|

市場調査レポート

商品コード

1740908

熱可塑性接着フィルムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Thermoplastic Adhesive Films Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 熱可塑性接着フィルムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月25日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

世界の熱可塑性接着フィルム市場は、2024年には24億米ドルと評価され、CAGR 8.8%で成長し、2034年には55億米ドルに達すると推定されています。

この増加傾向は、特に自動車や電子機器製造など、いくつかの最終用途産業で軽量材料への嗜好が高まっていることが大きな要因となっています。熱可塑性接着フィルムは、製品全体の重量を大幅に削減しながら部品を接合するためにますます使用されるようになっています。燃費目標をサポートし、排出量削減に貢献するその能力は、世界的に強化される環境規制と持続可能性ベンチマークに合致しています。

小型電子機器やウェアラブルデバイスにおいて、これらのフィルムは優れた耐熱性を提供し、小型で高密度な製品設計における性能維持に不可欠です。また、スマートフォン、フレキシブルガジェット、次世代コンシューマーデバイスなど、スペースに制約のあるアプリケーションでは、クリーンな加工と信頼性の高い接合が可能になります。さらに、医療技術分野は、生体適合性、耐薬品性、容易な滅菌が不可欠な、将来性の高い分野として浮上しています。これらのフィルムは、様々な医療用ウェアラブル製品や使い捨てヘルスケア製品に使用され、耐久性がありながら非侵襲的な接着を実現しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 24億米ドル |

| 予測金額 | 55億米ドル |

| CAGR | 8.8% |

持続可能性が需要形成の中心テーマとなりつつあります。熱可塑性接着フィルムは、無溶剤でリサイクル可能であるため、VOC排出を最小限に抑えたい産業に適した環境配慮型ソリューションとみなされています。規制の枠組みや環境・社会・ガバナンス(ESG)の目標に沿うため、環境に優しい接着剤の代替品を採用するメーカーが増えています。フィルムキャスティングやホットメルト・アプリケーションのような加工技術の進歩により、粘着フィルムの熱挙動、シール能力、タック特性が改善され、工業用ラミネートや光学システムのような高精度が要求される分野での使用が拡大しています。

材料のセグメント化では、2024年の市場にはポリエチレン、ポリアミド、熱可塑性ポリウレタン、ポリエステル、ポリプロピレン、ポリオレフィン、その他の材料タイプが含まれます。2024年の市場規模は24億米ドルで、今後大きく成長し、2034年には55億米ドルに達すると予測されます。このうち、ポリエチレンは2024年の総シェアの22.9%を占めているが、これは主にその手頃な価格、柔軟性、さまざまな基材とよく接着する能力によるものです。ポリエチレンはパッケージングや自動車などの分野で使用されているが、産業界がより先進的な性能のフィルムにシフトしているため、その成長率は緩やかなままです。熱可塑性ポリウレタンは、その伸縮性、透明性、優れた耐摩耗性により、大きな勢いを見せています。小型化された柔軟な部品へのニーズの高まりが、新たな用途での採用を後押ししています。

技術的な観点から、2024年の市場は押出コーティング、ホットメルト接着剤、樹脂混合、フィルムキャスティング、その他の加工技術に区分されます。エクストルージョンコーティング法は、その高速生産能力と様々な基材への一貫したコーティング品質により、市場シェア27.5%でセグメントをリードしています。ホットメルト接着剤は、無溶剤で環境に優しく、接着強度が安定していることから、エレクトロニクスや衛生関連製品を中心に急速に拡大しています。樹脂配合は、タックや耐熱性といったフィルム特性のカスタマイズには有利だが、複雑な配合要件や高い製造コストによる制約に直面しています。フィルムキャスティングは、滑らかで欠陥のないフィルムが不可欠な高精度環境、特に光学・医療グレードの用途で好まれています。

2024年の市場を最終用途別に分析すると、繊維、自動車、電気・電子、医療、防弾、建設、その他の分野に分けられます。繊維産業は、衣料品、家庭用家具、スマート・テキスタイルのシームレス・ラミネーション需要が高まっていることから、25%のシェアでリードしています。接着フィルムは、無溶剤繊維接着ソリューションにおいて重要な役割を果たしています。自動車分野では、自動車の軽量化が推進され、騒音、振動、ハーシュネス(NVH)を緩和する必要性が、これらのフィルムの関連性を高めています。医療用途も急速に進歩しており、特に皮膚感応性フィルムや滅菌可能なフィルムは、健康監視装置や診断ツールに使用されています。防弾・防衛用途では、高強度フィルムを保護複合材のレイヤリングに活用しています。

