|

|

市場調査レポート

商品コード

1426156

持続可能な包装の世界市場 - 見通しと予測(2024年~2029年)Sustainable Packaging Market - Global Outlook & Forecast 2024-2029 |

||||||

|

|||||||

|

|||||||

| 持続可能な包装の世界市場 - 見通しと予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Arizton Advisory & Intelligence

ページ情報: 英文 333 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

世界の持続可能な包装の市場規模は、2023年までに3,196億2,000万米ドルとなり、2023年~2029年にCAGRで7.44%の成長が予測されています。

市場の動向と促進要因

eコマース産業の成長

環境に対するeコマース市場の成長、特に持続可能な包装の文脈における成長は、近年大きく勢いを増している多面的な動向です。オンラインショッピングの人気がますます高まっていることが、この動向の主な促進要因となっています。自宅にいながらにして商品を購入できる利便性から、消費者は以前にも増してeコマースプラットフォームを利用するようになっています。このようなオンラインショッピングの急増は、消費者の玄関先まで商品を安全に配送するための包装材の需要につながっています。しかし、この成長はまた、プラスチックや段ボールの過剰使用など、従来の包装材の影響に注目させることにもつながっています。消費者の環境意識はますます高まり、持続可能で環境にやさしい包装オプションを積極的に求めるようになっています。その結果、eコマース企業は、消費者の期待に応え、カーボンフットプリントを削減するために、包装方法を持続可能性目標に合わせる必要性を認識しています。こうした要因が持続可能な包装市場の成長を支えると予測されます。

最終用途におけるパウチ包装の増加

利便性とシングルサーブ包装への需要が、さまざまな最終用途におけるパウチ包装の採用を可能にしています。さまざまな産業におけるパウチ包装の急増は、持続可能な包装市場の有力な促進要因です。パウチ包装は、その環境にやさしい特性と多くの利点により人気を博しています。軟質パウチ包装は、金属、ガラス、硬質プラスチック包装に取って代わるものです。硬質包装製品に比べたパウチ包装の使いやすさと費用対効果の高さに加え、包装された食品・飲料への需要が、主に世界中で需要を促進しています。パウチは場所をとらず軽量です。さらに、パウチは金属缶やガラス瓶のような硬質包装に比べ輸送関連コストを削減します。

地域の分析

欧州が2023年に世界の持続可能な包装市場でもっとも高いシェアを占めました。欧州市場は、使い捨てプラスチックの使用と持続可能性に関する消費者の意識の高まりと厳しい政府規制により、大きな成長を示しています。欧州の消費者は、持続可能な製品や包装へと選好をますますシフトさせています。European Consumer Packaging Perceptions Studyでは、回答者の約3分の2が包装への懸念から購入する製品を変更したことがわかっています。さらに、全消費者の4分の3超が、環境に配慮した包装のためならより高い金額を支払うことを望んでいます。その上、欧州では政府の厳しい規制がグリーン包装の需要を後押ししています。これらの規制は、使い捨てプラスチックを削減し、より持続可能な代替包装を促進することを目的としています。このような規制環境が、環境にやさしい包装オプションの成長に寄与しています。

競合情勢

世界の持続可能な包装市場は、世界の環境保全と企業の社会的責任の重視に後押しされ、ダイナミックで競争の激しい情勢を見せています。世界の持続可能な包装市場の主要企業には、Amcor、Tetra Pak International、Ball Corporationなどの多国籍企業が含まれ、豊富なリソースとイノベーション能力を活用して環境にやさしい包装ソリューションを開発しています。さらに、Ecover、Eco-Products、NatureWorksのようなニッチ企業も、特化した製品で競合に寄与しています。包装メーカーと消費財メーカーとの提携やパートナーシップは、包括的なエンドツーエンドの持続可能な包装ソリューションの開発を促進し、競合をさらに激化させています。

