|

|

市場調査レポート

商品コード

1377257

大容量変圧器市場- 世界の産業規模、シェア、動向、機会、予測Large Power Transformer Market - Global Industry Size, Share, Trends, Opportunity, and Forecast Segmented By Power Rating, By Cooling Type, By Insulation, By Cooling Type, By Region, Competition, 2018-2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 大容量変圧器市場- 世界の産業規模、シェア、動向、機会、予測 |

|

出版日: 2023年10月03日

発行: TechSci Research

ページ情報: 英文 182 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

大容量変圧器の世界市場規模は2022年に198億2,000万米ドルとなり、予測期間のCAGRは5.86%と堅調な成長が見込まれます。

電力市場は、需要の増加、送電網のアップグレードやスマートグリッドの必要性、再生可能エネルギーや非従来型エネルギー資源のシェア拡大といった要因によって牽引されています。さらに、厳しい政府規制、変電器の高コスト、技術的障壁も市場に影響を与えています。電力変圧器の価格が高いことが成長を妨げているもの、これらの要因が総合的に成長機会を生み出しています。

主な市場促進要因

世界の電力需要の増加

| 市場概要 | |

|---|---|

| 予測期間 | 2024-2028 |

| 2022年の市場規模 | 198億2,000万米ドル |

| 2028年の市場規模 | 281億4,000万米ドル |

| CAGR 2023-2028 | 5.86% |

| 急成長セグメント | 中電力定格 |

| 最大市場 | アジア太平洋 |

世界市場はここ数十年で大幅な経済成長と都市化が進み、電力需要の大幅な急増につながっています。このような電力消費の増加は、人口の拡大、工業化、生活水準の向上など、さまざまな要因によってもたらされています。農村部から都市部への移住者が増えるにつれ、信頼性が高く効率的な電力インフラが最も必要とされるようになります。

目次

第1章 概要

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 顧客の声

第5章 大容量変圧器の世界市場展望

- 市場規模・予測

- 金額別

- 市場シェアと予測

- 定格電力別(小型、中型、大型)

- 冷却タイプ別(空冷式、油冷式)

- 断熱材別(乾式、液浸式)

- 用途別(商業・住宅、ユーティリティ、産業用)

- 地域別

- 企業別(2022年)

- 市場マップ

第6章 北米の大容量変圧器市場展望

- 市場規模・予測

- 金額別

- 市場シェアと予測

- 電力定格別

- 冷却タイプ別

- 断熱材別

- 用途別

- 国別

- 北米国別分析

- 米国

- カナダ

- メキシコ

第7章 アジア太平洋大容量変圧器市場展望

- 市場規模・予測

- 金額別

- 市場シェアと予測

- 電力定格別

- 冷却タイプ別

- 断熱材別

- 用途別

- 国別

- アジア太平洋地域国別分析

- 中国

- インド

- 日本

- 韓国

- インドネシア

第8章 欧州大容量変圧器市場展望

- 市場規模と予測

- 金額別

- 市場シェアと予測

- 電力定格別

- 冷却タイプ別

- 断熱材別

- 用途別

- 国別

- 欧州国別分析

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

第9章 南米の大容量変圧器市場展望

- 市場規模・予測

- 金額別

- 市場シェアと予測

- 電力定格別

- 冷却タイプ別

- 断熱材別

- 用途別

- 国別

- 南米:国別分析

- ブラジル

- アルゼンチン

第10章 中東・アフリカの大容量変圧器市場展望

- 市場規模と予測

- 金額別

- 市場シェアと予測

- 電力定格別

- 冷却タイプ別

- 断熱材別

- 用途別

- 国別

- 中東・アフリカ:国別分析

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- イスラエル

- エジプト

第11章 市場力学

- 促進要因

- 課題

第12章 市場動向と発展

第13章 企業プロファイル

- Hitachi Energy Ltd

- CG Power and Industrial Solutions Limited

- General Electric Company

- Hyosung Power & Industrial Systems Performance Group

- Hyundai Heavy Industries Co. Ltd

- Mitsubishi Electric Corporation

- SGB-SMIT International GmbH

- Siemens Energy AG

- SPX Corporation

第14章 戦略的提言

Global Large Power Transformer market has valued at USD 19.82 Billion in 2022 and is anticipated to project robust growth in the forecast period with a CAGR of 5.86%. The market for electricity is driven by factors such as increased demand, the need for upgraded transmission networks and smart grids, and the growing share of renewable and non-conventional energy resources. Additionally, strict government regulations, high costs of power transformers, and technological barriers also influence the market. These factors collectively create growth opportunities, although the high price of power transformers hinders growth.

