|

|

市場調査レポート

商品コード

1420206

防空レーダーのアジア太平洋市場:地域別分析 - 範囲別、製品タイプ別、システムタイプ別、プラットフォーム別、用途別、予測(~2030年)Asia Pacific Air Defense Radar Market Forecast to 2030 - Regional Analysis - by Range, Product Type, System Type, Platform, and Application |

||||||

|

|

|||||||

|

|||||||

| 防空レーダーのアジア太平洋市場:地域別分析 - 範囲別、製品タイプ別、システムタイプ別、プラットフォーム別、用途別、予測(~2030年) |

|

出版日: 2023年12月14日

発行: The Insight Partners

ページ情報: 英文 136 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

アジア太平洋の防空レーダーの市場規模は、2022年に16億8,166万米ドルに達し、2022~2030年にかけてCAGR 5.9%で成長し、2030年には26億6,998万米ドルに成長すると予測されています。

小型化・低コストレーダーの市場開拓がアジア太平洋の防空レーダー市場を後押し

レーダーの小型化・低コスト化は、半導体製造プロセスの改善や関連部品の小型化などの技術進歩によるものです。これらの進歩により、従来のレーダーシステムと比較して、性能を損なうことなく、より小型・軽量で費用対効果の高いレーダーシステムや小型化レーダーシステムの開発が可能となっています。そのコンパクトな形状により、よりアクセスしやすくなり、さまざまな運用要件や環境に適応できるようになります。この特徴により、地上システム、艦艇、無人航空機(UAV)など、さまざまなプラットフォームへのレーダーの統合も容易になります。小型化レーダーの柔軟性と適応性は、多様な運用環境に適しており、市場の可能性を拡大しています。さらに、さまざまな市場プレーヤーは、防空レーダーシステムのコスト効率により焦点を当てています。例えば、多機能レーダーシステムなどのレーダーシステムは、複数のレーダー機能を単一のプラットフォームに統合することで、運用効率を高めています。単一のシステムで複数のタスクを実行できるため、運用効率と費用対効果が向上します。このため、市場では小型化・低コスト化が進んでいます。

アジア太平洋の防空レーダー市場概要

アジア太平洋の防空レーダー市場は著しい成長を遂げています。アジア太平洋の緊張と地政学的ダイナミクスの高まりにより、アジア太平洋諸国は防衛力を強化しています。その結果、国家安全保障と領土保全を守るため、レーダーを含む高度な防空システムに対する需要が高まっています。さらに、既存の防空システムの急速な近代化とアップグレード計画がアジア太平洋の防空レーダー市場を牽引しています。この地域の多くの国々は、進化する脅威の状況に対応するため、軍事設備のアップグレードに多額の投資を行っています。レーダーシステムのアップグレードは、ミサイル、航空機、ドローンなどの空中脅威の早期探知、追跡、迎撃を可能にするため、この近代化努力の重要な側面です。アジア太平洋は軍事技術に惜しみなく投資しています。例えば、2022年、アジア太平洋の主要国(対象範囲とする)は軍事技術に5,414億米ドルを投資しました。複数の軍事情報源によると、この地域は2023年に1,312隻以上の艦艇を占めました。また、中国、インド、日本、韓国などの国々は、地域全体で将来の調達のために~52隻の海軍艦艇を共同で発注しました。これにより、艦艇用防空レーダーシステムの需要がさらに高まります。

能動型電子走査アレイ(AESA)などのレーダー技術の進歩は、探知能力の強化、運用範囲の拡大、目標追尾精度の向上をもたらしてきました。こうした技術進歩により、アジア太平洋では次世代防空レーダーシステムの需要が急増しています。さらに、非対称戦争、テロリズム、サイバー脅威といった非伝統的な安全保障上の課題の台頭が、強固な防空レーダー・システムの必要性に拍車をかけています。各国政府は、従来型と非従来型の脅威を包含する包括的な防衛戦略を策定することに熱心であり、高度なレーダー技術への投資の増加につながっています。この地域の国々の経済発展と防衛予算の増加も、アジア太平洋の防空レーダー市場の成長を支えています。中国、インド、日本、韓国を含む多くの国々が、防空システムを含む防衛能力の強化に多額の資金を割り当てています。こうした財政的コミットメントが、アジア太平洋の防空レーダー市場の成長に有利な環境を作り出しています。

