|

|

市場調査レポート

商品コード

1684745

自動車用バッテリー市場 - 成長、将来展望、競合分析、2025年~2033年Automotive Battery Market - Growth, Future Prospects and Competitive Analysis, 2025 - 2033 |

||||||

|

|||||||

|

|||||||

| 自動車用バッテリー市場 - 成長、将来展望、競合分析、2025年~2033年 |

|

出版日: 2025年01月08日

発行: Acute Market Reports

ページ情報: 英文 172 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 図表

- 目次

自動車用バッテリー市場は、自動車用に特別に設計されたバッテリーの製造、流通、販売を包括しています。これらのバッテリーは、エンジンを始動させ、エンジンが作動していないときにライト、インフォテインメント・システム、エアコンなどの電装品に電力を供給するという主な機能を果たします。自動車用バッテリーは主に鉛蓄バッテリーをベースとしていますが、技術の進歩により、より電動化された最新の自動車の需要に対応するため、リチウムイオンやその他のタイプのバッテリーも開発されています。2025年現在、自動車用バッテリー市場は、電気自動車(EV)の普及拡大、排出ガスに関する政府の厳しい規制、バッテリーの寿命と性能を向上させるバッテリー技術の進歩によって、大きな成長を遂げています。同市場の特徴は、より効率的で耐久性があり、環境に優しいバッテリーの開発における革新性です。年間平均成長率(CAGR)は5.71%で、自動車産業がより持続可能な慣行へとシフトし、消費者がよりメンテナンスが不要で運転コストが低い自動車を好むようになるにつれて、市場は拡大を続けると予測されます。自動車用バッテリーの需要は、交換用バッテリーのアフターマーケットの拡大や、新興国における自動車製造の拡大によっても支えられています。

自動車産業の電動化へのシフトは、自動車用バッテリー市場の重要な促進要因です。世界各国政府は気候変動対策としてより厳しい排ガス規制を実施しており、自動車メーカーは先進的なバッテリーシステムに大きく依存するハイブリッド車や電気自動車(EV)の開発を推進しています。このような規制の後押しと、持続可能な交通手段に対する消費者の意識と嗜好の高まりが相まって、高容量で長寿命の自動車用バッテリーの需要が加速しています。例えば、欧州連合、中国、米国などの主要自動車市場は、今後10年間のEV販売と排出削減の野心的な目標を設定しており、バッテリー技術と生産能力の大幅な進歩が必要とされています。

自動車用バッテリー市場は、再生可能エネルギー源と充電インフラの統合によって大きく活性化します。再生可能エネルギーの送電網への浸透が進み、ビークル・ツー・グリッド(V2G)技術が開発されたことで、EVは送電網と相互作用して、再生可能エネルギー源から発電された電力を受け入れ、蓄電し、放電することができるようになっています。この統合は、EVの環境面での利点を高めるだけでなく、送電網の安定性をサポートし、より効率的なエネルギー利用を可能にします。再生可能エネルギーの導入が進むにつれ、断続的なエネルギー供給を効率的に管理し、バックアップ電力を供給できるバッテリーの必要性が高まるため、車載用バッテリー市場は恩恵を受けることになり、バッテリー開発と市場開拓の新たな道が開かれることになります。

当レポートでは、世界の自動車用バッテリー市場について調査し、市場の概要とともに、タイプ別、推進方式別、車両タイプ別、販売チャネル別、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

第1章 序文

第2章 エグゼクティブサマリー

第3章 自動車用バッテリー市場:競合分析

第4章 自動車用バッテリー市場:マクロ分析と市場力学

- イントロダクション

- 世界の自動車用バッテリー市場価値(2023年~2033年)

- 市場力学

- 促進要因と抑制要因の影響分析

- シーソー分析

- ポーターのファイブフォースモデル

- PESTEL分析

第5章 自動車用バッテリー市場:タイプ別(2023年~2033年)

- 市場概要

- 成長と収益分析:2024年対2033年

- 市場セグメンテーション

第6章 自動車用バッテリー市場:推進力別(2023年~2033年)

- 市場概要

- 成長と収益分析:2024年対2033年

- 市場セグメンテーション

第7章 自動車用バッテリー市場:車両タイプ別(2023年~2033年)