Key Market Drivers

Increasing Demand for Electricity in Global

| Market Overview | |

|---|---|

| Forecast Period | 2024-2028 |

| Market Size 2022 | USD 19.82 Billion |

| Market Size 2028 | USD 28.14 billion |

| CAGR 2023-2028 | 5.86% |

| Fastest Growing Segment | Medium Power Rating |

| Largest Market | Asia-Pacific |

The Global market has witnessed substantial economic growth and urbanization in recent decades, leading to a significant surge in electricity demand. This upswing in power consumption is driven by various factors, including population expansion, industrialization, and improving living standards. As more individuals migrate from rural to urban areas, the necessity for dependable and efficient electrical infrastructure becomes paramount.

One of the primary drivers for the Global power transformer market is the increasing need to upgrade and expand the existing power infrastructure to meet the escalating electricity demand. Power transformers play a critical role in efficiently transmitting and distributing electricity from power generation sources to end-users. Utilities and governments across the region are making substantial investments in grid expansion and modernization projects to ensure a stable and uninterrupted power supply.

Moreover, power transformers are vital for integrating renewable energy sources into the grid, in addition to meeting the augmented electricity demand. Numerous countries in the Global region are embracing renewable energy technologies such as wind and solar power to reduce their carbon footprint and achieve environmental targets. Power transformers are indispensable for connecting these intermittent renewable sources to the grid and ensuring a seamless and reliable power supply.

Furthermore, electrification of various sectors including transportation and heating is gaining momentum in the region. Electric vehicles (EVs) and electric heating systems are becoming increasingly popular, further driving up electricity consumption. To support this electrification trend, investments in power transformers are imperative to handle the increased load and maintain grid stability.

In conclusion, the escalating electricity demand in the Global region, propelled by population growth, urbanization, and the adoption of electrification and renewable energy, serves as a significant driver for the power transformer market. The requirement for reliable and efficient power transmission and distribution infrastructure is compelling governments and utilities to invest in power transformers.

Grid Modernization Initiatives

The Global power transformer market is currently witnessing substantial growth due to the ongoing grid modernization initiatives undertaken by governments and utilities across the region. Grid modernization entails the integration of advanced technologies and equipment to enhance the efficiency, reliability, and resilience of the electrical grid. Power transformers play a pivotal role in these initiatives and serve as essential components of modernized power systems.

A key driving factor for the power transformer market in Global is the imperative to upgrade aging infrastructure. Many countries in the region are burdened with outdated power transmission and distribution networks that are susceptible to outages and inefficiencies. To address these challenges, governments and utilities are investing in the replacement of old transformers with newer, more efficient models capable of handling higher voltage levels and offering improved grid management capabilities.

Furthermore, the adoption of smart grid technologies is gaining momentum in Global. Smart grids rely on advanced sensors, communication networks, and data analytics to optimize the flow of electricity, reduce losses, and enhance grid resilience. Power transformers equipped with monitoring and control capabilities are critical components of smart grids, enabling real-time monitoring and remote operation. This trend is fueling the demand for intelligent power transformers in the region.

Another significant driver for the power transformer market is the integration of renewable energy sources. Many countries in Global are actively pursuing renewable energy targets to reduce carbon emissions and combat climate change. Wind and solar power generation, which can be intermittent, require sophisticated grid infrastructure and power transformers to ensure seamless integration into the existing grid. Consequently, there is a growing need for power transformers that can handle variable and distributed energy sources.

In conclusion, the ongoing grid modernization initiatives in Global, driven by the necessity for infrastructure upgrades, the adoption of smart grid technologies, and the integration of renewable energy sources, serve as significant drivers for the power transformer market. These initiatives are essential for ensuring a reliable and resilient electrical grid in the face of increasing electricity demand and environmental concerns.

Rapid Industrialization and Urbanization

The Global region is currently witnessing rapid industrialization and urbanization, which serves as a significant catalyst for the power transformer market in the area. As countries in the region continue to develop and expand their industrial and urban sectors, the demand for electrical power for various applications, including manufacturing, commercial buildings, and infrastructure development, is experiencing a remarkable surge.

One of the primary drivers behind this growth is the expansion of the manufacturing sector. Several Asian countries have emerged as manufacturing hubs for diverse industries, such as automotive, electronics, and textiles. These industries rely heavily on a consistent and reliable power supply to ensure efficient operations. Power transformers play a critical role in stepping up or stepping down voltage levels, thereby ensuring a stable and uninterrupted electricity supply to industrial facilities.

