|

|

市場調査レポート

商品コード

1562424

欧州のガスパイプラインインフラ:2030年市場予測- 地域別分析- 事業別、設備別、用途別Europe Gas Pipeline Infrastructure Market Forecast to 2030 - Regional Analysis - by Operation (Transmission and Distribution), Equipment (Pipeline, Compressor Station, Metering Skids, and Others), and Application (Onshore and Offshore) |

||||||

|

|||||||

|

|||||||

| 欧州のガスパイプラインインフラ:2030年市場予測- 地域別分析- 事業別、設備別、用途別 |

|

出版日: 2024年07月04日

発行: The Insight Partners

ページ情報: 英文 89 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

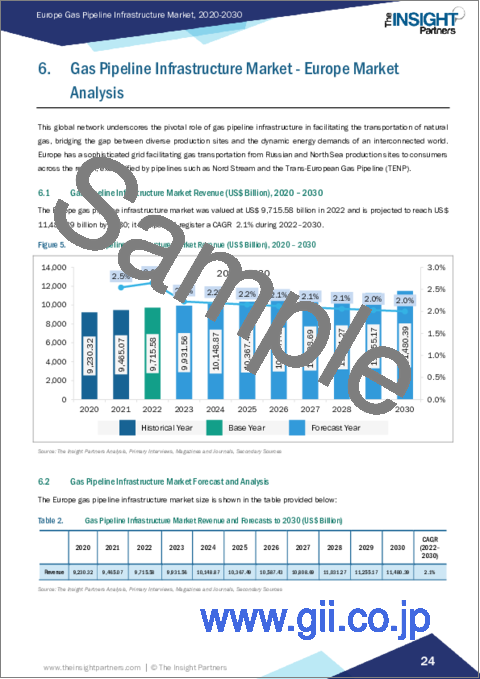

欧州のガスパイプラインインフラ市場は、2022年の9兆7,155億8,000万米ドルから2030年には11兆4,803億9,000万米ドルに成長すると予想されています。2022~2030年のCAGRは2.1%を記録すると推定されます。

再生可能エネルギーとの統合が欧州のガスパイプラインインフラ市場を牽引

再生可能エネルギーとの統合には、天然ガスパイプラインを活用して、太陽光発電や風力発電などの再生可能エネルギーの断続的な性質をサポートすることが含まれます。この統合は、パイプライン事業者が再生可能エネルギー発電事業者と協力し、再生可能エネルギー発電を補完するインフラに投資する機会を記載しています。例えば、ガス火力発電所は、再生可能エネルギーの出力が低い期間にバックアップと送電網の安定性を提供し、化石燃料への依存と二酸化炭素排出を削減することができます。さらに、電気からガスへというような技術の進歩は、余剰の再生可能エネルギーを水素や合成天然ガスに変換することを可能にし、それらは後の使用のためにパイプラインに貯蔵することができます。天然ガスパイプラインを再生可能エネルギー源と統合することで、企業は脱炭素化への取り組みに貢献し、エネルギー安全保障を強化し、よりサステイナブルエネルギーシステムへの移行を支援することができます。

欧州のガスパイプラインインフラ市場概要

ロシア、ドイツ、フランス、スペインは、欧州のガスパイプライン・インフラストラクチャ市場全体の成長を支えている主要国のひとつです。正味炭素排出量ゼロとクリーンエネルギー目標に沿った政府の政策と指令が、ガスパイプラインネットワークを含むサステイナブルインフラへの需要を生み出しています。欧州連合(EU)では、2022年に電力セクターの二酸化炭素排出比率が大幅に上昇しました。数カ国が石炭火力発電所の稼働を再開した一方で、原子力発電所の停止や水力発電量の低下が天然ガスへの依存度を高めました。2015年にフランスのパリで開催された国連気候変動会議(COP21)で196人が参加したパリ協定に沿って、政府はネット・ゼロ・エミッションとグリーン・エネルギー政策を確立しています。電力ミックスと産業部門における低炭素排出エネルギー資源のシェア拡大は、同地域のガスパイプライン・インフラストラクチャ市場の主要な促進要因です。新規パイプラインインフラの開拓と既存ガスパイプラインの能力向上も、予測期間における欧州のガスパイプラインインフラ市場の成長を促進するとみられます。ドイツは2022年末まで、国内の鉱山地帯におけるガス資源の不足により、ガス生産量の伸びが鈍化しました。同国は、米国、イタリア、英国、ノルウェーなど、さまざまな国からの輸入に大きく依存しています。国内生産量はガス消費量のわずか6%に過ぎないため、エネルギー需要の約70%を輸入しています。2023年、ドイツとイタリアの両政府は、ガスパイプラインの建設に合意しました。提案されているパイプラインは3,300kmのプロジェクトで、トランス・オーストリア・ガスライタング、スナム、バイエルネッツ、ドイツのガスコネクトオーストリアを含む、欧州の4つの送電システムオペレーターが組み込まれる予定です。このように、新しいパイプラインの開発と既存のガスネットワークのメンテナンスは、予測期間中にドイツのガスパイプラインインフラの開発を促進すると予想されます。