- 市場概要

- 成長と収益分析:2024年対2033年

- 市場セグメンテーション

第8章 自動車用バッテリー市場:販売チャネル別(2023年~2033年)

- 市場概要

- 成長と収益分析:2024年対2033年

- 市場セグメンテーション

第9章 北米の自動車用バッテリー市場(2023年~2033年)

第10章 英国およびEUの自動車用バッテリー市場(2023年~2033年)

第11章 アジア太平洋の自動車用バッテリー市場(2023年~2033年)

第12章 ラテンアメリカの自動車用バッテリー市場(2023年~2033年)

第13章 中東・アフリカの自動車用バッテリー市場(2023年~2033年)

第14章 企業プロファイル

- Leoch International Tech

- Furukawa Electric Co. Ltd.

- Hitachi Ltd.

- Haldex Incorporated

- Exide Industries Limited

- Panasonic Corporation

- CATL

- GS Yuasa

- LG Chem

- Samsung SDI

- SK Innovation

- その他

List of Tables

- TABLE 1 Global Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 2 Global Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 3 Global Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 4 Global Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 5 Global Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 6 Global Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 7 North America Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 8 North America Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 9 North America Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 10 North America Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 11 North America Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 12 North America Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 13 U.S. Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 14 U.S. Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 15 U.S. Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 16 U.S. Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 17 U.S. Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 18 U.S. Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 19 Canada Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 20 Canada Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 21 Canada Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 22 Canada Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 23 Canada Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 24 Canada Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 25 Rest of North America Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 26 Rest of North America Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 27 Rest of North America Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 28 Rest of North America Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 29 Rest of North America Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 30 Rest of North America Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 31 UK and European Union Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 32 UK and European Union Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 33 UK and European Union Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 34 UK and European Union Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 35 UK and European Union Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 36 UK and European Union Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 37 UK Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 38 UK Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 39 UK Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 40 UK Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 41 UK Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 42 UK Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 43 Germany Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 44 Germany Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 45 Germany Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 46 Germany Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 47 Germany Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 48 Germany Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 49 Spain Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 50 Spain Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 51 Spain Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 52 Spain Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 53 Spain Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 54 Spain Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 55 Italy Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 56 Italy Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 57 Italy Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 58 Italy Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 59 Italy Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 60 Italy Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 61 France Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 62 France Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 63 France Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 64 France Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 65 France Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 66 France Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 67 Rest of Europe Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 68 Rest of Europe Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 69 Rest of Europe Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 70 Rest of Europe Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 71 Rest of Europe Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 72 Rest of Europe Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 73 Asia Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 74 Asia Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 75 Asia Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 76 Asia Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 77 Asia Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 78 Asia Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 79 China Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 80 China Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 81 China Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 82 China Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 83 China Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 84 China Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 85 Japan Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 86 Japan Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 87 Japan Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 88 Japan Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 89 Japan Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 90 Japan Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 91 India Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 92 India Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 93 India Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 94 India Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 95 India Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 96 India Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 97 Australia Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 98 Australia Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 99 Australia Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 100 Australia Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 101 Australia Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 102 Australia Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 103 South Korea Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 104 South Korea Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 105 South Korea Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 106 South Korea Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 107 South Korea Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 108 South Korea Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 109 Latin America Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 110 Latin America Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 111 Latin America Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 112 Latin America Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 113 Latin America Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 114 Latin America Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 115 Brazil Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 116 Brazil Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 117 Brazil Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 118 Brazil Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 119 Brazil Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 120 Brazil Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 121 Mexico Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 122 Mexico Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 123 Mexico Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 124 Mexico Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 125 Mexico Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 126 Mexico Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 127 Rest of Latin America Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 128 Rest of Latin America Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 129 Rest of Latin America Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 130 Rest of Latin America Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 131 Rest of Latin America Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 132 Rest of Latin America Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 133 Middle East and Africa Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 134 Middle East and Africa Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 135 Middle East and Africa Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 136 Middle East and Africa Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 137 Middle East and Africa Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 138 Middle East and Africa Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 139 GCC Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 140 GCC Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 141 GCC Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 142 GCC Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 143 GCC Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 144 GCC Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 145 Africa Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 146 Africa Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 147 Africa Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 148 Africa Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 149 Africa Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 150 Africa Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

- TABLE 151 Rest of Middle East and Africa Automotive Battery Market By Type, 2023-2033, USD (Million)

- TABLE 152 Rest of Middle East and Africa Automotive Battery Market By Propulsion, 2023-2033, USD (Million)