Furthermore, the rapid urbanization in the Global region has led to the construction of numerous commercial and residential buildings. This increased construction activity has resulted in a higher demand for electrical power to support lighting, heating, cooling, and other electrical systems within these structures. Power transformers are indispensable for distributing electricity from the grid to these urban areas and effectively managing the load.

Moreover, the ongoing infrastructure development projects, such as airports, railways, and ports, also contribute to the growing demand for power transformers. These projects require substantial electrical infrastructure to power various systems and equipment, and power transformers are pivotal components in meeting these energy requirements.

Additionally, the electrification of public transportation systems, including the expansion of metro rail networks and the adoption of electric buses, is gaining momentum in many Asian cities. Power transformers are essential for powering and ensuring the reliability and efficiency of these transportation systems.

To summarize, the power transformer market in the Global region is being propelled by the rapid industrialization and urbanization taking place. The increasing demand for electricity in the manufacturing, commercial, and infrastructure sectors, along with the electrification of public transportation, is creating a robust market for power transformers in the region. As Asian economies continue to grow, the need for dependable and efficient electrical infrastructure will undoubtedly remain a driving force in the power transformer market.

Key Market Challenges

Aging Infrastructure

One of the key challenges confronting the Global power transformer market is the aging infrastructure of existing transformers and the associated costs of replacement. Numerous countries in the region are operating power transformers that have been in service for several decades, nearing the end of their operational life. As transformers age, their efficiency declines and failure rates increase, resulting in power outages and disruptions.

This challenge presents a dual aspect. Firstly, there is a necessity for comprehensive assessment and inspection of the existing transformer fleet to identify those requiring replacement. This process can be both time-consuming and costly. Secondly, the financial burden of replacing outdated transformers with modern, efficient models poses a significant challenge for utilities and governments. Power transformers are costly assets, and their replacement necessitates substantial capital investment.

Moreover, in certain instances, transformer replacement may also entail upgrades to other components of the electrical grid to accommodate the new equipment, thereby adding to the overall project cost. Striking a balance between the need for replacement and budgetary constraints presents a complex challenge that must be addressed by the Global power transformer market.

Addressing this challenge may include implementing proactive maintenance strategies to extend the lifespan of transformers, exploring financing options for replacement projects, and prioritizing replacements based on criticality and efficiency gains. It also requires collaboration among governments, utilities, and manufacturers to identify cost-effective solutions for transformer replacement.

Environmental Concerns

The Global power transformer market encounters challenges associated with regulatory compliance and environmental considerations. Governments in the region are increasingly prioritizing energy efficiency, environmental sustainability, and safety standards for electrical infrastructure, specifically power transformers.

One of the primary challenges is staying abreast of evolving regulations and standards. Different countries in Global may have diverse regulatory requirements for power transformers, encompassing energy efficiency standards, safety codes, and environmental compliance regulations. Manufacturers must allocate resources to research and development to design and manufacture transformers that meet these varying regulatory demands, which can be intricate and costly.

Environmental concerns also play a substantial role. Power transformers contain insulating oils, which can pose environmental risks if not managed properly. Many countries are imposing stricter regulations on the use, disposal, and recycling of transformer oils to minimize their environmental impact. Manufacturers and utilities must adapt to these regulations by utilizing environmentally friendly insulating materials and implementing effective waste management practices.

Another challenge lies in the necessity to reduce greenhouse gas emissions associated with power transformers. Certain older transformers employ insulating oils that contain high levels of potent greenhouse gases, such as sulfur hexafluoride (SF6). SF6 is a significant contributor to global warming, and there is mounting pressure to phase out its utilization. Effectively transitioning to alternative insulating materials and designs that minimize greenhouse gas emissions entails technical and regulatory hurdles.

To overcome these challenges, the power transformer industry in Global must invest in research and development endeavors to create more environmentally friendly and energy-efficient transformers. Collaborating with regulatory authorities to establish clear and standardized guidelines can also facilitate streamlined compliance efforts.

Supply Chain Disruptions and Raw Material Costs

The Global power transformer market is confronted with challenges related to disruptions in the supply chain and fluctuating costs of raw materials. With the increasing interconnectedness of the global supply chain, any disturbances in one part of the world can have far-reaching impacts on industries across the Global region.

One notable challenge pertains to the availability and cost of crucial raw materials used in transformer manufacturing. Copper, aluminum, steel, and various insulating materials are essential components of transformers. The prices of these raw materials can be volatile due to factors such as global demand, trade tensions, and interruptions in supply. Sudden increases in raw material costs can significantly affect the production expenses of transformers, potentially leading to higher prices for customers.

