|

|

市場調査レポート

商品コード

1494322

欧州の熱可塑性接着フィルム:2030年市場予測- 地域別分析- 材料、技術、用途、最終用途別Europe Thermoplastic Adhesive Films Market Forecast to 2030 - Regional Analysis - by Material, Technology, Application, and End Use |

||||||

|

|||||||

|

|||||||

| 欧州の熱可塑性接着フィルム:2030年市場予測- 地域別分析- 材料、技術、用途、最終用途別 |

|

出版日: 2024年03月14日

発行: The Insight Partners

ページ情報: 英文 98 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

欧州の熱可塑性接着フィルム市場は、2022年に5億5,504万米ドルと評価され、2030年には8億1,382万米ドルに達すると予測され、2022年から2030年までのCAGRは4.9%で成長すると予測されています。

防弾技術への政府投資の増加が欧州の熱可塑性接着フィルム市場を牽引

安全保障上のリスクの増大と国境警備強化の必要性から、各国政府は防衛と弾道防護への投資を増やしています。各国政府はInnovations for Defense ExcellenceやTechnology Development Fundといったイニシアチブを開始し、軍隊向けの製品イノベーションに資金援助を提供しています。高性能生地は、爆発、爆風、投射物に対する弾道保護に広く使用されています。これらの布地は、高強度、高弾性率、吸音性、衝撃エネルギー吸収性、耐薬品性などの明確な特性を持っています。

高度な複合材料は、芯地や断熱材、車両衝突ガード用保護製品、防護服用弾道パネル、ヘルメットなどの弾道用途にも利用されています。熱可塑性接着フィルムは、先端複合材料や繊維製品の製造に幅広く応用されています。そのため、軍用車両や高性能製品を開発するための防衛分野への政府投資の増加は、予測期間中に熱可塑性接着フィルムメーカーに成長機会をもたらすと期待されています。

欧州の熱可塑性接着フィルム市場概要

自動車は、ドイツ、イタリア、英国を含む欧州諸国のGDPに大きく貢献しており、欧州の主要産業の一つです。欧州委員会の報告によると、欧州の自動車産業が生み出す売上高は、同地域の総GDPの7%を占めています。2022年の国際エネルギー機関の報告によると、2021年には欧州で230万台の電気自動車が販売された(2020年の140万台から増加)。米国商務省の報告書によると、バイエルン自動車やランボルギーニ自動車は複合材料で構成された自動車を生産しており、車両重量の6~8%を占めています。さらに、Mercedes-Benz AG、Bayerische Motoren Werke AG、Audi AG、Volkswagen AGといったドイツの自動車メーカーは、自動車の内外装用途に軽量複合材を利用しています。

金属とプラスチックのハイブリッド部品は、自動車用途に広く使用されています。熱可塑性接着フィルムは、こうしたハイブリッド構造のプラスチックと金属を接着します。2022年に発表された国際貿易局の報告書によると、自動車産業への投資の増加は、電子技術と部品に有利な機会を生み出します。スペイン政府が2020年に発表した報告書によると、同国政府は自動車部門を強化するために41億米ドルの予算を宣言しました。同国政府は、持続可能でコネクテッドなモビリティに向けた自動車産業のバリューチェーンを強化する計画を打ち出しました。欧州委員会によると、欧州諸国は技術用および工業用繊維製品のトップ生産国のひとつです。欧州全域で自動車産業と繊維産業が盛んであることから、予測期間中、同地域の熱可塑性接着フィルム市場を牽引することが期待されます。

欧州の熱可塑性接着フィルム市場の収益と2030年までの予測(金額)