- TABLE 153 Rest of Middle East and Africa Automotive Battery Market By Internal Combustion Engine, 2023-2033, USD (Million)

- TABLE 154 Rest of Middle East and Africa Automotive Battery Market By Electric, 2023-2033, USD (Million)

- TABLE 155 Rest of Middle East and Africa Automotive Battery Market By Vehicle Type, 2023-2033, USD (Million)

- TABLE 156 Rest of Middle East and Africa Automotive Battery Market By Sales Channel, 2023-2033, USD (Million)

List of Figures

- FIG. 1 Global Automotive Battery Market: Market Coverage

- FIG. 2 Research Methodology and Data Sources

- FIG. 3 Market Size Estimation - Top Down & Bottom-Up Approach

- FIG. 4 Global Automotive Battery Market: Quality Assurance

- FIG. 5 Global Automotive Battery Market, By Type, 2024

- FIG. 6 Global Automotive Battery Market, By Propulsion, 2024

- FIG. 7 Global Automotive Battery Market, By Vehicle Type, 2024

- FIG. 8 Global Automotive Battery Market, By Sales Channel, 2024

- FIG. 9 Global Automotive Battery Market, By Geography, 2024

- FIG. 10 Market Geographical Opportunity Matrix - Global Automotive Battery Market, 2024

- FIG. 11Market Positioning of Key Automotive Battery Market Players, 2024

- FIG. 12 Global Automotive Battery Market, By Type, 2024 Vs 2033, %

- FIG. 13 Global Automotive Battery Market, By Propulsion, 2024 Vs 2033, %

- FIG. 14 Global Automotive Battery Market, By Vehicle Type, 2024 Vs 2033, %

- FIG. 15 Global Automotive Battery Market, By Sales Channel, 2024 Vs 2033, %

The automotive battery market encompasses the manufacturing, distribution, and sale of batteries specifically designed for use in automobiles. These batteries serve the primary function of starting the engine and providing power to electrical components such as lights, infotainment systems, and air conditioning when the engine is not running. Automotive batteries are predominantly lead-acid based, but advancements in technology have led to the development of lithium-ion and other battery types to meet the demands of modern, more electrified vehicles. As of 2025, the automotive battery market is experiencing significant growth driven by the increasing adoption of electric vehicles (EVs), stringent government regulations regarding emissions, and advancements in battery technology which improve battery life and performance. The market is characterized by its innovation in developing batteries that are more efficient, durable, and environmentally friendly. With a Compound Annual Growth Rate (CAGR) of 5.71%, the market is projected to continue expanding as the automotive industry shifts towards more sustainable practices and as consumers increasingly prefer vehicles that require less maintenance and offer lower operating costs. The demand for automotive batteries is also supported by the growing aftermarket for replacement batteries, as well as by the expansion of automotive manufacturing in emerging economies.

Increasing Electrification of Vehicles

The automotive industry's shift towards electrification is a significant driver of the automotive battery market. Governments worldwide are implementing stricter emission regulations to combat climate change, pushing automakers to develop more hybrid and electric vehicles (EVs) that rely heavily on advanced battery systems. This regulatory push, coupled with growing consumer awareness and preference for sustainable transportation options, has accelerated the demand for high-capacity, long-lasting automotive batteries. For instance, major automotive markets like the European Union, China, and the United States have set ambitious targets for EV sales and emission reductions over the next decade, necessitating substantial advancements in battery technology and production capabilities.

