|

|

市場調査レポート

商品コード

1402722

北米のクリニック向けギプス・スプリント製品の2030年までの市場予測- 地域別分析- 製品別、用途別、材料別North America Clinic Casting and Splinting Products Market Forecast to 2030 - Regional Analysis - by Product, Application (Acute Fractures or Sprains, Tendon and Ligament Injuries, and Others), and Material (Plaster of Paris, Fiberglass, and Others) |

||||||

|

|

|||||||

|

|||||||

| 北米のクリニック向けギプス・スプリント製品の2030年までの市場予測- 地域別分析- 製品別、用途別、材料別 |

|

出版日: 2023年11月01日

発行: The Insight Partners

ページ情報: 英文 87 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

北米のクリニック向けギプス・スプリント製品市場は、2022年の5億6,748万米ドルから2030年には8億6,947万米ドルに成長すると予測されています。2022年から2030年までのCAGRは5.5%と推定されます。

筋骨格系疾患の有病率の上昇が北米のクリニック向けギプス・スプリント製品市場を活性化

世界保健機関(WHO)によると、筋骨格系疾患は世界中で障害の主要原因となっており、腰痛は160カ国で障害の単一の主要原因となっています。筋骨格系疾患は、2019年、障害とともに生きた年数(YLDs)で世界第1位、障害調整生存年(DALYs)で世界第6位となった。WHOによると、2021年には全世界で17億1,000万人が筋骨格系疾患に罹患しています。National Library of Medicineに掲載された「Global prevalence of musculoskeletal disorders among physiotherapists:a systematic review and meta-analysis」と題する研究によると、米国では筋骨格系疾患の罹患率が増加しています。

関節リウマチ(RA)、変形性関節症(OA)、腰痛(LBP)、頚部痛(NP)などは、一般的な筋骨格系疾患です。2023年にSpringer Natureが発表した論文によると、主要自己免疫性リウマチ性疾患の一つである関節リウマチは、世界中で1,400万人が罹患しています。関節痛は専門医を紹介される最も一般的な理由です。ギプスやスプリントは様々な筋骨格系疾患の管理に使用されます。合併症を最小限に抑えながら効果を最大化するため、ギプスやスプリントの使用は一般的に短期間に限られています。従って、筋骨格系疾患の罹患率の上昇が北米のクリニック向けギプス・スプリント製品市場の成長を促進しています。

北米のクリニック向けギプス・スプリント製品市場概要

北米のクリニック向けギプス・スプリント製品市場は、米国、カナダ、メキシコにセグメント化されており、この地域の市場成長に大きく貢献しています。北米のクリニック向けギプス・スプリント製品市場は、骨粗鬆症や筋骨格系の損傷率の上昇、高齢者人口の増加による加齢関連整形外科疾患の増加により成長しています。さらに、慎重に検討された償還規制が、高価なギプスやスプリント製品へのアクセスを可能にし、市場の成長を支えています。

United States Bone and Joint Initiative(USBJI)によると、米国では筋骨格系疾患が65歳以上のほぼ4人に3人、18歳以上の2人に1人に影響を及ぼしています。米国疾病予防管理センター(CDC)によると、2019年には米国の成人のうち5,410万人が65歳以上で、人口の16%を占めています。2040年には、高齢者の数は8,080万人に達すると予想されています。2060年には9,470万人に達し、高齢者は米国人口の25%近くを占めることになります。整形外科的損傷は、高齢者の身体における生物学的変化のため、高齢者人口によく見られます。高齢になるにつれ、骨密度は低下します。筋骨格系疾患は、米国人口の高齢化に伴い、年々大きな負担となっています。高齢者が直面する深刻な問題の一つは骨折です。さらに、骨密度や骨質の低下を引き起こす代謝性骨疾患である骨粗鬆症は、米国では健康面でも経済面でも大きな負担となっています。骨折はどの骨にも起こりうるが、股関節と脊椎の骨折が最も多く、骨粗鬆症性骨折全体の42%を占める。米国では年間70万件以上の椎体圧迫骨折が発生しています。米国では、50歳以上の女性の2人に1人が、生涯のうちに骨粗鬆症に関連した骨折を経験しています。