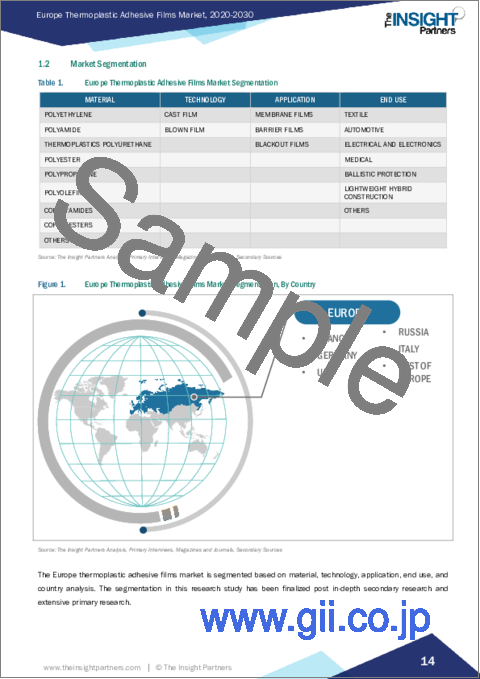

欧州の熱可塑性接着フィルム市場セグメンテーション

欧州の熱可塑性接着フィルム市場は、材料、技術、用途、最終用途、国によって区分されます。

材料別では、欧州の熱可塑性接着フィルム市場は、ポリエチレン、ポリアミド、熱可塑性ポリウレタン、ポリエステル、ポリプロピレン、ポリオレフィン、コポリアミド、コポリエステル、その他に区分されます。2022年には熱可塑性ポリウレタンセグメントが最大のシェアを占めました。

技術別に見ると、欧州の熱可塑性接着フィルム市場はキャストフィルムとブローフィルムに二分されます。2022年にはキャストフィルム部門がより大きなシェアを占めました。

用途別では、欧州の熱可塑性接着フィルム市場はメンブレンフィルム、バリアフィルム、遮光フィルムに区分されます。バリアフィルムセグメントが2022年に最も大きなシェアを占めました。

最終用途別では、欧州の熱可塑性接着フィルム市場は繊維、自動車、電気・電子、医療、防弾、軽量ハイブリッド構造、その他に区分されます。2022年には繊維分野が最大のシェアを占めています。

国別では、欧州の熱可塑性接着フィルム市場はドイツ、フランス、英国、イタリア、スペイン、その他欧州に分類されます。2022年の欧州の熱可塑性接着フィルム市場はドイツが独占。

PROTECHNIC SA、Pontacol AG、HB Fuller co、Covestro AG、Scapa Group Ltd、Gerlinger Industries GmbH、Fenyang Dingxin Films Technology Co Ltd、tesa SEは、欧州の熱可塑性接着フィルム市場で事業を展開する大手企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 欧州の熱可塑性接着フィルム市場情勢