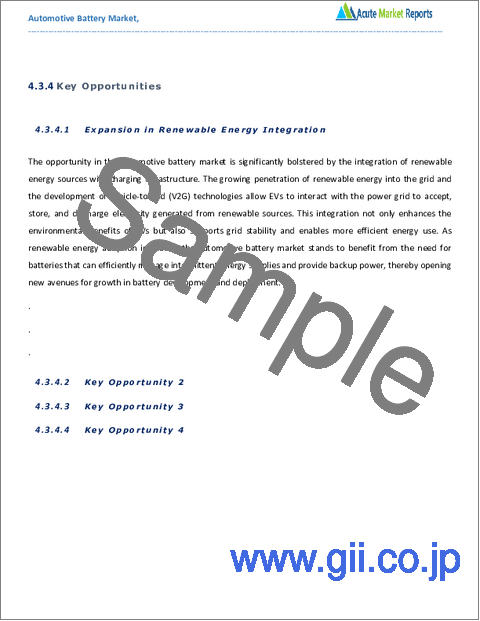

Expansion in Renewable Energy Integration

The opportunity in the automotive battery market is significantly bolstered by the integration of renewable energy sources with charging infrastructure. The growing penetration of renewable energy into the grid and the development of vehicle-to-grid (V2G) technologies allow EVs to interact with the power grid to accept, store, and discharge electricity generated from renewable sources. This integration not only enhances the environmental benefits of EVs but also supports grid stability and enables more efficient energy use. As renewable energy adoption increases, the automotive battery market stands to benefit from the need for batteries that can efficiently manage intermittent energy supplies and provide backup power, thereby opening new avenues for growth in battery development and deployment.

High Initial Investment Costs

A significant restraint in the automotive battery market is the high initial investment required for research, development, and manufacturing facilities capable of producing advanced battery technologies. The materials used in batteries, such as lithium and cobalt, are expensive and subject to price volatility. Additionally, setting up manufacturing facilities that adhere to safety and environmental standards involves substantial financial outlay, which can be a barrier for new entrants and can limit the expansion capacity of existing players. These high costs are often passed on to the consumer, making EVs more expensive than their internal combustion counterparts, which can inhibit the adoption of electric vehicles and, consequently, the growth of the automotive battery market.

Supply Chain Complexity

Managing the complex supply chain for battery production presents a major challenge in the automotive battery market. The supply chain for automotive batteries involves several critical raw materials that are sourced globally, leading to potential vulnerabilities including geopolitical tensions, regulatory changes, and logistic disruptions. For example, lithium and cobalt mining are concentrated in a few countries that can exercise significant influence over global supply and pricing. Moreover, the need for high standards of quality control, the requirement for rapid scalability in production, and the pressure to reduce costs while maintaining sustainability standards further complicate supply chain management, posing a challenge to steady growth in the automotive battery sector.

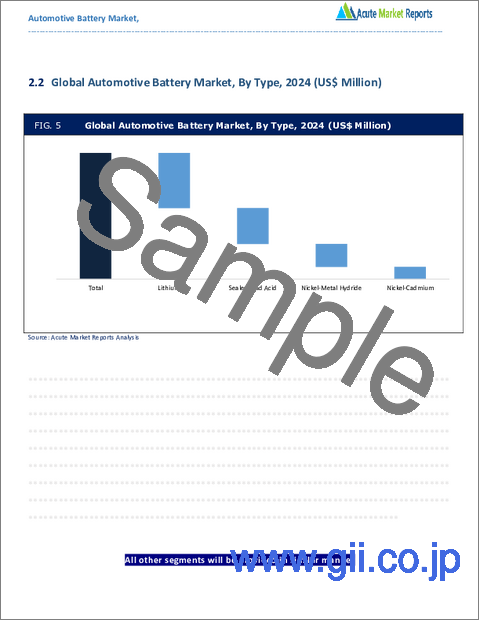

Market Segmentation by Type

The automotive battery market is segmented by type into Lithium Ion, Sealed Lead Acid, Nickel-Metal Hydride, and Nickel-Cadmium. Among these, Lithium Ion batteries are witnessing the highest Compound Annual Growth Rate (CAGR) due to their higher energy density, longer lifespan, and increasing adoption in electric vehicles (EVs). Their ability to provide a higher power-to-weight ratio makes them ideal for use in modern EVs that require efficient, lightweight, and space-saving energy solutions. Additionally, technological advancements in lithium ion batteries, such as improvements in cathode materials and electrolyte solutions, have significantly enhanced their performance and safety levels, further driving their market growth. Despite the higher cost associated with lithium ion batteries, their demand is expected to continue rising, driven by the global push towards electric mobility and renewable energy applications. On the other hand, Sealed Lead Acid batteries generate the highest revenue within the segment, primarily due to their widespread use in traditional internal combustion engine (ICE) vehicles and various industrial applications. These batteries are favored for their reliability, lower upfront cost, and established recycling infrastructure, making them a staple in automotive starting, lighting, and ignition applications. However, as the automotive industry gradually shifts towards electrification, the demand for sealed lead acid batteries is expected to see a relative decline, while lithium ion batteries are poised to dominate the future market landscape.

