|

|

市場調査レポート

商品コード

1533039

北米のフィルフィニッシュ製造市場:予測(~2030年):地域別分析 - 製品別、モダリティ別、エンドユーザー別North America Fill Finish Manufacturing Market Forecast to 2030 - Regional Analysis - by Product, Modality, and End User |

||||||

|

|||||||

|

|||||||

| 北米のフィルフィニッシュ製造市場:予測(~2030年):地域別分析 - 製品別、モダリティ別、エンドユーザー別 |

|

出版日: 2024年06月05日

発行: The Insight Partners

ページ情報: 英文 98 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

北米のフィルフィニッシュ製造の市場規模は、2022年に34億3,958万米ドルに達し、2022~2030年にかけてCAGR 8.3%で成長し、2030年には65億556万米ドルに達すると予測されています。

非経口投与用プレフィルドシリンジの採用拡大が北米の充填剤製造市場を活性化

非経口投与は、即時の免疫反応を刺激し、医薬品の完全なバイオアベイラビリティを確保するために選択される最も顕著な経路の1つです。非経口薬の開発と市場での入手が着実に増加していることから、投与の容易さを約束する高度でコスト効率の高いドラッグデリバリーデバイスに対する需要が高まっています。従来の送達システムに対するプレフィルドシリンジの利点には、容易な投与、安全性の向上、正確な投与、汚染リスクの低減などがあります。ドラッグデリバリーデバイスの中でも、プレフィルドシリンジは最も急速に成長している一次包装形態の一つであり、投与用に設計されています。過去10年間で、非経口薬(特にいくつかの生物製剤クラスのイントロダクション)の開発が明らかに増加し、その結果プレフィルドシリンジの消費量が約3倍に増加しました。プレフィルドシリンジに対する持続的な嗜好は、これらの製品の安全性と使いやすさに起因しています。最近の製品は、投与ミス、閉塞、液漏れ(i.e.血管外漏出)、静脈の炎症(静脈炎)を軽減するように設計されています。上記のような利点から、いくつかの注射剤-ヒュミラ、エンブレル、アバスチン、プレブナール13、アルプロリックス、ベネフィクスなど-、希釈剤、非経口投与を必要とするその他の製品はプレフィルドシリンジに包装されています。

過去7年間で、北米、欧州、アジア太平洋を含むさまざまな地域で、プレフィルドシリンジ包装の医薬品が約90品目承認されました。薬剤開発の臨床段階にあるいくつかの薬剤は、プレフィルドシリンジとの組み合わせで評価されています。

プレフィルドシリンジへの無菌薬剤の充填は、医薬品製造プロセスにおいて最も重要なステップのひとつと考えられています。薬理学的有効性と品質を維持し、エンドユーザーの安全性を確保するために、適切なフィルフィニッシュ作業は必然的に無菌条件下で実施されます。プレフィルドシリンジ充填は、シリンジ充填量とシリンジに充填された液体とプランジャー底部の間のヘッドスペースの両方を極めて厳密に監視する必要があるため、複雑な作業となります。加えて、低分子原薬の複雑化と生物学的製剤の多様化が、高度な無菌フィルフィニッシュ作業への需要を高めています。

中小企業や大企業を含む企業は、それぞれのフィルフィニッシュ作業を受託サービス業者に委託しています。第10回バイオ医薬品製造能力と生産に関する年次報告書および調査」によると、生物学的製剤メーカーは、フィルフィニッシュ作業の30%以上を外注していることが確認されています。プレフィルドシリンジ需要の増加とフィルフィニッシュ工程の複雑化に伴い、これらの業務のアウトソーシングは今後増加する可能性が高いです。世界中で100社以上がプレフィルドシリンジメーカー向けにフィルフィニッシュサービスを提供しています。医薬品需要の増加に対応するため、サービスプロバイダーは既存のインフラと能力の拡大に積極的に投資しており、過去数年間はサービス契約を通じて顧客層も拡大しています。世界の研究開発パイプラインにある医薬品候補の約55%が注射剤であるため、プレフィルドシリンジメーカーや関連サービスプロバイダーの事業も成長しています。COVID-19危機の出現により、ワクチン開発への取り組みが世界中で活発化し、プレフィルドシリンジの需要を大幅に押し上げました。このように、非経口投与用のプレフィルドシリンジの採用が増加していることが、フィルフィニッシュ製造市場を牽引しています。

