|

|

市場調査レポート

商品コード

1562253

アジア太平洋のトランスフェクション試薬・機器:2030年までの市場予測 - 地域分析 - 製品、手法、用途、エンドユーザー別Asia Pacific Transfection Reagents and Equipment Market Forecast to 2030 - Regional Analysis - by Product, Method, Application, and End User |

||||||

|

|||||||

|

|||||||

| アジア太平洋のトランスフェクション試薬・機器:2030年までの市場予測 - 地域分析 - 製品、手法、用途、エンドユーザー別 |

|

出版日: 2024年07月04日

発行: The Insight Partners

ページ情報: 英文 122 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

アジア太平洋のトランスフェクション試薬・機器市場は、2022年に2億2,223万米ドルと評価され、2030年には4億1,429万米ドルに達すると予測され、2022年から2030年までのCAGRは8.1%と推定されます。

がんの経済的負担の増大がアジア太平洋のトランスフェクション試薬・機器市場を押し上げる

世界保健機関(WHO)によると、がんは世界の主要死因の1つであり、2020年の死亡者数は1,000万人に達します。国際がん研究機関によると、2040年までに3,020万人の症例が追加され、世界のがん負担は増加する可能性が高いです。乳がん機構によると、世界の乳がん患者の約5~10%は遺伝性で、代々受け継がれた異常遺伝子が原因です。2023年にInternational Journal of Epidemiologyに掲載された論文「Lifestyle, Genetic Risk and Incidence of Cancer」によると、発生するがん疾患の33%近くが遺伝性であり、遺伝子変異のリスクが高い疾患です。それゆえ、人々は遺伝性がんの早期発見と個別化治療のために遺伝子プロファイリングを選択しています。BRCA1とBRCA2は腫瘍抑制遺伝子と呼ばれることもあります。これらの遺伝子の有害な変異体を受け継ぐ人は、いくつかのがん、特に乳がんと卵巣がんのリスクが高いです。また、これらの人々は、当該遺伝子に変異を持たない人々に比べ、若い年齢でがんを発症する傾向があります。がん細胞による核酸プロセッシングに焦点を当てた研究は、がんの代謝を理解するのに役立つと思われます。DNAは通常、ウイルスまたは非ウイルス性の粒子にパッケージされ、トランスフェクションされる細胞内に導入されます。遺伝子導入は、難治性がんや転移性がんの治療において、抗腫瘍薬の効果を高める新しいアプローチとして提案されています。肺がん、大腸がん、膵臓がん、膀胱がん、乳がんなどでは、遺伝子治療と薬剤の併用(類似療法)によって、従来の治療法の抗増殖効果が増強されることが報告されています。このように、がんの経済的負担の増大は、アジア太平洋のトランスフェクション試薬・機器市場を強化しています。

アジア太平洋トランスフェクション試薬・機器市場概要

アジア太平洋は、中国、日本、インド、韓国、オーストラリア、その他アジア太平洋に分類されます。2022年には中国が最大の市場シェアを占める。中国、インド、シンガポールなどのアジア太平洋諸国は、ヘルスケアシステムが確立されており、製薬・医療産業も急成長しています。これらの国々には、がん患者に治療やケアサービスを提供するヘルスケア施設が数多くあります。NIHの調査によると、中国のがん病院における年間入院患者数は2010年から2020年の間に110万人から324万人に増加しました。2023年にJournal of the American Medical Associationに発表された研究によると、中国本土の18歳以上の慢性腎臓病(CKD)有病率は8.2%です。さらに、国際がん研究機関(IARC)の最新データによると、中国における胃がんの推定年齢標準化率(ASR)は10万人当たり21人、粗率は33.06、膵臓がんのASRは10万人当たり5人、粗率は8.6です。同じ出典によると、2020年における0~74歳の胃がんと膵臓がんの新規患者数(男女とも)は、それぞれ47万8,508人と12万4,994人と推定されています。このように、慢性疾患の負担が大きいことは、中国におけるCGTの需要を促進し、ひいてはトランスフェクション試薬・機器市場の成長に拍車をかけています。

アジア太平洋トランスフェクション試薬・機器市場の収益と2030年までの予測(金額)