アジア太平洋の防空レーダー市場の収益と2030年までの予測(100万米ドル)

アジア太平洋の防空レーダー市場のセグメンテーション

アジア太平洋の防空レーダー市場は、機能、範囲、システムタイプ、プラットフォーム、用途、国別に区分されます。

機能別に見ると、アジア太平洋の防空レーダー市場は、合成開口レーダーと移動目標指示レーダー、監視レーダー、航空早期警戒レーダー、多機能レーダー、気象レーダー、その他に区分されます。2022年のアジア太平洋の防空レーダー市場では、合成開口レーダーと移動目標指示レーダー分野が大きなシェアを占めています。

射程距離に基づいて、アジア太平洋の防空レーダー市場は短距離、中距離、長距離に区分されます。2022年のアジア太平洋の防空レーダー市場では、中距離セグメントが最大のシェアを占めています。

システムタイプに基づいて、アジア太平洋の防空レーダー市場は固定レーダーとポータブルレーダーに区分されます。2022年のアジア太平洋の防空レーダー市場では、固定レーダー分野が最大のシェアを占めています。

プラットフォーム別では、アジア太平洋の防空レーダー市場は地上ベース、航空機搭載、海軍ベースに区分されます。2022年のアジア太平洋の防空レーダー市場では、地上ベースセグメントが最大のシェアを占めています。

用途別では、アジア太平洋の防空レーダー市場は弾道ミサイル防衛、敵味方識別、気象予測、その他に区分されます。敵味方識別分野が2022年のアジア太平洋の防空レーダー市場で最大のシェアを占めています。

国別では、アジア太平洋の防空レーダー市場は、オーストラリア、中国、インド、日本、韓国、その他アジア太平洋に区分されます。2022年のアジア太平洋の防空レーダー市場は中国が独占しました。

BAE Systems Plc、General Dynamics Corp、Honeywell International Inc、Israel Aerospace Industries Ltd、Leonardo SpA、Lockheed Martin Corp、Northrop Grumman Corp、Raytheon Technologies Corp、Saab AB、Thales SAは、アジア太平洋の防空レーダー市場で事業を展開している大手企業の一部です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 調査手法

- 範囲

- 2次調査

- 1次調査

第4章 アジア太平洋の防空レーダーの市場情勢

- ポーターのファイブフォース分析

- エコシステム分析

- 原材料・コンポーネントサプライヤー

- 防空レーダーメーカー

- システムインテグレーター・ソフトウェア開発者

- エンドユーザー

第5章 アジア太平洋の防空レーダー市場:主要産業力学

- 主な市場促進要因

- 防空レーダーの供給契約数の増加

- 国防費の継続的増加

- ネットワーク中心主義と現代戦争の出現

- 主な市場抑制要因

- 妨害電波となりすましの脅威

- エアロスタットレーダーとバルーンレーダーの配備減少

- 主な市場機会

- 無人航空機の採用増加

- 国境を越えた紛争の増加

- 今後の動向

- 小型化・低コストレーダーの開発

- 促進要因と抑制要因の影響

第6章 防空レーダー市場:アジア太平洋市場分析

- アジア太平洋の防空レーダー市場の収益シェア:地域別(2020年・2030年)

- アジア太平洋の防空レーダー市場収益の推移(2020~2030年)

第7章 アジア太平洋の防空レーダー市場分析:製品タイプ別

- アジア太平洋の防空レーダー市場の収益シェア:製品タイプ別(2022年・2030年)

- 合成開口レーダー・移動目標表示レーダー

- 監視レーダー

- 航空早期警戒レーダー

- 多機能レーダー

- 気象レーダー

- その他

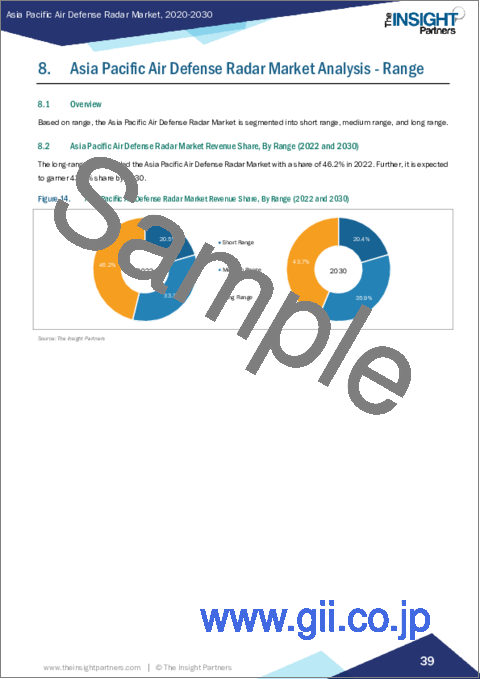

第8章 アジア太平洋の防空レーダー市場分析:範囲別

- アジア太平洋の防空レーダー市場の収益シェア:範囲別(2022年・2030年)