北米のフィルフィニッシュ製造の市場概要

米国のフィルフィニッシュ製造市場は、世界最大かつ最も急成長している市場になると予想されます。広範な研究開発活動や革新的なバイオ医薬品・医薬品の高度な製造など、いくつかの要因が市場の成長をもたらしています。市場成長のもう1つの主要因は、全世界におけるバイオ医薬品・医薬品の持続的な多様性と大規模供給です。

バイオ医薬品産業は、国内最大の収益創出セクターのひとつです。2023年には米国で130万人以上の雇用を創出しました。このように、バイオ医薬品産業の成長は、国内の経済全体のバランスを大幅に維持するのに役立っています。年間5億5,000万米ドルの収益を上げています。したがって、研究開発と製品開発の増加は、米国における凍結乾燥サービスの需要を増加させると予想されます。

北米のフィルフィニッシュ製造市場の収益と2030年までの予測(100万米ドル)

北米のフィルフィニッシュ製造市場のセグメンテーション

北米のフィルフィニッシュ製造市場は、製品、モダリティ、エンドユーザー、国に基づいてセグメント化されます。製品に基づき、北米のフィルフィニッシュ製造市場は消耗品と機器に二分されます。消耗品セグメントは2022年に大きな市場シェアを占めました。さらに、消耗品はプレフィルドシリンジ、ガラスバイアル/プラスチックバイアル、カートリッジ、その他に細分化されます。

モダリティ別では、北米のフィルフィニッシュ製造市場は、組換えタンパク質、モノクローナル抗体、ワクチン、細胞療法および生物学的療法、遺伝子療法、その他にセグメント化されます。2022年にはワクチン分野が最大の市場シェアを占めています。

エンドユーザー別では、北米のフィルフィニッシュ製造市場は、受託製造機関、バイオ医薬品企業、その他に区分されます。受託製造機関セグメントが2022年に最大の市場シェアを占めました。

国別に見ると、北米のフィルフィニッシュ製造市場は米国、カナダ、メキシコに区分されます。米国が2022年の北米フィルフィニッシュ製造市場シェアを独占しました。

Becton Dickinson and Co社、Gerresheimer AG社、Groninger and Co GmbH社、IMA Industria Macchine Automatiche SpA社、Maquinaria Industrial Dara SL社、Nipro Medical Europe NV社、NNE AS社、Optima Packaging Group Gmbh社、Schott AG社、SGD SA社、Stevanato Group SpA社、Syntegon Technology GmbH社、West Pharmaceutical Services Inc社は、北米のフィルフィニッシュ製造市場で事業を展開する大手企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要な洞察