当レポートでは、世界の持続可能な包装市場について調査分析し、市場規模と予測、機会と動向、主要企業などの情報を提供しています。

目次

第1章 調査対象・調査範囲

- 市場の定義

- 対象となるセグメントと定義

- 市場の導出

第2章 重要考察

- 機会ポケット

- レポートの概要

- セグメント分析

- 考察:材料別

- 考察:包装タイプ別

- 考察:プロセス別

- 考察:用途別

- 地域の分析

- 競合情勢

第3章 市場の概要

第4章 イントロダクション

- 概要

- 包装産業

- 包装の層

- 予測される2050年までの影響

- イノベーションと買収

- 循環経済

- バリューチェーン分析

- 原材料

- 製造

- 流通

- 小売

- リサイクル・堆肥化

- EOL

- 専門家の意見

第5章 市場の機会と動向

- eコマース産業の成長

- 持続可能な軟質包装へのさらなる注目

- 再使用可能な包装の増加

- 改質雰囲気包装製品への移行

第6章 市場成長の実現要因

- 加工食品と包装食品の増加

- 市場の長を促進する効率的なサプライチェーン

- 最終用途におけるパウチ包装の増加

第7章 市場抑制要因

- 規制遵守と基準

- 上昇する原材料のコスト

- 高い運用コスト

第8章 市場情勢

- 市場の概要

- 市場規模と予測

- 原材料

- 市場の危険因子

- ファイブフォース分析

第9章 材料

- 市場のスナップショットと成長促進要因

- 市場の概要

- 紙・板紙

- プラスチック

- 金属

- ガラス

第10章 包装形式

- 市場のスナップショットと成長促進要因

- 市場の概要

- 硬質

- 軟質

第11章 プロセス

- 市場のスナップショットと成長促進要因

- 市場の概要

- リサイクル可能

- 分解性

- 再使用可能

第12章 用途

- 市場のスナップショットと成長促進要因

- 市場の概要

- 食品・飲料

- パーソナルケア・化粧品

- 医療・製薬

- eコマース・小売

- その他

第13章 地域

- 市場のスナップショットと成長促進要因

- 地理的な概要

第14章 欧州

- 市場の概要

- 市場規模と予測

- 材料

- 包装形式

- プロセス

- 用途

- 主要国

- ドイツの市場規模と予測

- 英国の市場規模と予測

- フランスの市場規模と予測

- イタリアの市場規模と予測

- スペインの市場規模と予測

- ロシアの市場規模と予測

- ベネルクス:市場規模と予測

第15章 北米

- 市場の概要

- 市場規模と予測

- 材料

- 包装形式

- 用途

- プロセス

- 主要国

- 米国の市場規模と予測

- カナダの市場規模と予測

第16章 アジア太平洋

- 市場の概要

- 市場規模と予測

- 材料

- 包装形式

- プロセス

- 用途

- 主要国

- 中国の市場規模と予測

- インドの市場規模と予測

- 日本の市場規模と予測

- オーストラリアの市場規模と予測

- 韓国の市場規模と予測

- ニュージーランドの市場規模と予測

- その他のアジア太平洋の市場規模と予測

第17章 ラテンアメリカ

- 市場の概要

- 市場規模と予測

- 材料

- 包装形式

- プロセス

- 用途

- 主要国

- ブラジルの市場規模と予測

- メキシコの市場規模と予測

- アルゼンチンの市場規模と予測

第18章 中東・アフリカ

- 市場の概要

- 市場規模と予測

- 材料

- 包装形式

- プロセス

- 用途

- 主要国

- サウジアラビアの市場規模と予測

- アラブ首長国連邦の市場規模と予測

- エジプトの市場規模と予測

- イスラエル:市場規模と予測

- 南アフリカの市場規模と予測

第19章 競合情勢

- 競合の概要

第20章 主要企業プロファイル

- AMCOR

- ARDAGH GROUP

- BALL CORPORATION

- BILLERUD

- CROWN HOLDINGS

- DS SMITH

- INTERNATIONAL PAPER

- HUHTAMAKI

- MONDI

- SONOCO PRODUCTS COMPANY

- SEALED AIR CORPORATION

- SMURFIT KAPPA

- WESTROCK

第21章 その他の著名なベンダー

- AHLSTROM

- BERRY GLOBAL

- BOTANICAL PAPERWORKS

- BE GREEN PACKAGING

- CONSTANTIA FLEXIBLES

- DUPONT

- EVERGREEN RESOURCES

- ECOENCLOSE

- ELEVATE PACKAGING

- FUTAMURA GROUP

- GENPAK

- GRAPHIC PACKAGING INTERNATIONAL

- LIMELOOP

- NAMPAK

- NOTPLA

- NOVAMONT

- NUMI

- OJI HOLDINGS CORPORATION

- PLASTIPAK HOLDINGS

- PAKFACTORY

- REYNOLDS PACKAGING

- SAPPI

- STORA ENSO

- TAGHLEEF INDUSTRIES

- TETRA PAK

- TRANSCONTINENTAL

- UFLEX

第22章 レポートの概要

- 重要事項

- 戦略的な推奨事項

第23章 量的サマリー

- 市場:地域別

- 市場:材料別

- 市場:包装タイプ別

- 市場:プロセス別

- 市場:用途別

- 欧州

- 北米

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第24章 付録

List Of Exhibits

LIST OF EXHIBITS

- EXHIBIT 1 MARKET SIZE CALCULATION APPROACH 2023

- EXHIBIT 2 REQUISITE CRITERIA FOR COMPLIANCE: SUSTAINABLE PACKAGING

- EXHIBIT 3 MEGATRENDS IN THE PACKAGING INDUSTRY

- EXHIBIT 4 CONCEPT OF CIRCULAR ECONOMY IN SUSTAINABLE PACKAGING MARKET

- EXHIBIT 5 VALUE CHAIN OF SUSTAINABLE PACKAGING MARKET

- EXHIBIT 6 IMPACT OF GROWTH IN E-COMMERCE INDUSTRY

- EXHIBIT 7 KEY FACTS & STATISTICS ABOUT E-COMMERCE INDUSTRY

- EXHIBIT 8 IMPACT OF INCREASED FOCUS ON SUSTAINABLE FLEXIBLE PACKAGING

- EXHIBIT 9 IMPACT OF RISE IN REUSABLE PACKAGING

- EXHIBIT 10 COUNTRIES ENACTING MEASURES TO ADOPT REUSABLE PACKAGING

- EXHIBIT 11 IMPACT OF SHIFT TOWARD MODIFIED ATMOSPHERIC PACKAGING PRODUCTS

- EXHIBIT 12 FACTORS DRIVING MODIFIED ATMOSPHERIC PACKAGING (MAP) PRODUCTS

- EXHIBIT 13 IMPACT OF INCREASE IN PROCESSED AND PACKAGED FOOD

- EXHIBIT 14 IMPACT OF EFFICIENT SUPPLY CHAIN FUELING MARKET GROWTH

- EXHIBIT 15 KEY REASONS OF EFFICIENT SUPPLY CHAIN

- EXHIBIT 16 IMPACT OF INCREASE IN POUCH PACKAGING ACROSS END USERS

- EXHIBIT 17 FACTORS DRIVING THE DEMAND FOR POUCH PACKAGING

- EXHIBIT 18 IMPACT OF REGULATORY COMPLIANCE & STANDARDS

- EXHIBIT 19 REGULATIONS IN NORTH AMERICA REGARDING SUSTAINABLE PACKAGING

- EXHIBIT 20 IMPACT OF RISING COST OF RAW MATERIALS

- EXHIBIT 21 PRODUCER PRICE INDEX: PLASTICS AND RESIN MANUFACTURING 2023

- EXHIBIT 22 IMPACT OF HIGH OPERATIONAL COST

- EXHIBIT 23 GLOBAL SUSTAINABLE PACKAGING MARKET OVERVIEW

- EXHIBIT 24 FUTURE TRENDS IN THE SUSTAINABLE PACKAGING MARKET

- EXHIBIT 25 GLOBAL SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 26 KEY FACTS ABOUT INDONESIA PULP & PAPER INDUSTRY

- EXHIBIT 27 RISK FACTORS IN THE MARKET

- EXHIBIT 28 FIVE FORCES ANALYSIS 2023

- EXHIBIT 29 INCREMENTAL GROWTH BY MATERIAL 2023 & 2029

- EXHIBIT 30 MARKET SHARE (2023) & ABSOLUTE GROWTH 2023-2029 (%)

- EXHIBIT 31 GLOBAL PAPER & PAPERBOARD SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 32 GLOBAL PLASTIC SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 33 AVERAGE ALUMINUM PRICE OUTLOOK 2022-2023 ($ PER TON)

- EXHIBIT 34 GLOBAL METAL SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 35 GLOBAL GLASS SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 36 INCREMENTAL GROWTH BY PACKAGING TYPE 2023 & 2029

- EXHIBIT 37 MARKET SHARE & REVENUE BY PACKAGING TYPE, 2023 ($ BILLION)

- EXHIBIT 38 GLOBAL RIGID SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 39 GLOBAL FLEXIBLE SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 40 INCREMENTAL GROWTH BY PROCESS 2023 & 2029

- EXHIBIT 41 REVENUE GENERATED IN 2023 BY PROCESS & CAGR COMPARISON (2023-2029) (%)

- EXHIBIT 42 GLOBAL RECYCLABLE SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 43 MATERIALS UTILIZED IN PACKAGING AND THEIR APPROXIMATE DEGRADATION TIME

- EXHIBIT 44 GLOBAL DEGRADABLE SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 45 GLOBAL REUSABLE SUSTAINABLE PACKAGING MARKET 2023-2029 ($ BILLION)

- EXHIBIT 46 INCREMENTAL GROWTH BY APPLICATION 2023 & 2029

- EXHIBIT 47 MARKET SHARE & ABSOLUTE GROWTH BY APPLICATION (%)

- EXHIBIT 48 COMPONENTS OF F&B MANUFACTURING: REVENUE 2021

- EXHIBIT 49 GLOBAL F&B SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 50 GLOBAL PERSONAL CARE & COSMETICS SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 51 GLOBAL MEDICAL & PHARMACEUTICAL SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 52 E-COMMERCE SALES IN THE US, 2014-2022, ($ BILLION)

- EXHIBIT 53 E-COMMERCE PENETRATION BY MARKET, 2022

- EXHIBIT 54 GLOBAL E-COMMERCE & RETAIL SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 55 GLOBAL OTHERS SUSTAINABLE PACKAGING MARKET 2023-2029 ($ BILLION)

- EXHIBIT 56 INCREMENTAL GROWTH BY GEOGRAPHY 2023 & 2029

- EXHIBIT 57 INCREMENTAL GROWTH BY GEOGRAPHY 2023-2029 ($ BILLION)

- EXHIBIT 58 MARKET REVENUE BY COUNTRIES IN 2023 ($ BILLION)

- EXHIBIT 59 EUROPE SUSTAINABLE PACKAGING MARKET 2023-2029 ($ BILLION)