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- エコシステム分析

- 原材料サプライヤー

- 熱可塑性接着フィルムメーカー

- ディストリビューター/サプライヤー

- 最終用途産業

- バリューチェーンのベンダー一覧

第5章 欧州の熱可塑性接着フィルム市場:主要市場力学

- 市場促進要因

- 自動車産業と繊維産業の成長

- 家電需要の増加

- 市場抑制要因

- 原材料価格の変動

- 市場機会

- 弾道保護技術への政府投資の増加

- 今後の動向

- バイオベースの熱可塑性接着フィルムの採用

- 影響分析

第6章 熱可塑性接着フィルム市場:欧州市場分析

- 欧州の熱可塑性接着フィルム市場の売上高

- 熱可塑性接着フィルムの欧州市場予測・分析

第7章 熱可塑性接着フィルムの欧州市場分析-素材

- ポリエチレン

- ポリエチレンの概要

- ポリエチレンの収益と2030年までの予測

- ポリアミド

- ポリアミドの概要

- ポリアミドの市場規模、収益と2030年までの予測

- 熱可塑性ポリウレタン

- ポリウレタンの概要

- 熱可塑性ポリウレタンの市場規模、収益と2030年までの予測

- ポリエステル

- ポリエステルの概要

- ポリエステルの市場規模、収益と2030年までの予測

- ポリプロピレン

- ポリプロピレンの概要

- ポリプロピレンの市場規模、収益と2030年までの予測

- ポリオレフィン

- ポリオレフィンの概要

- ポリオレフィンの市場規模、収益と2030年までの予測

- コポリアミド

- コポリアミドの概要

- コポリアミドの市場規模、収益と2030年までの予測

- コポリエステル

- コポリエステルの概要

- コポリエステルの市場規模、収益と2030年までの予測

- その他

- その他の市場規模、収益と2030年までの予測

第8章 欧州の熱可塑性接着フィルム市場分析-技術

- キャストフィルム

- キャストフィルム市場、収益と2030年までの予測

- ブローフィルム

- ブローフィルム市場、収益と2030年までの予測

第9章 欧州の熱可塑性接着フィルム市場分析-用途

- メンブレンフィルム

- メンブレンフィルムの概要

- メンブレンフィルム市場の収益と2030年までの予測

- バリアフィルム

- バリアフィルム市場の収益と2030年までの予測

- 遮光フィルム

- 遮光フィルムの市場規模、収益と2030年までの予測

第10章 欧州の熱可塑性接着フィルム市場分析:最終用途

- 繊維

- 繊維製品の市場規模、収益と2030年までの予測

- 自動車

- 自動車市場の概要

- 自動車市場の収益と2030年までの予測

- 電気・電子

- 電気・電子市場の収益と2030年までの予測

- 医療

- 医療市場の収益と2030年までの予測

- 弾道保護

- 弾道保護市場の収益と2030年までの予測

- 軽量ハイブリッド構造

- 軽量ハイブリッド建設市場の収益と2030年までの予測

- その他

- その他の概要

- その他市場の収益と2030年までの予測

第11章 欧州の熱可塑性接着フィルム市場:国別分析

- 欧州の熱可塑性接着フィルム市場の収益と予測:国別分析

- 熱可塑性接着フィルムの市場内訳:国別

- ドイツの熱可塑性接着フィルム市場:2030年までの収益と予測

- フランスの熱可塑性接着フィルム市場の収益と2030年までの予測

- イタリアの熱可塑性接着フィルムの2030年までの収益と予測

- 英国の熱可塑性接着フィルム市場の収益と2030年までの予測

- ロシアの熱可塑性接着フィルム市場の収益と2030年までの予測

- その他欧州の熱可塑性接着フィルム市場の収益と2030年までの予測

第12章 業界情勢

- 市場イニシアティブ

- 新製品開発

- 合併と買収

第13章 企業プロファイル

- PROTECHNIC SA

- Pontacol AG

- HB Fuller Co

- Covestro AG

- Scapa Group Ltd

- tesa SE

- FAIT PLAST SpA

- Gerlinger Industries GmbH

第14章 付録

List Of Tables

- Table 1. Europe Thermoplastic Adhesive Films Market Segmentation

- Table 2. List of Raw Material Suppliers

- Table 3. List of Manufacturers

- Table 4. Europe Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million)

- Table 5. Europe Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - Material

- Table 6. North America Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - Technology

- Table 7. North America Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - Application

- Table 8. North America Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - End Use

- Table 9. Germany Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Material

- Table 10. Germany Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Technology

- Table 11. Germany Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Application

- Table 12. Germany Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By End Use

- Table 13. France Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Material

- Table 14. France Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Technology

- Table 15. France Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Application

- Table 16. France Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By End Use

- Table 17. Italy Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Material

- Table 18. Italy Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Technology

- Table 19. Italy Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Application

- Table 20. Italy Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By End Use

- Table 21. UK Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Material

- Table 22. UK Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Technology

- Table 23. UK Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Application

- Table 24. UK Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By End Use

- Table 25. Russia Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Material

- Table 26. Russia Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Technology

- Table 27. Russia Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Application

- Table 28. Russia Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By End Use

- Table 29. Rest of Europe Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Material

- Table 30. Rest of Europe Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Technology

- Table 31. Rest of Europe Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By Application

- Table 32. Rest of Europe Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million) - By End Use

List Of Figures

- Figure 1. Europe Thermoplastic Adhesive Films Market Segmentation, By Country

- Figure 2. Porter's Five Forces Analysis

- Figure 3. Ecosystem: Thermoplastic Adhesive Films Market

- Figure 4. Market Dynamics: Europe Thermoplastic Adhesive Films Market

- Figure 5. Europe thermoplastic adhesive films market Impact Analysis of Drivers and Restraints

- Figure 6. Europe Thermoplastic Adhesive Films Market Revenue (US$ Million), 2020 - 2030

- Figure 7. Europe Thermoplastic Adhesive Films Market Share (%) - Material, 2022 and 2030

- Figure 8. Polyethylene Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 9. Polyamide Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 10. Thermoplastics Polyurethane Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 11. Polyester Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 12. Polypropylene Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 13. Polyolefins Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 14. Copolyamides Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 15. Copolyesters Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 16. Others Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 17. North America Thermoplastic Adhesive Films Market Share (%) - Technology, 2022 and 2030

