レドックスフロー電池:市場予測ライン (23ライン)・ロードマップ・技術・製造業者 (59社)・最新の研究パイプライン (2025-2045年)

Redox Flow Batteries: 23 Market Forecast Lines, Roadmaps, Technologies, 59 Manufacturers, Latest Research Pipeline 2025-2045- 発行日

- ページ情報

- 英文 327 Pages

- 納期

- 即日から翌営業日

- 商品コード

- 1578352

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

- 通信/IT関連専門 通信/IT関連専門を専門とする市場調査会社です。

概要

レドックスフロー電池 (RFB) は、数十年間手付かずの状態にありましたが、現在は非常に活発な分野となっています。この理由としては主に、適切な市場ニーズの台頭や、重要な改良がなされている点などがあります。

当レポートでは、RFBの製造業者は2045年には200億米ドル超、あるいはその倍の事業規模を示すと予測しています。鍵となるのは、初期費用やLCOSなどのRFBの制約を克服する急速な進歩です。例えば、米国エネルギー省の新しいレポートによると、RFBは送電網用の長期貯蔵に必要とされる目安であるMWhあたり50ドルを実現できる3つの選択肢のうちの1つと報告されています。また、他の2つの技術は大規模な土木工事を必要としますが、RFBは必要としません。

復活するソーラーマイクログリッド

同様に重要な点として、10時間の持続時間を持ち、安全にスタック可能なRFBは、急速に成長しているソーラーマイクログリッド市場向けにすでに広く購入されているという点があります。実際、太陽光の間欠性への対応はRFBで容易に達成可能です。RFBは、必要に応じて電力と容量を個別に調整できるため、規模の経済性があります。RFBは、短時間と長時間の貯蔵を1台で行うことができます。

キャプション:3つのLDESサイズで異なる勝者 (2025-2045年)

現在のエビデンスに基づく

当レポートでは、世界のレドックスフロー電池 (RFB) の市場を調査し、長時間エネルギー貯蔵 (LDES) 技術の概要、RFBハードウェアとシステム設計、研究パイプライン、技術ロードマップ、グリッド内外のRFBの展望、主要企業のプロファイルなどをまとめています。

目次

第1章 エグゼクティブサマリー・総論

第2章 イントロダクション

- エネルギーの基礎とLCOS

- 急速なコスト削減で再生可能エネルギーへの参入を加速

- 太陽光発電の勝利と間欠性の課題

- LDESの回避ルート

- LDESの定義と選択肢の比較

- グリッドとグリッド外のLDESに対する異なるニーズ

- 2025年の主要なプロジェクトと主要な技術サブセット

- LDESの障害、代替案、投資環境

- LDESツールキット

- 技術別のパフォーマンスに関する最新の独立評価

- その他の側面

第3章 RFBの設計原則・研究パイプライン・毒素代替品・SWOT評価

- 概要、コスト分析、フットプリントの削減、次の設計課題

- 化学と反応によるRFBのタイプとパラメータ評価

- 基本的なRFBハードウェアとシステム設計

- バナジウムRFB設計

- オールアイアンRFB設計

- 鉄クロム金属配位子設計

- その他の金属配位子RFB設計

- 水素臭素RFB設計

- 有機RFB設計

- RFB膜設計

- RFB研究パイプライン

- 取り組むべき毒素問題と各社の現在の成果

- SWOT評価:通常のRFB

- SWOT評価:据置型貯蔵におけるRFB

- SWOT評価:ハイブリッドRFB

- SWOT評価:代替品と比較したバナジウムRFB

第4章 59社のRFB企業・製造業者・主要材料供給業者の比較・紹介

- 8要素による比較:名前、ブランド、技術、技術の準備状況、グリッド外の焦点、LDESの焦点、コメント

- 58社のRFB企業 (メーカー48社・主要材料/サービス10社) のプロファイル・グリッド外LDESの可能性

- Agora Energy Technologies

- Allegro Energy

- Beijing Herui Energy Storage

- Bryte Batteries Norway

- CellCube (Enerox)

- CERQ

- China CEC

- CMBlu

- Cougar Creek Technologies

- EDF bought Pivot Power

- Elestor

- ESS

- Green Energy Storage

- H2

- HBIS

- Hubei Lvdong

- Hunan Huifeng High Tech Energy

- HydraRedox

- Invinity Energy Systems

- Jolt Energy Storage Solutions

- Kemiwatt

- Korid Energy / AVESS

- Largo Inc

- LE System

- Lockheed Martin

- nanoFlowcell

- Noon Energy

- Pinflow

- Primus Power

- Prolux

- Quino Energy

- Redflow

- Redox One

- RFC Power

- Rongke Power

- Salgenx

- Shanghai Electric Energy Storage

- Shmid

- State Power Investment Corp.