- EXHIBIT 60 INCREMENTAL GROWTH IN EUROPE 2023 & 2029

- EXHIBIT 61 GERMANY SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 62 THE UK SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 63 SUSTAINABLE PACKAGING INITIATIVES IN FRANCE

- EXHIBIT 64 FRANCE SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 65 SUSTAINABLE PACKAGING MARKET IN ITALY 2019-2029 ($ BILLION)

- EXHIBIT 66 SOME OF THE SUSTAINABLE PACKAGING INITIATIVES IN SPAIN

- EXHIBIT 67 SPAIN SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 68 RUSSIA SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 69 BENELUX SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 70 ABSOLUTE GROWTH BY COUNTRIES IN NORTH AMERICA 2023-2029 (%)

- EXHIBIT 71 SUSTAINABLE PACKAGING USED IN NORTH AMERICA

- EXHIBIT 72 NORTH AMERICA SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 73 INCREMENTAL GROWTH IN NORTH AMERICA 2023 & 2029

- EXHIBIT 74 THE US SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 75 INITIATIVES & DEVELOPMENTS BY CANADA GOVERNMENT

- EXHIBIT 76 CANADA SUSTAINABLE PACKAGING MARKET 2023-2029 ($ BILLION)

- EXHIBIT 77 INCREMENTAL GROWTH BY COUNTRIES IN APAC 2023-2029 ($ BILLION)

- EXHIBIT 78 APAC SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 79 INCREMENTAL GROWTH IN APAC 2023 & 2029

- EXHIBIT 80 CHINA SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 81 GOVERNMENT PLANS TO BE ACHIEVED BY 2025

- EXHIBIT 82 INDIA SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 83 JAPAN SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 84 AMBITIOUS OBJECTIVES OUTLINED IN THE STRATEGY

- EXHIBIT 85 AUSTRALIA SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 86 AUSTRALIAN'S 2025 NATIONAL PACKAGING TARGETS

- EXHIBIT 87 SOUTH KOREA SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 88 NEW ZEALAND SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 89 SUSTAINABLE PACKAGING MARKET IN THE REST OF APAC 2019-2029 ($ BILLION)

- EXHIBIT 90 KEY HIGHLIGHTS & MARKET REVENUE IN 2023 BY COUNTRIES ($ BILLION)

- EXHIBIT 91 LATIN AMERICA SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 92 INCREMENTAL GROWTH IN LATIN AMERICA 2023 & 2029

- EXHIBIT 93 BRAZIL SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 94 MEXICO SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 95 ARGENTINA SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 96 FACTORS DRIVING THE MARKET IN ARGENTINA

- EXHIBIT 97 MARKET REVENUE BY COUNTRIES IN THE REGION, 2023 ($ BILLION)

- EXHIBIT 98 THE MIDDLE EAST & AFRICA SUSTAINABLE PACKAGING MARKET 2023-2029 ($ BILLION)

- EXHIBIT 99 INCREMENTAL GROWTH IN THE MIDDLE EAST & AFRICA 2023 & 2029

- EXHIBIT 100 SAUDI ARABIA SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 101 THE UAE SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 102 EGYPT SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 103 ISRAEL SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 104 SOUTH AFRICA SUSTAINABLE PACKAGING MARKET 2019-2029 ($ BILLION)

- EXHIBIT 105 MARKET DYNAMICS

- EXHIBIT 106 KEY CAVEATS

List Of Tables

LIST OF TABLES

- TABLE 1 PAPER & PAPERBOARD SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 2 PLASTIC SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 3 METAL SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 4 GLASS SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2019-2029 ($ BILLION)

- TABLE 5 RIGID SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 6 FLEXIBLE SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 7 RECYCLABLE SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 8 DEGRADABLE SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 9 REUSABLE SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 10 F&B SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 11 PERSONAL CARE & COSMETICS SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 12 MEDICAL & PHARMACEUTICAL SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 13 E-COMMERCE & RETAIL SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 14 OTHERS SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 15 EUROPE SUSTAINABLE PACKAGING MARKET BY MATERIAL 2023-2029 ($ BILLION)

- TABLE 16 EUROPE SUSTAINABLE PACKAGING MARKET BY PACKAGING TYPE 2023-2029 ($ BILLION)

- TABLE 17 EUROPE SUSTAINABLE PACKAGING MARKET BY PROCESS 2023-2029 ($ BILLION)

- TABLE 18 EUROPE SUSTAINABLE PACKAGING MARKET BY APPLICATION 2023-2029 ($ BILLION)

- TABLE 19 NORTH AMERICA SUSTAINABLE PACKAGING MARKET BY MATERIAL 2023-2029 ($ BILLION)

- TABLE 20 NORTH AMERICA SUSTAINABLE PACKAGING MARKET BY PACKAGING TYPE 2023-2029 ($ BILLION)

- TABLE 21 NORTH AMERICA SUSTAINABLE PACKAGING MARKET BY APPLICATION 2023-2029 ($ BILLION)

- TABLE 22 NORTH AMERICA SUSTAINABLE PACKAGING MARKET BY PROCESS 2023-2029 ($ BILLION)

- TABLE 23 APAC SUSTAINABLE PACKAGING MARKET BY MATERIAL 2023-2029 ($ BILLION)

- TABLE 24 APAC SUSTAINABLE PACKAGING MARKET BY PACKAGING TYPE 2023-2029 ($ BILLION)

- TABLE 25 APAC SUSTAINABLE PACKAGING MARKET BY PROCESS 2023-2029 ($ BILLION)

- TABLE 26 APAC SUSTAINABLE PACKAGING MARKET BY APPLICATION 2023-2029 ($ BILLION)

- TABLE 27 LATIN AMERICA SUSTAINABLE PACKAGING MARKET BY MATERIAL 2023-2029 ($ BILLION)

- TABLE 28 LATIN AMERICA SUSTAINABLE PACKAGING MARKET BY PACKAGING TYPE 2023-2029 ($ BILLION)

- TABLE 29 LATIN AMERICA SUSTAINABLE PACKAGING MARKET BY PROCESS 2023-2029 ($ BILLION)

- TABLE 30 LATIN AMERICA SUSTAINABLE PACKAGING MARKET BY APPLICATION 2023-2029 ($ BILLION)

- TABLE 31 MEXICO PACKAGING MATERIAL DEMAND BY TYPE

- TABLE 32 THE MIDDLE EAST & AFRICA SUSTAINABLE PACKAGING MARKET BY MATERIAL 2023-2029 ($ BILLION)

- TABLE 33 THE MIDDLE EAST & AFRICA SUSTAINABLE PACKAGING MARKET BY PACKAGING TYPE 2023-2029 ($ BILLION)

- TABLE 34 THE MIDDLE EAST & AFRICA SUSTAINABLE PACKAGING MARKET BY PROCESS 2023-2029 ($ BILLION)

- TABLE 35 THE MIDDLE EAST & AFRICA SUSTAINABLE PACKAGING MARKET BY APPLICATION 2023-2029 ($ BILLION)