- Figure 18. Cast Film Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 19. Blown Film Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 20. North America Thermoplastic Adhesive Films Market Share (%) - Application, 2022 and 2030

- Figure 21. Membrane Films Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 22. Barrier Films Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 23. Blackout Films Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 24. North America Thermoplastic Adhesive Films Market Share (%) - End Use, 2022 and 2030

- Figure 25. Textile Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 26. Automotive Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 27. Electrical and Electronics Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 28. Medical Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 29. Ballistic Protection Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 30. Lightweight Hybrid Construction Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 31. Others Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 32. Europe Thermoplastic Adhesive Films Market, by Key Country - Revenue (2022) (US$ Million)

- Figure 33. Thermoplastic Adhesive Films Market Breakdown by Key Countries, 2022 and 2030 (%)

- Figure 34. Germany Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 35. France Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 36. Italy Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 37. UK Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 38. Russia Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 39. Rest of Europe Thermoplastic Adhesive Films Market Revenue and Forecasts To 2030 (US$ Million)

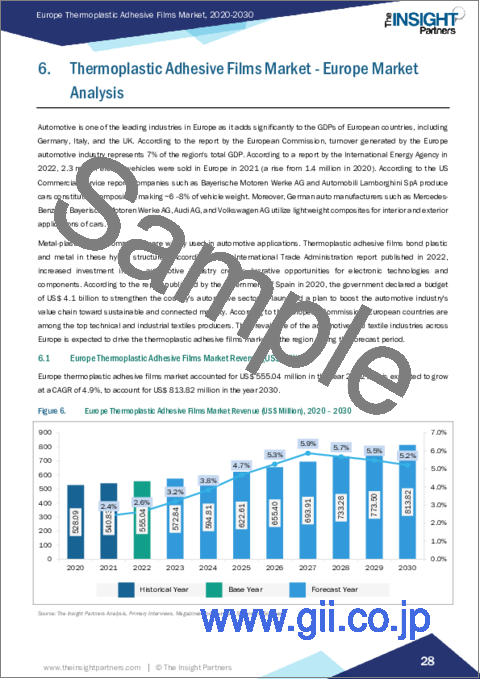

The Europe thermoplastic adhesive films market was valued at US$ 555.04 million in 2022 and is expected to reach US$ 813.82 million by 2030; it is estimated to grow at a CAGR of 4.9% from 2022 to 2030.

Growing Government Investment in Ballistic Protection Technologies Drive Europe Thermoplastic Adhesive Films Market

The increased security risks and the need to enhance national border security have prompted governments to increase investments in defense and ballistic protection. Governments started initiatives such as Innovations for Defense Excellence and Technology Development Fund to provide financial assistance for product innovations for the Armed Forces. High-performance fabrics are used widely for ballistic protection against explosions, blasts, and projectiles. These fabrics possess distinct characteristics such as high strength, high modulus, sound absorption, impact energy absorption, and chemical resistance.

Advanced composites are also utilized in ballistic applications such as interlinings and insulations, protective products for vehicular crash guards, ballistic panels for body armor, and helmets. Thermoplastic adhesive films have broad applications in the production of advanced composites and textiles. Thus, the growing government investments in the defense sector to develop military vehicles and high-performance products are expected to create growth opportunities for thermoplastic adhesive film manufacturers during the forecast period.

Europe Thermoplastic Adhesive Films Market Overview

Automotive is one of the leading industries in Europe as it adds significantly to the GDPs of European countries, including Germany, Italy, and the UK. According to the report by the European Commission, turnover generated by the Europe automotive industry represents 7% of the region's total GDP. According to a report by the International Energy Agency in 2022, 2.3?million electric vehicles were sold in Europe in 2021 (a rise from 1.4?million in 2020). According to the US Commercial Service report, companies such as Bayerische Motoren Werke AG and Automobili Lamborghini SpA produce cars constituting composites, making ~6-8% of vehicle weight. Moreover, German auto manufacturers such as Mercedes-Benz AG, Bayerische Motoren Werke AG, Audi AG, and Volkswagen AG utilize lightweight composites for interior and exterior applications of cars.