- StorEn Technologies

- StorTera

- Stryten Energy

- Sumitomo Electric

- Suntien Green Energy

- Swanbarton

- VFlowTech

- Vionx Energy

- VizBlue

- VLiquid

- Voith

- Volterion

- VoltStorage

- VRB Energy

- Wattjoule Corporation

- WeView

- Wuhan NARI

- XL Batteries

- Yinfeng New Energy

- Zhiguang

第5章 LDES (長時間エネルギー貯蔵) 向けRFB

- 概要

- RFBの研究:LDESに軸足を移す

- RFB LDESプロジェクトと2025年までの計算:時間、容量、現在勝っている技術

- RFB LDESの成果と目標

- 勝利をもたらすLDESレドックスフロー電池技術

- LDES機能に移行する可能性のあるRFB企業44社:8つの列で比較

- グリッドの向こう側とLDES RFBへの動向のリーダー

- LDESにおけるRFBの競争上の位置を明らかにする8つのパラメータマップ

第6章 グリッド外LDES向けレドックスフロー電池

- 概要

- グリッド外:建物、産業プロセス、ミニグリッド、マイクログリッド、その他

- グリッド外の発電と管理

- より長期の保管が必要となる傾向

- LDESの必要性を減らす戦略とLDESの拡大の抑制

- グリッドおよびグリッド外向けのLDESツールキット

- グリッド外発電の市場促進要因としてのLDES提供

- グリッド外貯蔵の多機能性

- LDESコストの課題

- グリッドおよびグリッド外におけるLDES技術の可能性の全体像

- グリッド外LDESが2025~2045年にRFBの最大数・最大価値の市場になる理由

- 2024~2045年に販売されるLDESの最大数を支える技術

目次

Summary

Redox flow batteries are now a very active area after decades in the wilderness. That is largely because the appropriate market needs have arrived but it is increasingly reinforced by important improvements.

Essential new report

The new commercially-oriented 327-page report, "Redox Flow Batteries: 23 Market Forecast Lines, Roadmaps, Technologies, 59 Manufacturers, Latest Research Pipeline 2025-2045" predicts that these manufacturers will share over $20 billion of business in 2045, possibly double. Key is the now rapid progress in overcoming RFB limitations such as up-front cost and Levelised Cost of Storage LCOS. For example, a new US Department of Energy report finds that RFB are one of only three options able to drop to the $50/MWh it sees as necessary for long duration storage for grids. The other two technologies identified need massive earthworks: RFB does not.

Solar microgrids resurgent

Equally important, safely stackable RFB with ten hours duration (MWh divided by MW) are already widely purchased for solar microgrids, a rapidly-growing market. Indeed, coping with longer solar intermittency is easily achievable with RFB and most competition cannot keep up with that trend mainly driven by solar power taking over but also wind and their attendant intermittency. RFB has economy of scale due to separate adjustment of power and capacity as needed. RFB can perform short-and long-duration storage in one unit.

Traditional vanadium gaining business

The traditional vanadium RFB is gaining business. That is mostly for systems capable of being off-grid but some grid giants are being erected in China. An even bigger one is now planned in Europe.

Iron and other approaches slash cost and hybrids go small

Much of the effort is directed at using iron and, later, other options, to save cost. For different applications, the industry is perfecting small hybrids of RFB with one side having conventional battery structure instead of a tank of liquid. These may offer long duration in our solar buildings, where space is very tight. Eliminate the expensive ion exchange membrane? Offer 50-year life? Switch it off to store power in its liquids for a year with no leak or fade? Only the new Zhar Research report has the analysis, latest research, roadmaps and forecasts.

What the report offers

The Executive Summary and Conclusions is sufficient in itself with the new infograms, three SWOT appraisals, roadmaps and 23 forecast lines, graphs with explanations. The Introduction (30 pages) explains the context of renewable energy, Long Duration Energy Storage (most of the future RFB opportunity), its best technologies compared with many diagrams and comparison tables. Here are escape routes from needing LDES, because this report is balanced, real-world appraisal of your opportunity, not the maximised dream of a trade association. The conclusion is that LDES will not be as large a market as enthusiasts portray, but huge, nonetheless.

Chapter 3. RFB design principles, research pipeline, toxigen alternatives and SWOT appraisals (63 pages) looks closely at the different chemistries, electrolytes, membranes and so on, with infograms and tables. Understand the implications of the latest research pipeline and how to deal with matters of concern to industry such as toxicity issues. Which objectives are far off, even unrealistic?