- 短距離

- 中距離

- 長距離

第9章 アジア太平洋の防空レーダー市場分析:システムタイプ

- アジア太平洋の防空レーダー市場の収益シェア:システムタイプ別(2022年・2030年)

- 固定レーダー

- ポータブルレーダー

第10章 アジア太平洋の防空レーダー市場分析:プラットフォーム

- アジア太平洋の防空レーダー市場の収益シェア:プラットフォーム別(2022年・2030年)

- 地上ベース

- 航空機搭載型

- 海軍ベース

第11章 アジア太平洋の防空レーダー市場分析:用途別

- アジア太平洋の防空レーダー市場の収益シェア:用途別(2022年・2030年)

- 弾道ミサイル防衛

- 敵味方識別

- 気象予測

- その他

第12章 アジア太平洋の防空レーダー市場:国別分析

- アジア太平洋

- オーストラリア

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

第13章 COVID-19前後の影響

- COVID-19前後の影響

第14章 競合情勢

- 主要企業別ヒートマップ分析

- 企業のポジショニングと集中度

第15章 産業情勢

- 市場イニシアティブ

- 合併と買収

- 新規開発

第16章 企業プロファイル

- BAE Systems Plc

- General Dynamics Corp

- Honeywell International Inc

- Israel Aerospace Industries Ltd

- Leonardo SpA

- Lockheed Martin Corp

- Northrop Grumman Corp

- Raytheon Technologies Corp

- Saab AB

- Thales SA

第17章 付録

List Of Tables

- Table 1. Asia Pacific Air Defense Radar Market Segmentation

- Table 2. Asia Pacific Air Defense Radar Market Revenue And Forecasts to 2030 (US$ Mn)

- Table 3. Australia: Asia Pacific Air Defense Radar Market, By Product Type - Revenue and Forecast to 2030 (US$ Million)

- Table 4. Australia: Asia Pacific Air Defense Radar Market, By Range - Revenue and Forecast to 2030 (US$ Million)

- Table 5. Australia: Asia Pacific Air Defense Radar Market, By System Type - Revenue and Forecast to 2030 (US$ Million)

- Table 6. Australia: Asia Pacific Air Defense Radar Market, By Platform - Revenue and Forecast to 2030 (US$ Million)

- Table 7. Australia: Asia Pacific Air Defense Radar Market, By Application - Revenue and Forecast to 2030 (US$ Million)

- Table 8. China: Asia Pacific Air Defense Radar Market, By Product Type - Revenue and Forecast to 2030 (US$ Million)

- Table 9. China: Asia Pacific Air Defense Radar Market, By Range - Revenue and Forecast to 2030 (US$ Million)

- Table 10. China: Asia Pacific Air Defense Radar Market, By System Type - Revenue and Forecast to 2030 (US$ Million)

- Table 11. China: Asia Pacific Air Defense Radar Market, By Platform - Revenue and Forecast to 2030 (US$ Million)

- Table 12. China: Asia Pacific Air Defense Radar Market, By Application - Revenue and Forecast to 2030 (US$ Million)

- Table 13. India: Asia Pacific Air Defense Radar Market, By Product Type - Revenue and Forecast to 2030 (US$ Million)

- Table 14. India: Asia Pacific Air Defense Radar Market, By Range - Revenue and Forecast to 2030 (US$ Million)

- Table 15. India: Asia Pacific Air Defense Radar Market, By System Type - Revenue and Forecast to 2030 (US$ Million)

- Table 16. India: Asia Pacific Air Defense Radar Market, By Platform - Revenue and Forecast to 2030 (US$ Million)

- Table 17. India: Asia Pacific Air Defense Radar Market, By Application - Revenue and Forecast to 2030 (US$ Million)

- Table 18. Japan: Asia Pacific Air Defense Radar Market, By Product Type - Revenue and Forecast to 2030 (US$ Million)

