|

|

市場調査レポート

商品コード

1567818

欧州の研磨剤市場の2030年予測- 地域別分析- 素材、タイプ、用途、販売チャネル別Europe Abrasive Market Forecast to 2030 - Regional Analysis - by Material, Type, Application, and Sales Channel |

||||||

|

|||||||

|

|||||||

| 欧州の研磨剤市場の2030年予測- 地域別分析- 素材、タイプ、用途、販売チャネル別 |

|

出版日: 2024年08月07日

発行: The Insight Partners

ページ情報: 英文 158 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

欧州の研磨剤市場は、2022年に49億1,115万米ドルと評価され、2030年には69億7,900万米ドルに達すると予測され、2022年から2030年までのCAGRは4.5%と推定されます。

自動化とロボット用途への研磨剤の採用が欧州研磨剤市場を牽引

国際ロボット連盟が2022年に発表した報告書によると、2021年の世界の年間ロボット導入台数は51万7,385台に達し、2020年比で31%増加しました。自動車産業は、2021年のロボット導入台数の23%を占める11万9,000台の年間導入台数を記録し、部品サプライヤー部門が大きく牽引しました。産業用ロボットは、自動車や電子機器メーカーなどの最終用途産業から最も高い需要を獲得しています。最終用途産業におけるロボット使用の増加は、ロボットの平均販売価格の低下に起因しています。Castrol Ltdの調査によると、2025年までに世界中で400万台以上の産業用ロボットが稼働すると予想されています。自動化およびロボット用途での研磨剤の使用増加の背景には、工業生産への移行があります。自動車、エレクトロニクス、航空宇宙などさまざまな分野でオートメーション技術が進歩し、ロボットの利用が増加していることが、精密工学を後押ししています。砥粒は、研削、研磨、バリ取りなどの作業を比類のない精度と一貫性で促進する重要な部品です。研磨剤を搭載したロボットの採用は、生産プロセスを合理化し、ダウンタイムを最小限に抑え、コスト削減につながります。3M Co、VSM Abrasives、Norton Abrasivesなどの市場各社は、ロボット用途に特化した研磨剤を提供しています。自動化が進化し続ける中、ロボット工学に研磨剤を活用することで、高精度、高生産性、高パフォーマンスを実現し、工業生産に革命をもたらすことが期待されます。

欧州研磨剤市場の概要

自動車産業は欧州で最も急成長している重要な産業のひとつです。自動車産業は、ドイツ、英国、イタリアなど欧州各国のGDPに大きく貢献しています。欧州委員会によると、欧州は世界最大の自動車メーカーです。自動車産業は直接・間接的に1,380万人を雇用しており、欧州連合(EU)の雇用全体の6.1%を占めています。国際自動車製造者機構(OICA)によると、EUでは2022年に1,620万台の自動車が生産されました。この地域には、フォルクスワーゲンAG、ステランティスNV、メルセデス・ベンツ・グループAG、バイエルン自動車工業AG、ルノーSAなど、著名な自動車メーカーが数社あります。欧州では自動車の生産台数が増加しているため、製造工程のさまざまな段階で研磨剤のニーズが高まっています。金属部品の成形や仕上げから自動車部品の表面の研磨に至るまで、研磨剤は自動車製造の精度と品質を確保する上で重要な役割を果たしています。さらに、自動車業界は高度な合金や複合材料を含む軽量素材を追求し続けているため、特殊な研磨剤への要求が高まっています。これらの材料は精密な機械加工と仕上げを要求するため、研磨剤は軽量で低燃費の自動車製造において望ましい仕様を達成するために不可欠となっています。

