax incentives for farmers investing in smart harvest solutions such as autonomous harvesters, precision agriculture tools, and IoT-integrated systems. By easing the financial burden, these measures facilitate the transition to more efficient and sustainable farming practices.

Educational programs and training sessions are also being implemented to raise awareness and enhance farmers' skills in utilizing these advanced technologies. These concerted efforts are instrumental in ensuring food security, improving crop yields, and promoting environmental sustainability, thereby significantly bolstering the smart harvest market.

How can this Report add value to an Organization?

Product/Innovation Strategy: This report provides a comprehensive product/innovation strategy for the smart harvest market, identifying opportunities for market entry, technology adoption, and sustainable growth. It offers actionable insights, helping organizations leverage smart harvest to meet environmental standards, gain a competitive edge, and capitalize on the increasing demand for eco-friendly solutions in agriculture.

Growth/Marketing Strategy: This report offers a comprehensive growth and marketing strategy designed specifically for the smart harvest market. It presents a targeted approach to identifying specialized market segments, establishing a competitive advantage, and implementing creative marketing initiatives aimed at optimizing market share and financial performance. By harnessing these strategic recommendations, organizations can elevate their market presence, seize emerging prospects, and efficiently propel revenue expansion.

Competitive Strategy: This report crafts a strong competitive strategy tailored to the smart harvest market. It evaluates market rivals, suggests methods to stand out, and offers guidance for maintaining a competitive edge. By adhering to these strategic directives, companies can position themselves effectively in the face of market competition, ensuring sustained prosperity and profitability.

Research Methodology

Factors for Data Prediction and Modeling

- The scope of this report focuses on several types of smart harvest applications and products.

- The base currency considered for the market analysis is US$. Currencies other than the US$ have been converted to the US$ for all statistical calculations, considering the average conversion rate for that particular year.

- The currency conversion rate has been taken from the historical exchange rate of the Oanda website.

- Nearly all the recent developments from January 2021 to March 2024 have been considered in this research study.

- The information rendered in the report is a result of in-depth primary interviews, surveys, and secondary analysis.

- Where relevant information was not available, proxy indicators and extrapolation were employed.

- Any economic downturn in the future has not been taken into consideration for the market estimation and forecast.

- Technologies currently used are expected to persist through the forecast with no major breakthroughs in technology.

Market Estimation and Forecast

This research study involves the usage of extensive secondary sources, such as certified publications, articles from recognized authors, white papers, annual reports of companies, directories, and major databases to collect useful and effective information for an extensive, technical, market-oriented, and commercial study of the global smart harvest market.

The process of market engineering involves the calculation of the market statistics, market size estimation, market forecast, market crackdown, and data triangulation (the methodology for such quantitative data processes is explained in further sections). The primary research study has been undertaken to gather information and validate the market numbers for segmentation types and industry trends of the key players in the market.

Primary Research

The primary sources involve industry experts from the smart harvest market and various stakeholders in the ecosystem. Respondents such as CEOs, vice presidents, marketing directors, and technology and innovation directors have been interviewed to obtain and verify both qualitative and quantitative aspects of this research study.

The key data points taken from primary sources include:

- validation and triangulation of all the numbers and graphs

- validation of reports segmentation and key qualitative findings

- understanding the competitive landscape

- validation of the numbers of various markets for market type

- percentage split of individual markets for geographical analysis

Secondary Research

This research study of the smart harvest market involves the usage of extensive secondary research, directories, company websites, and annual reports. It also makes use of databases, such as Hoovers, Bloomberg, Businessweek, and Factiva, to collect useful and effective information for an extensive, technical, market-oriented, and commercial study of the global market.

Secondary research was done in order to obtain crucial information about the industry's value chain, revenue models, the market's monetary chain, the total pool of key players, and the current and potential use cases and applications.

The key data points taken from secondary research include:

- segmentations and percentage shares

- data for market value

- key industry trends of the top players of the market

- qualitative insights into various aspects of the market, key trends, and emerging areas of innovation

- quantitative data for mathematical and statistical calculations

Key Market Players and Competition Synopsis

The companies that are profiled in the smart harvest market have been selected based on inputs gathered from primary experts and analyzing company coverage, product portfolio, and market penetration.

Some of the prominent names in this market are:

- Agrobot

- Dogtooth Technologies Limited

- FFRobotics

- OCTINION

- Harvest CROO Robotics LLC

- Advanced Farm Technologies, Inc.

