|

|

市場調査レポート

商品コード

1819728

アジア太平洋の水素コンプレッサー市場レポート、2017年~2035年:範囲、セグメント、動向、競合分析Asia Pacific Hydrogen Compressor Market Report 2017-2035 by Scope, Segmentation, Dynamics, and Competitive Analysis |

||||||

|

|||||||

|

|||||||

| アジア太平洋の水素コンプレッサー市場レポート、2017年~2035年:範囲、セグメント、動向、競合分析 |

|

出版日: 2025年07月10日

発行: The Insight Partners

ページ情報: 英文 185 Pages

納期: 即納可能

|

概要

アジア太平洋の水素コンプレッサー市場は大きく成長し、2023年の8億4,327万米ドルから2031年までには推定16億9,071万米ドルに達すると予測されています。この成長は、2024年から2035年までのCAGR6.2%に相当します。

エグゼクティブサマリーと市場分析

アジア太平洋の水素コンプレッサー市場は、オーストラリア、韓国、インド、中国、日本、インドネシア、シンガポール、台湾、ニュージーランド、東南アジアなどの主要国に分かれています。この地域の特徴は、インド、中国、タイ、ベトナムなどの新興経済諸国が急速に発展していることであり、これらの諸国は、低い人件費、有利な税制条件、先端技術の採用拡大などの恩恵を受けています。これらの要因は、グローバルメーカーがこの地域に生産施設を設立し、拡大するのに好都合な環境を作り出しています。

アジア太平洋市場では、持続可能なエネルギー源としての水素の可能性を認識し、各社がグリーン水素製造拠点の確立に努めているため、競争が激化しています。国内企業は、大規模プロジェクトで欧米企業との協力関係を強めています。例えば、2021年5月、デンマークの洋上風力発電会社であるOrstedは、洋上風力発電プロジェクトを通じてグリーン水素製造を探求するため、韓国のPOSCOと提携しました。例えばBPは2022年6月、オーストラリアのアジア再生可能エネルギー・ハブ(AREH)プロジェクトの筆頭株主となり、年間最大1.6トンのグリーン水素の生産を目指しています。

150以上の多国籍企業が参加する水素協議会の報告書によると、中国、インド、日本、韓国の水素需要は2050年までに2億8,500万トンに達し、世界全体の43%を占めると予想されています。最大の水素消費国である中国は、グリーン水素製造におけるリーダーシップを積極的に追求しています。グリーン水素の需要の増加は、企業による戦略的パートナーシップの形成や、新興のグリーン水素セクターへの多額の投資を促し、アジア太平洋における水素コンプレッサー市場の成長を促進しています。

石油・ガスセクターの成長も、上流と下流の両方の活動を強化し、これらの産業における水素コンプレッサーの需要を増加させると予想されます。インド、中国、インドネシアなどの国々は、この地域の石油・ガス生産に大きく貢献しています。2023年には、東南アジア政府が新規石油・ガスプロジェクトに160億米ドルを投資し、市場をさらに押し上げます。

市場セグメンテーション

水素コンプレッサー市場は、タイプ別、技術別、エンドユーザー別に区分することができます。

- タイプ別:潤滑コンプレッサーとオイルフリーコンプレッサーに分けられ、2023年には潤滑コンプレッサーの市場シェアが大きくなります。

- 技術別:レシプロ水素コンプレッサー、ダイヤフラムコンプレッサー、非機械式コンプレッサー、その他があり、レシプロコンプレッサーが市場をリードしています。

- エンドユーザー別:主要セグメントには、発電所、石油・ガス、食品・飲料、石油化学・化学産業、水素燃料ステーション、水素貯蔵ソリューションが含まれ、2023年は石油化学・化学セクターが優位を占めました。

市場展望

急速な都市化と産業の成長によりエネルギー需要が急増し、送電網の拡張が必要となっています。新しい電力プロジェクトの増加が、水素コンプレッサーの展開を促進しています。再生可能エネルギーは発電にますます欠かせないものとなっており、国際エネルギー機関(IEA)は、2040年までの世界の電力需要の伸びを年率2.1%と予測しています。東南アジアは、世界でも最も急速に電力需要が伸びており、再生可能エネルギー部門に大きな機会をもたらしています。

この地域で第3位の電力生産国であるインドは、政府の支援や数々の発電イニシアティブを通じて発電能力を拡大しています。例えば、Khargone送電プロジェクトは、主要な火力発電プロジェクトを複数の州に供給する送電システムに接続することを目的としています。このようなエネルギー分野の成長は、水素コンプレッサー市場に大きな機会をもたらすと期待されています。

再生可能エネルギー部門は、政府のイニシアティブと資金提供により投資が増加しており、水素コンプレッサーの採用を促進しています。IEAの報告によると、2023年上半期の再生可能エネルギーへの世界投資は3,580億米ドルに達し、前年比22%増を記録しました。中国がこの投資を牽引し、2023年第1四半期だけで1,770億米ドルを拠出しました。

