|

|

市場調査レポート

商品コード

1346759

電動建設機械市場:現状分析と予測(2022~2030年)Electric Construction Equipment Market: Current Analysis and Forecast (2022-2030) |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 電動建設機械市場:現状分析と予測(2022~2030年) |

|

出版日: 2023年08月01日

発行: UnivDatos Market Insights Pvt Ltd

ページ情報: 英文 144 Pages

納期: 即日から翌営業日

|

- 全表示

- 概要

- 目次

電動建設機械市場は予測期間中14.72%のCAGRで力強い成長が見込まれます。世界の建設業界では、排出量の削減と作業効率の向上という2つの目標に後押しされ、電動建設機械の採用が大幅に増加しています。この移行は主要な建設市場において顕著であり、多額の投資がこの分野に流れ込んでいます。例えば、米国は2022年、電気建設機械の研究開発に2億米ドル以上を割り当て、技術革新を促進し、より持続可能な産業を創出することを目指しています。同様に、ある有名な建設会社が2021年に10億米ドルを投資してディーゼルエンジン駆動の機械を電気代替品に置き換えるなど、業界大手は自社の車両を電動化するために多額のコミットメントを行っています。このような事例は、より環境にやさしく、技術的に進んだ業界の未来を浮き彫りにする、具体的な資金的裏付けを伴う電動建設機械へのシフトの加速を強調するものです。

機器の種類によって、市場は電動掘削機、電動アースムーバー、電動ホイールローダー、電動アスファルト機器、その他に区分されます。このうち、電動掘削機セグメントは2022年の市場シェアが高いです。電動掘削機は、従来の燃料式掘削機に比べてメンテナンスが少なくて済み、安価な電力を利用できるため、耐用年数を通じて運用コストを大幅に削減できます。この魅力的な費用対効果により、建設会社は長期的な財務上の利点を認識しており、普及が進んでいます。

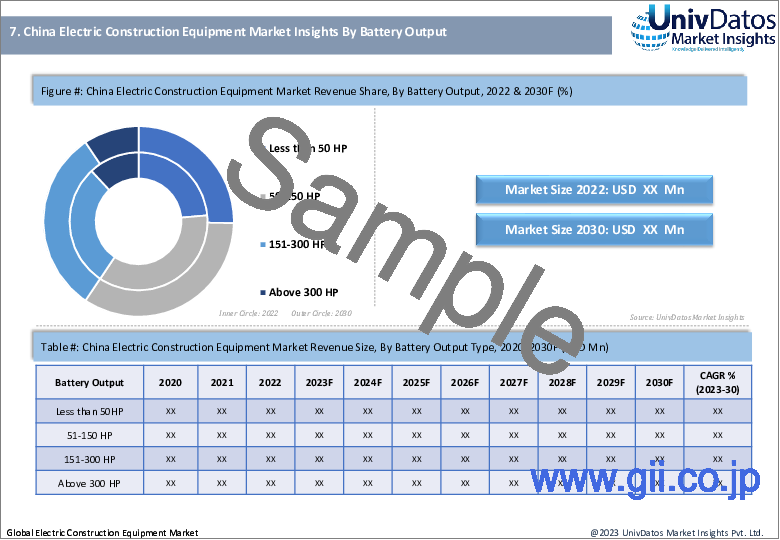

バッテリー出力に基づき、市場は50HP未満、50~150HP、151~300HP、300HP以上に区分されます。このうち、151~300HPのセグメントが2022年に高い市場シェアを占めています。この馬力レンジは、中規模プロジェクトからヘビーデューティー用途まで、幅広い建設作業に対応しています。建設会社は、これらの機械のバランスの取れた性能を高く評価しており、効率や能力に妥協することなく幅広い作業に取り組むことができます。この適応性は生産性の向上につながり、151~300HPの機器セグメントは建設業界の定番となっています。

バッテリーの種類によって、市場はリチウムイオン、鉛酸、その他に区分されます。このうち、2022年の市場シェアが高いのはリチウムイオンセグメントです。建設機械市場におけるリチウムイオンバッテリーの優位性は、その比類のないエネルギー密度、長寿命、急速充電能力に起因します。これらのバッテリーは、電動建設機械の稼働時間を延長し、ダウンタイムを削減し、生産性を向上させることで、実質的な利点を提供します。