アジア太平洋のトランスフェクション試薬・機器市場のセグメンテーション

アジア太平洋のトランスフェクション試薬・機器市場は、製品、手法、用途、エンドユーザー、国によって区分されます。

製品別では、アジア太平洋のトランスフェクション試薬・機器市場は試薬と機器に二分されます。試薬セグメントは2022年に大きなシェアを占めました。

手法別では、アジア太平洋のトランスフェクション試薬・機器市場は、ウイルス性手法、非ウイルス性手法、ハイブリッド手法に区分されます。2022年には非ウイルス法が最大のシェアを占めています。ウイルス法は、レトロウイルス、アデノウイルス、アデノ関連ウイルス、ヘルペスウイルスに分類されます。非ウイルス性セグメントは、物理的/機械的方法と化学的方法に二分されます。さらに、物理的/機械的方法は、エレクトロポレーション法、マイクロインジェクション法、バイオリスティック法、レーザー法、マグネトフェクション法、ソノポレーション法に細分化されます。また、化学的方法セグメントは、リポソームベース/高脂質ベースと非リポソーム/高脂質ベースに細分化されます。

用途別では、アジア太平洋のトランスフェクション試薬・機器市場は、生物医学研究、タンパク質生産、治療デリバリーに区分されます。バイオメディカル研究セグメントが2022年に最大のシェアを占めました。

エンドユーザー別では、アジア太平洋のトランスフェクション試薬・機器市場は学術・研究機関と製薬・バイオテクノロジー企業に二分されます。2022年には、学術・研究機関セグメントがより大きなシェアを占めています。

国別に見ると、アジア太平洋のトランスフェクション試薬・機器市場は、オーストラリア、中国、インド、日本、韓国、その他アジア太平洋に分類されます。中国が2022年のアジア太平洋トランスフェクション試薬・機器市場を独占しました。

Fisher Scientific Inc、Promega Corp、F. Hoffmann-La Roche Ltd、Bio-Rad Laboratories Inc、Mirus Bio LLC、QIAGEN NV、Merck KGaA、Lonza Group AG、MaxCyte Inc、Polyplus-Transfection SAは、アジア太平洋トランスフェクション試薬・機器市場で事業を展開する主要企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要な洞察

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 アジア太平洋のトランスフェクション試薬・機器市場-主要市場力学

- アジア太平洋のトランスフェクション試薬・機器市場:主要市場力学

- 市場促進要因

- 細胞治療と遺伝子治療の人気の高まり

- がんの経済的負担の増大

- 市場抑制要因

- 機器および消耗品の高コスト

- 市場機会

- 小規模プロセスから大規模プロセスへの拡大

- 今後の動向

- 企業の戦略的取り組み

- 促進要因と抑制要因の影響

第5章 トランスフェクション試薬・機器市場:アジア太平洋市場分析

- アジア太平洋のトランスフェクション試薬・機器市場の収益、2022年~2030年

- アジア太平洋のトランスフェクション試薬・機器市場予測分析

第6章 アジア太平洋のトランスフェクション試薬・機器市場分析:製品別

- 試薬

- 装置

第7章 アジア太平洋のトランスフェクション試薬・機器市場分析:モダリティ別

- ウイルス

- 非ウイルス

- ハイブリッド

第8章 アジア太平洋のトランスフェクション試薬・機器市場分析:用途別

- 生物医学研究

- タンパク質生産

- 治療デリバリー

第9章 アジア太平洋のトランスフェクション試薬・機器市場分析:エンドユーザー別

- 学術・研究機関

- 製薬・バイオテクノロジー企業

第10章 アジア太平洋のトランスフェクション試薬・機器市場:国別分析

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋

第11章 トランスフェクション試薬・機器市場:業界情勢

- トランスフェクション試薬・機器市場における成長戦略、2020~2023年

- 無機的成長戦略

- 有機的成長戦略

第12章 企業プロファイル

- Thermo Fisher Scientific Inc

- Promega Corp

- F. Hoffmann-La Roche Ltd

- Bio-Rad Laboratories Inc

- Mirus Bio LLC

- QIAGEN NV

- Merck KGaA

- Lonza Group AG

- MaxCyte Inc

第13章 付録

List Of Tables

- Table 1. Asia Pacific Transfection Reagents and Equipment Market Segmentation

- Table 2. Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Table 3. Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million) - by Product