- MetoMotion

- Mycionics Inc.

- Tortuga Agricultural Technologies, Inc.

- Organifarms GmbH

- Tevel Aerobotics Technologies

- AVL Motion B.V.

- Fieldwork Robotics

- AMB Rousset

- Deere & Company

Companies that are not a part of the aforementioned pool have been well represented across different sections of the report (wherever applicable).

Table of Contents

Executive Summary

Scope and Definition

1 Markets

- 1.1 Trends: Current and Future Impact Assessment

- 1.1.1 Trends: Current and Future Impact Assessment

- 1.1.1.1 Advancements in Satellite Imaging Technologies to Forecast Harvest Yield and Potential Disruptions

- 1.1.1.2 Introduction of Agriculture 4.0

- 1.1.1 Trends: Current and Future Impact Assessment

- 1.2 Supply Chain Overview

- 1.2.1 Value Chain Analysis

- 1.2.2 Market Map

- 1.2.2.1 Global Smart Harvest Market- by Product

- 1.2.2.1.1 Robotic Harvester

- 1.2.2.1.2 Smart Harvester

- 1.2.2.1.3 Harvest Dynamic Monitoring

- 1.2.2.1 Global Smart Harvest Market- by Product

- 1.2.3 Pricing Forecast

- 1.3 Research and Development Review

- 1.3.1 Patent Filing Trend (by Country and Company)

- 1.4 Regulatory Landscape

- 1.5 Stakeholder Analysis

- 1.5.1 Use Case

- 1.5.1.1 Use Case Examination:

- 1.5.1.1.1 Feil Agriculture & Service

- 1.5.1.1.2 Automation of Crop Yield Assessment:

- 1.5.1.1.3 Flaskamp Contracting Business

- 1.5.1.1.4 Deere & Company X9 Combine - Working Smarter, Not Harder

- 1.5.1.1.5 Deere & Company X9 1000 Combine - Revolutionizing Smart Harvest

- 1.5.1.1.6 Deere & Company X9 1000 Combine - Enhancing Harvest Efficiency in Crystal Brook

- 1.5.1.1.7 Deere & Company Operations Center - Empowering Data-Driven Decisions

- 1.5.1.1.8 Augmenta NVRA - Enhancing Efficiency in the Smart Harvest Market

- 1.5.1.1.9 Analyst View

- 1.5.1.1 Use Case Examination:

- 1.5.1 Use Case

- 1.6 Market Dynamics: Overview

- 1.6.1 Market Drivers

- 1.6.1.1 Need for Maximizing Productivity While Reducing Labor Costs and Human Effort

- 1.6.1.2 Increasing Adoption of Autonomous Harvesting Equipment and Integration of Sensors and Drones

- 1.6.1.3 Rising Crop Losses Caused by Improper Harvesting Practices

- 1.6.2 Market Restraints

- 1.6.2.1 High-Cost Factor Hindering the Growth of the Market

- 1.6.2.2 Slow Rate of Adoption in Developing Countries

- 1.6.3 Market Opportunities

- 1.6.3.1 Government Initiatives to Promote Sustainable Agriculture and Food Security

- 1.6.3.2 Introduction of Scalable Harvesting Technologies for Small Scale Farms

- 1.6.1 Market Drivers

- 1.7 Architectural/Technical Comparison of Key Products in the Market

2 Application

- 2.1 Application Segmentation

- 2.2 Application Summary

- 2.3 Global Smart Harvest Market (by Site of Operation)

- 2.3.1 Site of Operation

- 2.3.1.1 On-Field

- 2.3.1.2 Controlled Environment

- 2.3.1.2.1 Greenhouses

- 2.3.1.2.2 Indoor Farms

- 2.3.1 Site of Operation

- 2.4 Application Segmentation

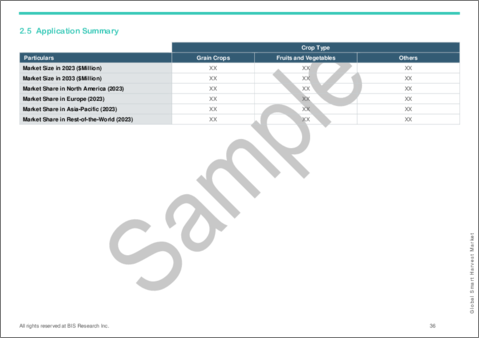

- 2.5 Application Summary

- 2.6 Global Smart Harvest Market (by Crop Type)