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 北米フィルフィニッシュ製造の市場情勢

- 概観

- PEST分析

第5章 北米のフィルフィニッシュ製造市場 - 主要産業力学

- フィルフィニッシュ製造市場:主要産業力学

- 主な市場促進要因

- 非経口投与用プレフィルドシリンジの採用拡大

- 生物製剤に対する需要の高まり

- 主な市場抑制要因

- バイオ医薬品受託製造産業における競合の激化

- 主な市場機会

- 生物製剤の重要なパイプライン

- 主な将来動向

- 無菌フィルフィニッシュ用シングルユースシステム

- 促進要因と抑制要因の影響

第6章 フィルフィニッシュ製造市場:北米市場分析

第7章 北米のフィルフィニッシュ製造市場分析 - 製品

- 消耗品

- 器具

第8章 北米のフィルフィニッシュ製造市場分析 - モダリティ

- 組換えタンパク質

- モノクローナル抗体

- ワクチン

- 細胞治療・生物学的治療

- 遺伝子治療

- その他

第9章 北米のフィルフィニッシュ製造市場分析 - エンドユーザー

- 受託製造機関

- バイオ医薬品企業

- その他

第10章 北米のフィルフィニッシュ製造市場:国別分析

- 米国

- カナダ

- メキシコ

第11章 産業情勢

- フィルフィニッシュ製造市場における成長戦略、2020~2023年

- 無機的成長戦略

- 有機的成長戦略

第12章 企業プロファイル

- IMA Industria Macchine Automatiche SpA

- Nipro Medical Europe NV

- Maquinaria Industrial Dara SL

- Groninger and Co GmbH

- SGD SA

- Optima Packaging Group Gmbh

- NNE AS

- Stevanato Group SpA

- Syntegon Technology GmbH

- West Pharmaceutical Services Inc

- Gerresheimer AG

- Schott AG

- Becton Dickinson and Co

第13章 付録

List Of Tables

- Table 1. Fill Finish Manufacturing Market Segmentation

- Table 2. Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Million) - Product

- Table 3. Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Million) - Consumables

- Table 4. Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Million) - Modality

- Table 5. Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Million) - End User

- Table 6. United States Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Product

- Table 7. United States Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Consumables

- Table 8. United States Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Modality

- Table 9. United States Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 10. Canada Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Product

- Table 11. Canada Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Consumables

- Table 12. Canada Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Modality

- Table 13. Canada Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 14. Mexico Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Product

- Table 15. Mexico Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Consumables

- Table 16. Mexico Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Modality

- Table 17. Mexico Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 18. Recent Inorganic Growth Strategies in the Fill Finish Manufacturing Market

- Table 19. Recent Organic Growth Strategies in the Fill Finish Manufacturing Market

- Table 20. Glossary of Terms, Fill Finish Manufacturing Market

List Of Figures

- Figure 1. Fill Finish Manufacturing Market Segmentation, By Country

- Figure 2. PEST Analysis

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. Fill Finish Manufacturing Market Revenue (US$ Million), 2022 - 2030

- Figure 5. Fill Finish Manufacturing Market Share (%) - Product, 2022 and 2030

- Figure 6. Consumables Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 7. Instruments Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 8. Fill Finish Manufacturing Market Share (%) - Modality, 2022 and 2030

- Figure 9. Recombinant Proteins Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 10. Monoclonal Antibodies Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 11. Vaccines Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 12. Cell Therapies and Biological Therapies Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 13. Gene Therapies Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 14. Others Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 15. Fill Finish Manufacturing Market Share (%) - End User, 2022 and 2030

- Figure 16. Contract Manufacturing Organizations Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 17. Biopharmaceutical Companies Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 18. Others Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 19. North America Fill Finish Manufacturing Market, by Key Countries - Revenue (2022) (US$ Million)

- Figure 20. North America Fill Finish Manufacturing Market Breakdown by Key Countries, 2022 and 2030 (%)

- Figure 21. US Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 22. Canada Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 23. Mexico Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 24. Growth Strategies in the Fill Finish Manufacturing Market, 2020-2023

The North America fill finish manufacturing market was valued at US$ 3,439.58 million in 2022 and is expected to reach US$ 6,505.56 million by 2030; it is estimated to grow at a CAGR of 8.3% from 2022 to 2030 .

Growing Adoption of Prefilled Syringes for Parenteral Administration Fuels North America Fill Finish Manufacturing Market

Parenteral administration is one of the most prominent routes chosen to stimulate immediate immune response and ensure the complete bioavailability of pharmaceutical products. A steady rise in the development and market availability of parenteral drugs has propelled the demand for advanced, cost-effective drug delivery devices that promise ease of administration. The benefits of prefilled syringes over traditional delivery systems include easy administration, improved safety, accurate dosing, and reduced contamination risks. Among drug delivery devices, prefilled syringes represent one of the fastest-growing primary packaging formats, which are designed for dose administration. In the past ten years, there has been an evident increase in the development of parenteral drugs (especially with the introduction of several classes of biologics), which has resulted in approximately three-fold increase in the consumption of prefilled syringes. The sustained preference for the prefilled syringes is attributed to the safety and ease of use of these products. Recent variants are designed with provisions to reduce errors in dosing, risk of occlusions, leakage of fluids (i.e., extravasation), and inflammation of veins (phlebitis). Owing to the benefits mentioned above, several injectable drugs-Humira, Enbrel, Avastin, PREVNAR 13, ALPROLIX, and Benefix, among others-diluents and other products requiring parenteral administration are packaged in prefilled syringes.