- Table 4. Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million) - by Modality

- Table 5. Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million) - by Viral

- Table 6. Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million) - by Non-Viral

- Table 7. Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million) - by Physical/mechanical Method

- Table 8. Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million) - by Chemical Method

- Table 9. Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million) - by Application

- Table 10. Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million) - by End Users

- Table 11. Asia Pacific: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Country

- Table 12. China: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Product

- Table 13. China: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Modality

- Table 14. China: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Viral

- Table 15. China: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Non-Viral

- Table 16. China: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Physical/mechanical Method

- Table 17. China: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Chemical Method

- Table 18. China: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Application

- Table 19. China: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by End Users

- Table 20. Japan: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Product

- Table 21. Japan: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Modality

- Table 22. Japan: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Viral

- Table 23. Japan: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Non-Viral

- Table 24. Japan: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Physical/mechanical Method

- Table 25. Japan: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Chemical Method

- Table 26. Japan: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Application

- Table 27. Japan: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by End Users

- Table 28. India: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Product

- Table 29. India: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Modality

- Table 30. India: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Viral

- Table 31. India: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Non-Viral

- Table 32. India: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Physical/mechanical Method

- Table 33. India: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Chemical Method

- Table 34. India: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Application

- Table 35. India: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by End Users

- Table 36. South Korea: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Product

- Table 37. South Korea: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Modality

- Table 38. South Korea: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Viral

- Table 39. South Korea: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Non-Viral

- Table 40. South Korea: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Physical/mechanical Method

- Table 41. South Korea: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Chemical Method

- Table 42. South Korea: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Application

- Table 43. South Korea: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by End Users

- Table 44. Australia: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Product

- Table 45. Australia: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Modality

- Table 46. Australia: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Viral

- Table 47. Australia: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Non-Viral

- Table 48. Australia: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Physical/mechanical Method

- Table 49. Australia: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Chemical Method

- Table 50. Australia: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Application

- Table 51. Australia: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by End Users

- Table 52. Rest of Asia Pacific: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Product

- Table 53. Rest of Asia Pacific: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Modality

- Table 54. Rest of Asia Pacific: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Viral

- Table 55. Rest of Asia Pacific: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Non-Viral

- Table 56. Rest of Asia Pacific: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Physical/mechanical Method

- Table 57. Rest of Asia Pacific: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Chemical Method

- Table 58. Rest of Asia Pacific: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by Application

- Table 59. Rest of Asia Pacific: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million) - by End Users

- Table 60. Recent Inorganic Growth Strategies in the Transfection Reagents and Equipment Market

- Table 61. Recent Organic Growth Strategies in The Transfection Reagents and Equipment Market

List Of Figures

- Figure 1. Asia Pacific Transfection Reagents and Equipment Market Segmentation, by Country

- Figure 2. Impact Analysis of Drivers and Restraints

- Figure 3. Asia Pacific Transfection Reagents and Equipment Market Revenue (US$ Million), 2022-2030

- Figure 4. Asia Pacific Transfection Reagents and Equipment Market Share (%) - by Product (2022 and 2030)

- Figure 5. Reagents: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 6. Equipment: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 7. Asia Pacific Transfection Reagents and Equipment Market Share (%) - by Modality (2022 and 2030)

- Figure 8. Viral: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 9. Retrovirus: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 10. Adenovirus: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 11. Adeno-Associated Virus: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 12. Herpes Virus: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 13. Non-Viral: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 14. Physical/Mechanical: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 15. Electroporation: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 16. Microinjection: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 17. Biolistic Method: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 18. Laser Method: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 19. Magnetofection: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 20. Sonoporation: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 21. Chemical Method: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 22. Liposomal Based/High Lipid: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 23. Non-Liposomal Based/High Lipid: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 24. Hybrid: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 25. Asia Pacific Transfection Reagents and Equipment Market Share (%) - by Application (2022 and 2030)

- Figure 26. Biomedical Research: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 27. Protein Production: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 28. Therapeutic Delivery: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 29. Asia Pacific Transfection Reagents and Equipment Market Share (%) - by End Users (2022 and 2030)

