|

市場調査レポート

商品コード

1833668

電動建設機械の市場機会、成長促進要因、産業動向分析と2025年~2034年予測Electric Construction Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 電動建設機械の市場機会、成長促進要因、産業動向分析と2025年~2034年予測 |

|

出版日: 2025年09月03日

発行: Global Market Insights Inc.

ページ情報: 英文 230 Pages

納期: 2~3営業日

|

概要

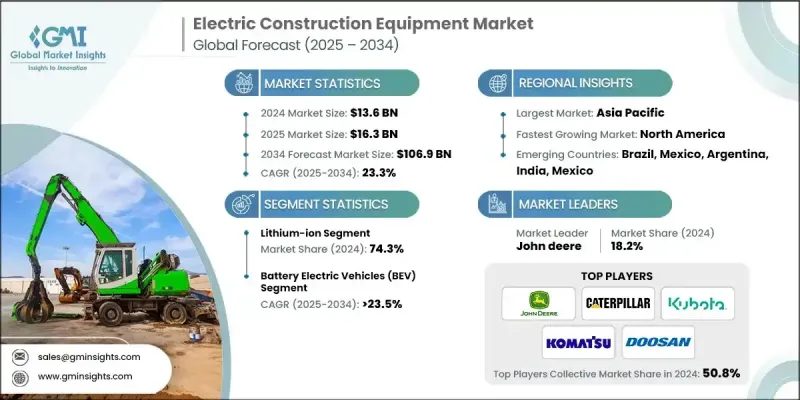

Global Market Insights Inc.が発行した最新レポートによると、世界の電動建設機械市場は2024年に136億米ドルと推定され、CAGR 23.3%で2025年の163億米ドルから2034年には1,069億米ドルに成長すると予測されています。

欧州、北米、アジアの一部の政府は、建設機械を含む非道路移動機械に対する排ガス規制をますます強化しています。これらの規制は、窒素酸化物(NOx)、粒子状物質(PM)、二酸化炭素(CO2)といった有害な汚染物質を抑制することを目的としており、大気汚染や気候変動の主な原因となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 136億米ドル |

| 予測金額 | 1,069億米ドル |

| CAGR | 23.3% |

リチウムイオンの採用増加

リチウムイオン電池は、エネルギー密度が高く、ライフサイクルが長く、急速充電が可能であることから、2024年に大きなシェアを占めました。企業がリチウムイオン技術を重視するのは、厳しい建設作業に必要な信頼性の高い電力を供給すると同時に、機器全体の重量を軽減できるからです。技術革新と規模の経済によってバッテリーのコストが下がり続けているため、リチウムイオンバッテリーはメーカーとエンドユーザーの両方にとって好ましい選択肢になりつつあります。

バッテリー電気自動車の需要増加

バッテリー電気自動車(BEV)は、ゼロ・エミッション・ソリューションに向けた世界的な後押しを受けて、2025年から2034年にかけて大幅な成長を遂げます。これらの車両は、騒音公害を最小限に抑え、テールパイプ排出をなくすという2つの利点を備えており、都市部や屋内の建設現場に理想的です。BEVを開発する企業は、稼働時間を延ばし、充電停止時間を減らすために、バッテリー技術の進歩を優先しています。

アジア太平洋地域が有望な地域となる

アジア太平洋電動建設機械市場は、急速な都市化、インフラ開拓、クリーンエネルギー導入を促進する政府の支援政策に牽引され、2024年には大きなシェアを占める。中国、日本、韓国などの国々が、研究開発と電気自動車の配備に多額の投資を行い、主導権を握っています。この地域の建設産業の拡大と環境意識の高まりが相まって、性能と持続可能性の両方の基準を満たす電気機械の需要が加速しています。

電動建設機械業界で事業を展開している主な企業は、Liebherr、Kubota、Doosan Infracore、Mecalac、John Deere、LiuGong Machinery、Caterpillar、Komatsu、Manitou、Hitachi Constructionです。

進化する電動建設機械市場で足場を固め、強化するために、企業は多面的な戦略を採用しています。製品革新は依然として中核的な焦点であり、より長持ちするバッテリー、改良されたエネルギー管理システム、さまざまな機器カテゴリーをカバーする多用途の電動モデルの開発に投資が注がれています。バッテリーメーカーやテクノロジー企業との戦略的提携や合弁事業は、企業がイノベーションを加速し、市場投入までの時間を短縮するのに役立ちます。さらに、アフターセールス・サービス・ネットワークを拡大し、顧客教育イニシアティブに投資することは、信頼を築き、ディーゼルから電気機械への移行を容易にするために不可欠です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 原材料サプライヤー