もう一つの重要な原動力は建設業界です。欧州ではインフラ整備や改修プロジェクトが進行しており、さまざまな建設用途で研磨剤のニーズが高まっています。FIEC(欧州建設産業連盟)によると、2022年12月の建設工事量は2021年12月と比べて15.1%増加しました。この増加には、資本補修工事(34.7%増)、現在の保守・補修工事(29.6%増)、新築工事(7.0%増)が含まれます。表面処理に加え、建設業界は金属、石材、石積みなどの材料の切断や成形にも研磨剤を使用しています。鉄骨梁の切断から建築要素の複雑な細部の成形に至るまで、研磨工具は建設プロジェクトで精度を達成し設計仕様を満たすために不可欠です。これは特に、構造フレームワークや建築の細部に使用される金属部品の製造において顕著です。

さらに2022年には、欧州の航空宇宙・防衛産業がパンデミック後の経済復活を維持しました。航空産業では、研磨剤は金属や複合材など様々な材料の成形、仕上げ、精錬に不可欠です。これらの材料は航空機構造の構築に幅広く使用されており、研磨剤は航空力学的効率と構造的完全性に必要な厳しい公差と滑らかな表面を達成する上で重要な役割を果たしています。

欧州研磨剤市場の収益と2030年までの予測(金額)

欧州研磨剤市場のセグメンテーション

欧州の研磨剤市場は、素材、タイプ、用途、販売チャネル、国に分類されます。

素材別では、欧州の研磨剤市場は天然と合成に二分されます。2022年の欧州研磨剤市場は合成セグメントが大きなシェアを占めています。

タイプ別では、欧州の研磨市場はボンド研磨剤とコーティング研磨剤に二分されます。ボンド砥粒セグメントは2022年に欧州研磨剤市場でより大きなシェアを占めました。さらに、ボンド砥粒セグメントはディスク、ホイール、その他に細分化されます。さらに、コーティング研磨剤セグメントは、フラップディスク、ファイバーディスク、フックアループディスク、ベルト、ロール、その他に細分化されます。

用途別では、欧州の研磨市場は自動車、航空宇宙、海洋、金属加工、木工、電気・電子、その他に区分されます。2022年の欧州の研磨市場では、自動車分野が最大のシェアを占めています。

難聴の販売チャネルに基づいて、欧州研磨剤市場は直接と間接に二分されます。2022年の欧州研磨剤市場では、間接セグメントが大きなシェアを占めています。

国別では、欧州研磨剤市場はドイツ、フランス、イタリア、スペイン、英国、ロシア、ポーランド、チェコ共和国、ハンガリー、エストニア、ラトビア、ルーマニア、その他欧州に区分されます。その他欧州が2022年の欧州研磨剤市場シェアを独占。

Deerfos Co.Ltd.、CUMI AWUKO Abrasives GmbH、Robert Bosch GmbH、Tyrolit Schleifmittelwerke Swarovski AG &Co KG、Sun Abrasives Co Ltd、Compagnie de Saint-Gobain S.A.、sia Abrasives Industries AG、RHODIUS Abrasives GmbH、3M Co.、Ekamant ABなどが欧州研磨剤市場で事業を展開する主要企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 研磨剤市場情勢

- ポーター分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係の強さ

- 代替品の脅威

- エコシステム分析

- 各種研磨メディアの特性

- バリューチェーンのベンダー一覧

第5章 欧州の研磨剤市場:主要市場力学

- 市場促進要因

- 自動車産業と金属加工産業の成長

- 電気・電子産業からの研磨剤需要の増加

- 市場抑制要因

- 原材料価格の変動

- 市場機会

- 自動化・ロボット用途での研磨剤の採用

- 今後の動向

- 持続可能な研磨剤の開発

- 促進要因と抑制要因の影響

第6章 研磨剤市場:欧州分析

- 研磨剤市場の売上高、2020年~2030年

- 研磨剤市場の予測分析

第7章 欧州研磨剤市場分析-素材別

- 天然

- 合成

第8章 欧州研磨剤市場分析:タイプ別

- ボンド砥粒

- コーティング砥粒

第9章 欧州研磨剤市場分析-用途別

- 自動車

- 航空宇宙

- 海洋

- 金属加工

- 木工

- 電気・電子

- その他

第10章 欧州研磨剤市場分析:販売チャネル別

- 直接

- 間接販売

第11章 欧州研磨剤市場欧州研磨剤市場:国別分析

- 欧州

- ドイツ

- フランス

- イタリア

- スペイン

- 英国

- ロシア

- ポーランド

- チェコ共和国

- ハンガリー

- エストニア

- ラトビア

- ルーマニア

- その他欧州

第12章 競合情勢

- 主要プレーヤーによるヒートマップ分析

- 企業のポジショニングと集中度

第13章 業界情勢

- 製品発売

- 合併と買収

- 事業拡大

- その他の戦略と展開

第14章 企業プロファイル

- Deerfos Co., Ltd.