- Figure 30. Academic and Research Institutes: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 31. Pharmaceutical and Biotechnological Companies: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 32. Asia Pacific: Transfection Reagents and Equipment Market- Revenue by Key Countries 2022 (US$ Million)

- Figure 33. Asia Pacific: Transfection Reagents and Equipment Market Breakdown, by Key Countries, 2022 and 2030 (%)

- Figure 34. China: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million)

- Figure 35. Japan: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million)

- Figure 36. India: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million)

- Figure 37. South Korea: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million)

- Figure 38. Australia: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million)

- Figure 39. Rest of Asia Pacific: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030(US$ Million)

- Figure 40. Growth Strategies in The Transfection Reagents and Equipment Market, 2020-2023

The Asia Pacific transfection reagents and equipment market was valued at US$ 222.23 million in 2022 and is expected to reach US$ 414.29 million by 2030; it is estimated to register at a CAGR of 8.1% from 2022 to 2030.

Growing Economic Burden of Cancer Boosts Asia Pacific Transfection Reagents and Equipment Market

According to the World Health Organization (WHO), cancer is one of the leading causes of death worldwide, and it accounted for ~10 million deaths in 2020. As per the International Agency for Research on Cancer, the global cancer burden is likely to increase with the addition of 30.2 million more cases by 2040. According to the Breast Cancer Organization, approximately 5-10% of breast cancer cases worldwide are hereditary and are caused by abnormal genes passed from generations. According to the article "Lifestyle, Genetic Risk and Incidence of Cancer," published in the International Journal of Epidemiology in 2023, nearly 33% of cancer conditions that occur are hereditary, and the risk of genetic mutations is high in the disease. Hence, people are opting for genetic profiling for the early detection and personalized treatment of hereditary cancer cases. BRCA1 and BRCA2 are sometimes referred to as tumor suppressor genes. People who inherit the harmful variants of one of these genes are at a greater risk of several cancers, most notably breast and ovarian cancer, among other types. These people also tend to develop cancer at younger ages compared to people who do not have variations in the said genes. Studies focused on nucleic acid processing by cancer cells are likely to help understand cancer metabolism. DNA is typically packaged into a viral or non-viral particle to be transferred into the cell that is to be transfected. Gene transfer has been proposed as a new approach to enhance the effectiveness of antitumor drugs in treating intractable or metastatic cancers. The association of gene therapy and drugs (similar therapy) has been reported to strengthen the antiproliferative effects of classical treatments in lung, colorectal, pancreatic, bladder, and breast cancers, among others. Thus, the elevating economic burden of cancer bolsters the Asia Pacific transfection reagents and equipment market.

Asia Pacific Transfection Reagents and Equipment Market Overview

The Asia Pacific region is classified into China, Japan, India, South Korea, Australia and rest of Asia Pacific. China holds the largest market share in the year 2022. Asia Pacific countries such as China, India, Singapore and more with a well-established healthcare system as well as fast-growing pharmaceutical and medical industries. These countries have many healthcare facilities providing treatment and care services to cancer patients. According to an NIH study, yearly patient admissions in cancer hospitals in China climbed from 1.10 million to 3.24 million during 2010-2020. According to a study published in 2023 in the Journal of the American Medical Association, chronic kidney disease (CKD) prevalence in people aged 18 years or older in Mainland China is recorded at 8.2%. Moreover, the latest data from the International Agency for Research on Cancer (IARC) indicates that the estimated age-standardized rate (ASR) for stomach cancer in China is 21 per 100,000, and the crude rate is 33.06; for pancreatic cancer, the ASR is 5 per 100,000 with the crude rate of 8.6. As per the same source, the estimated number of new cases of stomach cancer and pancreatic cancer in people aged 0-74 in 2020 (for both sexes) was 478,508 and 124,994, respectively. Thus, the high burden of chronic diseases propels the demand for CGTs in China, in turn, fueling the transfection reagents and equipment market growth.

Asia Pacific Transfection Reagents and Equipment Market Revenue and Forecast to 2030 (US$ Million)

Asia Pacific Transfection Reagents and Equipment Market Segmentation

The Asia Pacific transfection reagents and equipment market is segmented based on product, method, application, end user, and country.