Chapter 4. compares in eight columns then profiles 59 RFB companies, mostly manufacturers, but also some key materials providers in its 132 pages. Which four are already serious about 100 day LDES RFB, embarrassing the competition facing this very real emerging need? Chapter 5. Long Duration Energy Storage LDES RFB (28 pages) is equally detailed. It closely examines 13 relevant research advances in 2024. Parameters required, achieved and likely are revealed and explained because LDES is where the main potential of RFB now lies - from compact hybrid RFB in a building to very large RFB in a grid. Chapter 6. Redox flow batteries for LDES beyond grids (15 pages) then takes another look at this aspect because it will probably dominate value sales 2025-2045.

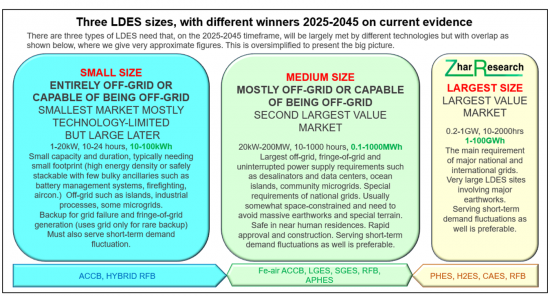

CAPTION: Three LDES sizes, with different winners 2025-2045

on current evidence

Table of Contents

1. Executive summary and conclusions

- 1.1. Purpose of this report

- 1.2. Methodology of this analysis

- 1.2. The different characteristics of grid utility and beyond-grid LDES 2025-2045

- 1.3. Eight primary conclusions: RFB markets and industry with ten infograms

- 1.4. 19 primary conclusions concerning RFB technologies

- 1.4.1. The 19 conclusions

- 1.4.2. Research pipeline analysis: 108 papers from 2022-2024

- 1.4.3. Seven RFB parameters in volume sales, vanadium vs other 2025-2045

- 1.5. 48 RFB manufacturers compared in 8 columns: name, brand, technology, tech. readiness, beyond grid focus, LDES focus, comment

- 1.6. Pie charts of active material and country of RFB manufacturers

- 1.7. SWOT appraisal of regular RFB

- 1.8. SWOT appraisal of hybrid RFB

- 1.9. SWOT appraisal of vanadium RFB against alternatives

- 1.10. RFB roadmap by market and by technology 2025-2045

- 1.11. Long Duration Energy Storage LDES roadmap 2025-2045

- 1.12. Market forecasts in 23 lines

- 1.12.1. RFB global value market grid vs beyond-grid 2025-2045 table, graph, explanation

- 1.12.2. RFB global value market short term and LDES 2025-2045 table, graph, explanation

- 1.12.3. Vanadium vs iron vs other RFB value market % 2025-2045 table, graph, explanation

- 1.12.4. Vanadium loses RFB share but rises elsewhere

- 1.12.5. Regional share of RFB value market in four regions 2025-2045

- 1.12.6. LDES value market $ billion in 9 technology categories with explanation 2025-2045