- CUMI AWUKO Abrasives GmbH

- Robert Bosch GmbH

- Tyrolit Schleifmittelwerke Swarovski AG & Co KG

- Sun Abrasives Co Ltd

- Compagnie de Saint-Gobain S.A.

- sia Abrasives Industries AG

- RHODIUS Abrasives GmbH

- 3M Co

- Ekamant AB

第15章 付録

List Of Tables

- Table 1. Europe Abrasive Market Segmentation

- Table 2. List of Vendors

- Table 3. Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Table 4. Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Material

- Table 5. Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Type

- Table 6. Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Application

- Table 7. Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Sales Channel

- Table 8. Germany: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Material

- Table 9. Germany: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Type

- Table 10. Germany: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Application

- Table 11. Germany: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Sales Channel

- Table 12. France: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Material

- Table 13. France: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Type

- Table 14. France: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Application

- Table 15. France: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Sales Channel

- Table 16. Italy: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Material

- Table 17. Italy: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Type

- Table 18. Italy: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Application

- Table 19. Italy: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Sales Channel

- Table 20. Spain: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Material

- Table 21. Spain: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Type

- Table 22. Spain: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Application

- Table 23. Spain: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Sales Channel

- Table 24. United Kingdom: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Material

- Table 25. United Kingdom: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Type

- Table 26. United Kingdom: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Application

- Table 27. United Kingdom: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Sales Channel

- Table 28. Russia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Material

- Table 29. Russia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Type

- Table 30. Russia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Application

- Table 31. Russia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Sales Channel

- Table 32. Poland: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Material

- Table 33. Poland: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Type

- Table 34. Poland: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Application

- Table 35. Poland: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Sales Channel

- Table 36. Czech Republic: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Material

- Table 37. Czech Republic: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Type

- Table 38. Czech Republic: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Application

- Table 39. Czech Republic: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Sales Channel

- Table 40. Hungary: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Material

- Table 41. Hungary: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Type

- Table 42. Hungary: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Application

- Table 43. Hungary: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Sales Channel

- Table 44. Estonia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Material

- Table 45. Estonia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Type

- Table 46. Estonia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Application

- Table 47. Estonia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Sales Channel

- Table 48. Latvia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Material

- Table 49. Latvia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Type

- Table 50. Latvia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Application

- Table 51. Latvia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Sales Channel

- Table 52. Romania: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Material

- Table 53. Romania: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Type

- Table 54. Romania: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Application

- Table 55. Romania: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Sales Channel

- Table 56. Rest of Europe: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Material

- Table 57. Rest of Europe: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Type

- Table 58. Rest of Europe: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Application

- Table 59. Rest of Europe: Abrasive Market - Revenue and Forecast to 2030 (US$ Million) - by Sales Channel

List Of Figures

- Figure 1. Europe Abrasive Market Segmentation, by Country

- Figure 2. Abrasive Market - Porter?s Analysis

- Figure 3. Ecosystem: Abrasive Market

- Figure 4. Abrasive Grain Processing

- Figure 5. Bonded Abrasive Product Manufacturing Process

- Figure 6. Coated Abrasive Product Manufacturing Process

- Figure 7. Abrasive Market - Key Market Dynamics

- Figure 8. Production Value by the Global Electronics and IT Industries (2015-2023)

- Figure 9. Impact Analysis of Drivers and Restraints

- Figure 10. Abrasive Market Revenue (US$ Million), 2020-2030

- Figure 11. Abrasive Market Share (%) - by Material (2022 and 2030)