様々な筋骨格系の疾患の管理には、ギプスやスプリントの使用が必要です。スプリントは、腫れに対応する非周囲固定具です。この性質により、スプリントは、急性骨折や捻挫、あるいは整形外科的介入前の、縮小骨折、転位骨折、不安定骨折の初期安定化など、腫脹が予測される様々な急性筋骨格系状態の管理に理想的です。したがって、筋骨格系疾患と骨粗鬆症の有病率の上昇は、米国におけるギプス・スプリント製品の需要を押し上げると思われます。

北米のクリニック向けギプス・スプリント製品の市場収益と2030年までの予測(金額)

北米のクリニック向けギプス・スプリント製品市場のセグメンテーション

北米のクリニック向けギプス・スプリント製品市場は、製品、用途、材料、国に区分されます。

製品別では、北米のクリニック向けギプス・スプリント製品市場はキャスティングとスプリントに区分されます。2022年の北米のクリニック向けギプス・スプリント製品市場では、ギプス部門が大きなシェアを占めています。キャスティングは、ギプス、テープ、カッター、キャスティング用付属品に細分化されます。スプリント分野はさらにスプリントとスプリント用付属品に細分化されます。

用途別では、北米のクリニック向けギプス・スプリント製品市場は、急性骨折または捻挫、腱と靭帯損傷、その他に区分されます。2022年には、急性骨折セグメントが北米のクリニック向けギプス・スプリント製品市場で最大のシェアを占めました。

材料別では、北米のクリニック向けギプス・スプリント製品市場はパリ石膏、グラスファイバー、その他に区分されます。パリ石膏セグメントが2022年の北米のクリニック向けギプス・スプリント製品市場で最大のシェアを占めています。

国別では、北米のクリニック向けギプス・スプリント製品市場は米国、カナダ、メキシコに区分されます。2022年の北米のクリニック向けギプス・スプリント製品市場は米国が支配的でした。

3M Co、Corflex Inc、DeRoyal Industries Inc、Dynatronics Corporation、Enovis Corp、Essity AB、Ossur hf、Performance Health Holding Inc、Zimmer Biomet Holdings Incは、北米のクリニック用ギプスとスプリント製品市場で事業を展開している大手企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要な洞察

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 北米のクリニック向けギプス・スプリント製品市場情勢

- 概観

- PEST分析

- 北米PEST分析

- エコシステム分析

- バリューチェーンのベンダー一覧

第5章 北米のクリニック向けギプス・スプリント製品市場:主要産業力学

- 市場促進要因

- 筋骨格系疾患の有病率の上昇

- 加齢に伴う整形外科疾患の高い有病率

- 主要市場抑制要因

- ギプス固定とスプリントに関する合併症

- 主要市場機会

- ギプス包帯とスプリントにおける3D技術の進歩

- 今後の動向

- ギプス包帯とスプリントにおけるファイバーグラス材料の採用増加

- 影響分析

第6章 クリニック向けギプス・スプリント製品市場:北米市場分析

- 北米のクリニック向けギプス・スプリント製品の市場収益(2022~2030年)

第7章 北米のクリニック向けギプス・スプリント製品市場:2030年までの収益と予測:製品別

- イントロダクション

- 北米のクリニック向けギプス・スプリント製品市場:2022年と2030年の製品別売上高シェア(%)

- ギプス包帯

- スプリント

第8章 北米のクリニック向けギプス・スプリント製品市場:2030年までの収益と予測:用途別

- イントロダクション

- 北米のクリニック向けギプス・スプリント製品市場:2022年と2030年の用途別売上高シェア(%)

- 急性骨折または捻挫

- 腱と靭帯損傷

- その他

第9章 北米のクリニック向けギプス・スプリント製品市場:2030年までの収益と予測:材料別

- イントロダクション

- 北米のクリニック向けギプス・スプリント製品市場:2022年と2030年の材料別売上高シェア(%)

- パリ石膏

- ガラス繊維

- その他

第10章 北米のクリニック向けギプス・スプリント製品市場:2030年までの収益と予測:国別分析

第11章 北米のギプス・ギブス市場-業界情勢

- イントロダクション

- 最近の成長戦略

第12章 企業プロファイル

- DeRoyal Industries Inc

- 3M Co

- Corflex Inc

- Essity AB

- Dynatronics Corporation

- Zimmer Biomet Holdings Inc

- Ossur hf

- Performance Health Holding Inc

- Enovis Corp

第13章 付録

List Of Tables

- Table 1. North America Clinic Casting and Splinting Products Market Segmentation

