|

市場調査レポート

商品コード

1851614

研磨材:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Abrasives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 研磨材:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月03日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

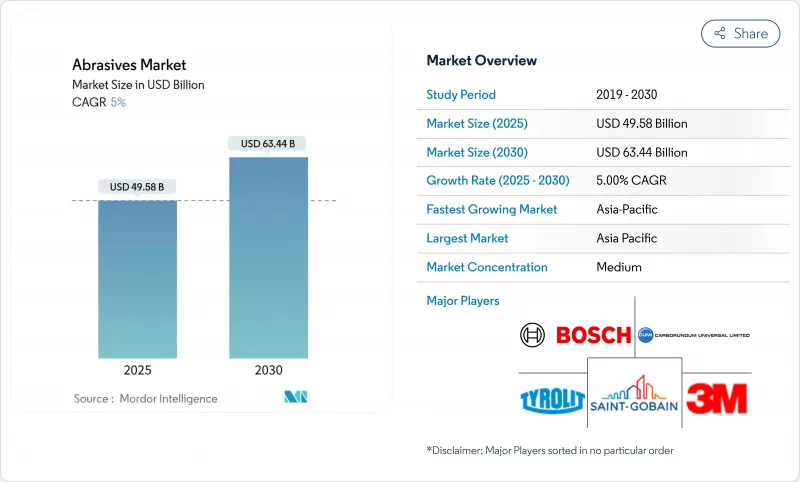

研磨材市場規模は2025年に495億8,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5%で、2030年には634億4,000万米ドルに達すると予測されます。

販売の勢いは、特に電気自動車(EV)や航空宇宙部品の加工において、高度なCNC装置で厳しい公差を保持できる高性能材料に対する需要の高まりを反映しています。合成グレードは、信頼できる硬度と熱安定性を提供するため、引き続き注文を獲得しており、一方、ボンド形式は依然として高温研削用の主力製品です。アジアにおける急速な工業化、精密エレクトロニクスへの軸足、積層造形のための後処理ニーズの出現は、すべて研磨材市場の成長余地を補強しています。競争企業間の敵対関係は激化しています。規制当局が粒子状物質や揮発性有機化合物(VOC)の基準を強化する中、大手既存企業は環境に優しい化学物質を中心に製品ポートフォリオを改良しており、ニッチメーカーはダイヤモンドベースのスーパー研磨材などの特殊なニッチ分野でシェアを拡大しています。

世界の研磨材市場の動向と洞察

航空宇宙産業と自動車産業での使用の増加

先進的な航空機用合金や軽量のEVドライブトレインの需要により、製造業者は高速で形状を維持する立方晶窒化ホウ素(CBN)ホイールやダイヤモンドホイールを指定するようになっています。ティアワン・サプライヤーは、サイクルタイムを短縮し、ドレッサ間隔を延長するビトリファイドCBNとセラミックメディアを使用して、Eアクスル、ローターシャフト、バッテリーハウジングの加工ラインを最適化しています。ノートンの研磨材は、ダイヤモンド工具を自動負荷検知システムと組み合わせることで、スクラップ率が測定可能なほど低下することを報告しており、OEMが再現性のために高級材種を標準とする理由を示しています。組立ラインにロボットが普及するにつれ、研磨材市場は、手動研削では対応できない一貫した表面仕上げの要求から利益を得ています。

成長する金属製造および加工産業

スチールサービスセンター、圧力容器工場、受託加工業者は、研削ステーションをセラミック砥粒ベルトでアップグレードしました。ベルト交換のためのダウンタイムの短縮は、リーンプログラムの下でますます監視されるようになっている指標である総合設備効率(OEE)の向上につながります。VSM TOP SIZEなどの特殊なトップコートは、ステンレスワークの熱変色を軽減し、熱歪みなしに高い送り圧力を可能にします。このような生産性の向上は、迅速な注文スループットをサポートし、ハイエンド・セラミック・グレードをコスト重視の大量生産環境において不可欠なものにしています。

高い生産コストと設備コスト

合成ダイヤモンドとCBN結晶は、地質学的条件を超える圧力と温度下で成長するため、反応容器の資本集約度が従来の溶融アルミナ・ラインをはるかに上回ります。ダイヤモンドホイール用に構成されたシングルヘッドCNCグラインダーは、高精度のスピンドルとクローズドループのクーラントシステムを必要とするため、取得コストが上昇します。これらの工具は、より長寿命で部品単価を下げるが、価格に敏感な経済圏の中小規模の加工工場では、いまだにアップグレードを先延ばしにしています。ベンダーは、リースモデルや消耗品クレジットプログラムを試みているが、資金調達の制約により、採用はまだ限られています。

セグメント分析

2024年の研磨材市場では、合成グレードのシェアが67%を占め、生産稼働中の予測可能な摩耗パターンにつながる一貫した結晶形態に対するユーザーの嗜好を裏付けています。酸化アルミニウムは依然として量的リーダーであるが、炭化ケイ素は非鉄機械加工に対応し、CBNは硬化鋼に好まれています。住友電工が開発中の新しいナノ多結晶ダイヤモンドは、優れた破壊靭性を約束し、研磨材市場をニッケル基超合金の低ホイール摩耗率加工に位置づける。天然ガーネットは、リサイクル可能なバルクメディアと低含有フリーシリカが現場の安全性を向上させ、インフラ改修プロジェクトに魅力的なウォータージェットとブラスト作業の足場を維持しています。