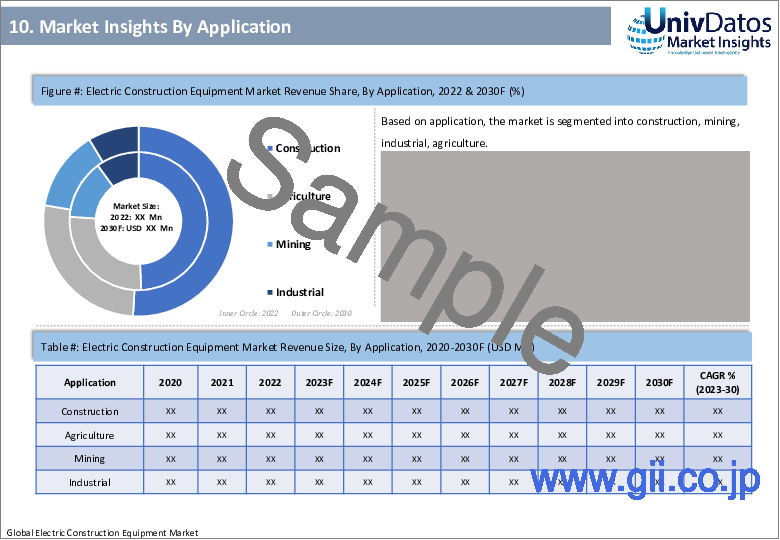

用途別に見ると、市場は建設、鉱業、工業、農業に区分されます。このうち、2022年の市場シェアが高いのは建設分野です。建設に対する固有のニーズが、このセグメントの高い市場シェアを牽引しています。インフラ開発、都市化、メンテナンス・プロジェクトは、膨大な数の機械と設備を絶えず必要としています。業界が進化するにつれ、より効率的で環境に優しいソリューションへの需要も高まっています。環境への影響に対する意識の高まりとともに、建設部門は汚染とエネルギー消費を最小限に抑える代替手段を模索しています。

産業用リレー産業の市場導入に関する理解を深めるため、市場は北米(米国、カナダ、その他の北米地域)、欧州(ドイツ、英国、フランス、イタリア、スペイン、その他の欧州地域)、アジア太平洋地域(中国、日本、インド、韓国、その他のアジア太平洋地域)、その他の地域における世界のプレゼンスに基づいて分析されています。アジア太平洋地域では、環境問題、急速な都市化、技術の進歩に後押しされ、電動建設機械の採用が著しく増加しています。例えば、中国の著名な建設機械メーカーであるSANYは、研究開発および生産設備に5,000万米ドルを超える投資を行い、2020年に全電気式コンパクトショベルを発表しました。この動きは、同地域の電動イノベーションへの献身を浮き彫りにし、アジア太平洋市場で電動機器が受け入れられつつあることを示しています。さらに、日本の大手建設会社である大林組は、2021年に電動建設機械を導入するため、約1,650万米ドルと推定される多額の投資を行っています。

目次

第1章 市場イントロダクション

- 市場の定義

- 主な目標

- ステークホルダー

- 制限事項

第2章 調査手法または前提

- 調査プロセス

- 調査手法

- 回答者プロファイル

第3章 市場要約

第4章 エグゼクティブサマリー

第5章 世界の電動建設機械市場新型コロナウイルス感染症(COVID-19)の影響

第6章 世界の電動建設機械市場収益 、2020~2030年

第7章 機器タイプ別の市場洞察

- 電動ショベル

- 電動アースムーバー

- 電動ホイールローダー

- 電動アスファルト装置

- その他(電動ダンプトラック、電動ロードホールダンプ、電動ブルドーザー、グレーダー)