Market Segmentation by Propulsion

In terms of propulsion, the automotive battery market is categorized into Internal Combustion Engine (ICE) and Electric. The segment for Electric propulsion is experiencing the highest CAGR, driven by the global transition towards sustainable transportation and the increasing governmental incentives and regulations favoring electric vehicles. The growth in the electric propulsion segment is significantly propelled by the escalating demand for EVs, which require advanced battery systems to operate. This demand is further supported by improvements in battery technology that have reduced costs and extended the driving range of EVs, making them more accessible and appealing to a broader range of consumers. Meanwhile, batteries for ICE vehicles still account for the highest revenue in the propulsion segment due to the sheer volume of ICE vehicles in operation globally. Despite the growth in EVs, ICE vehicles continue to dominate the automotive market in regions where electric infrastructure is still developing or where consumer preference for ICE vehicles remains strong. However, the revenue growth in the ICE segment is expected to slow down as more automakers pivot to electric vehicle production and as stricter emission regulations reduce the production and sale of ICE vehicles. Looking forward, the electric segment is projected to surpass the ICE segment in terms of revenue as the adoption of electric vehicles accelerates worldwide, spurred by technological advancements and shifting consumer preferences towards more environmentally friendly transportation options.

Geographic Segment

The automotive battery market is geographically segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific dominates both in terms of highest Compound Annual Growth Rate (CAGR) and highest revenue percentage. This region's leadership in the market can be attributed to its robust automotive manufacturing sector, rising adoption of electric vehicles, and significant investments in battery technology innovations, particularly in countries like China, Japan, and South Korea. These countries are home to some of the world's leading battery manufacturers and have government policies that aggressively promote the adoption of electric vehicles. The presence of a large consumer base and increasing environmental awareness also contribute to the rapid growth of this market. Additionally, Asia Pacific benefits from lower production costs and advanced technological capabilities, which are pivotal in driving the region's market dominance. Conversely, North America and Europe also show significant market activities due to stringent emission regulations and high consumer awareness regarding sustainable technologies. However, these regions trail Asia Pacific in terms of growth rate and revenue due to the faster saturation of the market and earlier adoption of emerging technologies.

Competitive Trends and Key Strategies

In the competitive landscape, major players like Leoch International Tech, Furukawa Electric Co. Ltd., Hitachi Ltd., Haldex Incorporated, Exide Industries Limited, Panasonic Corporation, CATL, GS Yuasa, LG Chem, Samsung SDI, and SK Innovation, along with other competitors, are shaping the market dynamics. In 2024, these companies focused on expanding their market presence through strategic alliances, advanced technology deployment, and expanding production capacities to meet the growing demand for high-performance automotive batteries. Panasonic Corporation and LG Chem have been prominent in advancing lithium-ion technology with significant investments in research and development to enhance battery efficiency and safety features. Meanwhile, CATL continued to expand its global footprint by establishing new manufacturing units and investing in raw material procurement strategies to hedge against price volatility. GS Yuasa and Exide Industries focused on innovation in lead-acid and alternative battery chemistries to maintain competitive pricing and appeal in traditional automotive markets. Looking ahead from 2025 to 2033, these companies are expected to intensify their strategies around sustainability and recycling practices to align with global regulatory standards and consumer expectations. New product developments and collaborations with automotive manufacturers are anticipated to be crucial in maintaining competitive edges. Additionally, the adoption of digital and automated technologies in manufacturing processes is expected to be a key strategy to reduce production costs and improve product quality, positioning these companies to leverage growth opportunities in both established and emerging markets.

Historical & Forecast Period

This study report represents an analysis of each segment from 2023 to 2033 considering 2024 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2025 to 2033.

The current report comprises quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends & technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. The key data points that enable the estimation of Automotive Battery market are as follows:

Research and development budgets of manufacturers and government spending

Revenues of key companies in the market segment

Number of end users & consumption volume, price, and value.

Geographical revenues generated by countries considered in the report

Micro and macro environment factors that are currently influencing the Automotive Battery market and their expected impact during the forecast period.