Over the past seven years, ~90 drugs have been approved in the prefilled syringe packaging form across different geographies, including North America, Europe, and Asia Pacific. Several drugs in the clinical stages of drug development are being evaluated in combination with prefilled syringes.

The loading of sterile drugs into prefilled syringes is considered one of the most crucial steps in the pharmaceutical production process. Proper fill-finish operations are necessarily carried out under aseptic conditions to maintain pharmacological efficacy and quality and to ensure the safety of end users. The prefilled syringe filling is a complex operation as it requires extremely close monitoring of both the syringe fill volume and the headspace between the liquid filled in the syringe and the bottom of the plunger. In addition, the rise in complexity of small molecule APIs and the increasing diversity of biological drugs contribute to the demand for advanced aseptic fill finish operations.

Companies, including small enterprises and large businesses, outsource their respective fill finish operations to contract service providers. Per the 10th Annual Report and Survey of Biopharmaceutical Manufacturing Capacity and Production, manufacturers of biological have been observed to outsource more than 30% of their fill finish operations. With the rise in the demand for prefilled syringes and the growing complexity of fill finish processes, outsourcing these operations is likely to increase in the future. Over 100 companies across the globe are providing fill finish services for prefilled syringe manufacturers. To cater to the growing demand of pharmaceutical products, service providers are actively investing in expanding their existing infrastructure and capabilities; they have also expanded their clientele through service agreements over the past few years. As injectables account for ~55% of drug candidates in the global R&D pipeline, the businesses of prefilled syringe manufacturers and associated service providers are also growing. Due to the emergence of the COVID-19 crisis, vaccine development initiatives have increased across the globe, which significantly boosted the demand for prefilled syringes. Thus, the rising adoption of prefilled syringes for parenteral administration drives the fill finish manufacturing market.

North America Fill Finish Manufacturing Market Overview

The fill finish manufacturing market in the US is anticipated to be the largest and fastest-growing market in the world. Several factors such as extensive research and development activities and advanced manufacturing of innovative biopharmaceutical and pharmaceutical products lead to the growth of the market. The other leading factor for market growth is sustained diversity and large-scale supply of biopharmaceutical and pharmaceutical products across the globe.

The biopharmaceutical industry is among the largest revenue-generating sector in the country. In 2023, it generated more than 1.3 million jobs in the US. Thus, the growth in the biopharmaceutical industry has assisted in maintaining the total economic balance in the country substantially. It generates ~US$ 550 million in revenue annually. Therefore, it is expected that the rise in research and product development will increase the demand for lyophilization services in the US.

North America Fill Finish Manufacturing Market Revenue and Forecast to 2030 (US$ Million)

North America Fill Finish Manufacturing Market Segmentation

The North America fill finish manufacturing market is segmented based on product, modality, end user, and country. Based on product, the North America fill finish manufacturing market is bifurcated into consumables and instruments. The consumables segment held a larger market share in 2022. Furthermore, the consumables is sub segmented into prefilled syringes, glass vial/plastic vials, cartridges, and others.

In terms of modality, the North America fill finish manufacturing market is segmented into recombinant proteins, monoclonal antibodies, vaccines, cell therapies and biological therapies, gene therapies, and others. The vaccines segment held the largest market share in 2022.

By end user, the North America fill finish manufacturing market is segmented into contract manufacturing organizations, biopharmaceutical companies, and others. The contract manufacturing organizations segment held the largest market share in 2022.