- 部品メーカー

- 機器メーカー

- 販売代理店およびディーラー

- アフターマーケットサプライヤー

- 業界への影響要因

- 促進要因

- 厳しい排出規制

- 都市化とスマートシティプロジェクト

- コスト削減と効率化

- OEMとレンタルの採用

- 業界の潜在的リスク&課題

- 初期費用が高め

- 充電インフラのギャップ

- 市場機会

- 政府のインセンティブと補助金

- バッテリー技術の進歩

- スマートな現場統合

- グリーンインフラプロジェクト

- 促進要因

- 成長可能性分析

- 特許分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 技術統合と標準化の課題

- 充電インフラの互換性と標準

- コネクタ標準と相互運用性の問題

- 通信プロトコルとデータ交換

- メーカー間の互換性の課題

- レガシーシステムの統合と移行コスト

- フリート管理システムの統合

- 複数ブランドのフリート管理の複雑さ

- データ統合および分析プラットフォーム

- テレマティクスおよび遠隔監視システム

- メンテナンスのスケジュールと最適化

- デジタルトランスフォーメーションとIoT統合

- 接続規格とプロトコル

- 3データセキュリティとプライバシーの要件

- エッジコンピューティングとリアルタイム分析

- デジタルツイン技術とシミュレーション

- 複数ベンダーの統合の複雑さ

- ブランド間の充電コネクタの互換性の問題

- フリート管理システム統合の課題(15以上のプラットフォーム)

- データ形式の標準化と相互運用性のギャップ

- サービス診断ツールの要件とトレーニング

- 充電インフラの互換性と標準

- 3エネルギー管理とグリッド統合

- スマート充電および負荷管理システム

- 動的負荷分散とピークシェービング

- 時間帯別最適化とコスト削減

- グリッド安定性と需要応答の統合

- AIと機械学習のアプリケーション

- 再生可能エネルギーの統合

- 太陽光と風力発電の統合によるメリット

- エネルギー貯蔵およびバッテリーシステム

- マイクログリッド開発とアイランド化機能

- カーボンフットプリントの削減と持続可能性

- 車両から電力網への(V2G)と双方向充電

- グリッドサービスと収益機会

- 技術要件と標準

- ビジネスモデルの開発と実装

- 規制枠組みと市場障壁

- スマート充電および負荷管理システム

- サービスネットワーク準備状況評価

- 地理的サービスカバレッジ分析

- サービスカバレッジギャップの特定(40%の市場がサービス不足)

- 地域サービス密度と応答時間分析

- 農村部と都市部のサービス利用可能性の格差

- 緊急サービス対応能力

- 技術者認定およびトレーニングインフラストラクチャ

- 高電圧認証プログラムの可用性

- トレーニング能力とボトルネック分析

- スキル開発のタイムラインと要件

- 認証コストと投資分析

- 診断機器およびツールの要件

- 特殊診断ツールへの投資

- ソフトウェアプラットフォームの統合と更新

- 複数ブランドの互換性と標準化

- 技術のアップグレードと陳腐化管理

- 地理的サービスカバレッジ分析

- 部品の入手可能性とサプライチェーンのサポート

- 電気部品サプライチェーンの成熟度

- バッテリー交換とサービスインフラ

- 緊急部品の入手可能性とリードタイム

- 地域サプライチェーンの開発とローカリゼーション

- サービスモデルの革新とデジタル統合

- リモート診断と予測メンテナンス

- 拡張現実とデジタルサービスツール

- サービス・アズ・ア・サービス(SaaS)モデルとサブスクリプション

- 顧客セルフサービスとデジタルプラットフォーム

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

- ユースケース

- 最良のシナリオ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:装備別、2021-2034

- 主要動向

- 掘削機

- ローダー

- ブルドーザー

- クレーン

- ダンプトラック

- ローラー

- その他

第6章 市場推計・予測:バッテリー容量別、2021-2034

- 主要動向

- 50kWh未満

- 50kWh~200kWh

- 200kWh以上

第7章 市場推計・予測:バッテリーテクノロジー, 2021-2034

- 主要動向

- 鉛蓄電池

- リチウムイオン

- ニッケル水素

第8章 市場推計・予測:電源別、2021-2034

- 主要動向

- バッテリー電気自動車(BEV)

- プラグインハイブリッド電気自動車(PHEV)

第9章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 建設

- 鉱業

- マテリアルハンドリング

- 農業

- その他

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- グローバルプレーヤー

- Caterpillar

- CNH Industrial

- Hitachi Construction Machinery

- JCB

- John Deere

- Komatsu

- Komatsu

- Liebherr

- 地域プレーヤー

- Develon

- Doosan Infracore

- Hyundai Construction Equipment

- LiuGong Machinery

- Manitou

- Mecalac

- SDLG

- 新興プレーヤー

- Avant Tecno

- Elematic

- Kramer-Werke

- Sunward Intelligent Equipment

- Zoomlion Heavy Industry Science &Technology