- Table 2. List of Vendors

- Table 3. US North America Clinic Casting and Splinting Products Market, by Product - Revenue and Forecast to 2030 (US$ Million)

- Table 4. US North America Clinic Casting and Splinting Products Market, For Casting by Product - Revenue and Forecast to 2030 (US$ Million)

- Table 5. US North America Clinic Casting and Splinting Products Market, For Splinting by Product - Revenue and Forecast to 2030 (US$ Million)

- Table 6. US North America Clinic Casting and Splinting Products Market, by Application - Revenue and Forecast to 2030 (US$ Million)

- Table 7. US North America Clinic Casting and Splinting Products Market, by Material - Revenue and Forecast to 2030 (US$ Million)

- Table 8. Canada North America Clinic Casting and Splinting Products Market, by Product - Revenue and Forecast to 2030 (US$ Million)

- Table 9. Canada North America Clinic Casting and Splinting Products Market, For Casting by Product - Revenue and Forecast to 2030 (US$ Million)

- Table 10. Canada North America Clinic Casting and Splinting Products Market, For Splinting by Product - Revenue and Forecast to 2030 (US$ Million)

- Table 11. Canada North America Clinic Casting and Splinting Products Market, by Application - Revenue and Forecast to 2030 (US$ Million)

- Table 12. Canada North America Clinic Casting and Splinting Products Market, by Material - Revenue and Forecast to 2030 (US$ Million)

- Table 13. Mexico North America Clinic Casting and Splinting Products Market, by Product - Revenue and Forecast to 2030 (US$ Million)

- Table 14. Mexico North America Clinic Casting and Splinting Products Market, For Casting by Product - Revenue and Forecast to 2030 (US$ Million)

- Table 15. Mexico North America Clinic Casting and Splinting Products Market, For Splinting by Product - Revenue and Forecast to 2030 (US$ Million)

- Table 16. Mexico North America Clinic Casting and Splinting Products Market, by Application - Revenue and Forecast to 2030 (US$ Million)

- Table 17. Mexico North America Clinic Casting and Splinting Products Market, by Material - Revenue and Forecast to 2030 (US$ Million)

- Table 18. Recent Growth Strategies in Clinic Casting and Splinting Products Market

- Table 19. Glossary of Terms, Digital Thoracic Drainage Devices Market

List Of Figures

- Figure 1. North America Clinic Casting and Splinting Products Market Segmentation, By Country

- Figure 2. North America - PEST Analysis

- Figure 3. North America Clinic Casting and Splinting Products Market: Key Industry Dynamics

- Figure 4. North America Clinic Casting and Splinting Products Market: Impact Analysis of Drivers and Restraints

- Figure 5. North America Clinic Casting and Splinting Products Market Revenue (US$ Mn), 2020 - 2030

- Figure 6. North America Clinic Casting and Splinting Products Market Revenue Share, by Product 2022 & 2030 (%)

- Figure 7. Casting: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 8. Casts: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 9. Tapes: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 10. Cutters: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 11. Casting Accessories: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 12. Splinting: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 13. Splints: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 14. Splinting Accessories: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 15. North America Clinic Casting and Splinting Products Market Revenue Share, by Application 2022 & 2030 (%)

- Figure 16. Acute Fracture or Sprains: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 17. Tendon and Ligament Injuries: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 18. Others: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 19. North America Clinic Casting and Splinting Products Market Revenue Share, by Material 2022 & 2030 (%)

- Figure 20. Plaster of Paris: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 21. Fiberglass: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 22. Others: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 23. North America: North America Clinic Casting and Splinting Products Market, by Key Country - Revenue (2022) (US$ Million)

- Figure 24. North America: North America Clinic Casting and Splinting Products Market, by Country, 2022 & 2030 (%)

- Figure 25. US: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 26. Canada: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 27. Mexico: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

The North America clinic casting and splinting products market is expected to grow from US$ 567.48 million in 2022 to US$ 869.47 million by 2030. It is estimated to grow at a CAGR of 5.5% from 2022 to 2030.