Based on country, the North America fill finish manufacturing market is segmented into the US, Canada, and Mexico. The US dominated the North America fill finish manufacturing market share in 2022.

Becton Dickinson and Co, Gerresheimer AG, Groninger and Co GmbH, IMA Industria Macchine Automatiche SpA, Maquinaria Industrial Dara SL, Nipro Medical Europe NV, NNE AS, Optima Packaging Group Gmbh, Schott AG, SGD SA, Stevanato Group SpA, Syntegon Technology GmbH, and West Pharmaceutical Services Inc are some of the leading players operating in the North America fill finish manufacturing market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. North America Fill Finish Manufacturing Market Landscape

- 4.1 Overview

- 4.2 PEST Analysis

5. North America Fill Finish Manufacturing Market - Key Industry Dynamics

- 5.1 Fill Finish Manufacturing Market - Key Industry Dynamics

- 5.2 Key Market Drivers

- 5.2.1 Growing Adoption of Prefilled Syringes for Parenteral Administration

- 5.2.2 Elevating Demand for Biologics

- 5.3 Key Market Restraints

- 5.3.1 Growing Competition in Biopharmaceutical Contract Manufacturing Industry

- 5.4 Key Market Opportunities

- 5.4.1 Significant Pipeline for Biologics

- 5.5 Key Future Trends

- 5.5.1 Single-Use Systems for Aseptic Fill Finish

- 5.6 Impact of Drivers and Restraints:

6. Fill Finish Manufacturing Market - North America Market Analysis

7. North America Fill Finish Manufacturing Market Analysis - Product

- 7.1 Consumables

- 7.1.1 Overview

- 7.1.2 Consumables Market, Revenue and Forecast to 2030 (US$ Million)

- 7.2 Instruments

- 7.2.1 Overview

- 7.2.2 Instruments Market, Revenue and Forecast to 2030 (US$ Million)

8. North America Fill Finish Manufacturing Market Analysis - Modality

- 8.1 Recombinant Proteins

- 8.1.1 Overview

- 8.1.2 Recombinant Proteins Market, Revenue and Forecast to 2030 (US$ Million)

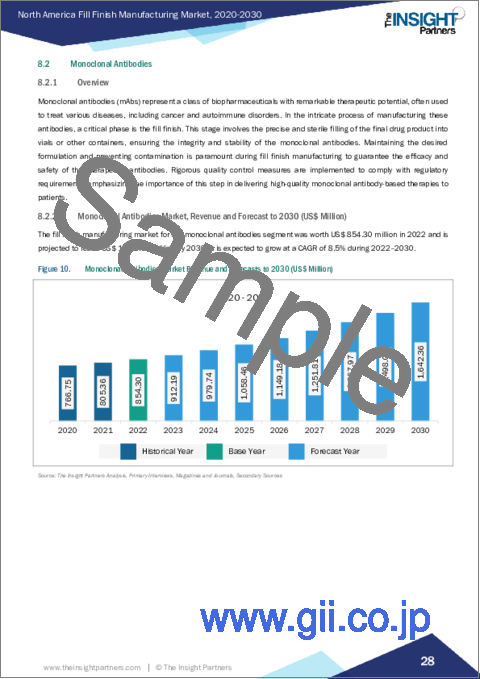

- 8.2 Monoclonal Antibodies

- 8.2.1 Overview

- 8.2.2 Monoclonal Antibodies Market, Revenue and Forecast to 2030 (US$ Million)

- 8.3 Vaccines

- 8.3.1 Overview

- 8.3.2 Vaccines Market, Revenue and Forecast to 2030 (US$ Million)

- 8.4 Cell Therapies and Biological Therapies

- 8.4.1 Overview

- 8.4.2 Cell Therapies and Biological Therapies Market, Revenue and Forecast to 2030 (US$ Million)

- 8.5 Gene Therapies

- 8.5.1 Overview

- 8.5.2 Gene Therapies Market, Revenue and Forecast to 2030 (US$ Million)