欧州のガスパイプラインインフラ市場の収益と2030年までの予測(10億米ドル)

欧州のガスパイプラインインフラ市場のセグメンテーション

欧州のガスパイプラインインフラ市場は、事業、設備、用途、国に区分されます。

事業に基づき、欧州のガスパイプラインインフラ市場は送電と配電に二分されます。2022年の欧州のガスパイプラインインフラ市場では、配給セグメントが大きなシェアを占めています。

機器の面では、欧州のガスパイプラインインフラ市場はパイプライン、コンプレッサーステーション、計量スキッド、バルブに分類されます。パイプラインセグメントは2022年に欧州のガスパイプラインインフラ市場で最大のシェアを占めました。

用途別では、欧州のガスパイプラインインフラ市場は陸上と海洋に二分されます。陸上セグメントが2022年の欧州のガスパイプラインインフラ市場でより大きなシェアを占めています。

国別では、欧州のガスパイプラインインフラ市場はドイツ、フランス、イタリア、スペイン、ロシア、英国、その他の欧州に区分されます。その他の欧州が2022年の欧州のガスパイプラインインフラ市場を独占。

Enbridge Inc、Berkshire Hathaway Inc、Kinder Morgan Inc、Beltps、Enagas SA、Saipem SpAなどは、欧州のガスパイプラインインフラ市場で事業を展開する主要企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 ガスパイプラインインフラ市場情勢

- イントロダクション

- エコシステム分析

- 発電

- 送電

- 配給

- エンドユーザー

第5章 欧州のガスパイプラインインフラ市場:主要産業力学

- 市場促進要因

- 天然ガス需要の増加

- 長距離における費用対効果

- 市場抑制要因

- 太陽光や風力による再生可能エネルギー発電への急速な拡大や投資

- 市場機会

- 再生可能エネルギーとの統合

- 市場動向

- オフショアガス産業の発展

- 促進要因と阻害要因の影響

第6章 ガスパイプラインインフラ市場:欧州市場分析

- ガスパイプラインインフラ市場の収益(2020~2030年)

- ガスパイプラインインフラ市場の予測と分析

第7章 欧州のガスパイプラインインフラ市場分析-事業

- イントロダクション

- ガスパイプラインインフラ市場:事業別(2022年、2030年)

- 送電

- 送電市場、収益と2030年までの予測

- 配電

- 配電市場、収益と2030年までの予測

第8章 欧州のガスパイプラインインフラ市場分析:設備

- イントロダクション

- ガスパイプラインインフラ市場:設備別(2022年、2030年)

- パイプライン

- パイプライン概要

- パイプライン市場、収益と2030年までの予測

- バルブ

- バルブ概要

- バルブ市場、収益と2030年までの予測

- コンプレッサーステーション

- コンプレッサーステーション概要

- コンプレッサーステーション市場、収益と2030年までの予測

- 計量スキッド

- 計量スキッド市場、収益と2030年までの予測

第9章 欧州のガスパイプラインインフラ市場分析:用途

- イントロダクション

- ガスパイプラインインフラ市場:用途別(2022年、2030年)

- オンショア

- オンショア

- オンショア市場の収益と2030年までの予測

- オフショア

- オフショア概要

- オフショア市場、収益と2030年までの予測

第10章 欧州のガスパイプラインインフラ市場:国別分析

- 欧州市場概要

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 英国

- その他の欧州

第11章 業界情勢

- イントロダクション

- 市場イニシアティブ

- 合併と買収

第12章 企業プロファイル

- Enbridge Inc

- Berkshire Hathaway Inc

- Kinder Morgan Inc

- Beltps

- Enagas SA

- Saipem SpA

第13章 付録

List Of Tables

- Table 1. Gas Pipeline Infrastructure Market Segmentation

- Table 2. Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Billion)