- Figure 12. Natural: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 13. Synthetic: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 14. Abrasive Market Share (%) - by Type (2022 and 2030)

- Figure 15. Bonded Abrasives: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 16. Discs: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 17. Wheels: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 18. Others: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 19. Coated Abrasives: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 20. Flap Discs: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 21. Fiber Discs: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 22. Hook and Loop Discs: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 23. Belts: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 24. Rolls: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 25. Others: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 26. Abrasive Market Share (%) - by Application (2022 and 2030)

- Figure 27. Automotive: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 28. Aerospace: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 29. Marine: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 30. Metal Fabrication: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 31. Woodworking: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 32. Electrical and Electronics: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 33. Others: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 34. Abrasive Market Share (%) - by Sales Channel (2022 and 2030)

- Figure 35. Direct: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 36. Indirect: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 37. Europe: Abrasive Market, By Key Country - Revenue 2022 (US$ Million)

- Figure 38. Europe: Abrasive Market Breakdown, by Key Countries, 2022 and 2030 (%)

- Figure 39. Germany: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 40. France: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 41. Italy: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 42. Spain: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 43. United Kingdom: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 44. Russia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 45. Poland: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 46. Czech Republic: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 47. Hungary: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 48. Estonia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 49. Latvia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 50. Romania: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 51. Rest of Europe: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 52. Heat Map Analysis by Key Players

- Figure 53. Company Positioning & Concentration

The Europe abrasive market was valued at US$ 4,911.15 million in 2022 and is expected to reach US$ 6,979.00 million by 2030; it is estimated to register a CAGR of 4.5% from 2022 to 2030.

Adoption of Abrasives in Automation and Robotic Applications Drives Europe Abrasive Market

According to the report published by the International Federation of Robotics in 2022, the total annual robot installations worldwide reached 517,385 units in 2021, a rise of 31% compared to 2020. The automotive industry registered ~119,000 units of annual robot installations worldwide, accounting for 23% of total robot installations in 2021, significantly driven by the component supplier segment. Industrial robots are gaining the highest demand from end-use industries such as automotive and electronics original equipment manufacturers. The increase in the use of robots in end-use industries is attributed to the reduction in the average selling price of robots. According to Castrol Ltd's research, more than 4 million industrial robots are expected to be operational worldwide by 2025. The rising use of abrasives in automation and robotic applications is attributed to the transition to industrial manufacturing. The advancement in automation technology and increased use of robots in various sectors such as automotive, electronics, and aerospace have driven precision engineering. Abrasives are significant components for facilitating tasks such as grinding, polishing, and deburring with unparalleled accuracy and consistency. The adoption of abrasive-equipped robots streamlines production processes, minimizes downtime, and leads to cost savings. Market players, such as 3M Co, VSM Abrasives, and Norton Abrasives, offer abrasives with distinct characteristics for robotic applications. As automation continues to evolve, the utilization of abrasives with robotics is expected to revolutionize industrial manufacturing, offering high precision, productivity, and performance.

Europe Abrasive Market Overview

The automobile industry is among the most rapidly growing and most important industries in Europe. The automotive industry contributes notably to the GDPs of several European countries, including Germany, the UK, and Italy. According to the European Commission, Europe is the largest manufacturer of motor vehicles worldwide. The automobile industry directly and indirectly employs ?13.8 million people, resulting in 6.1% of overall employment in the European Union (EU). According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), the EU produced 16.2 million vehicles in 2022. The region has several prominent automotive players, including Volkswagen AG, Stellantis NV, Mercedes-Benz Group AG, Bayerische Motoren Werke AG, and Renault SA. The increasing production of vehicles in Europe has amplified the need for abrasives in various stages of the manufacturing process. From shaping and finishing metal components to refining the surfaces of automotive parts, abrasives play a vital role in ensuring the precision and quality of vehicle manufacturing. Moreover, the automotive industry's continuous pursuit of lightweight materials, including advanced alloys and composites, has intensified the requirement for specialized abrasives. These materials demand precision machining and finishing, making abrasives essential for achieving the desired specifications in the production of lightweight and fuel-efficient vehicles.