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top-down and bottom-up approach for validation of market estimation assures logical, methodical, and mathematical consistency of the quantitative data.

Market Segmentation

- Type

- Lithium Ion

- Sealed Lead Acid

- Nickel-Metal Hydride

- Nickel-Cadmium

- Propulsion

- Internal Combustion Engine

- Gasoline

- Diesel

- Electric

- Battery Electric

- Hybrid Electric

- Vehicle Type

- Passenger Vehicle

- Light Commercial Vehicle

- Heavy Duty Trucks

- Bus & Coaches

- Two Wheeler Vehicle

- Sales Channel

- OEM

- Aftermarket

- Region Segment (2023-2033; US$ Million)

- North America

- U.S.

- Canada

- Rest of North America

- UK and European Union

- UK

- Germany

- Spain

- Italy

- France

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East and Africa

- GCC

- Africa

- Rest of Middle East and Africa

Key questions answered in this report

- What are the key micro and macro environmental factors that are impacting the growth of Automotive Battery market?

- What are the key investment pockets concerning product segments and geographies currently and during the forecast period?

- Estimated forecast and market projections up to 2033.

- Which segment accounts for the fastest CAGR during the forecast period?

- Which market segment holds a larger market share and why?

- Are low and middle-income economies investing in the Automotive Battery market?

- Which is the largest regional market for Automotive Battery market?

- What are the market trends and dynamics in emerging markets such as Asia Pacific, Latin America, and Middle East & Africa?

- Which are the key trends driving Automotive Battery market growth?

- Who are the key competitors and what are their key strategies to enhance their market presence in the Automotive Battery market worldwide?

Table of Contents

1. Preface

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. Target Audience

- 1.1.3. Key Offerings

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.3.1. Phase I - Secondary Research

- 1.3.2. Phase II - Primary Research

- 1.3.3. Phase III - Expert Panel Review

- 1.3.4. Assumptions

- 1.3.5. Approach Adopted

2. Executive Summary

- 2.1. Market Snapshot: Global Automotive Battery Market

- 2.2. Global Automotive Battery Market, By Type, 2024 (US$ Million)

- 2.3. Global Automotive Battery Market, By Propulsion, 2024 (US$ Million)

- 2.4. Global Automotive Battery Market, By Vehicle Type, 2024 (US$ Million)

- 2.5. Global Automotive Battery Market, By Sales Channel, 2024 (US$ Million)

- 2.6. Global Automotive Battery Market, By Geography, 2024 (US$ Million)

- 2.7. Attractive Investment Proposition by Geography, 2024

3. Automotive Battery Market: Competitive Analysis

- 3.1. Market Positioning of Key Automotive Battery Market Vendors

- 3.2. Strategies Adopted by Automotive Battery Market Vendors

- 3.3. Key Industry Strategies

4. Automotive Battery Market: Macro Analysis & Market Dynamics

- 4.1. Introduction

- 4.2. Global Automotive Battery Market Value, 2023 - 2033, (US$ Million)