Supply chain disruptions, whether caused by natural disasters, political instability, or global health crises like the COVID-19 pandemic, can impede the timely delivery of transformer components and finished products. Delays in production and delivery can impact project timelines and the ability to meet customer demand, resulting in financial losses and customer dissatisfaction.

To address these challenges, companies operating in the Global power transformer market must diversify their supply chains, strategically source raw materials, and implement risk mitigation strategies. Collaboration with suppliers to ensure a stable and secure supply chain is of utmost importance. Furthermore, investment in research and development to explore alternative materials or manufacturing processes that reduce reliance on volatile raw materials can help mitigate cost fluctuations.

In conclusion, the Global power transformer market faces significant challenges including aging infrastructure and replacement costs, regulatory and environmental compliance, as well as supply chain disruptions and raw material costs. Addressing these challenges necessitates collaboration, innovation, and adaptability to meet the growing demand for reliable and efficient electrical infrastructure in the region.

Key Market Trends

Integration of Smart Technologies in Power Transformers

The Global power transformer market is witnessing a notable trend in the integration of smart technologies into transformer design and operation. Smart transformers, also known as intelligent or digital transformers, are equipped with advanced sensors, communication capabilities, and data analytics tools that facilitate real-time monitoring, control, and optimization of transformer performance.

One of the driving factors behind this trend is the increasing necessity for grid modernization. Numerous countries in the Global region are investing in upgrading their electrical grids to enhance efficiency, reliability, and resilience. Smart transformers play a pivotal role in this modernization process by providing utilities with real-time insights into transformer condition, load management, and fault detection. These capabilities enhance grid stability, reducing downtime and ultimately benefiting consumers.

Another crucial driver for the adoption of smart transformers is the integration of renewable energy sources. The Global region has been rapidly expanding its renewable energy capacity, encompassing solar and wind power. Smart transformers effectively manage the intermittent nature of renewable energy sources by adjusting voltage levels and ensuring seamless integration into the grid. This trend aligns with the region's commitment to reducing carbon emissions and achieving sustainable energy goals.

Additionally, the rise of electric vehicles (EVs) in Global is influencing the adoption of smart transformers. EV charging infrastructure requires transformers capable of handling variable loads and providing real-time data on energy consumption. Smart transformers enable grid operators to effectively monitor and manage EV charging stations, ensuring reliable power supply to meet the growing demand for electric transportation.

In conclusion, the integration of smart technologies into power transformers is a prominent trend in the Global market. This trend addresses the imperative for grid modernization, the integration of renewable energy sources, and the growth of electric mobility, all of which are integral components of the region's evolving energy landscape.

Eco-Friendly and Energy-Efficient Transformer Designs

Another notable trend in the Global power transformer market is the increasing focus on environmentally friendly and energy-efficient transformer designs. The industry is driven by environmental concerns and sustainability objectives, pushing for the development of transformers that minimize energy losses, reduce greenhouse gas emissions, and utilize eco-friendly materials.

A key driver of this trend is the need to reduce the environmental impact of transformer insulating oils. Traditionally, transformers have relied on oils containing sulfur hexafluoride (SF6), a potent greenhouse gas. However, there is mounting pressure to phase out SF6 due to its high global warming potential. Manufacturers in the Global region are actively exploring alternative insulating materials and designs that have a lower environmental impact, such as biodegradable oils and dry-type transformers.

Energy efficiency is also a crucial aspect of this trend. Power transformers play a vital role in electrical grids, and any improvement in their energy efficiency can result in significant energy savings. Utilities and governments in Global are implementing more stringent energy efficiency standards, prompting manufacturers to develop transformers with reduced core and copper losses. These high-efficiency transformers minimize energy wastage and operating costs for end-users.

Moreover, transformer designs are evolving to accommodate distributed energy resources (DERs) and microgrids. As Global countries embrace DERs like rooftop solar panels and small-scale wind turbines, transformers are being developed with the capability to manage bidirectional power flows. This allows excess energy to be fed back into the grid or distributed locally within microgrids.

In summary, the Global power transformer market is experiencing a shift towards environmentally friendly and energy-efficient designs to meet regulatory requirements and fulfill the region's commitment to sustainability and energy conservation.