- TABLE 36 AMCOR: MAJOR PRODUCT OFFERINGS

- TABLE 37 ARDAGH GROUP: MAJOR PRODUCT OFFERINGS

- TABLE 38 BALL CORPORATION: MAJOR PRODUCT OFFERINGS

- TABLE 39 BILLERUD: MAJOR PRODUCT OFFERINGS

- TABLE 40 CROWN HOLDINGS: MAJOR PRODUCT OFFERINGS

- TABLE 41 DS SMITH: MAJOR PRODUCT OFFERINGS

- TABLE 42 INTERNATIONAL PAPER: MAJOR PRODUCT OFFERINGS

- TABLE 43 HUHTAMAKI: MAJOR PRODUCT OFFERINGS

- TABLE 44 MONDI: MAJOR PRODUCT OFFERINGS

- TABLE 45 SONOCO PRODUCTS COMPANY: MAJOR PRODUCT OFFERINGS

- TABLE 46 SEALED AIR CORPORATION: MAJOR PRODUCT OFFERINGS

- TABLE 47 SMURFIT KAPPA: MAJOR PRODUCT OFFERINGS

- TABLE 48 WESTROCK: MAJOR PRODUCT OFFERINGS

- TABLE 49 AHLSTROM: MAJOR PRODUCT OFFERINGS

- TABLE 50 BERRY GLOBAL: MAJOR PRODUCT OFFERINGS

- TABLE 51 BOTANICAL PAPERWORKS: MAJOR PRODUCT OFFERINGS

- TABLE 52 BE GREEN PACKAGING: MAJOR PRODUCT OFFERINGS

- TABLE 53 CONSTANTIA FLEXIBLES: MAJOR PRODUCT OFFERINGS

- TABLE 54 DUPONT: MAJOR PRODUCT OFFERINGS

- TABLE 55 EVERGREEN RESOURCES: MAJOR PRODUCT OFFERINGS

- TABLE 56 ECOENCLOSE: MAJOR PRODUCT OFFERINGS

- TABLE 57 ELEVATE PACKAGING: MAJOR PRODUCT OFFERINGS

- TABLE 58 FUTAMURA GROUP: MAJOR PRODUCT OFFERINGS

- TABLE 59 GENPAK: MAJOR PRODUCT OFFERINGS

- TABLE 60 GRAPHIC PACKAGING INTERNATIONAL: MAJOR PRODUCT OFFERINGS

- TABLE 61 LIMELOOP: MAJOR PRODUCT OFFERINGS

- TABLE 62 NAMPAK: MAJOR PRODUCT OFFERINGS

- TABLE 63 NOTPLA: MAJOR PRODUCT OFFERINGS

- TABLE 64 NOVAMONT: MAJOR PRODUCT OFFERINGS

- TABLE 65 NUMI: MAJOR PRODUCT OFFERINGS

- TABLE 66 OJI HOLDINGS CORPORATION: MAJOR PRODUCT OFFERINGS

- TABLE 67 PLASTIPAK HOLDINGS: MAJOR PRODUCT OFFERINGS

- TABLE 68 PAKFACTORY: MAJOR PRODUCT OFFERINGS

- TABLE 69 REYNOLDS PACKAGING: MAJOR PRODUCT OFFERINGS

- TABLE 70 SAPPI: MAJOR PRODUCT OFFERINGS

- TABLE 71 STORA ENSO: MAJOR PRODUCT OFFERINGS

- TABLE 72 TAGHLEEF INDUSTRIES: MAJOR PRODUCT OFFERINGS

- TABLE 73 TETRA PAK: MAJOR PRODUCT OFFERINGS

- TABLE 74 TRANSCONTINENTAL: MAJOR PRODUCT OFFERINGS

- TABLE 75 UFLEX: MAJOR PRODUCT OFFERINGS

- TABLE 76 GLOBAL SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 77 GLOBAL SUSTAINABLE PACKAGING MARKET BY GEOGRAPHY 2023-2029 (%)

- TABLE 78 GLOBAL SUSTAINABLE PACKAGING MARKET BY MATERIAL 2023-2029 ($ BILLION)

- TABLE 79 GLOBAL SUSTAINABLE PACKAGING MARKET BY PACKAGING TYPE 2023-2029 ($ BILLION)

- TABLE 80 GLOBAL SUSTAINABLE PACKAGING MARKET BY PROCESS 2023-2029 ($ BILLION)

- TABLE 81 GLOBAL SUSTAINABLE PACKAGING MARKET BY APPLICATION 2023-2029 ($ BILLION)

- TABLE 82 EUROPE SUSTAINABLE PACKAGING MARKET BY MATERIAL 2023-2029 ($ BILLION)

- TABLE 83 EUROPE SUSTAINABLE PACKAGING MARKET BY PACKAGING TYPE 2023-2029 ($ BILLION)

- TABLE 84 EUROPE SUSTAINABLE PACKAGING MARKET BY PROCESS 2023-2029 ($ BILLION)

- TABLE 85 EUROPE SUSTAINABLE PACKAGING MARKET BY APPLICATION 2023-2029 ($ BILLION)

- TABLE 86 NORTH AMERICA SUSTAINABLE PACKAGING MARKET BY MATERIAL 2023-2029 ($ BILLION)

- TABLE 87 NORTH AMERICA SUSTAINABLE PACKAGING MARKET BY PACKAGING TYPE 2023-2029 ($ BILLION)

- TABLE 88 NORTH AMERICA SUSTAINABLE PACKAGING MARKET BY PROCESS 2023-2029 ($ BILLION)

- TABLE 89 NORTH AMERICA SUSTAINABLE PACKAGING MARKET BY APPLICATION 2023-2029 ($ BILLION)

- TABLE 90 APAC SUSTAINABLE PACKAGING MARKET BY MATERIAL 2023-2029 ($ BILLION)

- TABLE 91 APAC SUSTAINABLE PACKAGING MARKET BY PACKAGING TYPE 2023-2029 ($ BILLION)

- TABLE 92 APAC SUSTAINABLE PACKAGING MARKET BY PROCESS 2023-2029 ($ BILLION)

- TABLE 93 APAC SUSTAINABLE PACKAGING MARKET BY APPLICATION 2023-2029 ($ BILLION)

- TABLE 94 LATIN AMERICA SUSTAINABLE PACKAGING MARKET BY MATERIAL 2023-2029 ($ BILLION)

- TABLE 95 LATIN AMERICA SUSTAINABLE PACKAGING MARKET BY PACKAGING TYPE 2023-2029 ($ BILLION)

- TABLE 96 LATIN AMERICA SUSTAINABLE PACKAGING MARKET BY PROCESS 2023-2029 ($ BILLION)

- TABLE 97 LATIN AMERICA SUSTAINABLE PACKAGING MARKET BY APPLICATION 2023-2029 ($ BILLION)

- TABLE 98 THE MIDDLE EAST & AFRICA SUSTAINABLE PACKAGING MARKET BY MATERIAL 2023-2029 ($ BILLION)

- TABLE 99 THE MIDDLE EAST & AFRICA SUSTAINABLE PACKAGING MARKET BY PACKAGING TYPE 2023-2029 ($ BILLION)

- TABLE 100 THE MIDDLE EAST & AFRICA SUSTAINABLE PACKAGING MARKET BY PROCESS 2023-2029 ($ BILLION)

- TABLE 101 THE MIDDLE EAST & AFRICA SUSTAINABLE PACKAGING MARKET BY APPLICATION 2023-2029 ($ BILLION)

- TABLE 102 CURRENCY CONVERSION 2016-2023

The global sustainable packaging market was valued at USD 319.62 billion in 2023 and is expected to grow at a CAGR of 7.44% from 2023-2029.