- 4.3. Market Dynamics

- 4.3.1. Market Drivers

- 4.3.2. Market Restraints

- 4.3.3. Key Challenges

- 4.3.4. Key Opportunities

- 4.4. Impact Analysis of Drivers and Restraints

- 4.5. See-Saw Analysis

- 4.6. Porter's Five Force Model

- 4.6.1. Supplier Power

- 4.6.2. Buyer Power

- 4.6.3. Threat Of Substitutes

- 4.6.4. Threat Of New Entrants

- 4.6.5. Competitive Rivalry

- 4.7. PESTEL Analysis

- 4.7.1. Political Landscape

- 4.7.2. Economic Landscape

- 4.7.3. Technology Landscape

- 4.7.4. Legal Landscape

- 4.7.5. Social Landscape

5. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 5.1. Market Overview

- 5.2. Growth & Revenue Analysis: 2024 Versus 2033

- 5.3. Market Segmentation

- 5.3.1. Lithium Ion

- 5.3.2. Sealed Lead Acid

- 5.3.3. Nickel-Metal Hydride

- 5.3.4. Nickel-Cadmium

6. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 6.1. Market Overview

- 6.2. Growth & Revenue Analysis: 2024 Versus 2033

- 6.3. Market Segmentation

- 6.3.1. Internal Combustion Engine

- 6.3.1.1. Gasoline

- 6.3.1.2. Diesel

- 6.3.2. Electric

- 6.3.2.1. Battery Electric

- 6.3.2.2. Hybrid Electric

- 6.3.1. Internal Combustion Engine

7. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 7.1. Market Overview

- 7.2. Growth & Revenue Analysis: 2024 Versus 2033

- 7.3. Market Segmentation

- 7.3.1. Passenger Vehicle

- 7.3.2. Light Commercial Vehicle

- 7.3.3. Heavy Duty Trucks

- 7.3.4. Bus & Coaches

- 7.3.5. Two Wheeler Vehicle

8. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 8.1. Market Overview

- 8.2. Growth & Revenue Analysis: 2024 Versus 2033

- 8.3. Market Segmentation

- 8.3.1. OEM

- 8.3.2. Aftermarket

9. North America Automotive Battery Market, 2023-2033, USD (Million)

- 9.1. Market Overview

- 9.2. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 9.3. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 9.4. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 9.5. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 9.6.Automotive Battery Market: By Region, 2023-2033, USD (Million)

- 9.6.1.North America

- 9.6.1.1. U.S.

- 9.6.1.1.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 9.6.1.1.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 9.6.1.1.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 9.6.1.1.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 9.6.1.2. Canada

- 9.6.1.2.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 9.6.1.2.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 9.6.1.2.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 9.6.1.2.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 9.6.1.3. Rest of North America

- 9.6.1.3.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 9.6.1.3.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 9.6.1.3.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 9.6.1.3.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 9.6.1.1. U.S.

- 9.6.1.North America

10. UK and European Union Automotive Battery Market, 2023-2033, USD (Million)

- 10.1. Market Overview

- 10.2. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 10.3. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 10.4. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 10.5. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 10.6.Automotive Battery Market: By Region, 2023-2033, USD (Million)

- 10.6.1.UK and European Union

- 10.6.1.1. UK

- 10.6.1.1.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 10.6.1.1.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 10.6.1.1.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 10.6.1.1.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 10.6.1.2. Germany

- 10.6.1.2.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 10.6.1.2.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 10.6.1.2.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 10.6.1.2.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 10.6.1.3. Spain

- 10.6.1.3.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 10.6.1.3.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 10.6.1.3.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 10.6.1.3.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 10.6.1.4. Italy

- 10.6.1.4.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 10.6.1.4.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 10.6.1.4.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 10.6.1.4.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 10.6.1.5. France

- 10.6.1.5.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 10.6.1.5.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 10.6.1.5.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 10.6.1.5.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 10.6.1.6. Rest of Europe

- 10.6.1.6.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 10.6.1.6.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 10.6.1.6.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 10.6.1.6.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 10.6.1.1. UK

- 10.6.1.UK and European Union

11. Asia Pacific Automotive Battery Market, 2023-2033, USD (Million)

- 11.1. Market Overview

- 11.2. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 11.3. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 11.4. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 11.5. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 11.6.Automotive Battery Market: By Region, 2023-2033, USD (Million)

- 11.6.1.Asia Pacific

- 11.6.1.1. China

- 11.6.1.1.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 11.6.1.1.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 11.6.1.1.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 11.6.1.1.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 11.6.1.2. Japan

- 11.6.1.2.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 11.6.1.2.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 11.6.1.2.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 11.6.1.2.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 11.6.1.3. India

- 11.6.1.3.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 11.6.1.3.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 11.6.1.3.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 11.6.1.3.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 11.6.1.4. Australia

- 11.6.1.4.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 11.6.1.4.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 11.6.1.4.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 11.6.1.4.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 11.6.1.5. South Korea

- 11.6.1.5.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 11.6.1.5.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 11.6.1.5.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 11.6.1.5.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 11.6.1.6. Rest of Asia Pacific

- 11.6.1.6.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 11.6.1.6.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 11.6.1.6.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 11.6.1.6.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 11.6.1.1. China