合成品へのシフトは、粒度分布の厳密さが要求される自動供給システムと整合しており、このパラメーターは設計された生産ルートによって達成しやすくなっています。アジアでは溶融アルミナの生産能力が増強されており、供給安定性は向上しているが、電力料金の変動が生産コストを左右する可能性があります。エコラベルを追求するメーカーは、再生可能エネルギーで稼働するアーク炉やクローズドループ急冷回路に投資し、規制地域でのシェア維持に努めています。その結果、研磨材市場は、大量生産分野でも品質ベンチマークのアップグレードを続けています。

ボンド砥石は、自動車、航空宇宙、および一般的なエンジニアリング工場での切断、研磨、表面調整作業における役割を反映して、2024年の売上高の48%を占めました。レジノイドとビトリファイドマトリックスは、深い切断作業中に熱安定性を提供し、冶金的完全性が重要なクランクシャフトやタービンブレードの一貫した公差を可能にします。ゾルゲルアルミナと人工気孔構造の進歩により、切り屑の排出性が向上し、焼き付きのリスクを伴わずに高い金属除去率を実現します。

コーティングされた研磨材は、トン数が軽いもの、仕上げとバリ取りで広く使用されています。柔軟なフィルムからファイバーディスクまで、さまざまな裏打ち材が、曲面や届きにくい領域での性能を最適化します。Super-研磨材は現在ニッチな地位を占めていますが、その2桁成長は研磨材市場の将来の方向性を支えています。アディティブ・マニュファクチャリングショップは、従来のホイールがすぐに負荷がかかる薄肉のチタン部品用に、ダイヤモンドパッドとCBNマンドレルを指定しています。Imerys社などのサプライヤーは、ドレッサ間隔を延長するオーダーメイドの溶融アルミナやゾルゲル砥粒を提供し、ボンドホイールの優位性を強化すると同時に、スーパー研磨材との性能ギャップを埋めています。

研磨材市場レポートは、素材(天然研磨材と合成研磨材)、タイプ(ボンド研磨材、コーティング研磨材、スーパー研磨材)、研磨材砥粒/原料(酸化アルミニウム、炭化ケイ素、その他)、エンドユーザー産業(金属製造・加工、自動車・航空宇宙、その他)、地域(アジア太平洋、北米、欧州、南米、中東・アフリカ)。

地域分析

アジア太平洋地域は、中国の大規模な機械加工基盤とインドの加速するインフラ整備を反映して、2024年の世界購入量の56%を占める。国内のEVバッテリー製造と電子機器組立に対する政府の優遇措置が、現地の需要をさらに刺激しています。日本と韓国は、先進的なダイヤモンド半導体研究を活用し、大面積ダイヤモンドウェーハのスライスなど、スーパー研磨材の新たな川下用途を創出します。これらの要因が相まって、アジアのリーダー的地位が維持され、多国籍企業による混合・プレス加工の現地化が促進されます。

北米は、航空宇宙、医療、添加物製造の分野で力強い勢いを維持しています。VOCと粒子状物質の排出に関する規制の監視が、ガーネットブラストメディアと水性クーラントへのシフトを推進し、製品ミックスのアップグレードを生み出しています。

欧州では持続可能性と循環型経済の原則が重視され、サンゴバンのようなサプライヤーはリサイクルボンド・システムを導入して炭素強度を抑制しています。ドイツの精密工学クラスターではスーパー研磨材の採用が加速しており、南欧では建設関連のブラストとカッティングディスクの消費に注力しています。ブラジルの造船所と湾岸の石油化学プロジェクトは、エンドユーザーの多様性の拡大を示しています。ブラジル造船所と湾岸石油化学プロジェクトは、エンドユーザーの多様性の拡大を示しています。現地でのコンバーティングパートナーシップは、グローバルブランドがこれらの地域に浸透し、研磨材市場のグローバルカバレッジを強化するのに役立っています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 航空宇宙産業と自動車産業での用途拡大

- 成長する金属製造・加工産業

- 新興経済圏で高まる製造活動

- 超砥粒を必要とする積層造形後工程

- 精密機械とCNC機械の採用増加

- 市場抑制要因

- 高い生産コストと設備コスト

- 研磨材の厳しい使用規制

- 代替材料または代替方法による代替

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 材料別

- 天然研磨材

- 合成研磨材

- タイプ別

- ボンド研磨材

- コーティング研磨材

- スーパー研磨材

- 砥粒/原料別

- 酸化アルミニウム

- 炭化ケイ素

- セラミックおよびジルコニア・アルミナ

- その他(ガーネットを含む)

- エンドユーザー業界別

- 金属製造・加工

- 自動車・航空宇宙

- エレクトロニクスと半導体

- 建設・インフラ

- 医療機器

- 石油・ガス

- その他(産業機械・農業機械)

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- 3M

- Abrasive Technology

- ARC Abrasives Inc.

- Asahi Diamond Industrial Co. Ltd.

- CUMI

- Deerfos

- Fujimi Incorporated

- Imerys

- Mirka Ltd.

- NORITAKE CO., LIMITED

- Robert Bosch GmbH

- Saint-Gobain

- SAK ABRASIVES LIMITED

- Sia Abrasives Industries AG

- Tyrolit-Schleifmittelwerke Swarovski AG & Co KG