- Table 19. Japan: Asia Pacific Air Defense Radar Market, By Range - Revenue and Forecast to 2030 (US$ Million)

- Table 20. Japan: Asia Pacific Air Defense Radar Market, By System Type - Revenue and Forecast to 2030 (US$ Million)

- Table 21. Japan: Asia Pacific Air Defense Radar Market, By Platform - Revenue and Forecast to 2030 (US$ Million)

- Table 22. Japan: Asia Pacific Air Defense Radar Market, By Application - Revenue and Forecast to 2030 (US$ Million)

- Table 23. South Korea: Asia Pacific Air Defense Radar Market, By Product Type - Revenue and Forecast to 2030 (US$ Million)

- Table 24. South Korea: Asia Pacific Air Defense Radar Market, By Range - Revenue and Forecast to 2030 (US$ Million)

- Table 25. South Korea: Asia Pacific Air Defense Radar Market, By System Type - Revenue and Forecast to 2030 (US$ Million)

- Table 26. South Korea: Asia Pacific Air Defense Radar Market, By Platform - Revenue and Forecast to 2030 (US$ Million)

- Table 27. South Korea: Asia Pacific Air Defense Radar Market, By Application - Revenue and Forecast to 2030 (US$ Million)

- Table 28. Rest of APAC: Asia Pacific Air Defense Radar Market, By Product Type - Revenue and Forecast to 2030 (US$ Million)

- Table 29. Rest of APAC: Asia Pacific Air Defense Radar Market, By Range - Revenue and Forecast to 2030 (US$ Million)

- Table 30. Rest of APAC: Asia Pacific Air Defense Radar Market, By System Type - Revenue and Forecast to 2030 (US$ Million)

- Table 31. Rest of APAC: Asia Pacific Air Defense Radar Market, By Platform - Revenue and Forecast to 2030 (US$ Million)

- Table 32. Rest of APAC: Asia Pacific Air Defense Radar Market, By Application - Revenue and Forecast to 2030 (US$ Million)

- Table 33. Company Positioning & Concentration

List Of Figures

- Figure 1. Asia Pacific Air Defense Radar Market Segmentation, By Country

- Figure 2. Asia Pacific Air Defense Radar Market - Porter's Five Forces Analysis

- Figure 3. Asia Pacific Air Defense Radar Market - Ecosystem Analysis

- Figure 4. Asia Pacific Air Defense Radar Market - Key Industry Dynamics

- Figure 5. Impact Analysis of Drivers and Restraints

- Figure 6. Asia Pacific Air Defense Radar Market Revenue (US$ Mn), 2020 - 2030

- Figure 7. Asia Pacific Air Defense Radar Market Revenue Share, By Function (2022 and 2030)

- Figure 8. Synthetic Aperture Radar and Moving Target Radar: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 9. Surveillance Radar: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 10. Airborne Early Warning Radar: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 11. Multi-Functional Radar: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 12. Weather Radar: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 13. Others: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 14. Asia Pacific Air Defense Radar Market Revenue Share, By Range (2022 and 2030)

- Figure 15. Short Range: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 16. Medium Range: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 17. Long Range: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 18. Asia Pacific Air Defense Radar Market Revenue Share, By System Type (2022 and 2030)

- Figure 19. Fixed Radar: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 20. Portable Radar: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 21. Asia Pacific Air Defense Radar Market Revenue Share, By Platform (2022 and 2030)

- Figure 22. Ground-Base: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 23. Aircraft-Mounted: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 24. Naval Based: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 25. Asia Pacific Air Defense Radar Market Revenue Share, By Application (2022 and 2030)

- Figure 26. Ballistic Missile Defense: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 27. Identification Friend or Foe: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 28. Weather Forecasting: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 29. Others: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- Figure 30. Asia Pacific Air Defense Radar Market Revenue, by Key Country (2022) (US$ Million)

- Figure 31. Asia Pacific Air Defense Radar Market Revenue Share, By Key Country (2022 and 2030) (%)

- Figure 32. Australia: Asia Pacific Air Defense Radar Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 33. China: Asia Pacific Air Defense Radar Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 34. India: Asia Pacific Air Defense Radar Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 35. Japan: Asia Pacific Air Defense Radar Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 36. South Korea: Asia Pacific Air Defense Radar Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 37. Rest of APAC: Asia Pacific Air Defense Radar Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 38. Pre & Post Covid-19 Impact

- Figure 39. Company Positioning & Concentration

The Asia Pacific air defense radar market is expected to grow from US$ 1,681.66 million in 2022 to US$ 2,669.98 million by 2030. It is estimated to grow at a CAGR of 5.9% from 2022 to 2030.