- Table 3. Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Billion) - Operation

- Table 4. Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Billion) - Equipment

- Table 5. Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Billion) - Application

- Table 6. Europe Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Country

- Table 7. Germany Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Operation

- Table 8. Germany Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Equipment

- Table 9. Germany Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Application

- Table 10. France Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Operation

- Table 11. France Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Equipment

- Table 12. France Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Application

- Table 13. Italy Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Operation

- Table 14. Italy Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Equipment

- Table 15. Italy Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Application

- Table 16. Spain Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Operation

- Table 17. Spain Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Equipment

- Table 18. Spain Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Application

- Table 19. Russia Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Operation

- Table 20. Russia Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Equipment

- Table 21. Russia Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Application

- Table 22. UK Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Operation

- Table 23. UK Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Equipment

- Table 24. UK Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Application

- Table 25. Rest of Europe Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Operation

- Table 26. Rest of Europe Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Equipment

- Table 27. Rest of Europe Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn) - By Application

- Table 28. List of Abbreviation

List Of Figures

- Figure 1. Gas Pipeline Infrastructure Market Segmentation, By Country

- Figure 2. Ecosystem: Gas pipeline infrastructure market

- Figure 3. Gas Pipeline Infrastructure Market - Key Industry Dynamics

- Figure 4. Impact Analysis of Drivers and Restraints

- Figure 5. Gas Pipeline Infrastructure Market Revenue (US$ Billion), 2020 - 2030

- Figure 6. Gas Pipeline Infrastructure Market Share (%) - Operation, 2022 and 2030

- Figure 7. Transmission Market Revenue and Forecasts to 2030 (US$ Billion)

- Figure 8. Distribution Market Revenue and Forecasts to 2030 (US$ Billion)

- Figure 9. Gas Pipeline Infrastructure Market Share (%) - Equipment, 2022 and 2030

- Figure 10. Pipeline Market Revenue and Forecasts to 2030 (US$ Billion)

- Figure 11. Valves Market Revenue and Forecasts to 2030 (US$ Billion)

- Figure 12. Compressor station Market Revenue and Forecasts to 2030 (US$ Billion)

- Figure 13. Metering skids Market Revenue and Forecasts to 2030 (US$ Billion)

- Figure 14. Gas Pipeline Infrastructure Market Share (%) - Application, 2022 and 2030

- Figure 15. Onshore Market Revenue and Forecasts to 2030 (US$ Billion)

- Figure 16. Offshore Market Revenue and Forecasts to 2030 (US$ Billion)

- Figure 17. Europe Gas Pipeline Infrastructure Market, By Key Country - Revenue 2022 (US$ Bn)

- Figure 18. Europe Gas Pipeline Infrastructure Market Breakdown by Country (2022 and 2030)

- Figure 19. Germany Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn)

- Figure 20. France Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn)

- Figure 21. Italy Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn)

- Figure 22. Spain Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn)

- Figure 23. Russia Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn)

- Figure 24. UK Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn)

- Figure 25. Rest of Europe Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn)

The Europe gas pipeline infrastructure market is expected to grow from US$ 9,715.58 billion in 2022 to US$ 11,480.39 billion by 2030. It is estimated to record a CAGR of 2.1% from 2022 to 2030.

Integration with Renewable Energy Drives Europe Gas Pipeline Infrastructure Market

Integration with renewable energy involves leveraging natural gas pipelines to support the intermittent nature of renewable sources such as solar and wind power. This integration offers opportunities for pipeline operators to collaborate with renewable energy developers and invest in infrastructure that complements renewable energy generation. For example, gas-fired power plants can provide backup and grid stability during periods of low renewable energy output, reducing reliance on fossil fuels and carbon emissions. Additionally, advancements in technologies like power-to-gas allow excess renewable energy to be converted into hydrogen or synthetic natural gas, which can be stored in pipelines for later use. By integrating natural gas pipelines with renewable energy sources, companies can contribute to decarbonization efforts, enhance energy security, and support the transition to a more sustainable energy system.