MARKET TRENDS & DRIVERS

Growth in E-commerce Industry

The growth of the e-commerce market, particularly in the context of sustainable packaging, is a multifaceted trend that has gained significant momentum in recent years. The ever-increasing popularity of online shopping is the key driver behind this trend. With the convenience of purchasing products from the comfort of their homes, consumers are turning to e-commerce platforms more than ever before. This surge in online shopping has led to demand for packaging materials to ship products safely to consumers' doorsteps. However, this growth has also brought attention to the environmental impact of traditional packaging materials, such as plastic, and excessive use of cardboard. Consumers are becoming increasingly eco-conscious and actively seeking sustainable and environmentally friendly packaging options. As a result, e-commerce companies are recognizing the need to align their packaging practices with sustainability goals to meet consumer expectations and reduce their carbon footprint. Such factors are projected to support the growth of the sustainable packaging market.

Increase in Pouch Packaging Across End-Users

The demand for convenience and single-serve packaging enables pouch packaging adoption among various end-users. The surge in pouch packaging across various industries is a compelling driver in the sustainable packaging market. Pouch packaging has gained popularity due to its environmentally friendly attributes and numerous advantages. The flexible pouch packaging replaces metal, glass, and rigid plastic packaging. Compared to rigid packaging products, the demand for packaged food and drinks combined with the ease of use and cost-effectiveness of pouches mainly fuels demand globally. Pouches consume less space and are also light in weight. Further, pouches decrease the transport-related costs relative to rigid packaging such as metal cans and glass bottles.

SEGMENTATION INSIGHTS

INSIGHTS BY MATERIAL

Various materials play distinct roles in the sustainable packaging market in addressing environmental concerns and consumer preferences. Paper and paperboard are widely embraced for their biodegradability and renewability, offering a compelling eco-friendly alternative. Paper & paperboard accounted for the highest global sustainable packaging market share in 2023. The emphasis on reducing single-use plastics has fueled innovations in bio-based and recyclable plastics, contributing to a more sustainable packaging landscape. During the forecast period, the plastic segment will likely grow at the highest CAGR in the global sustainable packaging market. Metal packaging, particularly aluminum, is valued for its recyclability and ability to maintain product freshness. Glass, while heavier, is prized for its recyclability and inert nature, ensuring the preservation of product quality.

Segmentation by Material

- Paper & Paperboard

- Plastic

- Metal

- Glass

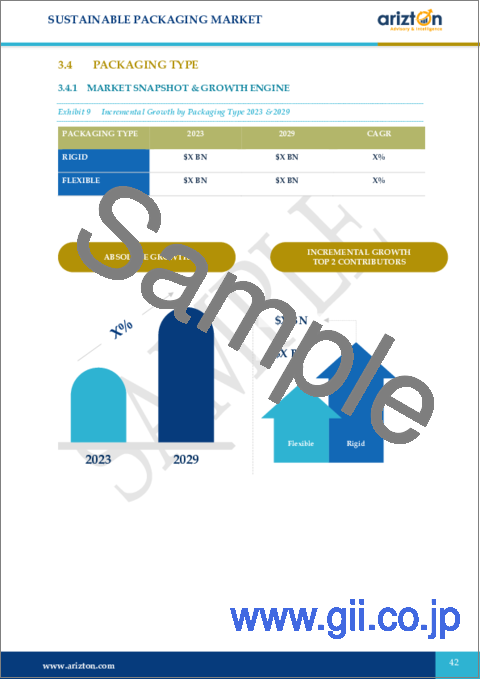

INSIGHTS BY PACKAGING TYPE

The global sustainable packaging market by packaging type is segmented into rigid and flexible packaging. Rigid packaging, such as glass or metal, is often favored for its durability and recyclability, contributing to a closed-loop system. Rigid packaging held the highest share in 2023. On the other hand, flexible packaging, including materials like compostable plastics or recycled films, offers lightweight and resource-efficient alternatives, reducing transportation-related carbon footprint. Flexible packaging is expected to grow at the highest CAGR during the forecast period.

Segmentation by Packaging Type

- Rigid

- Flexible

INSIGHTS BY PROCESS

The global sustainable packaging market by process is segmented into recyclability, degradability, and reusability. Recyclable packaging, which can be collected and processed to create new products, addresses the issue of waste accumulation. The recyclable packaging segment accounted for the highest share of the global market in 2023. Many countries have introduced or strengthened laws and regulations related to recycling and packaging waste. Such factors have increased demand for recyclable packaging materials as companies strive to comply with these requirements. Extended Producer Responsibility (EPR) programs, which make manufacturers responsible for the entire lifecycle of their products, further motivate the adoption of recyclable packaging. Developed regions like North America and Europe have been at the forefront of sustainable packaging adoption due to strong environmental awareness, stringent regulations, and higher consumer expectations for eco-friendly options. Furthermore, reusable packaging is expected to grow at the highest CAGR during the forecast period. Reusable packaging focuses on creating durable containers that can be used multiple times, minimizing the need for single-use items.

Segmentation by Process

- Recyclable

- Degradable

- Reusable

INSIGHTS BY APPLICATION

The food & beverages application segment holds the largest global sustainable packaging market share in 2023. In the food and beverage industry, there is a shift towards sustainable packaging solutions to reduce the environmental impact of packaging waste. With the increasing threat of several airborne diseases, rapid urbanization driving the growth of supermarkets, and increasing demand from people for safe and convenient small-sized packaging, the demand for packaged food is significantly growing globally, thereby propelling the sustainable packaging market growth. Furthermore, the cosmetics and personal care sector also adopts eco-friendly packaging, responding to consumer preferences for sustainable and recyclable materials. Additionally, the pharmaceutical market is increasingly exploring sustainable packaging alternatives to align with corporate social responsibility goals and to meet stringent regulatory requirements. E-commerce and retail segments are incorporating sustainable packaging to address the escalating volume of online deliveries and reduce the carbon footprint associated with packaging materials.

Segmentation by Application

- Food & Beverages

- Personal Care & Cosmetics

- Medical & Pharmaceutical

- E-commerce & Retail

- Others

GEOGRAPHICAL ANALYSIS

Europe accounted for the highest global sustainable packaging market share in 2023. The European market has been experiencing significant growth due to increased consumer awareness and stringent government regulations regarding using single-use plastics and sustainability. European consumers have been increasingly shifting their preferences towards sustainable products and packaging. A European Consumer Packaging Perceptions Study found that nearly two-thirds of respondents changed the products they bought due to concerns about packaging. Moreover, over three-quarters of all consumers are willing to pay more for environmentally friendly packaging. On top of that, stringent government regulations in Europe are driving the demand for green packaging. These regulations aim to reduce single-use plastics and promote more sustainable packaging alternatives. This regulatory environment is contributing to the growth of eco-friendly packaging options.

Segmentation by Geography

- Europe

- Germany

- The U.K.

- France

- Italy

- Spain

- Russia

- Benelux

- North America

- The U.S.

- Canada

- APAC

- China

- Japan

- India

- South Korea

- Australia

- New Zealand

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Israel

- South Africa

COMPETITIVE LANDSCAPE

The global sustainable packaging market is witnessing a dynamic and competitive landscape driven by the growing global emphasis on environmental conservation and corporate social responsibility. Key players in the global sustainable packaging market include multinational corporations, such as Amcor, Tetra Pak International, and Ball Corporation, leveraging their extensive resources and innovation capabilities to develop eco-friendly packaging solutions. Additionally, niche players like Ecover, Eco-Products, and NatureWorks contribute to the competitive mix with specialized offerings. Collaboration and partnerships between packaging manufacturers and consumer goods companies further intensify competition, fostering the development of comprehensive, end-to-end, sustainable packaging solutions.