Development of Miniaturized and Low-Cost Radars Fuel the Asia Pacific Air Defense Radar Market

The development of miniaturized and low-cost radars is due to technological advancements, such as improved semiconductor manufacturing processes and the miniaturization of associated components. These advancements enable the development of smaller, lighter, and more cost-effective radar systems or miniaturized radar systems compared to traditional ones without compromising performance. Their compact form makes them more accessible and adaptable to different operational requirements and environments. This feature also allows easier integration of radars into various platforms, such as ground-based systems, naval vessels, or unmanned aerial vehicles (UAVs). The flexibility and adaptability of miniaturized radars make them suitable for diverse operational environments, expanding their market potential. Further, the various market players are focusing more on the cost efficiency of the air defense radar systems. For instance, radar systems such as multifunction radar systems offer enhanced operational efficiency by integrating multiple radar capabilities into a single platform. The ability to perform multiple tasks with a single system increases operational efficiency and cost-effectiveness. Thus, the market is witnessing the growing trend of miniaturized and low-cost radars development.

Asia Pacific Air Defense Radar Market Overview

The air defense radar market in Asia Pacific (APAC) is experiencing significant growth. The increasing regional tensions and geopolitical dynamics have led countries in Asia Pacific to enhance their defense capabilities. As a result, there is a growing demand for advanced air defense systems, including radars, to safeguard national security and territorial integrity. Moreover, rapid modernization and upgrade programs for existing air defense systems drive the Asia Pacific Air Defense Radar Market. Many countries in the region are investing heavily in upgrading their military equipment to match the evolving threat landscape. Upgrading radar systems is a crucial aspect of this modernization effort, as it enables early detection, tracking, and interception of aerial threats such as missiles, aircraft, and drones. APAC is investing generously in military technologies. For instance, in 2022, major countries in APAC (considered in the scope) invested US$ 541.4 billion in military technology. According to several military sources, the region accounted for more than 1,312 naval vessels in 2023. Also, countries such as China, India, Japan, and South Korea collaboratively commissioned ~52 naval vessels for future procurement across the region. This will further generate demand for air defense radar systems for naval vessels.

Advancements in radar technologies, such as active electronically scanned arrays (AESAs), have provided enhanced detection capabilities, increased operational range, and improved target tracking accuracy. These technological advancements have generated a surge in demand for next-generation air defense radar systems in Asia Pacific. Moreover, the rise of nontraditional security challenges, such as asymmetric warfare, terrorism, and cyber threats, has fueled the need for robust air defense radar systems. Governments are keen to develop comprehensive defense strategies encompassing conventional and unconventional threats, leading to increased investments in advanced radar technologies. Economic development and rise in defense budgets of countries in the region also support the growth of the Asia Pacific Air Defense Radar Market. Many countries, including China, India, Japan, and South Korea, have allocated substantial funds to enhance their defense capabilities, including air defense systems. This financial commitment has created a favorable environment for the growth of the Asia Pacific air defense radar market.

Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

Asia Pacific Air Defense Radar Market Segmentation

The Asia Pacific air defense radar market is segmented into function, range, system type, platform, application, and country.

Based on function, the Asia Pacific air defense radar market is segmented into synthetic aperture radar and moving target indicator radar, surveillance radar, airborne early warning radar, multi-functional radar, weather radar, and others. The synthetic aperture radar and moving target indicator radar segment held a larger share of the Asia Pacific air defense radar market in 2022.

Based on range, the Asia Pacific air defense radar market is segmented into short range, medium range, and long range. The medium range segment held the largest share of the Asia Pacific air defense radar market in 2022.

Based on system type, the Asia Pacific air defense radar market is segmented into fixed radar, and portable radar. The fixed radar segment held the largest share of the Asia Pacific air defense radar market in 2022.

Based on platform, the Asia Pacific air defense radar market is segmented into ground-base, aircraft-mounted, and naval based. The ground-base segment held the largest share of the Asia Pacific air defense radar market in 2022.

Based on application, the Asia Pacific air defense radar market is segmented into ballistic missile defense, identification friend or foe, weather forecasting, and others. The identification friend or foe segment held the largest share of the Asia Pacific air defense radar market in 2022.