Based on product, the Asia Pacific transfection reagents and equipment market is bifurcated into reagents and instruments. The reagents segment held a larger share in 2022.

In terms of method, the Asia Pacific transfection reagents and equipment market is segmented into viral methods, non-viral methods, and hybrid methods. The non-viral methods segment held the largest share in 2022. The viral segment is subcategorized into retrovirus, adenovirus, adeno associated virus, and herpes virus. The non-viral segment is bifurcated into physical/mechanical method and chemical method. Further, the physical/mechanical method segment is subcategorized into electroporation, microinjection, biolistic method, laser method, magnetofection, and sonoporation. Also, the chemical method segment is subcategorized into liposomal based/high lipid and non-liposomal/high lipid based.

By application, the Asia Pacific transfection reagents and equipment market is segmented into biomedical research, protein production, and therapeutic delivery. The biomedical research segment held the largest share in 2022.

Based on end user, the Asia Pacific transfection reagents and equipment market is bifurcated into academics & research institutes and pharmaceutical & biotechnology companies. The academics & research institutes segment held a larger share in 2022.

Based on country, the Asia Pacific transfection reagents and equipment market is categorized into Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific transfection reagents and equipment market in 2022.

Fisher Scientific Inc, Promega Corp, F. Hoffmann-La Roche Ltd, Bio-Rad Laboratories Inc, Mirus Bio LLC, QIAGEN NV, Merck KGaA, Lonza Group AG, MaxCyte Inc, and Polyplus-Transfection SA are some of the leading companies operating in the Asia Pacific transfection reagents and equipment market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Asia Pacific Transfection Reagents and Equipment Market - Key Market Dynamics

- 4.1 Asia Pacific Transfection Reagents and Equipment Market - Key Market Dynamics

- 4.2 Market Drivers

- 4.2.1 Increasing Popularity of Cell and Gene Therapy

- 4.2.2 Growing Economic Burden of Cancer

- 4.3 Market Restraints

- 4.3.1 High Cost of Instruments and Consumables

- 4.4 Market Opportunities

- 4.4.1 Ramping Up Small-Scale Processes to Large-Scale Processes

- 4.5 Future Trends

- 4.5.1 Strategic Initiatives by Companies

- 4.6 Impact of Drivers and Restraints:

5. Transfection Reagents and Equipment Market - Asia Pacific Market Analysis

- 5.1 Asia Pacific Transfection Reagents and Equipment Market Revenue (US$ Million), 2022-2030

- 5.2 Asia Pacific Transfection Reagents and Equipment Market Forecast Analysis

6. Asia Pacific Transfection Reagents and Equipment Market Analysis - by Product

- 6.1 Reagents

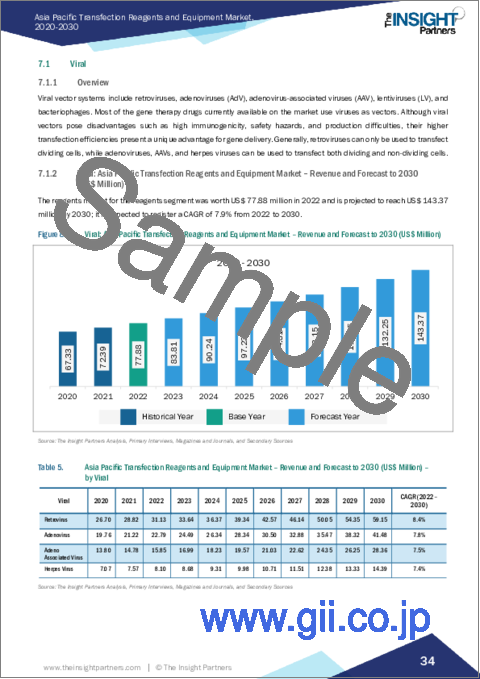

- 6.1.1 Overview

- 6.1.2 Reagents: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 6.2 Equipment

- 6.2.1 Overview

- 6.2.2 Equipment: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

7. Asia Pacific Transfection Reagents and Equipment Market Analysis - by Modality

- 7.1 Viral

- 7.1.1 Overview

- 7.1.2 Viral: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.1.2.1 Retrovirus: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.1.2.2 Adenovirus: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.1.2.3 Adeno-Associated Virus: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.1.2.4 Herpes Virus: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2 Non-Viral