Key Company Profiles

- Amcor

- Ardagh Group

- Ball Corporation

- Billerud

- Crown Holdings

- DS Smith

- International Paper

- Huhtamaki

- Mondi

- Sonoco Products Company

- Sealed Air Corporation

- Smurfit Kappa

- WestRock

Other Prominent Vendors

- Ahlstrom

- Berry Global

- Botanical PaperWorks

- Be Green Packaging

- Constantia Flexibles

- DuPont

- Evergreen Resources

- EcoEnclose

- Elevate Packaging

- Futamura Group

- Genpak

- Graphic Packaging International

- LimeLoop

- Nampak

- Notpla

- Novamont

- Numi

- Oji Holdings Corporation

- Plastipak Holdings

- PakFactory

- Reynolds Packaging

- Sappi

- Stora Enso

- Taghleef Industries

- Tetra Pak

- Transcontinental

- UFlex

KEY QUESTIONS ANSWERED:

1. How big is the sustainable packaging market?

2. What is the growth rate of the global sustainable packaging market?

3. Which region dominates the global sustainable packaging market share?

4. What are the significant trends in the sustainable packaging industry?

5. Who are the key players in the global sustainable packaging market?

TABLE OF CONTENTS

1 SCOPE & COVERAGE

- 1.1. MARKET DEFINITION

- 1.1.1. INCLUSIONS

- 1.1.2. EXCLUSIONS

- 1.1.3. MARKET ESTIMATION CAVEATS

- 1.2. SEGMENTS COVERED & DEFINITIONS

- 1.2.1. MARKET BY MATERIAL

- 1.2.2. MARKET BY PACKAGING TYPE

- 1.2.3. MARKET BY PROCESS

- 1.2.4. MARKET BY APPLICATION

- 1.2.5. REGIONS & COUNTRIES COVERED

- 1.3. MARKET DERIVATION

- 1.3.1. BASE YEAR

2 PREMIUM INSIGHTS

- 2.1. OPPORTUNITY POCKETS

- 2.2. REPORT OVERVIEW

- 2.3. SEGMENT ANALYSIS

- 2.3.1. INSIGHTS BY MATERIAL

- 2.3.2. INSIGHTS BY PACKAGING TYPE

- 2.3.3. INSIGHTS BY PROCESS

- 2.3.4. INSIGHTS BY APPLICATION

- 2.4. REGIONAL ANALYSIS

- 2.5. COMPETITIVE LANDSCAPE

3 MARKET AT A GLANCE

4 INTRODUCTION

- 4.1. OVERVIEW

- 4.2. PACKAGING INDUSTRY

- 4.2.1. LAYERS OF PACKAGING

- 4.3. ANTICIPATED IMPACTS BY 2050

- 4.4. INNOVATIONS & ACQUISITIONS

- 4.5. CIRCULAR ECONOMY

- 4.6. VALUE CHAIN ANALYSIS

- 4.6.1. RAW MATERIALS

- 4.6.2. MANUFACTURING

- 4.6.3. DISTRIBUTION

- 4.6.4. RETAIL

- 4.6.5. RECYCLING & COMPOSTING

- 4.6.6. END OF LIFE

- 4.7. EXPERTS OPINION

5 MARKET OPPORTUNITIES & TRENDS

- 5.1. GROWTH IN E-COMMERCE INDUSTRY

- 5.2. INCREASED FOCUS ON SUSTAINABLE FLEXIBLE PACKAGING

- 5.3. RISE IN REUSABLE PACKAGING

- 5.4. SHIFT TOWARD MODIFIED ATMOSPHERIC PACKAGING PRODUCTS

6 MARKET GROWTH ENABLERS

- 6.1 INCREASE IN PROCESSED AND PACKAGED FOOD

- 6.2 EFFICIENT SUPPLY CHAIN FUELING MARKET GROWTH

- 6.3 INCREASE IN POUCH PACKAGING ACROSS END USERS

7 MARKET RESTRAINTS

- 7.1 REGULATORY COMPLIANCE & STANDARDS

- 7.2 RISING COST OF RAW MATERIALS

- 7.3 HIGH OPERATIONAL COST

8 MARKET LANDSCAPE

- 8.1. MARKET OVERVIEW

- 8.2. MARKET SIZE & FORECAST

- 8.3. RAW MATERIALS

- 8.4. RISK FACTORS IN THE MARKET

- 8.5. FIVE FORCES ANALYSIS

- 8.5.1. THREAT OF NEW ENTRANTS

- 8.5.2. BARGAINING POWER OF SUPPLIERS

- 8.5.3. BARGAINING POWER OF BUYERS

- 8.5.4. THREAT OF SUBSTITUTES

- 8.5.5. COMPETITIVE RIVALRY

9 MATERIAL

- 9.1. MARKET SNAPSHOT & GROWTH ENGINE

- 9.2. MARKET OVERVIEW

- 9.3. PAPER & PAPERBOARD

- 9.3.1. MARKET SIZE & FORECAST

- 9.3.2. MARKET BY GEOGRAPHY

- 9.4. PLASTIC

- 9.4.1. MARKET SIZE & FORECAST

- 9.4.2. MARKET BY GEOGRAPHY

- 9.5. METAL

- 9.5.1. MARKET SIZE & FORECAST

- 9.5.2. MARKET BY GEOGRAPHY

- 9.6. GLASS

- 9.6.1. MARKET SIZE & FORECAST

- 9.6.2. MARKET BY GEOGRAPHY

10 PACKAGING TYPE

- 10.1. MARKET SNAPSHOT & GROWTH ENGINE

- 10.2. MARKET OVERVIEW

- 10.3. RIGID

- 10.3.1. MARKET SIZE & FORECAST

- 10.3.2. MARKET BY GEOGRAPHY

- 10.4. FLEXIBLE

- 10.4.1. MARKET SIZE & FORECAST

- 10.4.2. MARKET BY GEOGRAPHY

11 PROCESS

- 11.1. MARKET SNAPSHOT & GROWTH ENGINE

- 11.2. MARKET OVERVIEW

- 11.3. RECYCLABLE

- 11.3.1. MARKET SIZE & FORECAST

- 11.3.2. MARKET BY GEOGRAPHY

- 11.4. DEGRADABLE

- 11.4.1. MARKET SIZE & FORECAST

- 11.4.2. MARKET BY GEOGRAPHY

- 11.5. REUSABLE

- 11.5.1. MARKET SIZE & FORECAST

- 11.5.2. MARKET BY GEOGRAPHY

12 APPLICATION

- 12.1. MARKET SNAPSHOT & GROWTH ENGINE

- 12.2. MARKET OVERVIEW

- 12.3. FOOD & BEVERAGES

- 12.3.1. MARKET SIZE & FORECAST

- 12.3.2. MARKET BY GEOGRAPHY

- 12.4. PERSONAL CARE & COSMETICS

- 12.4.1. MARKET SIZE & FORECAST

- 12.4.2. MARKET BY GEOGRAPHY

- 12.5. MEDICAL & PHARMACEUTICAL

- 12.5.1. MARKET SIZE & FORECAST

- 12.5.2. MARKET BY GEOGRAPHY