Based on country, the Asia Pacific air defense radar market is segmented int o Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific air defense radar market in 2022.

BAE Systems Plc, General Dynamics Corp, Honeywell International Inc, Israel Aerospace Industries Ltd, Leonardo SpA, Lockheed Martin Corp, Northrop Grumman Corp, Raytheon Technologies Corp, Saab AB, and Thales SA are some of the leading companies operating in the Asia Pacific air defense radar market.

Reasons to Buy:

- Save and reduce time carrying out entry-level research by identifying the growth, size, leading players, and segments in the Asia Pacific Air Defense Radar Market.

- Highlights key business priorities in order to assist companies to realign their business strategies.

- The key findings and recommendations highlight crucial progressive industry trends in Asia Pacific Air Defense Radar Market, thereby allowing players across the value chain to develop effective long-term strategies.

- Develop/modify business expansion plans by using substantial growth offering developed and emerging markets.

- Scrutinize in-depth Asia Pacific Market trends and outlook coupled with the factors driving the market, as well as those hindering it.

- Enhance the decision-making process by understanding the strategies that underpin security interest with respect to client products, segmentation, pricing and distribution.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Asia Pacific Air Defense Radar Market Landscape

- 4.1 Overview

- 4.2 Porter's Five Forces Analysis

- 4.3 Ecosystem Analysis

- 4.3.1 Raw Material and Component Suppliers:

- 4.3.2 Air Defense Radar Manufacturers:

- 4.3.3 System Integrators & Software Developers:

- 4.3.4 End Users:

5. Asia Pacific Air Defense Radar Market - Key Industry Dynamics

- 5.1 Key Market Drivers:

- 5.1.1 Rise in Number of Contracts for Supply of Air Defense Radar

- 5.1.2 Continuous Rise in Defense Spending

- 5.1.3 Emergence of Network-Centric and Modern Warfare

- 5.2 Key Market Restraints:

- 5.2.1 Threat of Jamming and Spoofing

- 5.2.2 Decreasing Deployment of Aerostat Radars and Balloon Radars

- 5.3 Key Market Opportunities:

- 5.3.1 Rising Adoption of Unmanned Aerial Vehicles

- 5.3.2 Rise in Cross-Border Conflicts

- 5.4 Future Trend:

- 5.4.1 Development of Miniaturized and Low-Cost Radars

- 5.5 Impact of Drivers and Restraints:

6. Air Defense Radar Market - Asia Pacific Market Analysis

- 6.1 Asia Pacific Air Defense Radar Market Share, By Region (%), 2020 and 2030

- 6.2 Asia Pacific Air Defense Radar Market Revenue (US$ Mn), 2020 - 2030

7. Asia Pacific Air Defense Radar Market Analysis - Product Type

- 7.1 Overview

- 7.2 Asia Pacific Air Defense Radar Market Revenue Share, By Function (2022 and 2030)

- 7.3 Synthetic Aperture Radar & Moving Target Indicator Radar

- 7.3.1 Overview

- 7.3.2 Synthetic Aperture Radar and Moving Target Radar: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- 7.4 Surveillance Radar

- 7.4.1 Overview

- 7.4.2 Surveillance Radar: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- 7.5 Airborne Early Warning Radar

- 7.5.1 Overview

- 7.5.2 Airborne Early Warning Radar: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- 7.6 Multi-Functional Radar

- 7.6.1 Overview

- 7.6.2 Multi-Functional Radar: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- 7.7 Weather Radar

- 7.7.1 Overview

- 7.7.2 Weather Radar: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- 7.8 Others

- 7.8.1 Overview

- 7.8.2 Others: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

8. Asia Pacific Air Defense Radar Market Analysis - Range

- 8.1 Overview

- 8.2 Asia Pacific Air Defense Radar Market Revenue Share, By Range (2022 and 2030)

- 8.3 Short Range

- 8.3.1 Overview

- 8.3.2 Short Range: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- 8.4 Medium Range

- 8.4.1 Overview

- 8.4.2 Medium Range: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- 8.5 Long Range

- 8.5.1 Overview

- 8.5.2 Long Range: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

9. Asia Pacific Air Defense Radar Market Analysis - System Type

- 9.1 Overview

- 9.2 Asia Pacific Air Defense Radar Market Revenue Share, By System Type (2022 and 2030)