Europe Gas Pipeline Infrastructure Market Overview

Russia, Germany, France, and Spain are some of the major countries aiding to the overall growth of the gas pipeline infrastructure market in Europe. The government policies and mandates in line with the net zero carbon emission and clean energy targets are creating the demand for sustainable infrastructure, including gas pipeline networks. In the European Union, the carbon dioxide ratio in the power sector intensified substantially in 2022. A few countries resumed operations at coal-driven power plants, while outages at nuclear plants and low hydropower production fueled the dependability of natural gas. In line with the Paris Agreement, which involved 196 participants at the UN Climate Change Conference (COP21) in Paris, France, in 2015-the government is establishing net zero emission and green energy policies. The growing share of low-carbon emission energy resources in the power mix and the industrial sector are major driving factors for the gas pipeline infrastructure market in the region. The development of new pipeline infrastructure and the advancement of the capacity of existing gas pipelines are also likely to fuel the growth of the gas pipeline infrastructure market in Europe over the forecast period. Germany experienced slow growth in gas production until the end of 2022 due to the scarcity of gas resources across the country's mining areas. The country relies majorly on imports from different countries, such as the US, Italy, the UK, and Norway. It imports approximately 70% of its energy requirements as its domestic production caters to only ~6% of its gas consumption. In 2023, the governments of Germany and Italy collaborated to form a projected gas pipeline. The proposed pipeline is a 3,300 km project and is anticipated to incorporate four European transmission system operators, including Trans Austria Gasleitung, Snam, Bayernets, and Gas Connect Austria in Germany. Thus, the development of the new pipeline and maintenance of the existing gas network is anticipated to boost the development of gas pipeline infrastructure in Germany over the forecast period.

Europe Gas Pipeline Infrastructure Market Revenue and Forecast to 2030 (US$ Billion)

Europe Gas Pipeline Infrastructure Market Segmentation

The Europe gas pipeline infrastructure market is segmented into operation, equipment, application, and country.

Based on operation, the Europe gas pipeline infrastructure market is bifurcated into transmission and distribution. The distribution segment held a larger share of Europe gas pipeline infrastructure market in 2022.

In terms of equipment, the Europe gas pipeline infrastructure market is categorized into pipeline, compressor station, metering skids, and valves. The pipeline segment held the largest share of Europe gas pipeline infrastructure market in 2022.

Based on application, the Europe gas pipeline infrastructure market is bifurcated into onshore and offshore. The onshore segment held a larger share of Europe gas pipeline infrastructure market in 2022.

Based on country, the Europe gas pipeline infrastructure market is segmented into Germany, France, Italy, Spain, Russia, the UK, and the Rest of Europe. The Rest of Europe dominated the Europe gas pipeline infrastructure market in 2022.

Enbridge Inc, Berkshire Hathaway Inc, Kinder Morgan Inc, Beltps, Enagas SA, and Saipem SpA are some of the leading companies operating in the Europe gas pipeline infrastructure market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Gas Pipeline Infrastructure Market Landscape

- 4.1 Overview

- 4.2 Ecosystem Analysis

- 4.2.1 Production

- 4.2.2 Transmission

- 4.2.3 Distribution

- 4.2.4 End User

5. Europe Gas Pipeline Infrastructure Market - Key Industry Dynamics

- 5.1 Market Drivers

- 5.1.1 Rise in Demand for Natural Gas

- 5.1.2 Cost-Effectiveness Over Long Distances

- 5.2 Market Restraints

- 5.2.1 Rapid Expansion or Investment towards Renewable Power Generation from Solar and Wind

- 5.3 Market Opportunities

- 5.3.1 Integration with Renewable Energy

- 5.4 Market Trends

- 5.4.1 Growing Developments in the Offshore Gas Industry

- 5.5 Impact of Drivers and Restraints:

6. Gas Pipeline Infrastructure Market - Europe Market Analysis

- 6.1 Gas Pipeline Infrastructure Market Revenue (US$ Billion), 2020 - 2030

- 6.2 Gas Pipeline Infrastructure Market Forecast and Analysis

7. Europe Gas Pipeline Infrastructure Market Analysis - Operation

- 7.1 Overview

- 7.2 Gas Pipeline Infrastructure Market, By Operation (2022 and 2030)

- 7.3 Transmission

- 7.3.1 Overview

- 7.3.2 Transmission Market, Revenue and Forecast to 2030 (US$ Billion)

- 7.4 Distribution

- 7.4.1 Overview

- 7.4.2 Distribution Market, Revenue and Forecast to 2030 (US$ Billion)

8. Europe Gas Pipeline Infrastructure Market Analysis - Equipment

- 8.1 Overview

- 8.2 Gas Pipeline Infrastructure Market, By Equipment (2022 and 2030)

- 8.3 Pipeline

- 8.3.1 Overview

- 8.3.2 Pipeline Market, Revenue and Forecast to 2030 (US$ Billion)