Metal-plastic hybrid components are widely used in automotive applications. Thermoplastic adhesive films bond plastic and metal in these hybrid structures. According to the International Trade Administration report published in 2022, increased investment in the automotive industry creates lucrative opportunities for electronic technologies and components. According to the report published by the government of Spain in 2020, the government declared a budget of US$ 4.1 billion to strengthen the country's automotive sector. It launched a plan to boost the automotive industry's value chain toward sustainable and connected mobility. According to the European Commission, European countries are among the top technical and industrial textiles producers. The prevalence of the automotive and textile industries across Europe is expected to drive the thermoplastic adhesive films market in the region during the forecast period.

Europe Thermoplastic Adhesive Films Market Revenue and Forecast to 2030 (US$ Million)

Europe Thermoplastic Adhesive Films Market Segmentation

The Europe thermoplastic adhesive films market is segmented based on material, technology, application, end use, and country.

Based on material, the Europe thermoplastic adhesive films market is segmented into polyethylene, polyamide, thermoplastics polyurethane, polyester, polypropylene, polyolefins, copolyamides, copolyesters, and others. The thermoplastics polyurethane segment held the largest share in 2022.

Based on technology, the Europe thermoplastic adhesive films market is bifurcated into cast film and blown film. The cast film segment held a larger share in 2022.

Based on application, the Europe thermoplastic adhesive films market is segmented into membrane films, barrier films, and blackout films. The barrier films segment held the largest share in 2022.

Based on end use, the Europe thermoplastic adhesive films market is segmented into textile, automotive, electrical and electronics, medical, ballistic protection, lightweight hybrid construction, and others. The textile segment held the largest share in 2022.

Based on country, the Europe thermoplastic adhesive films market is categorized into Germany, France, the UK, Italy, Spain, and the Rest of Europe. Germany dominated the Europe thermoplastic adhesive films market in 2022.

PROTECHNIC SA, Pontacol AG, HB Fuller co, Covestro AG, Scapa Group Ltd, Gerlinger Industries GmbH, Fenyang Dingxin Films Technology Co Ltd, and tesa SE are some of the leading companies operating in the Europe thermoplastic adhesive films market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

- 2.2.1 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Europe Thermoplastic Adhesive Films Market Landscape

- 4.1 Overview

- 4.2 Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Ecosystem Analysis

- 4.3.1 Raw Material Suppliers

- 4.3.2 Thermoplastic Adhesive Films Manufacturers

- 4.3.3 Distributors/Suppliers

- 4.3.4 End-Use Industries

- 4.4 List of Vendors in the Value Chain

5. Europe Thermoplastic Adhesive Films Market - Key Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Growing Automotive and Textile Industries

- 5.1.2 Rising Demand for Consumer Electronics

- 5.2 Market Restraints

- 5.2.1 Fluctuations in Raw Material Prices

- 5.3 Market Opportunities

- 5.3.1 Growing Government Investment in Ballistic Protection Technologies

- 5.4 Future Trends

- 5.4.1 Adoption of Bio-Based Thermoplastic Adhesive Films

- 5.5 Impact Analysis

6. Thermoplastic Adhesive Films Market - Europe Market Analysis

- 6.1 Europe Thermoplastic Adhesive Films Market Revenue (US$ Million)

- 6.2 Europe Thermoplastic Adhesive Films Market Forecast and Analysis

7. Europe Thermoplastic Adhesive Films Market Analysis - Material

- 7.1 Polyethylene

- 7.1.1 Overview

- 7.1.2 Polyethylene Market Revenue and Forecast to 2030 (US$ Million)

- 7.2 Polyamide

- 7.2.1 Overview

- 7.2.2 Polyamide Market Volume, Revenue and Forecast to 2030 (US$ Million)

- 7.3 Thermoplastics Polyurethane

- 7.3.1 Overview

- 7.3.2 Thermoplastics Polyurethane Market Volume, Revenue and Forecast to 2030 (US$ Million)

- 7.4 Polyester

- 7.4.1 Overview

- 7.4.2 Polyester Market Volume, Revenue and Forecast to 2030 (US$ Million)

- 7.5 Polypropylene

- 7.5.1 Overview

- 7.5.2 Polypropylene Market Volume, Revenue and Forecast to 2030 (US$ Million)

- 7.6 Polyolefins

- 7.6.1 Overview

- 7.6.2 Polyolefins Market Volume, Revenue and Forecast to 2030 (US$ Million)