- 7.2.1 Overview

- 7.2.2 Non-Viral: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2.2.1 Physical/Mechanical Method: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2.2.1.1 Electroporation: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2.2.1.2 Microinjection: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2.2.1.3 Biolistic Method: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2.2.1.4 Laser Method: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2.2.1.5 Magnetofection: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2.2.1.6 Sonoporation: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2.2.2 Chemical Method: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2.2.2.1 Liposomal Based/High Lipid: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2.2.2.2 Non-Liposomal Based/High Lipid: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2.2.1 Physical/Mechanical Method: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 7.3 Hybrid

- 7.3.1 Overview

- 7.3.2 Hybrid: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

8. Asia Pacific Transfection Reagents and Equipment Market Analysis - by Application

- 8.1 Biomedical Research

- 8.1.1 Overview

- 8.1.2 Biomedical Research: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 8.2 Protein Production

- 8.2.1 Overview

- 8.2.2 Protein Production: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 8.3 Therapeutic Delivery

- 8.3.1 Overview

- 8.3.2 Therapeutic Delivery: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

9. Asia Pacific Transfection Reagents and Equipment Market Analysis - by End Users

- 9.1 Academic and Research Institutes

- 9.1.1 Overview

- 9.1.2 Academic and Research Institutes: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 9.2 Pharmaceutical and Biotechnological Companies

- 9.2.1 Overview

- 9.2.2 Pharmaceutical and Biotechnological Companies: Asia Pacific Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

10. Asia Pacific Transfection Reagents and Equipment Market -Country Analysis

- 10.1 Asia Pacific: Transfection Reagents and Equipment Market - Revenue and Forecast Analysis - by Country

- 10.1.1 Asia Pacific: Transfection Reagents and Equipment Market - Revenue and Forecast Analysis - by Country

- 10.1.1.1 China: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.1.1 China: Transfection Reagents and Equipment Market Breakdown, by Product

- 10.1.1.1.2 China: Transfection Reagents and Equipment Market Breakdown, by Modality

- 10.1.1.1.2.1 China: Transfection Reagents and Equipment Market Breakdown, by Viral

- 10.1.1.1.2.2 China: Transfection Reagents and Equipment Market Breakdown, by Non-Viral

- 10.1.1.1.2.2.1 China: Transfection Reagents and Equipment Market Breakdown, by Physical/mechanical Method

- 10.1.1.1.2.2.2 China: Transfection Reagents and Equipment Market Breakdown, by Chemical Method

- 10.1.1.1.3 China: Transfection Reagents and Equipment Market Breakdown, by Application

- 10.1.1.1.4 China: Transfection Reagents and Equipment Market Breakdown, by End Users

- 10.1.1.2 Japan: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.2.1 Japan: Transfection Reagents and Equipment Market Breakdown, by Product

- 10.1.1.2.2 Japan: Transfection Reagents and Equipment Market Breakdown, by Modality

- 10.1.1.2.2.1 Japan: Transfection Reagents and Equipment Market Breakdown, by Viral

- 10.1.1.2.2.2 Japan: Transfection Reagents and Equipment Market Breakdown, by Non-Viral

- 10.1.1.2.2.2.1 Japan: Transfection Reagents and Equipment Market Breakdown, by Physical/mechanical Method

- 10.1.1.2.2.2.2 Japan: Transfection Reagents and Equipment Market Breakdown, by Chemical Method

- 10.1.1.2.3 Japan: Transfection Reagents and Equipment Market Breakdown, by Application

- 10.1.1.2.4 Japan: Transfection Reagents and Equipment Market Breakdown, by End Users

- 10.1.1.3 India: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.3.1 India: Transfection Reagents and Equipment Market Breakdown, by Product

- 10.1.1.3.2 India: Transfection Reagents and Equipment Market Breakdown, by Modality

- 10.1.1.3.2.1 India: Transfection Reagents and Equipment Market Breakdown, by Viral

- 10.1.1.3.2.2 India: Transfection Reagents and Equipment Market Breakdown, by Non-Viral

- 10.1.1.3.2.2.1 India: Transfection Reagents and Equipment Market Breakdown, by Physical/mechanical Method