- 8.4 Valves

- 8.4.1 Overview

- 8.4.2 Valves Market, Revenue and Forecast to 2030 (US$ Billion)

- 8.5 Compressor station

- 8.5.1 Overview

- 8.5.2 Compressor station Market, Revenue and Forecast to 2030 (US$ Billion)

- 8.6 Metering skids

- 8.6.1 Overview

- 8.6.2 Metering skids Market, Revenue and Forecast to 2030 (US$ Billion)

9. Europe Gas Pipeline Infrastructure Market Analysis - Application

- 9.1 Overview

- 9.2 Gas Pipeline Infrastructure Market, By Application (2022 and 2030)

- 9.3 Onshore

- 9.3.1 Overview

- 9.3.2 Onshore Market, Revenue and Forecast to 2030 (US$ Billion)

- 9.4 Offshore

- 9.4.1 Overview

- 9.4.2 Offshore Market, Revenue and Forecast to 2030 (US$ Billion)

10. Europe Gas Pipeline Infrastructure Market - Country Analysis

- 10.1 Europe Market Overview

- 10.1.1 Europe Gas Pipeline Infrastructure Market, By Key Country - Revenue 2022 (US$ Bn)

- 10.1.2 Europe Gas Pipeline Infrastructure Market Revenue and Forecasts and Analysis - By Country

- 10.1.2.1 Europe Gas Pipeline Infrastructure Market Revenue and Forecasts and Analysis - By Country

- 10.1.2.2 Germany Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn)

- 10.1.2.2.1 Germany Gas Pipeline Infrastructure Market Breakdown by Operation

- 10.1.2.2.2 Germany Gas Pipeline Infrastructure Market Breakdown by Equipment

- 10.1.2.2.3 Germany Gas Pipeline Infrastructure Market Breakdown by Application

- 10.1.2.3 France Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn)

- 10.1.2.3.1 France Gas Pipeline Infrastructure Market Breakdown by Operation

- 10.1.2.3.2 France Gas Pipeline Infrastructure Market Breakdown by Equipment

- 10.1.2.3.3 France Gas Pipeline Infrastructure Market Breakdown by Application

- 10.1.2.4 Italy Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn)

- 10.1.2.4.1 Italy Gas Pipeline Infrastructure Market Breakdown by Operation

- 10.1.2.4.2 Italy Gas Pipeline Infrastructure Market Breakdown by Equipment

- 10.1.2.4.3 Italy Gas Pipeline Infrastructure Market Breakdown by Application

- 10.1.2.5 Spain Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn)

- 10.1.2.5.1 Spain Gas Pipeline Infrastructure Market Breakdown by Operation

- 10.1.2.5.2 Spain Gas Pipeline Infrastructure Market Breakdown by Equipment

- 10.1.2.5.3 Spain Gas Pipeline Infrastructure Market Breakdown by Application

- 10.1.2.6 Russia Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn)

- 10.1.2.6.1 Russia Gas Pipeline Infrastructure Market Breakdown by Operation

- 10.1.2.6.2 Russia Gas Pipeline Infrastructure Market Breakdown by Equipment

- 10.1.2.6.3 Russia Gas Pipeline Infrastructure Market Breakdown by Application

- 10.1.2.7 UK Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn)

- 10.1.2.7.1 UK Gas Pipeline Infrastructure Market Breakdown by Operation

- 10.1.2.7.2 UK Gas Pipeline Infrastructure Market Breakdown by Equipment

- 10.1.2.7.3 UK Gas Pipeline Infrastructure Market Breakdown by Application

- 10.1.2.8 Rest of Europe Gas Pipeline Infrastructure Market Revenue and Forecasts to 2030 (US$ Bn)

- 10.1.2.8.1 Rest of Europe Gas Pipeline Infrastructure Market Breakdown by Operation

- 10.1.2.8.2 Rest of Europe Gas Pipeline Infrastructure Market Breakdown by Equipment

- 10.1.2.8.3 Rest of Europe Gas Pipeline Infrastructure Market Breakdown by Application

11. Industry Landscape

- 11.1 Overview

- 11.2 Market Initiative

- 11.3 Mergers & Acquisitions

12. Company Profiles

- 12.1 Enbridge Inc

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Berkshire Hathaway Inc

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 Kinder Morgan Inc

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Beltps

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Enagas SA

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 Saipem SpA

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

13. Appendix

- 13.1 About the Insight Partners

- 13.2 Word Index