- 7.7 Copolyamides

- 7.7.1 Overview

- 7.7.2 Copolyamides Market Volume, Revenue and Forecast to 2030 (US$ Million)

- 7.8 Copolyesters

- 7.8.1 Overview

- 7.8.2 Copolyesters Market Volume, Revenue and Forecast to 2030 (US$ Million)

- 7.9 Others

- 7.9.1 Overview

- 7.9.2 Others Market Volume, Revenue and Forecast to 2030 (US$ Million)

8. Europe Thermoplastic Adhesive Films Market Analysis - Technology

- 8.1 Cast Film

- 8.1.1 Overview

- 8.1.2 Cast Film Market, Revenue and Forecast to 2030 (US$ Million)

- 8.2 Blown Film

- 8.2.1 Overview

- 8.2.2 Blown Film Market, Revenue and Forecast to 2030 (US$ Million)

9. Europe Thermoplastic Adhesive Films Market Analysis - Application

- 9.1 Membrane Films

- 9.1.1 Overview

- 9.1.2 Membrane Films Market Revenue and Forecast to 2030 (US$ Million)

- 9.2 Barrier Films

- 9.2.1 Overview

- 9.2.2 Barrier Films Market Revenue and Forecast to 2030 (US$ Million)

- 9.3 Blackout Films

- 9.3.1 Overview

- 9.3.2 Blackout Films Market Volume, Revenue and Forecast to 2030 (US$ Million)

10. Europe Thermoplastic Adhesive Films Market Analysis - End Use

- 10.1 Textile

- 10.1.1 Overview

- 10.1.2 Textile Market, Revenue, and Forecast to 2030 (US$ Million)

- 10.2 Automotive

- 10.2.1 Overview

- 10.2.2 Automotive Market Revenue, and Forecast to 2030 (US$ Million)

- 10.3 Electrical and Electronics

- 10.3.1 Overview

- 10.3.2 Electrical and Electronics Market Revenue and Forecast to 2030 (US$ Million)

- 10.4 Medical

- 10.4.1 Overview

- 10.4.2 Medical Market Revenue and Forecast to 2030 (US$ Million)

- 10.5 Ballistic Protection

- 10.5.1 Overview

- 10.5.2 Ballistic Protection Market Revenue and Forecast to 2030 (US$ Million)

- 10.6 Lightweight Hybrid Construction

- 10.6.1 Overview

- 10.6.2 Lightweight Hybrid Construction Market Revenue and Forecast to 2030 (US$ Million)

- 10.7 Others

- 10.7.1 Overview

- 10.7.2 Others Market Revenue and Forecast to 2030 (US$ Million)

11. Europe Thermoplastic Adhesive Films Market - Country Analysis

- 11.1.1 Europe Thermoplastic Adhesive Films Market Revenue and Forecasts and Analysis - By Countries

- 11.1.1.1 Thermoplastic Adhesive Films Market Breakdown by Country

- 11.1.1.2 Germany Thermoplastic Adhesive Films Market Revenue and Forecasts to 2030 (US$ Million)

- 11.1.1.2.1 Germany Thermoplastic Adhesive Films Market Breakdown by Material

- 11.1.1.2.2 Germany Thermoplastic Adhesive Films Market Breakdown by Technology

- 11.1.1.2.3 Germany Thermoplastic Adhesive Films Market Breakdown by Application

- 11.1.1.2.4 Germany Thermoplastic Adhesive Films Market Breakdown by End Use

- 11.1.1.3 France Thermoplastic Adhesive Films Market Revenue and Forecasts to 2030 (US$ Million)

- 11.1.1.3.1 France Thermoplastic Adhesive Films Market Breakdown by Material

- 11.1.1.3.2 France Thermoplastic Adhesive Films Market Breakdown by Technology

- 11.1.1.3.3 France Thermoplastic Adhesive Films Market Breakdown by Application

- 11.1.1.3.4 France Thermoplastic Adhesive Films Market Breakdown by End Use

- 11.1.1.4 Italy Thermoplastic Adhesive Films Market Revenue and Forecasts to 2030 (US$ Million)