- 8.6 Others

- 8.6.1 Overview

- 8.6.2 Others Market, Revenue and Forecast to 2030 (US$ Million)

9. North America Fill Finish Manufacturing Market Analysis - End User

- 9.1 Contract Manufacturing Organizations

- 9.1.1 Overview

- 9.1.2 Contract Manufacturing Organizations Market, Revenue and Forecast to 2030 (US$ Million)

- 9.2 Biopharmaceutical Companies

- 9.2.1 Overview

- 9.2.2 Biopharmaceutical Companies Market, Revenue and Forecast to 2030 (US$ Million)

- 9.3 Others

- 9.3.1 Overview

- 9.3.2 Others Market, Revenue and Forecast to 2030 (US$ Million)

10. North America Fill Finish Manufacturing Market - Country Analysis

- 10.1 North America Fill Finish Manufacturing Market Revenue Forecasts and Analysis - By Country

- 10.1.1 US

- 10.1.1.1 US Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- 10.1.1.2 United States Fill Finish Manufacturing Market Breakdown by Product

- 10.1.1.3 United States Fill Finish Manufacturing Market Breakdown by Consumables

- 10.1.1.4 United States Fill Finish Manufacturing Market Breakdown by Modality

- 10.1.1.5 United States Fill Finish Manufacturing Market Breakdown by End User

- 10.1.2 Canada

- 10.1.2.1 Canada Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- 10.1.2.2 Canada Fill Finish Manufacturing Market Breakdown by Product

- 10.1.2.3 Canada Fill Finish Manufacturing Market Breakdown by Consumables

- 10.1.2.4 Canada Fill Finish Manufacturing Market Breakdown by Modality

- 10.1.2.5 Canada Fill Finish Manufacturing Market Breakdown by End User

- 10.1.3 Mexico

- 10.1.3.1 Mexico Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- 10.1.3.2 Mexico Fill Finish Manufacturing Market Breakdown by Product

- 10.1.3.3 Mexico Fill Finish Manufacturing Market Breakdown by Consumables

- 10.1.3.4 Mexico Fill Finish Manufacturing Market Breakdown by Modality

- 10.1.3.5 Mexico Fill Finish Manufacturing Market Breakdown by End User

- 10.1.1 US

11. Industry Landscape

- 11.1 Overview

- 11.2 Growth Strategies in the Fill Finish Manufacturing Market, 2020-2023

- 11.3 Inorganic Growth Strategies

- 11.3.1 Overview

- 11.4 Organic Growth Strategies

- 11.4.1 Overview

12. Company Profiles

- 12.1 IMA Industria Macchine Automatiche SpA

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Nipro Medical Europe NV

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 Maquinaria Industrial Dara SL

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Groninger and Co GmbH

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 SGD SA

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 Optima Packaging Group Gmbh

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 NNE AS

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Product & Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 Stevanato Group SpA

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 Syntegon Technology GmbH

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

- 12.10 West Pharmaceutical Services Inc

- 12.10.1 Key Facts

- 12.10.2 Business Description

- 12.10.3 Products and Services

- 12.10.4 Financial Overview

- 12.10.5 SWOT Analysis

- 12.10.6 Key Developments

- 12.11 Gerresheimer AG

- 12.11.1 Key Facts

- 12.11.2 Business Description

- 12.11.3 Products and Services

- 12.11.4 Financial Overview

- 12.11.5 SWOT Analysis

- 12.11.6 Key Developments

- 12.12 Schott AG

- 12.12.1 Key Facts

- 12.12.2 Business Description

- 12.12.3 Products and Services

- 12.12.4 Financial Overview

- 12.12.5 SWOT Analysis

- 12.12.6 Key Developments

- 12.13 Becton Dickinson and Co

- 12.13.1 Key Facts

- 12.13.2 Business Description

- 12.13.3 Products and Services

- 12.13.4 Financial Overview

- 12.13.5 SWOT Analysis

- 12.13.6 Key Developments

13. Appendix

- 13.1 About Us

- 13.2 Glossary of Terms