|

|

市場調査レポート

商品コード

1375100

南米のリグニン市場の2028年までの予測-地域別分析-タイプ、形態、用途別South America Lignin Market Forecast to 2028 - COVID-19 Impact and Regional Analysis - by Type, Form, and Application |

||||||

|

|

|||||||

| 南米のリグニン市場の2028年までの予測-地域別分析-タイプ、形態、用途別 |

|

出版日: 2023年08月22日

発行: The Insight Partners

ページ情報: 英文 121 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

南米のリグニン市場は2022年に2,728万9,610米ドルと評価され、2028年には3,526万1,050米ドルに達すると予測され、2022年から2028年までのCAGRは4.4%で成長すると予測されています。

新興国市場の主な参入企業による戦略的発展への取り組み

リグニンメーカーは、幅広い顧客層を獲得し市場での地位を高めるため、製品革新、M&A、事業拡大などの戦略的開拓に多額の投資を行っています。さらに、リグニンに対する需要は、環境問題や持続可能性の問題の高まりにより、最終用途産業の間で増加しています。例えば、2021年12月、Nippon Paper(日本)とStora Enso Oyj(フィンランド)は、樹木を利用してバッテリー業界に革命を起こすためのパートナーシップ契約を締結しました。両社の調査は、リチウムイオン電池やレアメタル電池をリグニンに置き換えることに焦点を当てた。このような製品イノベーションは、企業が国際市場で競争上の優位性を獲得するのに役立ちます。

大手メーカーは、顧客により良いサービスを提供し、高まる需要を満たすために、買収、拡大、生産能力の拡大といった独創的な戦略を採用しています。したがって、メーカーによる戦略的な取り組みが、予測期間中のリグニン市場の成長を促進すると予想されます。

南米のリグニン市場概要

南米では、パルプと紙の生産と輸出の増加により、パルプ・製紙産業の存在感が高まっています。2020年には、ブラジルが1,500万トン以上のパルプを輸出して世界ランキングのトップに立ち、世界の主要な原料供給国となっています。リグニンは主にパルプ・製紙工場とセルロース系バイオリファイナリーから供給されます。リグニンは、コスト効率が高く、無公害の生分解性ポリマーであるため、生分解性を改善するために市販のポリマーに使用されています。地域全体の紙・パルプ需要の増加を緩和するため、多くのバイオベース原料メーカーがイニシアチブを取り、生産能力の拡大に注力しています。例えば、2021年5月12日、南米のユーカリ・パルプ・メーカーであるスザノSAは、ブラジルに年産230万トンのパルプ工場を28億米ドルで新設すると発表しました。各メーカーによるこうした拡張プロジェクトは、同地域全体の紙パルプの高い生産性に寄与しており、リグニン市場の成長を後押ししています。

南米のリグニン市場の収益と2028年までの予測(千米ドル)

南米のリグニン市場のセグメンテーション

南米のリグニン市場は、タイプ、形態、用途、国によって区分されます。タイプ別では、南米のリグニン市場はリグノスルホン酸塩、クラフトリグニン、高純度リグニン、その他に区分されます。2022年の南米リグニン市場シェアはリグノスルホネートセグメントが最大でした。

南米のリグニン市場は形態によって固体と液体に二分されます。2022年には固体セグメントがより大きな市場シェアを占めました。

用途別では、南米リグニン市場はコンクリート添加剤、プラスチック・ポリマー、アスファルト、水処理、染料・顔料、活性炭、炭素繊維、その他に区分されます。2022年にはその他セグメントが最大の市場シェアを占めました。

国別に見ると、南米のリグニン市場はブラジル、アルゼンチン、その他南米に区分されます。2022年の南米リグニン市場シェアはブラジルが独占。

Nippon Paper Industries Co Ltd、Borregaard ASA、Burgo Group SpA、Domsjo Fabriker AB、Sappi Ltd、Stora Enso Oyj、Suzano SA、The Dallas Group of America Incが南米リグニン市場の主要企業です。

目次

第1章 イントロダクション

第2章 キーポイント

第3章 調査手法

- 調査範囲

- 調査手法

- データ収集

- 一次インタビュー

- 仮説の策定

- マクロ経済要因分析

- 基礎数値の作成

- データの三角測量

- 国レベルのデータ

第4章 南米リグニン市場情勢

- 市場概要

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力:新規参入の脅威

- 競争企業間の敵対関係の強さ

- 代替品の脅威

- エコシステム分析

- 原材料

- 生産プロセス

- 最終用途産業

- 専門家の見解

第5章 南米リグニン市場:主要市場力学

- 市場促進要因

- 複数の最終用途産業からのリグニン需要の増加

- 市場抑制要因

- リグニンの代替品の入手可能性

- 市場機会

- 炭素繊維生産へのリグニンの採用

- 今後の動向

- 新興国市場の主な参入企業による戦略的発展への取り組み

- 促進要因と抑制要因の影響分析

第6章 リグニン-南米市場分析

- 南米のリグニン市場-2028年までの数量と予測

第7章 南米リグニン市場分析-タイプ別

- 南米のリグニン市場:タイプ別(2021年、2028年)