Another significant driver is the construction industry. With ongoing infrastructure development and renovation projects in Europe, there is a heightened need for abrasives in various construction applications. According to the FIEC - European Construction Industry Federation, the volume of construction works increased by 15.1% in December 2022 as compared with December 2021. The increase highlighted capital repair works (+34.7%), current maintenance and repair works (+29.6%), and new construction works (+7.0%). In addition to surface preparation, the construction industry relies on abrasives for cutting and shaping materials such as metal, stone, and masonry. From cutting steel beams to shaping intricate details in architectural elements, abrasive tools are indispensable for achieving precision and meeting the design specifications in construction projects. This is particularly evident in the fabrication of metal components used in structural frameworks and architectural details.

Furthermore, in 2022, the European aerospace & defense industry sustained its post-pandemic economic resurgence. In the aviation industry, abrasives are essential for shaping, finishing, and refining various materials such as metals and composites. These materials are used extensively in the construction of aircraft structures, and abrasives play a critical role in achieving the tight tolerance and smooth surfaces necessary for aerodynamic efficiency and structural integrity.

Europe Abrasive Market Revenue and Forecast to 2030 (US$ Million)

Europe Abrasive Market Segmentation

The Europe abrasive market is categorized into material, type, application, sales channel, and country.

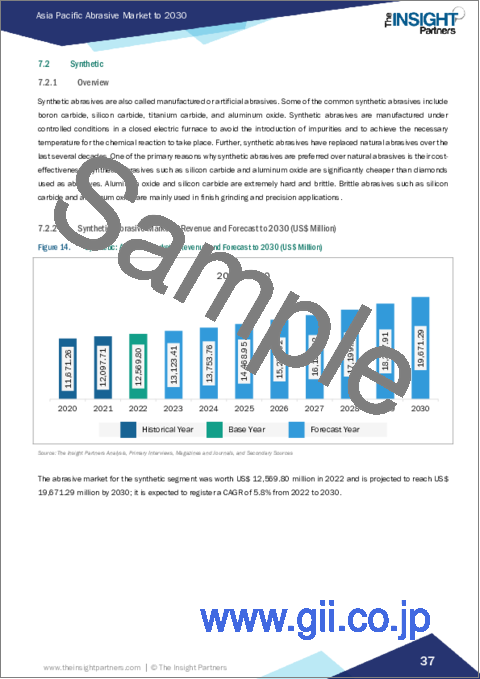

By material, the Europe abrasive market is bifurcated into natural and synthetic. The synthetic segment held a larger share of Europe abrasive market in 2022.

In terms of type, the Europe abrasive market is bifurcated into bonded abrasives and coated abrasives. The bonded abrasives segment held a larger share of Europe abrasive market in 2022. Furthermore, the bonded abrasives segment is subcategorized into discs, wheels, and others. Additionally, the coated abrasives segment is subcategorized into flap discs, fiber discs, hook a loop discs, belts, rolls, and others.

By application, the Europe abrasive market is segmented into automotive, aerospace, marine, metal fabrication, woodworking, electrical & electronics, and others. The automotive segment held the largest share of Europe abrasive market in 2022.

Based on sales channel of hearing loss, the Europe abrasive market is bifurcated into direct and indirect. The indirect segment held a larger share of Europe abrasive market in 2022.

By country, the Europe abrasive market is segmented into Germany, France, Italy, Spain, the UK, Russia, Poland, Czech Republic, Hungary, Estonia, Latvia, Romania, and the Rest of Europe. The Rest of Europe dominated the Europe abrasive market share in 2022.