第8章 バッテリー出力別の市場洞察

- 50HP未満

- 50~150HP

- 151~300HP

- 300HP以上

第9章 バッテリータイプ別の市場洞察

- リチウムイオン

- 鉛酸

- その他

第10章 用途別の市場洞察

- 建設

- 鉱業

- 産業用

- 農業

第11章 地域別の市場洞察

- 北米の電動建設機械市場

- 米国

- カナダ

- その他の北米地域

- 欧州の電動建設機械市場

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州地域

- アジア太平洋の電動建設機械市場

- 中国

- インド

- 日本

- 韓国

- アジア太平洋のその他諸国

- その他地域の電動建設機械市場

第12章 世界の電動建設機械市場ダイナミクス

- 市場促進要因

- 市場の課題

- 影響分析

第13章 世界の電動建設機械市場機会

第14章 世界の電動建設機械市場動向

第15章 需要側と供給側の分析

- 需要側分析

- 供給側分析

第16章 サプライチェーン分析

第17章 バリューチェーン分析

第18章 競合シナリオ

- 競合ベンチマーキング

- ポーターのファイブフォース分析

第19章 紹介された企業

- Caterpillar Inc

- Hitachi Construction Machinery

- Komatsu Ltd

- XCMG

- CNH Industrial NV

- JCB

- Sany Heavy Industry Co Ltd

- Hyundai CE

- Liebherr-International AG

- Volvo CE

第20章 免責事項

The electric construction equipment market is rapidly gaining traction as a cleaner, quieter, and more environmentally friendly alternative to traditional diesel-powered machinery. With lower operating costs, reduced emissions, and advancements in battery technology, electric construction equipment is finding applications in various sectors. Despite initial challenges, such as higher purchase costs and charging infrastructure, the market's growth is being fueled by increasing environmental concerns and regulatory pressures, making it a significant and evolving segment within the construction industry

The electric forklift Market is expected to grow at a strong CAGR of 14.72% during the forecast period. The global construction industry has witnessed a significant surge in the adoption of electric construction equipment, driven by the dual goals of reducing emissions and improving operational efficiency. This transition is evident in major construction markets, with substantial investments in USD flowing into this sector. For instance, in 2022, the United States allocated over $200 million for research and development of electric construction machinery, aiming to spur innovation and create a more sustainable industry. Similarly, industry giants have made substantial commitments to electrify their fleets, such as a renowned construction firm's $1 billion investment in 2021 to replace diesel-powered machinery with electric alternatives. These instances underscore the accelerating shift towards electric construction equipment, with tangible financial backing, highlighting a greener and more technologically advanced future for the industry.

Based on equipment type, the market is segmented into electric excavators, electric earth mover, electric wheel loader, electric asphalt equipment and others. Among these, electric excavators segment is having a high market share in 2022. Electric excavators significantly lower operational costs over their lifespan, as they require less maintenance and utilize cheaper electricity compared to traditional fuel-powered excavators. This compelling cost-effectiveness has driven widespread adoption, with construction companies recognizing the long-term financial advantages.

Based on Battery Output, the market is segmented into less than 50 HP, 50-150HP, 151-300HP and above 300. Among these, 151-300 HP segment is having a high market share in 2022. This horsepower range caters to a wide array of construction tasks, from medium-sized projects to heavy-duty applications. Construction companies value the balanced performance of these machines, enabling them to tackle a broad spectrum of work without compromising on efficiency or capacity. This adaptability translates into increased productivity, making the 151-300 HP equipment segment a staple in the construction industry.

Based on battery type, the market is segmented into lithium ion, lead acid and others. Among these, the lithium-ion segment is having a high market share in 2022. The dominance of lithium-ion batteries in the construction equipment market stems from their unparalleled energy density, longevity, and fast charging capabilities. These batteries provide a substantial advantage by extending the operating hours of electric construction machinery, reducing downtime, and boosting productivity.

Based on application, the market is segmented into construction, mining, industrial, agriculture. Among these, the construction segment is having a high market share in 2022. The inherent need for construction drives the high market share in this segment. Infrastructure development, urbanization, and maintenance projects persistently require a vast array of machinery and equipment. As the industry evolves, so does its demand for more efficient, environmentally friendly solutions. With growing awareness of environmental impact, the construction sector seeks alternatives that minimize pollution and energy consumption.

For a better understanding of the market adoption of the Industrial Relay industry, the market is analyzed based on its worldwide presence in the countries such as North America (U.S., Canada, and the Rest of North America), Europe (Germany, UK, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Korea, and Rest of Asia-Pacific), Rest of World. The Asia-Pacific region is witnessing a remarkable surge in the adoption of electric construction equipment, fueled by a blend of environmental concerns, rapid urbanization, and technological advancements. For instance, SANY, a prominent Chinese construction equipment manufacturer, introduced its all-electric compact excavator in 2020, with an investment exceeding $50 million in research, development, and production facilities. This move highlights the region's dedication to electric innovation and signifies the growing acceptance of electric equipment in Asia-Pacific markets. Furthermore, Japanese construction giant Obayashi Corporation made a significant investment, estimated at around 16.5 million, to acquire a fleet of electric construction machinery in 2021.