- 1.12.7. LDES total value market showing beyond-grid gaining share 2025-2045

2. Introduction

- 2.1. Energy fundamentals and LCOS

- 2.2. Racing into renewables with rapid cost reduction

- 2.3. Solar winning and the intermittency challenge

- 2.4. Escape routes from LDES

- 2.4.1. General situation

- 2.4.2. Reduction of LDES need by unrelated actions

- 2.4.3. Many options to deliberately reduce the need for LDES

- 2.5. LDES definitions and choices compared

- 2.6. The very different needs for grid vs beyond-grid LDES 2025-2045

- 2.7. Leading projects in 2025 showing leading technology subsets

- 2.8. LDES impediments, alternatives and investment climate

- 2.9. LDES toolkit

- 2.9.1. Overview

- 2.9.2. LDES choices compared

- 2.10. Latest independent assessments of performance by technology

- 2.12. Other aspects

3. RFB design principles, research pipeline, toxigen alternatives and SWOT appraisals

- 3.1. Overview, cost analysis, footprint reduction and next design challenges

- 3.1.1. General

- 3.1.2. Cost issues, cost breakdown and potential improvement

- 3.1.3. Footprint reduction

- 3.2. Types of RFB by chemistry and reaction with parameter appraisal

- 3.3. Basic RFB hardware and system design

- 3.4. Vanadium RFB design

- 3.5. All-iron RFB design

- 3.6. Iron Chromium metal ligand design

- 3.7. Other metal ligand RFB design

- 3.8. Hydrogen-bromine RFB design

- 3.9. Organic RFB design

- 3.10. RFB membrane design

- 3.10.1. Issues

- 3.10.2. Membrane difficulty levels and materials used and proposed

- 3.10.3. Recent RFB membrane research

- 3.11. RFB research pipeline

- 3.11.1. Overview

- 3.11.2. Extreme promises

- 3.11.3. Research pipeline analysis: 108 papers from 2022 to 2024

- 3.11.4. Iron-based electrolyte RFB research 2024

- 3.11.5. Vanadium electrolyte RFB research

- 3.11.6. Organic electrolyte RFB research

- 3.11.7. Zinc electrolyte RFB research

- 3.11.8. General and other metals RFB research

- 3.11.9. Manganese-based RFB research

- 3.12. Toxigen issues to tackle and current achievements by company

- 3.13. SWOT appraisal of regular RFB

- 3.14. SWOT appraisal of RFB for stationary storage

- 3.15. SWOT appraisal of hybrid RFB

- 3.16. SWOT appraisal of vanadium RFB against alternatives

4. 59 RFB companies, manufacturers, key materials providers compared and profiled in 132 pages

- 4.1. 58 RFB companies compared in 8 columns: name, brand, technology, tech. readiness, beyond grid focus, LDES focus, comment

- 4.2. Profiles of 58 RFB companies (48 manufacturers, 10 in key materials/ services) in 130 pages with appraisal for beyond-grid LDES potential

- Agora Energy Technologies

- Allegro Energy

- Beijing Herui Energy Storage

- Bryte Batteries Norway

- CellCube (Enerox)

- CERQ

- China CEC

- CMBlu

- Cougar Creek Technologies

- EDF bought Pivot Power

- Elestor

- ESS

- Green Energy Storage

- H2

- HBIS

- Hubei Lvdong

- Hunan Huifeng High Tech Energy

- HydraRedox

- Invinity Energy Systems

- Jolt Energy Storage Solutions

- Kemiwatt

- Korid Energy / AVESS

- Largo Inc

- LE System

- Lockheed Martin

- nanoFlowcell

- Noon Energy

- Pinflow

- Primus Power

- Prolux

- Quino Energy

- Redflow

- Redox One

- RFC Power

- Rongke Power

- Salgenx

- Shanghai Electric Energy Storage

- Shmid

- State Power Investment Corp.

- StorEn Technologies

- StorTera

- Stryten Energy

- Sumitomo Electric

- Suntien Green Energy

- Swanbarton

- VFlowTech

- Vionx Energy

- VizBlue

- VLiquid

- Voith

- Volterion

- VoltStorage

- VRB Energy

- Wattjoule Corporation

- WeView

- Wuhan NARI

- XL Batteries

- Yinfeng New Energy

- Zhiguang

5. Long Duration Energy Storage LDES RFB

- 5.1. Overview

- 5.1.1. Definition

- 5.1.2. Very different LDES needs for grid vs beyond-grid

- 5.1.3. RFB capability in the LDES world

- 5.1.4. Duration vs power of LDES technologies not needing major earthworks compared with others in 2025

- 5.2. RFB research pivoting to LDES

- 5.2.1. Overview of research

- 5.2.2. 13 important RFB research advances in 2024 relevant to LDES

- 5.3. RFB LDES projects and calculations to 2025: hours, capacity, currently winning technology

- 5.4. RFB LDES achievements and aspirations 2025-2045

- 5.5. Winning LDES redox flow battery technologies 2025-2045

- 5.7 44 RFB companies likely to move to LDES capability compared in 8 columns

- 5.8. Leaders in the trends to beyond-grid and LDES RFB

- 5.9. Eight parameter maps revealing RFB competitive position in LDES

6. Redox flow batteries for LDES beyond grids

- 6.1. Overview

- 6.2. Beyond-grid: buildings, industrial processes, minigrids, microgrids, other

- 6.3. Beyond-grid electricity production and management

- 6.4. The trend to needing longer duration storage

- 6.5. Strategies for reducing LDES need can limit escalation of LDES

- 6.6. LDES toolkit for grid and beyond-grid

- 6.7. Market drivers of beyond-grid electricity generation notably providing LDES

- 6.8. Multifunctional nature of beyond-grid storage

- 6.9. LDES cost challenge

- 6.10. Big picture of LDES technology potential for grid and beyond-grid

- 6.11. Why beyond-grid LDES will become the largest number and value market for RFB 2025-2045

- 6.12. Technologies for largest number of LDES sold 2024-2045

- 発行日

- 発行

- Zhar Research

- ページ情報

- 英文 327 Pages

- 納期

- 即日から翌営業日