Rising Prevalence of Musculoskeletal Conditions Fuels North America Clinic Casting and Splinting Products Market

According to the World Health Organization (WHO) musculoskeletal conditions are the leading cause of disability across the world, and low back pain is the single leading cause of disability in 160 countries. Musculoskeletal disorders ranked first in years lived with disability (YLDs) and sixth in disability-adjusted life-years (DALYs) globally in 2019. According to WHO, ~1.71 billion people across the world had musculoskeletal conditions in 2021. According to a study titled "Global prevalence of musculoskeletal disorders among physiotherapists: a systematic review and meta-analysis" published in the National Library of Medicine, there has been an increase in the incidence of musculoskeletal diseases in the US.

Rheumatoid arthritis (RA), osteoarthritis (OA), low-back pain (LBP), and neck pain (NP) are a few common musculoskeletal conditions. According to an article published by Springer Nature in 2023, rheumatoid arthritis, one of the main autoimmune rheumatic diseases, affects 14 million people worldwide. Joint pain is the most common reason for specialist referrals. Cast or splint is used in the management of various musculoskeletal conditions. To maximize benefits while minimizing complications, the use of casts and splints is generally limited to the short term. Thus, the rising incidence of musculoskeletal conditions is driving the growth of the North America clinic casting and splinting products market .

North America Clinic Casting and Splinting Products Market Overview

The North America clinic casting and splinting products market has been segmented into the US, Canada, and Mexico; being the major contributors to the market growth in this region. The North America casting and splinting market is growing because of the rising rates of osteoporosis and musculoskeletal injuries and increased rates of age-related orthopedic disorders brought on by the growing geriatric population. Furthermore, carefully thought-out reimbursement regulations enable access to pricey casting and splinting equipment, supporting market growth.

According to the United States Bone and Joint Initiative (USBJI), musculoskeletal diseases affect nearly three out of four people aged 65 and over and one in every two persons aged 18 and above in the US. According to Centers for Disease Control and Prevention (CDC), in 2019, 54.1 million US adults were 65 or older, representing 16% of the population. By 2040, the number of older adults is expected to reach 80.8 million. By 2060, it will reach 94.7 million, and older adults will make up nearly 25% of the US population. Orthopedic injuries are common in the aging population due to biological changes in older adults' bodies. As people grow older, their bone mineral density decreases. Musculoskeletal diseases are becoming a greater burden every year with the aging US population. One of the serious problems facing the elderly is fractures. Moreover, osteoporosis, a metabolic bone disease that causes reduced mineral density and quality of bone, is a significant health and economic burden in the US. Fractures can occur in any bone; however, hip and spine fractures are the most common, accounting for 42% of all osteoporotic fractures. More than 700,000 vertebral body compression fractures occur per year in the United States. In the US, one in two women over 50 have an osteoporosis-related bone break in their lifetime.

The management of a wide variety of musculoskeletal conditions requires the use of a cast or splint. Splints are noncircumferential immobilizers that accommodate swelling. This quality makes splints ideal for the management of a variety of acute musculoskeletal conditions in which swelling is anticipated, such as acute fractures or sprains or initial stabilization of reduced, displaced, or unstable fractures before orthopedic intervention. Thus, the rising prevalence of musculoskeletal conditions and osteoporosis will boost the demand for casting and splinting products in the US.

North America Clinic Casting and Splinting Products Market Revenue and Forecast to 2030 (US$ Million)

North America Clinic Casting and Splinting Products Market Segmentation

The North America clinic casting and splinting products market is segmented into product, application, material, and country.

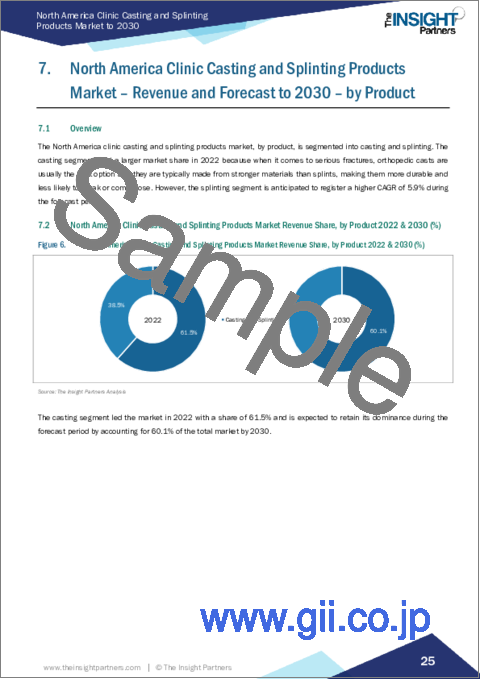

Based on product, the North America clinic casting and splinting products market is segmented into casting and splinting. The casting segment held a larger share of the North America clinic casting and splinting products market in 2022. The casting is sub-segmented into casts, tapes, cutters, and casting accessories. The splinting segment is further segmented into splints and splinting accessories.