- 9.3 Fixed Radar

- 9.3.1 Overview

- 9.3.2 Fixed Radar: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- 9.4 Portable Radar

- 9.4.1 Overview

- 9.4.2 Portable Radar: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

10. Asia Pacific Air Defense Radar Market Analysis - Platform

- 10.1 Overview

- 10.2 Asia Pacific Air Defense Radar Market Revenue Share, By Platform (2022 and 2030)

- 10.3 Ground-Base

- 10.3.1 Overview

- 10.3.2 Ground-Base: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- 10.4 Aircraft-Mounted

- 10.4.1 Overview

- 10.4.2 Aircraft-Mounted: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- 10.5 Naval Based

- 10.5.1 Overview

- 10.5.2 Naval Based: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

11. Asia Pacific Air Defense Radar Market Analysis - Application

- 11.1 Overview

- 11.2 Asia Pacific Air Defense Radar Market Revenue Share, By Application (2022 and 2030)

- 11.3 Ballistic Missile Defense

- 11.3.1 Overview

- 11.3.2 Ballistic Missile Defense: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- 11.4 Identification Friend or Foe

- 11.4.1 Overview

- 11.4.2 Identification Friend or Foe: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- 11.5 Weather Forecasting

- 11.5.1 Overview

- 11.5.2 Weather Forecasting: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

- 11.6 Others

- 11.6.1 Overview

- 11.6.2 Others: Asia Pacific Air Defense Radar Market Revenue and Forecast to 2030 (US$ Million)

12. Asia Pacific Air Defense Radar Market - Country Analysis

- 12.1 Asia Pacific Air Defense Radar Market

- 12.1.1 Asia Pacific: Asia Pacific Air Defense Radar Market, by Key Country

- 12.1.1.1 Australia: Asia Pacific Air Defense Radar Market Revenue and Forecasts to 2030 (US$ Million)

- 12.1.1.1.1 Australia: Asia Pacific Air Defense Radar Market, By Product Type

- 12.1.1.1.2 Australia: Asia Pacific Air Defense Radar Market, By Range

- 12.1.1.1.3 Australia: Asia Pacific Air Defense Radar Market, By System Type

- 12.1.1.1.4 Australia: Asia Pacific Air Defense Radar Market, By Platform

- 12.1.1.1.5 Australia: Asia Pacific Air Defense Radar Market, By Application

- 12.1.1.2 China: Asia Pacific Air Defense Radar Market Revenue and Forecasts to 2030 (US$ Million)

- 12.1.1.2.1 China: Asia Pacific Air Defense Radar Market, By Product Type

- 12.1.1.2.2 China: Asia Pacific Air Defense Radar Market, By Range

- 12.1.1.2.3 China: Asia Pacific Air Defense Radar Market, By System Type

- 12.1.1.2.4 China: Asia Pacific Air Defense Radar Market, By Platform

- 12.1.1.2.5 China: Asia Pacific Air Defense Radar Market, By Application

- 12.1.1.3 India: Asia Pacific Air Defense Radar Market Revenue and Forecasts to 2030 (US$ Million)

- 12.1.1.3.1 India: Asia Pacific Air Defense Radar Market, By Product Type

- 12.1.1.3.2 India: Asia Pacific Air Defense Radar Market, By Range

- 12.1.1.3.3 India: Asia Pacific Air Defense Radar Market, By System Type

- 12.1.1.3.4 India: Asia Pacific Air Defense Radar Market, By Platform

- 12.1.1.3.5 India: Asia Pacific Air Defense Radar Market, By Application

- 12.1.1.4 Japan: Asia Pacific Air Defense Radar Market Revenue and Forecasts to 2030 (US$ Million)

- 12.1.1.4.1 Japan: Asia Pacific Air Defense Radar Market, By Product Type

- 12.1.1.4.2 Japan: Asia Pacific Air Defense Radar Market, By Range

- 12.1.1.4.3 Japan: Asia Pacific Air Defense Radar Market, By System Type

- 12.1.1.4.4 Japan: Asia Pacific Air Defense Radar Market, By Platform

- 12.1.1.4.5 Japan: Asia Pacific Air Defense Radar Market, By Application

- 12.1.1.5 South Korea: Asia Pacific Air Defense Radar Market Revenue and Forecasts to 2030 (US$ Million)