- 11.6.1.Asia Pacific

12. Latin America Automotive Battery Market, 2023-2033, USD (Million)

- 12.1. Market Overview

- 12.2. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 12.3. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 12.4. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 12.5. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 12.6.Automotive Battery Market: By Region, 2023-2033, USD (Million)

- 12.6.1.Latin America

- 12.6.1.1. Brazil

- 12.6.1.1.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 12.6.1.1.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 12.6.1.1.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 12.6.1.1.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 12.6.1.2. Mexico

- 12.6.1.2.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 12.6.1.2.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 12.6.1.2.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 12.6.1.2.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 12.6.1.3. Rest of Latin America

- 12.6.1.3.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 12.6.1.3.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 12.6.1.3.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 12.6.1.3.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 12.6.1.1. Brazil

- 12.6.1.Latin America

13. Middle East and Africa Automotive Battery Market, 2023-2033, USD (Million)

- 13.1. Market Overview

- 13.2. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 13.3. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 13.4. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 13.5. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 13.6.Automotive Battery Market: By Region, 2023-2033, USD (Million)

- 13.6.1.Middle East and Africa

- 13.6.1.1. GCC

- 13.6.1.1.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 13.6.1.1.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 13.6.1.1.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 13.6.1.1.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 13.6.1.2. Africa

- 13.6.1.2.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 13.6.1.2.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 13.6.1.2.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 13.6.1.2.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 13.6.1.3. Rest of Middle East and Africa

- 13.6.1.3.1. Automotive Battery Market: By Type, 2023-2033, USD (Million)

- 13.6.1.3.2. Automotive Battery Market: By Propulsion, 2023-2033, USD (Million)

- 13.6.1.3.3. Automotive Battery Market: By Vehicle Type, 2023-2033, USD (Million)

- 13.6.1.3.4. Automotive Battery Market: By Sales Channel, 2023-2033, USD (Million)

- 13.6.1.1. GCC

- 13.6.1.Middle East and Africa

14. Company Profile

- 14.1. Leoch International Tech,

- 14.1.1. Company Overview

- 14.1.2. Financial Performance

- 14.1.3. Product Portfolio

- 14.1.4. Strategic Initiatives

- 14.2. Furukawa Electric Co. Ltd.,

- 14.2.1. Company Overview

- 14.2.2. Financial Performance

- 14.2.3. Product Portfolio

- 14.2.4. Strategic Initiatives

- 14.3. Hitachi Ltd.,

- 14.3.1. Company Overview

- 14.3.2. Financial Performance

- 14.3.3. Product Portfolio

- 14.3.4. Strategic Initiatives

- 14.4. Haldex Incorporated,

- 14.4.1. Company Overview

- 14.4.2. Financial Performance

- 14.4.3. Product Portfolio

- 14.4.4. Strategic Initiatives

- 14.5. Exide Industries Limited,

- 14.5.1. Company Overview

- 14.5.2. Financial Performance

- 14.5.3. Product Portfolio

- 14.5.4. Strategic Initiatives

- 14.6. Panasonic Corporation,

- 14.6.1. Company Overview

- 14.6.2. Financial Performance

- 14.6.3. Product Portfolio

- 14.6.4. Strategic Initiatives

- 14.7. CATL

- 14.7.1. Company Overview

- 14.7.2. Financial Performance

- 14.7.3. Product Portfolio

- 14.7.4. Strategic Initiatives

- 14.8. GS Yuasa

- 14.8.1. Company Overview

- 14.8.2. Financial Performance

- 14.8.3. Product Portfolio

- 14.8.4. Strategic Initiatives

- 14.9. LG Chem,

- 14.9.1. Company Overview

- 14.9.2. Financial Performance

- 14.9.3. Product Portfolio

- 14.9.4. Strategic Initiatives

- 14.10. Samsung SDI

- 14.10.1. Company Overview

- 14.10.2. Financial Performance

- 14.10.3. Product Portfolio

- 14.10.4. Strategic Initiatives

- 14.11. SK Innovation

- 14.11.1. Company Overview

- 14.11.2. Financial Performance

- 14.11.3. Product Portfolio

- 14.11.4. Strategic Initiatives

- 14.12. Others

- 14.12.1. Company Overview

- 14.12.2. Financial Performance

- 14.12.3. Product Portfolio

- 14.12.4. Strategic Initiatives