Deerfos Co., Ltd; CUMI AWUKO Abrasives GmbH; Robert Bosch GmbH; Tyrolit Schleifmittelwerke Swarovski AG & Co KG; Sun Abrasives Co Ltd; Compagnie de Saint-Gobain S.A.; sia Abrasives Industries AG; RHODIUS Abrasives GmbH; 3M Co; and Ekamant AB are the among leading companies operating in the Europe abrasive market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Abrasive Market Landscape

- 4.1 Overview

- 4.2 Porter's Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Ecosystem Analysis

- 4.3.1 Properties of Different Abrasive Media Types

- 4.3.2 List of Vendors in the Value Chain

5. Europe Abrasive Market - Key Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Growing Automotive and Metal Fabrication Industry

- 5.1.2 Rising Demand for Abrasives from Electrical and Electronics Industry

- 5.2 Market Restraints

- 5.2.1 Fluctuations in Raw Material Prices

- 5.3 Market Opportunities

- 5.3.1 Adoption of Abrasives in Automation and Robotic Applications

- 5.4 Future Trends

- 5.4.1 Development of Sustainable Abrasives

- 5.5 Impact of Drivers and Restraints:

6. Abrasive Market -Europe Analysis

- 6.1 Overview

- 6.2 Abrasive Market Revenue (US$ Million), 2020-2030

- 6.3 Abrasive Market Forecast Analysis

7. Europe Abrasive Market Analysis - by Material

- 7.1 Natural

- 7.1.1 Overview

- 7.1.2 Natural: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2 Synthetic

- 7.2.1 Overview

- 7.2.2 Synthetic: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

8. Europe Abrasive Market Analysis - by Type

- 8.1 Bonded Abrasives

- 8.1.1 Overview

- 8.1.2 Bonded Abrasives: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 8.1.3 Discs

- 8.1.3.1 Overview

- 8.1.3.2 Discs: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 8.1.4 Wheels

- 8.1.4.1 Overview

- 8.1.4.2 Wheels: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 8.1.5 Others

- 8.1.5.1 Overview

- 8.1.5.2 Others: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 8.2 Coated Abrasives

- 8.2.1 Overview

- 8.2.1.1 Coated Abrasives: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 8.2.2 Flap Discs

- 8.2.2.1 Overview

- 8.2.2.2 Flap Discs: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 8.2.3 Fiber Discs

- 8.2.3.1 Overview

- 8.2.3.2 Fiber Discs: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 8.2.4 Hook and Loop Discs

- 8.2.4.1 Overview

- 8.2.4.2 Hook and Loop Discs: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 8.2.5 Belts

- 8.2.5.1 Overview

- 8.2.5.2 Belts: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 8.2.6 Rolls

- 8.2.6.1 Overview

- 8.2.6.2 Rolls: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 8.2.7 Others

- 8.2.7.1 Overview

- 8.2.7.2 Others: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 8.2.1 Overview

9. Europe Abrasive Market Analysis - by Application

- 9.1 Automotive

- 9.1.1 Overview

- 9.1.2 Automotive: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 9.2 Aerospace

- 9.2.1 Overview

- 9.2.2 Aerospace: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 9.3 Marine

- 9.3.1 Overview

- 9.3.2 Marine: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 9.4 Metal Fabrication

- 9.4.1 Overview

- 9.4.2 Metal Fabrication: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 9.5 Woodworking

- 9.5.1 Overview

- 9.5.2 Woodworking: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 9.6 Electrical and Electronics

- 9.6.1 Overview

- 9.6.2 Electrical and Electronics: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 9.7 Others

- 9.7.1 Overview

- 9.7.2 Others: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

10. Europe Abrasive Market Analysis - by Sales Channel

- 10.1 Direct

- 10.1.1 Overview

- 10.1.2 Direct: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 10.2 Indirect

- 10.2.1 Overview

- 10.2.2 Indirect: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

11. Europe Abrasive Market - Country Analysis

- 11.1 Europe

- 11.1.1 Europe: Abrasive Market - Revenue and Forecast Analysis - by Country

- 11.1.1.1 Germany: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.1.1 Germany: Abrasive Market Breakdown, by Material