Segmental Insights

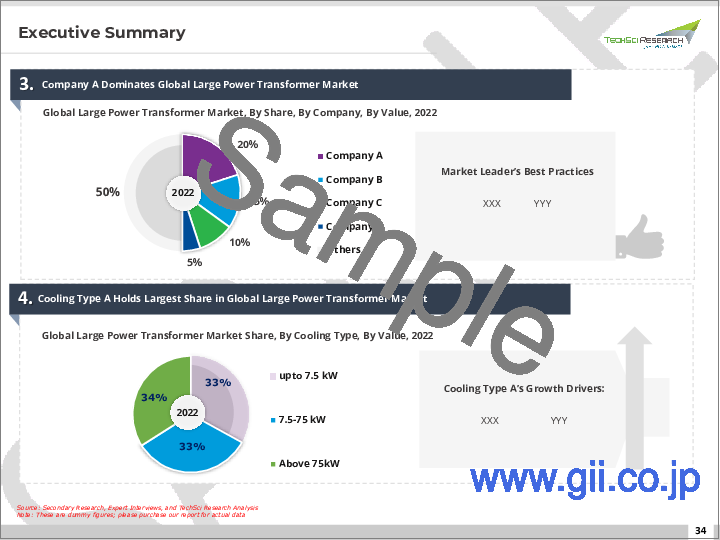

Cabla Type Insights

The Air-Cooled segment holds a significant market share in the Global Power Transformers Market. The adoption of smart grid technologies and intelligent transformers is exerting influence on the air-cooled transformer segment. These transformers are equipped with sensors and monitoring systems that facilitate real-time data collection and remote operation. This trend is primarily driven by the imperative for efficient grid management and fault detection, particularly in areas prone to extreme weather conditions.

The adoption of air-cooled transformers may vary across countries in the Global region. In countries abundant in water resources, liquid-immersed transformers may still dominate the market. However, in arid regions or areas susceptible to flooding, air-cooled transformers offer a reliable alternative. Geographical factors, climate conditions, and regulatory requirements can exert influence on market dynamics within specific countries.

Regional Insights

Asia Pacific has established itself as the leader in the Global Large Power Transformer Market with a significant revenue share in 2022.

This Asia-Pacific dominated the large power transformer market in 2021. It is expected to continue its dominance in the coming years. The region saw an unprecedented increase in the demand for large power transformers during the past few years, which is expected to increase further during the forecast period.

Industries such as automotive, chemical, fertilizers, and petrochemical are witnessing steady growth in the region, leading to an increase in electricity demand. This factor is expected to offer tremendous growth opportunities for the market players in the region.

Key Market Players

Hitachi Energy Ltd

CG Power and Industrial Solutions Limited

General Electric Company

Hyosung Power & Industrial Systems Performance Group

Hyundai Heavy Industries Co. Ltd

Mitsubishi Electric Corporation

SGB-SMIT International GmbH

Siemens Energy AG

SPX Corporation

Toshiba Energy Systems & Solutions Corporation

Report Scope:

In this report, the Global Large Power Transformer Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

Global Power Transformers Market, By Power Rating:

- Small

- Medium

- Large

Global Power Transformers Market, By Cooling Type:

- Air-Cooled

- Oil-Cooled

Global Power Transformers Market, By Insulation:

- Dry

- Liquid Immersed

Global Power Transformers Market, By Application:

- Commercial & Residential

- Utility

- Industrial

Large Power Transformer Market, By Region:

- North America

- United States

- Canada

- Mexico

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Indonesia

- Europe

- Germany

- United Kingdom

- France

- Russia

- Spain

- South America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

- Egypt

- UAE

- Israel

Competitive Landscape

- Company Profiles: Detailed analysis of the major companies present in the Global Large Power Transformer Market.

Available Customizations:

- Global Large Power Transformer Market report with the given market data, Tech Sci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Table of Contents

1. Product Overview

- 1.1. Market Definition

- 1.2. Scope of the Market

- 1.3. Markets Covered

- 1.4. Years Considered for Study

- 1.5. Key Market Segmentations

2. Research Methodology

- 2.1. Objective of the Study

- 2.2. Baseline Methodology

- 2.3. Key Industry Partners

- 2.4. Major Association and Secondary Sources

- 2.5. Forecasting Methodology

- 2.6. Data Triangulation & Validation

- 2.7. Assumptions and Limitations

3. Executive Summary

4. Voice of Customers

5. Global Large Power Transformer Market Outlook

- 5.1. Market Size & Forecast

- 5.1.1. By Value

- 5.2. Market Share & Forecast

- 5.2.1. By Power Rating (Small, Medium and Large)

- 5.2.2. By Cooling Type (Air-Cooled and Oil-Cooled)

- 5.2.3. By Insulation (Dry and Liquid Immersed)

- 5.2.4. By Application (Commercial & Residential, Utility, Industrial)