- 11.1.1.4.1 Italy Thermoplastic Adhesive Films Market Breakdown by Material

- 11.1.1.4.2 Italy Thermoplastic Adhesive Films Market Breakdown by Technology

- 11.1.1.4.3 Italy Thermoplastic Adhesive Films Market Breakdown by Application

- 11.1.1.4.4 Italy Thermoplastic Adhesive Films Market Breakdown by End Use

- 11.1.1.5 UK Thermoplastic Adhesive Films Market Revenue and Forecasts to 2030 (US$ Million)

- 11.1.1.5.1 UK Thermoplastic Adhesive Films Market Breakdown by Material

- 11.1.1.5.2 UK Thermoplastic Adhesive Films Market Breakdown by Technology

- 11.1.1.5.3 UK Thermoplastic Adhesive Films Market Breakdown by Application

- 11.1.1.5.4 UK Thermoplastic Adhesive Films Market Breakdown by End Use

- 11.1.1.6 Russia Thermoplastic Adhesive Films Market Revenue and Forecasts to 2030 (US$ Million)

- 11.1.1.6.1 Russia Thermoplastic Adhesive Films Market Breakdown by Material

- 11.1.1.6.2 Russia Thermoplastic Adhesive Films Market Breakdown by Technology

- 11.1.1.6.3 Russia Thermoplastic Adhesive Films Market Breakdown by Application

- 11.1.1.6.4 Russia Thermoplastic Adhesive Films Market Breakdown by End Use

- 11.1.1.7 Rest of Europe Thermoplastic Adhesive Films Market Revenue and Forecasts to 2030 (US$ Million)

- 11.1.1.7.1 Rest of Europe Thermoplastic Adhesive Films Market Breakdown by Material

- 11.1.1.7.2 Rest of Europe Thermoplastic Adhesive Films Market Breakdown by Technology

- 11.1.1.7.3 Rest of Europe Thermoplastic Adhesive Films Market Breakdown by Application

- 11.1.1.7.4 Rest of Europe Thermoplastic Adhesive Films Market Breakdown by End Use

12. Industry Landscape

- 12.1 Overview

- 12.2 Market Initiative

- 12.3 New Product Development

- 12.4 Merger and Acquisition

13. Company Profiles

- 13.1 PROTECHNIC SA

- 13.1.1 Key Facts

- 13.1.2 Business Description

- 13.1.3 Products and Services

- 13.1.4 Financial Overview

- 13.1.5 SWOT Analysis

- 13.1.6 Key Developments

- 13.2 Pontacol AG

- 13.2.1 Key Facts

- 13.2.2 Business Description

- 13.2.3 Products and Services

- 13.2.4 Financial Overview

- 13.2.5 SWOT Analysis

- 13.2.6 Key Developments

- 13.3 HB Fuller Co

- 13.3.1 Key Facts

- 13.3.2 Business Description

- 13.3.3 Products and Services

- 13.3.4 Financial Overview

- 13.3.5 SWOT Analysis

- 13.3.6 Key Developments

- 13.4 Covestro AG

- 13.4.1 Key Facts

- 13.4.2 Business Description

- 13.4.3 Products and Services

- 13.4.4 Financial Overview

- 13.4.5 SWOT Analysis

- 13.4.6 Key Developments

- 13.5 Scapa Group Ltd

- 13.5.1 Key Facts

- 13.5.2 Business Description

- 13.5.3 Products and Services

- 13.5.4 Financial Overview

- 13.5.5 SWOT Analysis

- 13.5.6 Key Developments

- 13.6 tesa SE

- 13.6.1 Key Facts

- 13.6.2 Business Description

- 13.6.3 Products and Services

- 13.6.4 Financial Overview

- 13.6.5 SWOT Analysis

- 13.6.6 Key Developments

- 13.7 FAIT PLAST SpA

- 13.7.1 Key Facts

- 13.7.2 Business Description

- 13.7.3 Products and Services

- 13.7.4 Financial Overview

- 13.7.5 SWOT Analysis

- 13.7.6 Key Developments

- 13.8 Gerlinger Industries GmbH

- 13.8.1 Key Facts

- 13.8.2 Business Description

- 13.8.3 Products and Services

- 13.8.4 Financial Overview

- 13.8.5 SWOT Analysis

- 13.8.6 Key Developments