- 2.6.1 Crop Type

- 2.6.1.1 Grain Crops

- 2.6.1.2 Fruits and Vegetables

- 2.6.1.3 Others

- 2.6.1 Crop Type

3 Products

- 3.1 Product Segmentation

- 3.2 Product Summary

- 3.3 Global Smart Harvest Market (by Product)

- 3.3.1 Robotic Harvester

- 3.3.2 Smart Harvester

- 3.3.2.1 Tractor Mounted

- 3.3.2.2 Self Propelled

- 3.3.3 Harvest Dynamic Monitoring

4 Regions

- 4.1 Regional Summary

- 4.2 Drivers and Restraints

- 4.3 North America

- 4.3.1 Regional Overview

- 4.3.2 Driving Factors for Market Growth

- 4.3.3 Factors Challenging the Market

- 4.3.4 Application

- 4.3.5 Product

- 4.3.6 U.S.

- 4.3.6.1 Application

- 4.3.6.2 Product

- 4.3.7 Canada

- 4.3.7.1 Application

- 4.3.7.2 Product

- 4.3.8 Mexico

- 4.3.8.1 Application

- 4.3.8.2 Product

- 4.4 Europe

- 4.4.1 Regional Overview

- 4.4.2 Driving Factors for Market Growth

- 4.4.3 Factors Challenging the Market

- 4.4.4 Application

- 4.4.5 Product

- 4.4.6 Germany

- 4.4.6.1 Application

- 4.4.6.2 Product

- 4.4.7 France

- 4.4.7.1 Application

- 4.4.7.2 Product

- 4.4.8 Italy

- 4.4.8.1 Application

- 4.4.8.2 Product

- 4.4.9 Spain

- 4.4.9.1 Application

- 4.4.9.2 Product

- 4.4.10 U.K.

- 4.4.10.1 Application

- 4.4.10.2 Product

- 4.4.11 Rest-of-Europe

- 4.4.11.1 Application

- 4.4.11.2 Product

- 4.5 Asia-Pacific

- 4.5.1 Regional Overview

- 4.5.2 Driving Factors for Market Growth

- 4.5.3 Factors Challenging the Market

- 4.5.4 Application

- 4.5.5 Product

- 4.5.6 China

- 4.5.6.1 Application

- 4.5.6.2 Product

- 4.5.7 Japan

- 4.5.7.1 Application

- 4.5.7.2 Product

- 4.5.8 South Korea

- 4.5.8.1 Application

- 4.5.8.2 Product

- 4.5.9 India

- 4.5.9.1 Application

- 4.5.9.2 Product

- 4.5.10 Rest-of-Asia-Pacific

- 4.5.10.1 Application

- 4.5.10.2 Product

- 4.6 Rest-of-the-World

- 4.6.1 Regional Overview

- 4.6.2 Driving Factors for Market Growth

- 4.6.3 Factors Challenging the Market

- 4.6.4 Application

- 4.6.5 Product

- 4.6.6 Middle East and Africa (MEA)