- 12.6. E-COMMERCE & RETAIL

- 12.6.1. MARKET SIZE & FORECAST

- 12.6.2. MARKET BY GEOGRAPHY

- 12.7. OTHERS

- 12.7.1. MARKET SIZE & FORECAST

- 12.7.2. MARKET BY GEOGRAPHY

13 GEOGRAPHY

- 13.1. MARKET SNAPSHOT & GROWTH ENGINE

- 13.2. GEOGRAPHIC OVERVIEW

14 EUROPE

- 14.1. MARKET OVERVIEW

- 14.2. MARKET SIZE & FORECAST

- 14.3. MATERIAL

- 14.3.1. MARKET SIZE & FORECAST

- 14.4. PACKAGING TYPE

- 14.4.1. MARKET SIZE & FORECAST

- 14.5. PROCESS

- 14.5.1. MARKET SIZE & FORECAST

- 14.6. APPLICATION

- 14.6.1. MARKET SIZE & FORECAST

- 14.7. KEY COUNTRIES

- 14.8. GERMANY: MARKET SIZE & FORECAST

- 14.9. UK: MARKET SIZE & FORECAST

- 14.10. FRANCE: MARKET SIZE & FORECAST

- 14.11. ITALY: MARKET SIZE & FORECAST

- 14.12. SPAIN: MARKET SIZE & FORECAST

- 14.13. RUSSIA: MARKET SIZE & FORECAST

- 14.14. BENELUX: MARKET SIZE & FORECAST

15 NORTH AMERICA

- 15.1. MARKET OVERVIEW

- 15.2. MARKET SIZE & FORECAST

- 15.3. MATERIAL

- 15.3.1. MARKET SIZE & FORECAST

- 15.4. PACKAGING TYPE

- 15.4.1. MARKET SIZE & FORECAST

- 15.5. APPLICATION

- 15.5.1. MARKET SIZE & FORECAST

- 15.6. PROCESS

- 15.6.1. MARKET SIZE & FORECAST

- 15.7. KEY COUNTRIES

- 15.8. US: MARKET SIZE & FORECAST

- 15.9. CANADA: MARKET SIZE & FORECAST

16 APAC

- 16.1. MARKET OVERVIEW

- 16.2. MARKET SIZE & FORECAST

- 16.3. MATERIAL

- 16.3.1. MARKET SIZE & FORECAST

- 16.4. PACKAGING TYPE

- 16.4.1. MARKET SIZE & FORECAST

- 16.5. PROCESS

- 16.5.1. MARKET SIZE & FORECAST

- 16.6. APPLICATION

- 16.6.1. MARKET SIZE & FORECAST

- 16.7. KEY COUNTRIES

- 16.8. CHINA: MARKET SIZE & FORECAST

- 16.9. INDIA: MARKET SIZE & FORECAST

- 16.10. JAPAN: MARKET SIZE & FORECAST

- 16.11. AUSTRALIA: MARKET SIZE & FORECAST

- 16.12. SOUTH KOREA: MARKET SIZE & FORECAST

- 16.13. NEW ZEALAND: MARKET SIZE & FORECAST

- 16.14. REST OF APAC: MARKET SIZE & FORECAST

17 LATIN AMERICA

- 17.1. MARKET OVERVIEW

- 17.2. MARKET SIZE & FORECAST

- 17.3. MATERIAL

- 17.3.1. MARKET SIZE & FORECAST

- 17.4. PACKAGING TYPE

- 17.4.1. MARKET SIZE & FORECAST

- 17.5. PROCESS

- 17.5.1. MARKET SIZE & FORECAST

- 17.6. APPLICATION

- 17.6.1. MARKET SIZE & FORECAST

- 17.7. KEY COUNTRIES

- 17.8. BRAZIL: MARKET SIZE & FORECAST

- 17.9. MEXICO: MARKET SIZE & FORECAST

- 17.10. ARGENTINA: MARKET SIZE & FORECAST

18 MIDDLE EAST & AFRICA

- 18.1. MARKET OVERVIEW

- 18.2. MARKET SIZE & FORECAST

- 18.3. MATERIAL

- 18.3.1. MARKET SIZE & FORECAST

- 18.4. PACKAGING TYPE

- 18.4.1. MARKET SIZE & FORECAST

- 18.5. PROCESS

- 18.5.1. MARKET SIZE & FORECAST

- 18.6. APPLICATION

- 18.6.1. MARKET SIZE & FORECAST

- 18.7. KEY COUNTRIES

- 18.8. SAUDI ARABIA: MARKET SIZE & FORECAST

- 18.9. UAE: MARKET SIZE & FORECAST

- 18.10. EGYPT: MARKET SIZE & FORECAST

- 18.11. ISRAEL: MARKET SIZE & FORECAST

- 18.12. SOUTH AFRICA: MARKET SIZE & FORECAST

19 COMPETITIVE LANDSCAPE

- 19.1. COMPETITION OVERVIEW

20 KEY COMPANY PROFILES

- 20.1. AMCOR

- 20.1.1. BUSINESS OVERVIEW

- 20.1.2. PRODUCT OFFERINGS

- 20.1.3. KEY STRATEGIES

- 20.1.4. KEY STRENGTHS

- 20.1.5. KEY OPPORTUNITIES

- 20.2. ARDAGH GROUP

- 20.2.1. BUSINESS OVERVIEW

- 20.2.2. PRODUCT OFFERINGS

- 20.2.3. KEY STRATEGIES

- 20.2.4. KEY STRENGTHS

- 20.2.5. KEY OPPORTUNITIES

- 20.3. BALL CORPORATION

- 20.3.1. BUSINESS OVERVIEW

- 20.3.2. PRODUCT OFFERINGS

- 20.3.3. KEY STRATEGIES

- 20.3.4. KEY STRENGTHS

- 20.3.5. KEY OPPORTUNITIES

- 20.4. BILLERUD

- 20.4.1. BUSINESS OVERVIEW

- 20.4.2. PRODUCT OFFERINGS

- 20.4.3. KEY STRATEGIES

- 20.4.4. KEY STRENGTHS

- 20.4.5. KEY OPPORTUNITIES

- 20.5. CROWN HOLDINGS

- 20.5.1. BUSINESS OVERVIEW

- 20.5.2. PRODUCT OFFERINGS

- 20.5.3. KEY STRATEGIES

- 20.5.4. KEY STRENGTHS

- 20.5.5. KEY OPPORTUNITIES

- 20.6. DS SMITH

- 20.6.1. BUSINESS OVERVIEW

- 20.6.2. PRODUCT OFFERINGS

- 20.6.3. KEY STRATEGIES

- 20.6.4. KEY STRENGTHS

- 20.6.5. KEY OPPORTUNITIES

- 20.7. INTERNATIONAL PAPER

- 20.7.1. BUSINESS OVERVIEW

- 20.7.2. PRODUCT OFFERINGS

- 20.7.3. KEY STRATEGIES

- 20.7.4. KEY STRENGTHS

- 20.7.5. KEY OPPORTUNITIES

- 20.8. HUHTAMAKI

- 20.8.1. BUSINESS OVERVIEW

- 20.8.2. PRODUCT OFFERINGS

- 20.8.3. KEY STRATEGIES

- 20.8.4. KEY STRENGTHS

- 20.8.5. KEY OPPORTUNITIES

- 20.9. MONDI

- 20.9.1. BUSINESS OVERVIEW

- 20.9.2. PRODUCT OFFERINGS

- 20.9.3. KEY STRATEGIES

- 20.9.4. KEY STRENGTHS

- 20.9.5. KEY OPPORTUNITIES

- 20.10. SONOCO PRODUCTS COMPANY