Based on application, the North America clinic casting and splinting products market is segmented into acute fractures or sprains, tendon and ligament injuries, and others. The acute fractures segment held the largest share of the North America clinic casting and splinting products market in 2022.

Based on material, the North America clinic casting and splinting products market is segmented into Plaster of Paris, fiberglass, and others. The Plaster of Paris segment held the largest share of the North America clinic casting and splinting products market in 2022.

Based on country, the North America clinic casting and splinting products market is segmented into the US, Canada, and Mexico. The US dominated the North America clinic casting and splinting products market in 2022.

3M Co, Corflex Inc, DeRoyal Industries Inc, Dynatronics Corporation, Enovis Corp, Essity AB, Ossur hf, Performance Health Holding Inc, and Zimmer Biomet Holdings Inc are some of the leading companies operating in the North America clinic casting and splinting products market.

Reasons to Buy:

- Save and reduce time carrying out entry-level research by identifying the growth, size, leading players, and segments in the North America Clinic Casting and Splinting Products Market.

- Highlights key business priorities in order to assist companies to realign their business strategies.

- The key findings and recommendations highlight crucial progressive industry trends in the North America Clinic Casting and Splinting Products Market, thereby allowing players across the value chain to develop effective long-term strategies.

- Develop/modify business expansion plans by using substantial growth offering developed and emerging markets.

- Scrutinize in-depth North America market trends and outlook coupled with the factors driving the market, as well as those hindering it.

- Enhance the decision-making process by understanding the strategies that underpin security interest with respect to client products, segmentation, pricing and distribution.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. North America Clinic Casting and Splinting Products Market Landscape

- 4.1 Overview

- 4.2 PEST Analysis

- 4.2.1 North America PEST Analysis

- 4.3 Ecosystem Analysis

- 4.3.1 List of Vendors in the Value Chain

5. North America Clinic Casting and Splinting Products Market - Key Industry Dynamics

- 5.1 Market Drivers

- 5.1.1 Rising Prevalence of Musculoskeletal Conditions

- 5.1.2 High Prevalence of Age-Related Orthopedic Disorders

- 5.2 Key Market Restraints

- 5.2.1 Complications Related to Casting and Splinting

- 5.3 Key Market Opportunities

- 5.3.1 Advancements in 3D Technology in Casting and Splinting

- 5.4 Future Trends

- 5.4.1 Rising Adoption of Fiberglass Material for Casting and Splinting

- 5.5 Impact Analysis

6. Clinic Casting and Splinting Products Market - North America Market Analysis

- 6.1 North America Clinic Casting and Splinting Products Market Revenue (US$ Mn), 2022 - 2030

7. North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 - by Product

- 7.1 Overview

- 7.2 North America Clinic Casting and Splinting Products Market Revenue Share, by Product 2022 & 2030 (%)

- 7.3 Casting

- 7.3.1 Overview

- 7.3.2 Casting: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 7.3.2.1 Casts

- 7.3.2.1.1 Overview

- 7.3.2.1.2 Casts: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 7.3.2.2 Tapes

- 7.3.2.2.1 Overview

- 7.3.2.2.2 Tapes: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 7.3.2.3 Cutters

- 7.3.2.3.1 Overview

- 7.3.2.3.2 Cutters: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 7.3.2.4 Casting Accessories

- 7.3.2.4.1 Overview

- 7.3.2.4.2 Casting Accessories: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 7.3.2.1 Casts

- 7.4 Splinting

- 7.4.1 Overview

- 7.4.2 Splinting: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 7.4.2.1 Splints

- 7.4.2.1.1 Overview

- 7.4.2.1.2 Splints: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 7.4.2.2 Splinting Accessories