各国の洞察

アジア太平洋の水素コンプレッサー市場は、世界の製造拠点として台頭してきた中国が支配的です。同国は最大の水素生産国で、年間生産量は3,300万トンです。中国政府は、特に鉄鋼業界においてグリーン水素イニシアチブを積極的に推進しており、これが水素コンプレッサーの需要を促進すると予想されます。2030年までに中国の水素需要は3,500万トンに達すると予測され、市場に大きな影響を与えます。

中国の製造業も拡大しており、製造業への海外直接投資は2023年初頭に6.8%増加しました。同国は発電とインフラに多額の投資を行っており、水素コンプレッサー市場をさらに押し上げています。

企業プロファイル

アジア太平洋の水素コンプレッサー市場の主要企業には、Atlas Copco AB、Burckhardt Compression AG、Fluitron, Inc.、Gardner Denver Nash, LLCなどがあります。これらの企業は、市場での存在感を高め、顧客に革新的なソリューションを提供するために、事業拡大、製品革新、M&Aなどの戦略に注力しています。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

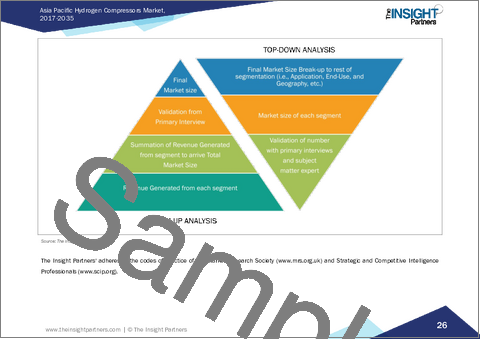

第3章 調査手法

- 2次調査

- 1次調査

- 仮説の策定

- マクロ経済要因分析

- 基礎数値の開発

- データの三角測量

- 国レベルのデータ

第4章 アジア太平洋の水素コンプレッサー市場情勢

- PEST分析

- 水素コンプレッサー市場エコシステム分析

- 水素コンプレッサー市場:水素コンプレッサーサプライヤー一覧

- マーケティングチャネル、流通業者、顧客

- マーケティングチャネル

- 水素コンプレッサー市場:水素コンプレッサー販売業者一覧

- 水素コンプレッサー市場:水素コンプレッサーの顧客一覧

- 水素コンプレッサーの市場価格分析

第5章 アジア太平洋の水素コンプレッサー市場:主要市場力学

- 市場促進要因

- 水素燃料電池自動車の普及拡大

- 石油・ガスセクターへの投資の増加

- 工業生産活動の増加

- 市場抑制要因

- 高いメンテナンス費用

- 市場機会

- 世界の再生可能エネルギーおよび水素発電プロジェクトへの投資の増加

- 今後の動向

- 電気化学式水素コンプレッサー(EHC)の開発

- グリーン水素へのシフトの高まり

- 促進要因と抑制要因の影響

第6章 水素コンプレッサー市場:アジア太平洋市場分析

- アジア太平洋の水素コンプレッサー市場収益、2017年~2035年

- アジア太平洋の水素コンプレッサー市場予測分析

第7章 アジア太平洋の水素コンプレッサー市場分析-タイプ別

- 潤滑式

- オイルフリー

第8章 アジア太平洋の水素コンプレッサー市場分析-技術別

- 往復式水素コンプレッサー

- ダイヤフラム式水素コンプレッサー

- 非機械式水素コンプレッサー

- その他

第9章 アジア太平洋の水素コンプレッサー市場分析-エンドユーザー別

- 発電所

- 石油・ガス

- 食品・飲料

- 石油化学・化学

- 水素充填ステーション

- 水素貯蔵(チューブトレーラー)

- その他

第10章 アジア太平洋の水素コンプレッサー市場:国別分析

- アジア太平洋

- オーストラリア

- 中国

- インド

- 日本

- 韓国

- インドネシア

- シンガポール

- 台湾

- ニュージーランド

- その他の東南アジア諸国

- アジア太平洋のその他諸国

第11章 競合情勢

- ヒートマップ分析:主要企業別

- 企業のポジショニングと集中度

第12章 業界情勢

- 市場イニシアティブ

- 製品開発

- 合併と買収

第13章 企業プロファイル

- Atlas Copco AB

- Burckhardt Compression AG

- Fluitron, Inc.

- Gardner Denver Nash, LLC

- Howden Group

- HAUG Sauer Kompressoren AG

- NEUMAN & ESSER GROUP

- Hydro-Pac, Inc.

- Lenhardt & Wagner GmbH

- PDC Machines Inc.

- Sundyne

- Ariel Corporation