- 12.1.1.5.1 South Korea: Asia Pacific Air Defense Radar Market, By Product Type

- 12.1.1.5.2 South Korea: Asia Pacific Air Defense Radar Market, By Range

- 12.1.1.5.3 South Korea: Asia Pacific Air Defense Radar Market, By System Type

- 12.1.1.5.4 South Korea: Asia Pacific Air Defense Radar Market, By Platform

- 12.1.1.5.5 South Korea: Asia Pacific Air Defense Radar Market, By Application

- 12.1.1.6 Rest of APAC: Asia Pacific Air Defense Radar Market Revenue and Forecasts to 2030 (US$ Million)

- 12.1.1.6.1 Rest of APAC: Asia Pacific Air Defense Radar Market, By Product Type

- 12.1.1.6.2 Rest of APAC: Asia Pacific Air Defense Radar Market, By Range

- 12.1.1.6.3 Rest of APAC: Asia Pacific Air Defense Radar Market, By System Type

- 12.1.1.6.4 Rest of APAC: Asia Pacific Air Defense Radar Market, By Platform

- 12.1.1.6.5 Rest of APAC: Asia Pacific Air Defense Radar Market, By Application

- 12.1.1.1 Australia: Asia Pacific Air Defense Radar Market Revenue and Forecasts to 2030 (US$ Million)

- 12.1.1 Asia Pacific: Asia Pacific Air Defense Radar Market, by Key Country

13. Pre & Post Covid-19 Impact

- 13.1 Pre & Post Covid-19 Impact

14. Competitive Landscape

- 14.1 Heat Map Analysis By Key Players

- 14.2 Company Positioning & Concentration

15. Industry Landscape

- 15.1 Overview

- 15.2 Market Initiative

- 15.3 Merger and Acquisition

- 15.4 New Development

16. Company Profiles

- 16.1 BAE Systems Plc

- 16.1.1 Key Facts

- 16.1.2 Business Description

- 16.1.3 Products and Services

- 16.1.4 Financial Overview

- 16.1.5 SWOT Analysis

- 16.1.6 Key Developments

- 16.2 General Dynamics Corp

- 16.2.1 Key Facts

- 16.2.2 Business Description

- 16.2.3 Products and Services

- 16.2.4 Financial Overview

- 16.2.5 SWOT Analysis

- 16.2.6 Key Developments

- 16.3 Honeywell International Inc

- 16.3.1 Key Facts

- 16.3.2 Business Description

- 16.3.3 Products and Services

- 16.3.4 Financial Overview

- 16.3.5 SWOT Analysis

- 16.3.6 Key Developments

- 16.4 Israel Aerospace Industries Ltd

- 16.4.1 Key Facts

- 16.4.2 Business Description

- 16.4.3 Products and Services

- 16.4.4 Financial Overview

- 16.4.5 SWOT Analysis

- 16.4.6 Key Developments

- 16.5 Leonardo SpA

- 16.5.1 Key Facts

- 16.5.2 Business Description

- 16.5.3 Products and Services

- 16.5.4 Financial Overview

- 16.5.5 SWOT Analysis

- 16.5.6 Key Developments

- 16.6 Lockheed Martin Corp

- 16.6.1 Key Facts

- 16.6.2 Business Description

- 16.6.3 Products and Services

- 16.6.4 Financial Overview

- 16.6.5 SWOT Analysis

- 16.6.6 Key Developments

- 16.7 Northrop Grumman Corp

- 16.7.1 Key Facts

- 16.7.2 Business Description

- 16.7.3 Products and Services

- 16.7.4 Financial Overview

- 16.7.5 SWOT Analysis

- 16.7.6 Key Developments

- 16.8 Raytheon Technologies Corp

- 16.8.1 Key Facts

- 16.8.2 Business Description

- 16.8.3 Products and Services

- 16.8.4 Financial Overview

- 16.8.5 SWOT Analysis

- 16.8.6 Key Developments

- 16.9 Saab AB

- 16.9.1 Key Facts

- 16.9.2 Business Description

- 16.9.3 Products and Services

- 16.9.4 Financial Overview

- 16.9.5 SWOT Analysis

- 16.9.6 Key Developments

- 16.10 Thales SA

- 16.10.1 Key Facts

- 16.10.2 Business Description

- 16.10.3 Products and Services

- 16.10.4 Financial Overview

- 16.10.5 SWOT Analysis

- 16.10.6 Key Developments

17. Appendix

- 17.1 Appendix