- 4.6.6.1 Application

- 4.6.6.2 Product

- 4.6.7 South America

- 4.6.7.1 Application

- 4.6.7.2 Product

5 Markets - Competitive Benchmarking & Company Profiles

- 5.1 Next Frontiers

- 5.2 Geographic Assessment

- 5.2.1 Agrobot

- 5.2.1.1 Overview

- 5.2.1.2 Top Products/Product Portfolio

- 5.2.1.3 Top Competitors

- 5.2.1.4 Target Customers

- 5.2.1.5 Key Personnel

- 5.2.1.6 Analyst View

- 5.2.1.7 Market Share, 2023

- 5.2.2 Dogtooth Technologies Limited

- 5.2.2.1 Overview

- 5.2.2.2 Top Products/Product Portfolio

- 5.2.2.3 Top Competitors

- 5.2.2.4 Target Customers

- 5.2.2.5 Key Personnel

- 5.2.2.6 Analyst View

- 5.2.2.7 Market Share, 2023

- 5.2.3 FFRobotics

- 5.2.3.1 Overview

- 5.2.3.2 Top Products/Product Portfolio

- 5.2.3.3 Top Competitors

- 5.2.3.4 Target Customers

- 5.2.3.5 Key Personnel

- 5.2.3.6 Analyst View

- 5.2.3.7 Market Share, 2023

- 5.2.4 OCTINION

- 5.2.4.1 Overview

- 5.2.4.2 Top Products/Product Portfolio

- 5.2.4.3 Top Competitors

- 5.2.4.4 Target Customers

- 5.2.4.5 Key Personnel

- 5.2.4.6 Analyst View

- 5.2.5 Harvest CROO Robotics LLC

- 5.2.5.1 Overview

- 5.2.5.2 Top Products/Product Portfolio

- 5.2.5.3 Top Competitors

- 5.2.5.4 Target Customers

- 5.2.5.5 Key Personnel

- 5.2.5.6 Analyst View

- 5.2.5.7 Market Share, 2023

- 5.2.6 Advanced Farm Technologies, Inc.

- 5.2.6.1 Overview

- 5.2.6.2 Top Products/Product Portfolio

- 5.2.6.3 Top Competitors

- 5.2.6.4 Target Customers

- 5.2.6.5 Key Personnel

- 5.2.6.6 Analyst View

- 5.2.6.7 Market Share, 2023

- 5.2.7 MetoMotion

- 5.2.7.1 Overview

- 5.2.7.2 Top Products/Product Portfolio

- 5.2.7.3 Top Competitors

- 5.2.7.4 Target Customers

- 5.2.7.5 Key Personnel

- 5.2.7.6 Analyst View

- 5.2.7.7 Market Share, 2023

- 5.2.8 Mycionics Inc.

- 5.2.8.1 Overview

- 5.2.8.2 Top Products/Product Portfolio

- 5.2.8.3 Top Competitors

- 5.2.8.4 Target Customers

- 5.2.8.5 Key Personnel

- 5.2.8.6 Analyst View

- 5.2.8.7 Market Share, 2023

- 5.2.9 Tortuga Agricultural Technologies, Inc.

- 5.2.9.1 Overview

- 5.2.9.2 Top Products/Product Portfolio

- 5.2.9.3 Top Competitors

- 5.2.9.4 Target Customers

- 5.2.9.5 Key Personnel

- 5.2.9.6 Analyst View

- 5.2.10 Organifarms GmbH

- 5.2.10.1 Overview

- 5.2.10.2 Top Products/Product Portfolio

- 5.2.10.3 Top Competitors

- 5.2.10.4 Target Customers

- 5.2.10.5 Key Personnel

- 5.2.10.6 Analyst View

- 5.2.11 Tevel Aerobotics Technologies

- 5.2.11.1 Overview

- 5.2.11.2 Top Products/Product Portfolio

- 5.2.11.3 Top Competitors

- 5.2.11.4 Target Customers

- 5.2.11.5 Key Personnel

- 5.2.11.6 Analyst View

- 5.2.11.7 Market Share, 2023

- 5.2.12 AVL Motion B.V.

- 5.2.12.1 Overview

- 5.2.12.2 Top Products/Product Portfolio

- 5.2.12.3 Top Competitors

- 5.2.12.4 Target Customers

- 5.2.12.5 Key Personnel

- 5.2.12.6 Analyst View

- 5.2.13 Fieldwork Robotics

- 5.2.13.1 Overview

- 5.2.13.2 Top Products/Product Portfolio

- 5.2.13.3 Top Competitors

- 5.2.13.4 Target Customers

- 5.2.13.5 Key Personnel

- 5.2.13.6 Analyst View

- 5.2.14 AMB Rousset

- 5.2.14.1 Overview

- 5.2.14.2 Top Products/Product Portfolio

- 5.2.14.3 Top Competitors

- 5.2.14.4 Target Customers

- 5.2.14.5 Key Personnel

- 5.2.14.6 Analyst View

- 5.2.14.7 Market Share, 2023

- 5.2.15 Deere & Company

- 5.2.15.1 Overview

- 5.2.15.2 Top Products/Product Portfolio

- 5.2.15.3 Top Competitors

- 5.2.15.4 Target Customers

- 5.2.15.5 Key Personnel

- 5.2.15.6 Analyst View

- 5.2.15.7 Market Share, 2023

- 5.2.1 Agrobot

6 Research Methodology

- 6.1 Data Sources

- 6.1.1 Primary Data Sources

- 6.1.2 Secondary Data Sources

- 6.1.3 Data Triangulation

- 6.2 Market Estimation and Forecast