- 5.2.5. By Region

- 5.3. By Company (2022)

- 5.4. Market Map

6. North America Large Power Transformer Market Outlook

- 6.1. Market Size & Forecast

- 6.1.1. By Value

- 6.2. Market Share & Forecast

- 6.2.1. By Power Rating

- 6.2.2. By Cooling Type

- 6.2.3. By Insulation

- 6.2.4. By Application

- 6.2.5. By Country

- 6.3. North America: Country Analysis

- 6.3.1. United States Large Power Transformer Market Outlook

- 6.3.1.1. Market Size & Forecast

- 6.3.1.1.1. By Value

- 6.3.1.2. Market Share & Forecast

- 6.3.1.2.1. By Power Rating

- 6.3.1.2.2. By Cooling Type

- 6.3.1.2.3. By Insulation

- 6.3.1.2.4. By Application

- 6.3.1.1. Market Size & Forecast

- 6.3.2. Canada Large Power Transformer Market Outlook

- 6.3.2.1. Market Size & Forecast

- 6.3.2.1.1. By Value

- 6.3.2.2. Market Share & Forecast

- 6.3.2.2.1. By Power Rating

- 6.3.2.2.2. By Cooling Type

- 6.3.2.2.3. By Insulation

- 6.3.2.2.4. By Application

- 6.3.2.1. Market Size & Forecast

- 6.3.3. Mexico Large Power Transformer Market Outlook

- 6.3.3.1. Market Size & Forecast

- 6.3.3.1.1. By Value

- 6.3.3.2. Market Share & Forecast

- 6.3.3.2.1. By Power Rating

- 6.3.3.2.2. By Cooling Type

- 6.3.3.2.3. By Insulation

- 6.3.3.2.4. By Application

- 6.3.3.1. Market Size & Forecast

- 6.3.1. United States Large Power Transformer Market Outlook

7. Asia-Pacific Large Power Transformer Market Outlook

- 7.1. Market Size & Forecast

- 7.1.1. By Value

- 7.2. Market Share & Forecast

- 7.2.1. By Power Rating

- 7.2.2. By Cooling Type

- 7.2.3. By Insulation

- 7.2.4. By Application

- 7.2.5. By Country

- 7.3. Asia-Pacific: Country Analysis

- 7.3.1. China Large Power Transformer Market Outlook

- 7.3.1.1. Market Size & Forecast

- 7.3.1.1.1. By Value

- 7.3.1.2. Market Share & Forecast

- 7.3.1.2.1. By Power Rating

- 7.3.1.2.2. By Cooling Type

- 7.3.1.2.3. By Insulation

- 7.3.1.2.4. By Application

- 7.3.1.1. Market Size & Forecast

- 7.3.2. India Large Power Transformer Market Outlook

- 7.3.2.1. Market Size & Forecast

- 7.3.2.1.1. By Value

- 7.3.2.2. Market Share & Forecast

- 7.3.2.2.1. By Power Rating

- 7.3.2.2.2. By Cooling Type

- 7.3.2.2.3. By Insulation

- 7.3.2.2.4. By Application

- 7.3.2.1. Market Size & Forecast

- 7.3.3. Japan Large Power Transformer Market Outlook

- 7.3.3.1. Market Size & Forecast

- 7.3.3.1.1. By Value

- 7.3.3.2. Market Share & Forecast

- 7.3.3.2.1. By Power Rating

- 7.3.3.2.2. By Cooling Type

- 7.3.3.2.3. By Insulation

- 7.3.3.2.4. By Application

- 7.3.3.1. Market Size & Forecast

- 7.3.4. South Korea Large Power Transformer Market Outlook

- 7.3.4.1. Market Size & Forecast

- 7.3.4.1.1. By Value

- 7.3.4.2. Market Share & Forecast

- 7.3.4.2.1. By Power Rating

- 7.3.4.2.2. By Cooling Type

- 7.3.4.2.3. By Insulation

- 7.3.4.2.4. By Application

- 7.3.4.1. Market Size & Forecast

- 7.3.5. Indonesia Large Power Transformer Market Outlook

- 7.3.5.1. Market Size & Forecast

- 7.3.5.1.1. By Value

- 7.3.5.2. Market Share & Forecast

- 7.3.5.2.1. By Power Rating

- 7.3.5.2.2. By Cooling Type

- 7.3.5.2.3. By Insulation

- 7.3.5.2.4. By Application

- 7.3.5.1. Market Size & Forecast

- 7.3.1. China Large Power Transformer Market Outlook

8. Europe Large Power Transformer Market Outlook

- 8.1. Market Size & Forecast

- 8.1.1. By Value

- 8.2. Market Share & Forecast