- 20.10.1. BUSINESS OVERVIEW

- 20.10.2. PRODUCT OFFERINGS

- 20.10.3. KEY STRATEGIES

- 20.10.4. KEY STRENGTHS

- 20.10.5. KEY OPPORTUNITIES

- 20.11. SEALED AIR CORPORATION

- 20.11.1. BUSINESS OVERVIEW

- 20.11.2. PRODUCT OFFERINGS

- 20.11.3. KEY STRATEGIES

- 20.11.4. KEY STRENGTHS

- 20.11.5. KEY OPPORTUNITIES

- 20.12. SMURFIT KAPPA

- 20.12.1. BUSINESS OVERVIEW

- 20.12.2. PRODUCT OFFERINGS

- 20.12.3. KEY STRATEGIES

- 20.12.4. KEY STRENGTHS

- 20.12.5. KEY OPPORTUNITIES

- 20.13. WESTROCK

- 20.13.1. BUSINESS OVERVIEW

- 20.13.2. PRODUCT OFFERINGS

- 20.13.3. KEY STRATEGIES

- 20.13.4. KEY STRENGTHS

- 20.13.5. KEY OPPORTUNITIES

21 OTHER PROMINENT VENDORS

- 21.1. AHLSTROM

- 21.1.1. BUSINESS OVERVIEW

- 21.1.2. PRODUCT OFFERINGS

- 21.2. BERRY GLOBAL

- 21.2.1. BUSINESS OVERVIEW

- 21.2.2. PRODUCT OFFERINGS

- 21.3. BOTANICAL PAPERWORKS

- 21.3.1. BUSINESS OVERVIEW

- 21.3.2. PRODUCT OFFERINGS

- 21.4. BE GREEN PACKAGING

- 21.4.1. BUSINESS OVERVIEW

- 21.4.2. PRODUCT OFFERINGS

- 21.5. CONSTANTIA FLEXIBLES

- 21.5.1. BUSINESS OVERVIEW

- 21.5.2. PRODUCT OFFERINGS

- 21.6. DUPONT

- 21.6.1. BUSINESS OVERVIEW

- 21.6.2. PRODUCT OFFERINGS

- 21.7. EVERGREEN RESOURCES

- 21.7.1. BUSINESS OVERVIEW

- 21.7.2. PRODUCT OFFERINGS

- 21.8. ECOENCLOSE

- 21.8.1. BUSINESS OVERVIEW

- 21.8.2. PRODUCT OFFERINGS

- 21.9. ELEVATE PACKAGING

- 21.9.1. BUSINESS OVERVIEW

- 21.9.2. PRODUCT OFFERINGS

- 21.10. FUTAMURA GROUP

- 21.10.1. BUSINESS OVERVIEW

- 21.10.2. PRODUCT OFFERINGS

- 21.11. GENPAK

- 21.11.1. BUSINESS OVERVIEW

- 21.11.2. PRODUCT OFFERINGS

- 21.12. GRAPHIC PACKAGING INTERNATIONAL

- 21.12.1. BUSINESS OVERVIEW

- 21.12.2. PRODUCT OFFERINGS

- 21.13. LIMELOOP

- 21.13.1. BUSINESS OVERVIEW

- 21.13.2. PRODUCT OFFERINGS

- 21.14. NAMPAK

- 21.14.1. BUSINESS OVERVIEW

- 21.14.2. PRODUCT OFFERINGS

- 21.15. NOTPLA

- 21.15.1. BUSINESS OVERVIEW

- 21.15.2. PRODUCT OFFERINGS

- 21.16. NOVAMONT

- 21.16.1. BUSINESS OVERVIEW

- 21.16.2. PRODUCT OFFERINGS

- 21.17. NUMI

- 21.17.1. BUSINESS OVERVIEW

- 21.17.2. PRODUCT OFFERINGS

- 21.18. OJI HOLDINGS CORPORATION

- 21.18.1. BUSINESS OVERVIEW

- 21.18.2. PRODUCT OFFERINGS

- 21.19. PLASTIPAK HOLDINGS

- 21.19.1. BUSINESS OVERVIEW

- 21.19.2. PRODUCT OFFERINGS

- 21.20. PAKFACTORY

- 21.20.1. BUSINESS OVERVIEW

- 21.20.2. PRODUCT OFFERINGS

- 21.21. REYNOLDS PACKAGING

- 21.21.1. BUSINESS OVERVIEW

- 21.21.2. PRODUCT OFFERINGS

- 21.22. SAPPI

- 21.22.1. BUSINESS OVERVIEW

- 21.22.2. PRODUCT OFFERINGS

- 21.23. STORA ENSO

- 21.23.1. BUSINESS OVERVIEW

- 21.23.2. PRODUCT OFFERINGS

- 21.24. TAGHLEEF INDUSTRIES

- 21.24.1. BUSINESS OVERVIEW

- 21.24.2. PRODUCT OFFERINGS

- 21.25. TETRA PAK

- 21.25.1. BUSINESS OVERVIEW

- 21.25.2. PRODUCT OFFERINGS

- 21.26. TRANSCONTINENTAL

- 21.26.1. BUSINESS OVERVIEW

- 21.26.2. PRODUCT OFFERINGS

- 21.27. UFLEX

- 21.27.1. BUSINESS OVERVIEW

- 21.27.2. PRODUCT OFFERINGS

22 REPORT SUMMARY

- 22.1. KEY TAKEAWAYS

- 22.2. STRATEGIC RECOMMENDATIONS

23 QUANTITATIVE SUMMARY

- 23.1. MARKET BY GEOGRAPHY

- 23.2. MARKET BY MATERIAL

- 23.3. MARKET BY PACKAGING TYPE

- 23.4. MARKET BY PROCESS

- 23.5. MARKET BY APPLICATION

- 23.6. EUROPE

- 23.6.1. MATERIAL: MARKET SIZE & FORECAST

- 23.6.2. PACKAGING TYPE: MARKET SIZE & FORECAST

- 23.6.3. PROCESS: MARKET SIZE & FORECAST

- 23.6.4. APPLICATION: MARKET SIZE & FORECAST

- 23.7. NORTH AMERICA

- 23.7.1. MATERIAL: MARKET SIZE & FORECAST

- 23.7.2. PACKAGING TYPE: MARKET SIZE & FORECAST

- 23.7.3. PROCESS: MARKET SIZE & FORECAST

- 23.7.4. APPLICATION: MARKET SIZE & FORECAST

- 23.8. APAC

- 23.8.1. MATERIAL: MARKET SIZE & FORECAST

- 23.8.2. PACKAGING TYPE: MARKET SIZE & FORECAST

- 23.8.3. PROCESS: MARKET SIZE & FORECAST

- 23.8.4. APPLICATION: MARKET SIZE & FORECAST

- 23.9. LATIN AMERICA

- 23.9.1. MATERIAL: MARKET SIZE & FORECAST

- 23.9.2. PACKAGING TYPE: MARKET SIZE & FORECAST

- 23.9.3. PROCESS: MARKET SIZE & FORECAST

- 23.9.4. APPLICATION: MARKET SIZE & FORECAST

- 23.10. MIDDLE EAST & AFRICA

- 23.10.1. MATERIAL: MARKET SIZE & FORECAST

- 23.10.2. PACKAGING TYPE: MARKET SIZE & FORECAST

- 23.10.3. PROCESS: MARKET SIZE & FORECAST

- 23.10.4. APPLICATION: MARKET SIZE & FORECAST

24 APPENDIX

- 24.1. RESEARCH METHODOLOGY

- 24.2. RESEARCH PROCESS

- 24.3. REPORT ASSUMPTIONS & CAVEATS

- 24.3.1. KEY CAVEATS

- 24.3.2. CURRENCY CONVERSION

- 24.4. ABBREVIATIONS