- リグノスルホン酸塩

- クラフトリグニン

- 高純度リグニン

- その他

第8章 南米リグニン市場分析:形態別

- リグニン市場:形態別(2021年、2028年)

- 固体

- 液体

第9章 南米リグニン市場の分析-用途別

- リグニン市場:用途別(2021年、2028年)

- コンクリート添加剤

- プラスチックおよびポリマー

- ビチューメン

- 水処理

- 染料・顔料

- 活性炭

- 炭素繊維

- その他

第10章 南米リグニン市場:国別分析

- 南米

第11章 業界情勢

- 市場イニシアティブ

- パートナーシップとコラボレーション

第12章 企業プロファイル

- Nippon Paper Industries Co Ltd

- Borregaard ASA

- Burgo Group SpA

- Domsjo Fabriker AB

- Sappi Ltd

- Stora Enso Oyj

- Suzano SA

- The Dallas Group of America Inc

第13章 付録

List Of Tables

- Table 1. South America Lignin Market -Volume and Forecast to 2028 (Tons)

- Table 2. South America Lignin Market -Revenue and Forecast to 2028 (US$ Thousand)

- Table 3. Brazil Lignin Market, by Type - Revenue and Forecast to 2028 (US$ Thousand)

- Table 4. Brazil Lignin Market, by Type - Volume and Forecast to 2028 (Tons)

- Table 5. Brazil Lignin Market, by Form - Revenue and Forecast to 2028 (US$ Thousand)

- Table 6. Brazil Lignin Market, by Application - Revenue and Forecast to 2028 (US$ Thousand)

- Table 7. Argentina Lignin Market, by Type - Revenue and Forecast to 2028 (US$ Thousand)

- Table 8. Argentina Lignin Market, by Type - Volume and Forecast to 2028 (Tons)

- Table 9. Argentina Lignin Market, by Form - Revenue and Forecast to 2028 (US$ Thousand)

- Table 10. Argentina Lignin Market, by Application - Revenue and Forecast to 2028 (US$ Thousand)

- Table 11. Rest of South America Lignin Market, by Type - Revenue and Forecast to 2028 (US$ Thousand)

- Table 12. Rest of South America Lignin Market, by Type - Volume and Forecast to 2028 (Tons)

- Table 13. Rest of South America Lignin Market, by Form - Revenue and Forecast to 2028 (US$ Thousand)

- Table 14. Rest of South America Lignin Market, by Application - Revenue and Forecast to 2028 (US$ Thousand)

- Table 15. Glossary of Terms, South America Lignin Market

List Of Figures

- Figure 1. South America Lignin Market Segmentation

- Figure 2. South America Lignin Market Segmentation - By Country

- Figure 3. South America Lignin Market Overview

- Figure 4. South America Lignin Market, By Form

- Figure 5. South America Lignin Market, by Country

- Figure 6. South America Porter's Five Forces Analysis: Lignin Market

- Figure 7. Ecosystem: South America Lignin Market

- Figure 8. South America Expert Opinion

- Figure 9. South America Lignin Market: Impact Analysis of Drivers and Restraints

- Figure 10. South America Lignin Market - Volume and Forecast to 2028 (Tons)

- Figure 11. South America Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- Figure 12. South America Lignin Market Revenue Share, By Type (2021 and 2028)

- Figure 13. Lignosulfonates: South America Lignin Market - Volume and Forecast To 2028 (Tons)

- Figure 14. Lignosulfonates: South America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 15. Kraft Lignin: South America Lignin Market - Volume and Forecast To 2028 (Tons)

- Figure 16. Kraft Lignin: South America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 17. High Purity Lignin: South America Lignin Market - Volume and Forecast To 2028 (Tons)

- Figure 18. High Purity Lignin: South America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 19. Others: South America Lignin Market - Volume and Forecast To 2028 (Tons)

- Figure 20. Others: South America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 21. South America Lignin Market Revenue Share, By Form (2021 and 2028)

- Figure 22. Solid: South America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 23. Liquid: South America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 24. South America Lignin Market Revenue Share, By Application (2021 and 2028)