- 10.1.1.3.2.2.2 India: Transfection Reagents and Equipment Market Breakdown, by Chemical Method

- 10.1.1.3.3 India: Transfection Reagents and Equipment Market Breakdown, by Application

- 10.1.1.3.4 India: Transfection Reagents and Equipment Market Breakdown, by End Users

- 10.1.1.4 South Korea: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.4.1 South Korea: Transfection Reagents and Equipment Market Breakdown, by Product

- 10.1.1.4.2 South Korea: Transfection Reagents and Equipment Market Breakdown, by Modality

- 10.1.1.4.2.1 South Korea: Transfection Reagents and Equipment Market Breakdown, by Viral

- 10.1.1.4.2.2 South Korea: Transfection Reagents and Equipment Market Breakdown, by Non-Viral

- 10.1.1.4.2.2.1 South Korea: Transfection Reagents and Equipment Market Breakdown, by Physical/mechanical Method

- 10.1.1.4.2.2.2 South Korea: Transfection Reagents and Equipment Market Breakdown, by Chemical Method

- 10.1.1.4.3 South Korea: Transfection Reagents and Equipment Market Breakdown, by Application

- 10.1.1.4.4 South Korea: Transfection Reagents and Equipment Market Breakdown, by End Users

- 10.1.1.5 Australia: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.5.1 Australia: Transfection Reagents and Equipment Market Breakdown, by Product

- 10.1.1.5.2 Australia: Transfection Reagents and Equipment Market Breakdown, by Modality

- 10.1.1.5.2.1 Australia: Transfection Reagents and Equipment Market Breakdown, by Viral

- 10.1.1.5.2.2 Australia: Transfection Reagents and Equipment Market Breakdown, by Non-Viral

- 10.1.1.5.2.2.1 Australia: Transfection Reagents and Equipment Market Breakdown, by Physical/mechanical Method

- 10.1.1.5.2.2.2 Australia: Transfection Reagents and Equipment Market Breakdown, by Chemical Method

- 10.1.1.5.3 Australia: Transfection Reagents and Equipment Market Breakdown, by Application

- 10.1.1.5.4 Australia: Transfection Reagents and Equipment Market Breakdown, by End Users

- 10.1.1.6 Rest of Asia Pacific: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.6.1 Rest of Asia Pacific: Transfection Reagents and Equipment Market Breakdown, by Product

- 10.1.1.6.2 Rest of Asia Pacific: Transfection Reagents and Equipment Market Breakdown, by Modality

- 10.1.1.6.2.1 Rest of Asia Pacific: Transfection Reagents and Equipment Market Breakdown, by Viral

- 10.1.1.6.2.2 Rest of Asia Pacific: Transfection Reagents and Equipment Market Breakdown, by Non-Viral

- 10.1.1.6.2.2.1 Rest of Asia Pacific: Transfection Reagents and Equipment Market Breakdown, by Physical/mechanical Method

- 10.1.1.6.2.2.2 Rest of Asia Pacific: Transfection Reagents and Equipment Market Breakdown, by Chemical Method

- 10.1.1.6.3 Rest of Asia Pacific: Transfection Reagents and Equipment Market Breakdown, by Application

- 10.1.1.6.4 Rest of Asia Pacific: Transfection Reagents and Equipment Market Breakdown, by End Users

- 10.1.1.1 China: Transfection Reagents and Equipment Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1 Asia Pacific: Transfection Reagents and Equipment Market - Revenue and Forecast Analysis - by Country

11. Transfection Reagents and Equipment Market -Industry Landscape

- 11.1 Overview

- 11.2 Growth Strategies in The Transfection Reagents and Equipment Market, 2020-2023

- 11.3 Inorganic Growth Strategies

- 11.3.1 Overview

- 11.4 Organic Growth Strategies

- 11.4.1 Overview

12. Company Profiles

- 12.1 Thermo Fisher Scientific Inc

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Promega Corp

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 F. Hoffmann-La Roche Ltd

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Bio-Rad Laboratories Inc

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Mirus Bio LLC

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 QIAGEN NV

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 Merck KGaA

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 Lonza Group AG

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 MaxCyte Inc

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

13. Appendix

- 13.1 About Us