地域別では、米国が2024年の世界市場で17.8%のシェアを占め、その市場規模は約4億3,000万米ドルで、2034年には10億2,000万米ドルに成長すると予測されています。この優位性は、自動車、航空宇宙、医療、エレクトロニクスなどの先端製造分野で熱可塑性接着フィルムの浸透が進んでいることに起因しています。同国は無溶剤接着剤に注力しており、貿易規制と国内調達戦略の調整を含む支援的な政策環境が、国内生産と技術革新を後押ししています。

同業界の競争を牽引している主な企業には、ダウ、3M、BASF SE、ヘンケルAG、コベストロAGなどがあり、それぞれが市場での存在感を高めるために異なるアプローチを採用しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 自動車軽量化の需要の高まり

- 家電製品とウェアラブル機器の成長

- 医療機器産業の拡大

- 持続可能な接着剤への関心の高まり

- フィルムキャスティングとホットメルトにおける技術の進歩

- 繊維産業の革新の台頭(例:スマートテキスタイル)

- 業界の潜在的リスク&課題

- 原材料コストが高い(例:TPU、ポリアミド)

- 熱硬化性樹脂に比べて耐熱性および耐薬品性が限られている

- 多層構造の複雑なリサイクル性

- 促進要因

- トランプ政権の関税の影響- 構造化された概要

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:材料別、2021 –2034

- 主要動向

- ポリエチレン

- ポリアミド

- 熱可塑性ポリウレタン

- ポリエステル

- ポリプロピレン

- ポリオレン

- その他の材料

第6章 市場推計・予測:テクノロジー別、2021 –2034

- 主要動向

- 押し出しコーティング

- ホットメルト接着剤

- 樹脂ブレンド

- 映画キャスティング

第7章 市場推計・予測:最終用途別、2021 –2034

- 主要動向

- 繊維

- 自動車

- 電気・電子工学

- 医学

- 弾道保護

- 工事

- その他の用途

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- 3M Company

- Arkema SA

- Ashland Global

- Avery Dennison

- BASF SE

- Covestro AG

- Dow Inc.

- DuPont

- EMS-Chemie Holding AG

- H.B. Fuller

- Henkel AG

- Huntsman Corporation

- Mitsui Chemicals Inc.

- Sika AG

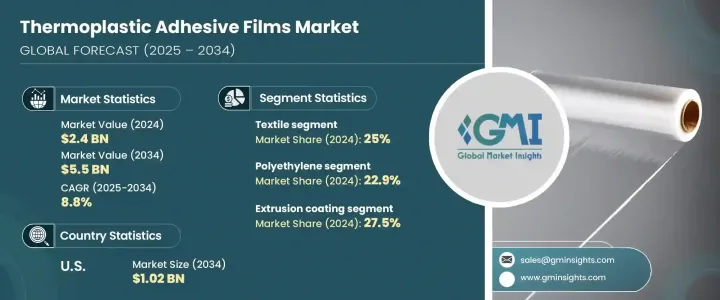

The Global Thermoplastic Adhesive Films Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 8.8% to reach USD 5.5 billion by 2034. This upward trend is largely fueled by the growing preference for lightweight materials across several end-use industries, especially in automotive and electronics manufacturing. Thermoplastic adhesive films are being increasingly used to bond components while significantly reducing overall product weight. Their ability to support fuel efficiency goals and contribute to reduced emissions aligns well with tightening environmental regulations and sustainability benchmarks globally.

In compact electronics and wearable devices, these films offer excellent thermal resistance, which is essential for maintaining performance in miniature, high-density product designs. They allow for clean processing and reliable bonding in space-constrained applications such as smartphones, flexible gadgets, and next-gen consumer devices. Additionally, the medical technology sector is emerging as a high-potential area, where biocompatibility, chemical resistance, and easy sterilization are vital. These films are used in a variety of medical wearables and disposable healthcare products, delivering durable yet non-invasive adhesion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $5.5 Billion |

| CAGR | 8.8% |

Sustainability is becoming a central theme in shaping demand. Thermoplastic adhesive films are seen as an eco-conscious solution due to their solvent-free nature and recyclability, making them suitable for industries seeking to minimize VOC emissions. Manufacturers are increasingly adopting environmentally friendly adhesive alternatives to align with regulatory frameworks and environmental, social, and governance (ESG) goals. Advances in processing technologies like film casting and hot melt applications have improved the thermal behavior, sealing ability, and tack properties of adhesive films, expanding their use in areas that demand high precision, such as industrial laminates and optical systems.

In terms of material segmentation, the market in 2024 includes polyethylene, polyamide, thermoplastic polyurethane, polyester, polypropylene, polyolefins, and other material types. With the market valued at USD 2.4 billion in 2024, it is forecast to grow substantially and reach USD 5.5 billion by 2034. Among these, polyethylene accounted for 22.9% of the total share in 2024, primarily due to its affordability, flexibility, and ability to bond well with various substrates. It is used in sectors like packaging and automotive, although its growth rate remains modest as industries shift toward more advanced performance films. Thermoplastic polyurethane is experiencing significant momentum thanks to its elasticity, transparency, and superior abrasion resistance. The growing need for miniaturized and flexible components is supporting its adoption across emerging applications.