- 8.2.1. By Power Rating

- 8.2.2. By Cooling Type

- 8.2.3. By Insulation

- 8.2.4. By Application

- 8.2.5. By Country

- 8.3. Europe: Country Analysis

- 8.3.1. Germany Large Power Transformer Market Outlook

- 8.3.1.1. Market Size & Forecast

- 8.3.1.1.1. By Value

- 8.3.1.2. Market Share & Forecast

- 8.3.1.2.1. By Power Rating

- 8.3.1.2.2. By Cooling Type

- 8.3.1.2.3. By Insulation

- 8.3.1.2.4. By Application

- 8.3.1.1. Market Size & Forecast

- 8.3.2. United Kingdom Large Power Transformer Market Outlook

- 8.3.2.1. Market Size & Forecast

- 8.3.2.1.1. By Value

- 8.3.2.2. Market Share & Forecast

- 8.3.2.2.1. By Power Rating

- 8.3.2.2.2. By Cooling Type

- 8.3.2.2.3. By Insulation

- 8.3.2.2.4. By Application

- 8.3.2.1. Market Size & Forecast

- 8.3.3. France Large Power Transformer Market Outlook

- 8.3.3.1. Market Size & Forecast

- 8.3.3.1.1. By Value

- 8.3.3.2. Market Share & Forecast

- 8.3.3.2.1. By Power Rating

- 8.3.3.2.2. By Cooling Type

- 8.3.3.2.3. By Insulation

- 8.3.3.2.4. By Application

- 8.3.3.1. Market Size & Forecast

- 8.3.4. Russia Large Power Transformer Market Outlook

- 8.3.4.1. Market Size & Forecast

- 8.3.4.1.1. By Value

- 8.3.4.2. Market Share & Forecast

- 8.3.4.2.1. By Power Rating

- 8.3.4.2.2. By Cooling Type

- 8.3.4.2.3. By Insulation

- 8.3.4.2.4. By Application

- 8.3.4.1. Market Size & Forecast

- 8.3.5. Spain Large Power Transformer Market Outlook

- 8.3.5.1. Market Size & Forecast

- 8.3.5.1.1. By Value

- 8.3.5.2. Market Share & Forecast

- 8.3.5.2.1. By Power Rating

- 8.3.5.2.2. By Cooling Type

- 8.3.5.2.3. By Insulation

- 8.3.5.2.4. By Application

- 8.3.5.1. Market Size & Forecast

- 8.3.1. Germany Large Power Transformer Market Outlook

9. South America Large Power Transformer Market Outlook

- 9.1. Market Size & Forecast

- 9.1.1. By Value

- 9.2. Market Share & Forecast

- 9.2.1. By Power Rating

- 9.2.2. By Cooling Type

- 9.2.3. By Insulation

- 9.2.4. By Application

- 9.2.5. By Country

- 9.3. South America: Country Analysis

- 9.3.1. Brazil Large Power Transformer Market Outlook

- 9.3.1.1. Market Size & Forecast

- 9.3.1.1.1. By Value

- 9.3.1.2. Market Share & Forecast

- 9.3.1.2.1. By Power Rating

- 9.3.1.2.2. By Cooling Type

- 9.3.1.2.3. By Insulation

- 9.3.1.2.4. By Application

- 9.3.1.1. Market Size & Forecast

- 9.3.2. Argentina Large Power Transformer Market Outlook

- 9.3.2.1. Market Size & Forecast

- 9.3.2.1.1. By Value

- 9.3.2.2. Market Share & Forecast

- 9.3.2.2.1. By Power Rating

- 9.3.2.2.2. By Cooling Type

- 9.3.2.2.3. By Insulation

- 9.3.2.2.4. By Application

- 9.3.2.1. Market Size & Forecast

- 9.3.1. Brazil Large Power Transformer Market Outlook

10. Middle East & Africa Large Power Transformer Market Outlook

- 10.1. Market Size & Forecast

- 10.1.1. By Value

- 10.2. Market Share & Forecast

- 10.2.1. By Power Rating

- 10.2.2. By Cooling Type

- 10.2.3. By Insulation

- 10.2.4. By Application

- 10.2.5. By Country

- 10.3. Middle East & Africa: Country Analysis

- 10.3.1. Saudi Arabia Large Power Transformer Market Outlook

- 10.3.1.1. Market Size & Forecast

- 10.3.1.1.1. By Value

- 10.3.1.2. Market Share & Forecast

- 10.3.1.2.1. By Power Rating

- 10.3.1.2.2. By Cooling Type

- 10.3.1.2.3. By Insulation

- 10.3.1.2.4. By Application

- 10.3.1.1. Market Size & Forecast