- 7.4.2.2.1 Overview

- 7.4.2.2.2 Splinting Accessories: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 7.4.2.1 Splints

8. North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 - by Application

- 8.1 Overview

- 8.2 North America Clinic Casting and Splinting Products Market Revenue Share, by Application 2022 & 2030 (%)

- 8.3 Acute Fracture or Sprains

- 8.3.1 Overview

- 8.3.2 Acute Fracture or Sprains: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 8.4 Tendon and Ligament Injuries

- 8.4.1 Overview

- 8.4.2 Tendon and Ligament Injuries: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 8.5 Others

- 8.5.1 Overview

- 8.5.2 Others: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

9. North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 - by Material

- 9.1 Overview

- 9.2 North America Clinic Casting and Splinting Products Market Revenue Share, by Material 2022 & 2030 (%)

- 9.3 Plaster of Paris

- 9.3.1 Overview

- 9.3.2 Plaster of Paris: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 9.4 Fiberglass

- 9.4.1 Overview

- 9.4.2 Fiberglass: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 9.5 Others

- 9.5.1 Overview

- 9.5.2 Others: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

10. North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 - Country Analysis

- 10.1 North America Clinic Casting and Splinting Products Market

- 10.1.1 Overview

- 10.1.1.1 US: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.1.1 Overview

- 10.1.1.1.2 US: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.1.3 US: North America Clinic Casting and Splinting Products Market, by Product, 2020-2030 (US$ Million)

- 10.1.1.1.3.1 US: North America Clinic Casting and Splinting Products Market, For Casting by Product, 2020-2030 (US$ Million)

- 10.1.1.1.3.2 US: North America Clinic Casting and Splinting Products Market, For Splinting by Product, 2020-2030 (US$ Million)

- 10.1.1.1.4 US: North America Clinic Casting and Splinting Products Market, by Application, 2020-2030 (US$ Million)

- 10.1.1.1.5 US: North America Clinic Casting and Splinting Products Market, by Material, 2020-2030 (US$ Million)

- 10.1.1.2 Canada: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.2.1 Overview

- 10.1.1.2.2 Canada: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.2.3 Canada: North America Clinic Casting and Splinting Products Market, by Product, 2020-2030 (US$ Million)

- 10.1.1.2.3.1 Canada: North America Clinic Casting and Splinting Products Market, For Casting by Product, 2020-2030 (US$ Million)

- 10.1.1.2.3.2 Canada: North America Clinic Casting and Splinting Products Market, For Splinting by Product, 2020-2030 (US$ Million)

- 10.1.1.2.4 Canada: North America Clinic Casting and Splinting Products Market, by Application, 2020-2030 (US$ Million)

- 10.1.1.2.5 Canada: North America Clinic Casting and Splinting Products Market, by Material, 2020-2030 (US$ Million)

- 10.1.1.3 Mexico: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.3.1 Overview

- 10.1.1.3.2 Mexico: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.3.3 Mexico: North America Clinic Casting and Splinting Products Market, by Product, 2020-2030 (US$ Million)

- 10.1.1.3.3.1 Mexico: North America Clinic Casting and Splinting Products Market, For Casting by Product, 2020-2030 (US$ Million)

- 10.1.1.3.3.2 Mexico: North America Clinic Casting and Splinting Products Market, For Splinting by Product, 2020-2030 (US$ Million)

- 10.1.1.3.4 Mexico: North America Clinic Casting and Splinting Products Market, by Application, 2020-2030 (US$ Million)

- 10.1.1.3.5 Mexico: North America Clinic Casting and Splinting Products Market, by Material, 2020-2030 (US$ Million)

- 10.1.1.1 US: North America Clinic Casting and Splinting Products Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1 Overview

11. North America Clinic Casting and Splinting Products Market-Industry Landscape

- 11.1 Overview

- 11.2 Recent Growth Strategies

- 11.2.1 Overview

12. Company Profiles

- 12.1 DeRoyal Industries Inc

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 3M Co

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 Corflex Inc

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Essity AB

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Dynatronics Corporation

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 Zimmer Biomet Holdings Inc

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 Ossur hf

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 Performance Health Holding Inc

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 Enovis Corp

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

13. Appendix

- 13.1 About Us

- 13.2 Glossary of Terms