From a technology standpoint, the 2024 market is segmented into extrusion coating, hot melt adhesives, resin blending, film casting, and other processing techniques. The extrusion coating method led the segment with a 27.5% market share due to its high-speed production capability and consistent coating quality across various substrates. Hot melt adhesives are expanding quickly, especially in electronics and hygiene-related products, driven by their solvent-free, environmentally sound properties and dependable bond strength. Resin blending, while advantageous for customizing film characteristics like tack and heat resistance, faces constraints due to complex formulation requirements and elevated production costs. Film casting is finding preference in high-precision environments where smooth, defect-free films are essential, particularly for optical and medical-grade applications.

When analyzed by end use in 2024, the market is divided into textiles, automotive, electrical and electronics, medical, ballistic protection, construction, and other sectors. The textile industry led with a 25% share, as demand rises for seamless lamination in garments, home furnishings, and smart textiles. Adhesive films are playing a key role in solvent-free textile bonding solutions. In the automotive domain, the push for lighter vehicles and the need to mitigate noise, vibration, and harshness (NVH) have reinforced the relevance of these films. Medical uses are also advancing rapidly, particularly in skin-sensitive and sterilizable films for health-monitoring devices and diagnostic tools. Ballistic and defense applications leverage high-strength films for layering purposes in protective composites.

Regionally, the United States held a 17.8% share in the global market in 2024, valued at approximately USD 430 million, and is projected to grow to USD 1.02 billion by 2034. This dominance is attributed to the increasing penetration of thermoplastic adhesive films in advanced manufacturing sectors like automotive, aerospace, medical, and electronics. The country's focus on solvent-free adhesives and its supportive policy environment, including adjustments in trade regulations and domestic sourcing strategies, are boosting local production and innovation.

Major players driving competition in the industry include companies like Dow Inc., 3M Company, BASF SE, Henkel AG, and Covestro AG, each adopting different approaches to strengthen their market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand in automotive lightweighting

- 3.6.1.2 Growth in consumer electronics and wearables

- 3.6.1.3 Expansion of the medical device industry

- 3.6.1.4 Increasing preference for sustainable adhesives

- 3.6.1.5 Technological advancements in film casting and hot melt

- 3.6.1.6 Rising textile industry innovations (e.g., smart textiles)

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High raw material costs (e.g., TPU, polyamide)

- 3.6.2.2 Limited heat and chemical resistance compared to thermosets

- 3.6.2.3 Complex recyclability of multi-layer structures

- 3.6.1 Growth drivers

- 3.7 Impact of trump administration tariffs – structured overview

- 3.7.1 Impact on trade

- 3.7.1.1 Trade volume disruptions

- 3.7.1.2 Retaliatory measures

- 3.7.2 Impact on the industry

- 3.7.2.1 Supply-side impact (raw materials)

- 3.7.2.1.1 Price volatility in key materials

- 3.7.2.1.2 Supply chain restructuring

- 3.7.2.1.3 Production cost implications

- 3.7.2.2 Demand-side impact (selling price)

- 3.7.2.2.1 Price transmission to end markets

- 3.7.2.2.2 Market share dynamics

- 3.7.2.2.3 Consumer response patterns

- 3.7.2.1 Supply-side impact (raw materials)

- 3.7.3 Key companies impacted

- 3.7.4 Strategic industry responses

- 3.7.4.1 Supply chain reconfiguration

- 3.7.4.2 Pricing and product strategies

- 3.7.4.3 Policy engagement

- 3.7.4.4 Outlook and future considerations

- 3.7.1 Impact on trade

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene

- 5.3 Polyamide

- 5.4 Thermoplastics polyurethane

- 5.5 Polyester

- 5.6 Polypropylene

- 5.7 Polyolens

- 5.8 Other materials

Chapter 6 Market Estimates and Forecast, By Technologies, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Extrusion coating

- 6.3 Hot melt adhesive

- 6.4 Resin blending

- 6.5 Film casting

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Textile

- 7.3 Automotive

- 7.4 Electrical and electronics

- 7.5 Medical

- 7.6 Ballistic protection

- 7.7 Construction

- 7.8 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M Company

- 9.2 Arkema SA

- 9.3 Ashland Global

- 9.4 Avery Dennison

- 9.5 BASF SE

- 9.6 Covestro AG

- 9.7 Dow Inc.

- 9.8 DuPont

- 9.9 EMS-Chemie Holding AG

- 9.10 H.B. Fuller

- 9.11 Henkel AG

- 9.12 Huntsman Corporation

- 9.13 Mitsui Chemicals Inc.

- 9.14 Sika AG