- 10.3.2. South Africa Large Power Transformer Market Outlook

- 10.3.2.1. Market Size & Forecast

- 10.3.2.1.1. By Value

- 10.3.2.2. Market Share & Forecast

- 10.3.2.2.1. By Power Rating

- 10.3.2.2.2. By Cooling Type

- 10.3.2.2.3. By Insulation

- 10.3.2.2.4. By Application

- 10.3.2.1. Market Size & Forecast

- 10.3.3. UAE Large Power Transformer Market Outlook

- 10.3.3.1. Market Size & Forecast

- 10.3.3.1.1. By Value

- 10.3.3.2. Market Share & Forecast

- 10.3.3.2.1. By Power Rating

- 10.3.3.2.2. By Cooling Type

- 10.3.3.2.3. By Insulation

- 10.3.3.2.4. By Application

- 10.3.3.1. Market Size & Forecast

- 10.3.4. Israel Large Power Transformer Market Outlook

- 10.3.4.1. Market Size & Forecast

- 10.3.4.1.1. By Value

- 10.3.4.2. Market Share & Forecast

- 10.3.4.2.1. By Power Rating

- 10.3.4.2.2. By Cooling Type

- 10.3.4.2.3. By Insulation

- 10.3.4.2.4. By Application

- 10.3.4.1. Market Size & Forecast

- 10.3.5. Egypt Large Power Transformer Market Outlook

- 10.3.5.1. Market Size & Forecast

- 10.3.5.1.1. By Value

- 10.3.5.2. Market Share & Forecast

- 10.3.5.2.1. By Power Rating

- 10.3.5.2.2. By Cooling Type

- 10.3.5.2.3. By Insulation

- 10.3.5.2.4. By Application

- 10.3.5.1. Market Size & Forecast

- 10.3.1. Saudi Arabia Large Power Transformer Market Outlook

11. Market Dynamics

- 11.1. Drivers

- 11.2. Challenge

12. Market Trends & Developments

13. Company Profiles

- 13.1. Hitachi Energy Ltd

- 13.1.1. Business Overview

- 13.1.2. Key Revenue and Financials (If Available)

- 13.1.3. Recent Developments

- 13.1.4. Key Personnel

- 13.1.5. Key Product/Services

- 13.2. CG Power and Industrial Solutions Limited

- 13.2.1. Business Overview

- 13.2.2. Key Revenue and Financials

- 13.2.3. Recent Developments

- 13.2.4. Key Personnel

- 13.2.5. Key Product/Services

- 13.3. General Electric Company

- 13.3.1. Business Overview

- 13.3.2. Key Revenue and Financials (If Available)

- 13.3.3. Recent Developments

- 13.3.4. Key Personnel

- 13.3.5. Key Product/Services

- 13.4. Hyosung Power & Industrial Systems Performance Group

- 13.4.1. Business Overview

- 13.4.2. Key Revenue and Financials (If Available)

- 13.4.3. Recent Developments

- 13.4.4. Key Personnel

- 13.4.5. Key Product/Services

- 13.5. Hyundai Heavy Industries Co. Ltd

- 13.5.1. Business Overview

- 13.5.2. Key Revenue and Financials (If Available)

- 13.5.3. Recent Developments

- 13.5.4. Key Personnel

- 13.5.5. Key Product/Services

- 13.6. Mitsubishi Electric Corporation

- 13.6.1. Business Overview

- 13.6.2. Key Revenue and Financials (If Available)

- 13.6.3. Recent Developments

- 13.6.4. Key Personnel

- 13.6.5. Key Product/Services

- 13.7. SGB-SMIT International GmbH

- 13.7.1. Business Overview

- 13.7.2. Key Revenue and Financials

- 13.7.3. Recent Developments

- 13.7.4. Key Personnel

- 13.7.5. Key Product/Services

- 13.8. Siemens Energy AG

- 13.8.1. Business Overview

- 13.8.2. Key Revenue and Financials (If Available)

- 13.8.3. Recent Developments

- 13.8.4. Key Personnel

- 13.8.5. Key Product/Services

- 13.9. SPX Corporation

- 13.9.1. Business Overview

- 13.9.2. Key Revenue and Financials (If Available)

- 13.9.3. Recent Developments

- 13.9.4. Key Personnel

- 13.9.5. Key Product/Services

14. Strategic Recommendations

About Us & Disclaimer