- 11.1.1.1.2 Germany: Abrasive Market Breakdown, by Type

- 11.1.1.1.3 Germany: Abrasive Market Breakdown, by Application

- 11.1.1.1.4 Germany: Abrasive Market Breakdown, by Sales Channel

- 11.1.1.2 France: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.2.1 France: Abrasive Market Breakdown, by Material

- 11.1.1.2.2 France: Abrasive Market Breakdown, by Type

- 11.1.1.2.3 France: Abrasive Market Breakdown, by Application

- 11.1.1.2.4 France: Abrasive Market Breakdown, by Sales Channel

- 11.1.1.3 Italy: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.3.1 Italy: Abrasive Market Breakdown, by Material

- 11.1.1.3.2 Italy: Abrasive Market Breakdown, by Type

- 11.1.1.3.3 Italy: Abrasive Market Breakdown, by Application

- 11.1.1.3.4 Italy: Abrasive Market Breakdown, by Sales Channel

- 11.1.1.4 Spain: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.4.1 Spain: Abrasive Market Breakdown, by Material

- 11.1.1.4.2 Spain: Abrasive Market Breakdown, by Type

- 11.1.1.4.3 Spain: Abrasive Market Breakdown, by Application

- 11.1.1.4.4 Spain: Abrasive Market Breakdown, by Sales Channel

- 11.1.1.5 United Kingdom: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.5.1 United Kingdom: Abrasive Market Breakdown, by Material

- 11.1.1.5.2 United Kingdom: Abrasive Market Breakdown, by Type

- 11.1.1.5.3 United Kingdom: Abrasive Market Breakdown, by Application

- 11.1.1.5.4 United Kingdom: Abrasive Market Breakdown, by Sales Channel

- 11.1.1.6 Russia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.6.1 Russia: Abrasive Market Breakdown, by Material

- 11.1.1.6.2 Russia: Abrasive Market Breakdown, by Type

- 11.1.1.6.3 Russia: Abrasive Market Breakdown, by Application

- 11.1.1.6.4 Russia: Abrasive Market Breakdown, by Sales Channel

- 11.1.1.7 Poland: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.7.1 Poland: Abrasive Market Breakdown, by Material

- 11.1.1.7.2 Poland: Abrasive Market Breakdown, by Type

- 11.1.1.7.3 Poland: Abrasive Market Breakdown, by Application

- 11.1.1.7.4 Poland: Abrasive Market Breakdown, by Sales Channel

- 11.1.1.8 Czech Republic: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.8.1 Czech Republic: Abrasive Market Breakdown, by Material

- 11.1.1.8.2 Czech Republic: Abrasive Market Breakdown, by Type

- 11.1.1.8.3 Czech Republic: Abrasive Market Breakdown, by Application

- 11.1.1.8.4 Czech Republic: Abrasive Market Breakdown, by Sales Channel

- 11.1.1.9 Hungary: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.9.1 Hungary: Abrasive Market Breakdown, by Material

- 11.1.1.9.2 Hungary: Abrasive Market Breakdown, by Type

- 11.1.1.9.3 Hungary: Abrasive Market Breakdown, by Application

- 11.1.1.9.4 Hungary: Abrasive Market Breakdown, by Sales Channel

- 11.1.1.10 Estonia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.10.1 Estonia: Abrasive Market Breakdown, by Material

- 11.1.1.10.2 Estonia: Abrasive Market Breakdown, by Type

- 11.1.1.10.3 Estonia: Abrasive Market Breakdown, by Application

- 11.1.1.10.4 Estonia: Abrasive Market Breakdown, by Sales Channel

- 11.1.1.11 Latvia: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.11.1 Latvia: Abrasive Market Breakdown, by Material

- 11.1.1.11.2 Latvia: Abrasive Market Breakdown, by Type

- 11.1.1.11.3 Latvia: Abrasive Market Breakdown, by Application

- 11.1.1.11.4 Latvia: Abrasive Market Breakdown, by Sales Channel

- 11.1.1.12 Romania: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.12.1 Romania: Abrasive Market Breakdown, by Material