Some of the major players operating in the market include: Caterpillar Inc, Hitachi Construction Machinery, Komatsu Ltd, XCMG, CNH Industrial NV, JCB, Sany Heavy Industry Co Ltd, Hyundai CE., Liebherr-International AG, Volvo CE.

TABLE OF CONTENTS

1 MARKET INTRODUCTION

- 1.1. Market Definitions

- 1.2. Main Objective

- 1.3. Stakeholders

- 1.4. Limitation

2 RESEARCH METHODOLOGY OR ASSUMPTION

- 2.1. Research Process of the Global Electric Construction Equipment Market

- 2.2. Research Methodology of the Global Electric Construction Equipment Market

- 2.3. Respondent Profile

3 MARKET SYNOPSIS

4 EXECUTIVE SUMMARY

5 GLOBAL ELECTRIC CONSTRUCTION EQUIPMENT MARKET COVID-19 IMPACT

6 GLOBAL ELECTRIC CONSTRUCTION EQUIPMENT MARKET REVENUE, 2020-2030F

7 MARKET INSIGHTS BY EQUIPMENT TYPE

- 7.1. Electric Excavator

- 7.2. Electric Earth mover

- 7.3. Electric Wheel loader

- 7.4. Electric Asphalt Equipment

- 7.5. Others (Electric Dump Truck, Electric laud haul dump, Electric Dozers, Graders)

8 MARKET INSIGHTS BY BATTERY OUTPUT

- 8.1. Less than 50 HP

- 8.2. 50-150 HP

- 8.3. 151-300 HP

- 8.4. Above 300 HP

9 MARKET INSIGHTS BY BATTERY TYPE

- 9.1. Lithium-ion

- 9.2. Lead-acid

- 9.3. Others

10 MARKET INSIGHTS BY APPLICATION

- 10.1. Construction

- 10.2. Mining

- 10.3. Industrial

- 10.4. Agriculture

11 MARKET INSIGHTS BY REGION

- 11.1. North America Electric Construction Equipment Market

- 11.1.1. U.S.

- 11.1.2. Canada

- 11.1.3. Rest of North America

- 11.2. Europe Electric Construction Equipment Market

- 11.2.1. Germany

- 11.2.2. UK

- 11.2.3. France

- 11.2.4. Italy

- 11.2.5. Spain

- 11.2.6. Rest of Europe

- 11.3. Asia-Pacific Electric Construction Equipment Market

- 11.3.1. China

- 11.3.2. India

- 11.3.3. Japan

- 11.3.4. South Korea

- 11.3.5. Rest of APAC

- 11.4. Rest Of the World Electric Construction Equipment Market

12 GLOBAL ELECTRIC CONSTRUCTION EQUIPMENT MARKET DYNAMICS

- 12.1. Market Drivers

- 12.2. Market Challenges

- 12.3. Impact Analysis

13 GLOBAL ELECTRIC CONSTRUCTION EQUIPMENT MARKET OPPORTUNITIES

14 GLOBAL ELECTRIC CONSTRUCTION EQUIPMENT MARKET TRENDS

15 DEMAND AND SUPPLY-SIDE ANALYSIS

- 15.1. Demand Side Analysis

- 15.2. Supply Side Analysis

16 SUPPLY CHAIN ANALYSIS

17 VALUE CHAIN ANALYSIS

18 COMPETITIVE SCENARIO

- 18.1. Competitive Benchmarking

- 18.1.1. Porters Fiver Forces Analysis

19 COMPANIES PROFILED

- 19.1. Caterpillar Inc

- 19.2. Hitachi Construction Machinery

- 19.3. Komatsu Ltd

- 19.4. XCMG

- 19.5. CNH Industrial NV

- 19.6. JCB

- 19.7. Sany Heavy Industry Co Ltd

- 19.8. Hyundai CE

- 19.9. Liebherr-International AG

- 19.10. Volvo CE