- 11.1.1.12.2 Romania: Abrasive Market Breakdown, by Type

- 11.1.1.12.3 Romania: Abrasive Market Breakdown, by Application

- 11.1.1.12.4 Romania: Abrasive Market Breakdown, by Sales Channel

- 11.1.1.13 Rest of Europe: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.13.1 Rest of Europe: Abrasive Market Breakdown, by Material

- 11.1.1.13.2 Rest of Europe: Abrasive Market Breakdown, by Type

- 11.1.1.13.3 Rest of Europe: Abrasive Market Breakdown, by Application

- 11.1.1.13.4 Rest of Europe: Abrasive Market Breakdown, by Sales Channel

- 11.1.1.1 Germany: Abrasive Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1 Europe: Abrasive Market - Revenue and Forecast Analysis - by Country

12. Competitive Landscape

- 12.1 Heat Map Analysis by Key Players

- 12.2 Company Positioning & Concentration

13. Industry Landscape

- 13.1 Overview

- 13.2 Product launch

- 13.3 Mergers and Acquisitions

- 13.4 Expansion

- 13.5 Other Strategies and Developments

14. Company Profiles

- 14.1 Deerfos Co., Ltd.

- 14.1.1 Key Facts

- 14.1.2 Business Description

- 14.1.3 Products and Services

- 14.1.4 Financial Overview

- 14.1.5 SWOT Analysis

- 14.1.6 Key Developments

- 14.2 CUMI AWUKO Abrasives GmbH

- 14.2.1 Key Facts

- 14.2.2 Business Description

- 14.2.3 Products and Services

- 14.2.4 Financial Overview

- 14.2.5 SWOT Analysis

- 14.2.6 Key Developments

- 14.3 Robert Bosch GmbH

- 14.3.1 Key Facts

- 14.3.2 Business Description

- 14.3.3 Products and Services

- 14.3.4 Financial Overview

- 14.3.5 SWOT Analysis

- 14.3.6 Key Developments

- 14.4 Tyrolit Schleifmittelwerke Swarovski AG & Co KG

- 14.4.1 Key Facts

- 14.4.2 Business Description

- 14.4.3 Products and Services

- 14.4.4 Financial Overview

- 14.4.5 SWOT Analysis

- 14.4.6 Key Developments

- 14.5 Sun Abrasives Co Ltd

- 14.5.1 Key Facts

- 14.5.2 Business Description

- 14.5.3 Products and Services

- 14.5.4 Financial Overview

- 14.5.5 SWOT Analysis

- 14.5.6 Key Developments

- 14.6 Compagnie de Saint-Gobain S.A.

- 14.6.1 Key Facts

- 14.6.2 Business Description

- 14.6.3 Products and Services

- 14.6.4 Financial Overview

- 14.6.5 SWOT Analysis

- 14.6.6 Key Developments

- 14.7 sia Abrasives Industries AG

- 14.7.1 Key Facts

- 14.7.2 Business Description

- 14.7.3 Products and Services

- 14.7.4 Financial Overview

- 14.7.5 SWOT Analysis

- 14.7.6 Key Developments

- 14.8 RHODIUS Abrasives GmbH

- 14.8.1 Key Facts

- 14.8.2 Business Description

- 14.8.3 Products and Services

- 14.8.4 Financial Overview

- 14.8.5 SWOT Analysis

- 14.8.6 Key Developments

- 14.9 3M Co

- 14.9.1 Key Facts

- 14.9.2 Business Description

- 14.9.3 Products and Services

- 14.9.4 Financial Overview

- 14.9.5 SWOT Analysis

- 14.9.6 Key Developments

- 14.10 Ekamant AB

- 14.10.1 Key Facts

- 14.10.2 Business Description

- 14.10.3 Products and Services

- 14.10.4 Financial Overview

- 14.10.5 SWOT Analysis

- 14.10.6 Key Developments

15. Appendix

- 15.1 About the Insight Partners

?