- Figure 25. Concrete Additives: South America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 26. Plastics and Polymers: South America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 27. Bitumen: South America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 28. Water Treatment: South America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 29. Dyes and Pigments: South America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 30. Activated Carbon: South America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 31. Carbon Fiber: South America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 32. Others: South America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 33. South America: Lignin Market, by Key Country - Revenue (2021) (US$ Million)

- Figure 34. South America: Lignin Market Revenue Share, by Key Country (2021 and 2028)

- Figure 35. Brazil: Lignin Market -Revenue and Forecast to 2028 (US$ Thousand)

- Figure 36. Brazil: Lignin Market -Volume and Forecast to 2028 (Tons)

- Figure 37. Argentina: Lignin Market -Revenue and Forecast to 2028 (US$ Thousand)

- Figure 38. Argentina: Lignin Market -Volume and Forecast to 2028 (Tons)

- Figure 39. Rest of South America: Lignin Market -Revenue and Forecast to 2028 (US$ Thousand)

- Figure 40. Rest of South America: Lignin Market -Volume and Forecast to 2028 (Tons)

The South America lignin market was valued at US$ 27,289.61 thousand in 2022 and is expected to reach US$ 35,261.05 thousand by 2028; it is estimated to grow at a CAGR of 4.4% from 2022 to 2028.

Strategic Development Initiatives by Key Market Players

Lignin manufacturers are investing significantly in strategic development initiatives such as product innovation, mergers & acquisitions, and expansion of their businesses to attract a wide customer base and enhance their market position. Moreover, the demand for lignin is increasing among end-use industries due to rising environmental concerns and sustainability issues. For instance, in December 2021, Nippon Paper (Japan) and Stora Enso Oyj (Finland) signed a partnership agreement to use trees to revolutionize the battery industry. Their research focused on the replacement of lithium-ion and rare-metal batteries with lignin. Such product innovations help companies to gain a competitive advantage in international markets.

Major manufacturers are adopting creative strategies such as acquisition, expansion, and production capacity scaleup to serve their customers better and satisfy their growing demands. Therefore, strategic initiatives by manufacturers are expected to fuel the growth of the lignin market during the forecast period.

South America Lignin Market Overview

The presence of the pulp & paper industry has been increasing in South America owing to the rising production and export of pulp and paper. In 2020, Brazil led the world ranking for exporting more than 15 million tons of pulp, making it a major global input supplier. Lignin is predominantly sourced from pulp & paper mills and cellulosic biorefineries. Lignin is being used in commercial polymers to improve biodegradability, as it is cost effective and a non-polluting biodegradable polymer. To mitigate the growing demand for pulp and paper across the region, many manufacturers of bio-based materials have been taking initiatives and focusing on expanding their production capacity. For instance, on May 12, 2021, Suzano SA, a eucalyptus pulp producer in South America, announced the construction of a new US$ 2.8 billion pulp plant project in Brazil with an annual production capacity of 2.3 million tons. These expansion projects by the manufacturers contribute to the high productivity of pulp and paper across the region, which bolster the growth of the lignin market.

South America Lignin Market Revenue and Forecast to 2028 (US$ Thousand)

South America Lignin Market Segmentation

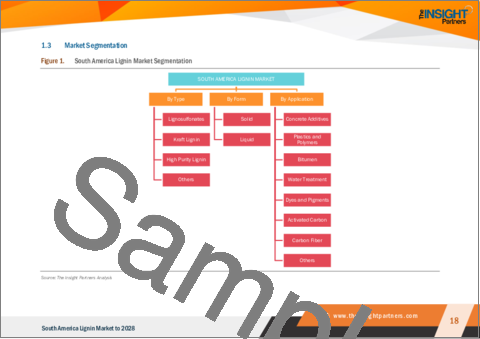

The South America lignin market is segmented based on type, form, application, and country. Based on type, the South America lignin market is segmented into lignosulfonates, kraft lignin, high purity lignin, and others. The lignosulfonates segment held the largest South America lignin market share in 2022.

Based on form, the South America lignin market is bifurcated into solid and liquid. The solid segment held a larger market share in 2022.

Based on application, the South America lignin market is segmented into concrete additives, plastics and polymers, bitumen, water treatment, dyes and pigments, activated carbon, carbon fiber, and others. The others segment held the largest market share in 2022.

Based on country, the South America lignin market is segmented into Brazil, Argentina, and the Rest of South America. Brazil dominated the South America lignin market share in 2022.

Nippon Paper Industries Co Ltd; Borregaard ASA; Burgo Group SpA; Domsjo Fabriker AB; Sappi Ltd; Stora Enso Oyj; Suzano SA; and The Dallas Group of America Inc are the leading companies operating in the South America lignin market.

Reasons to Buy:

- Save and reduce time carrying out entry-level research by identifying the growth, size, leading players, and segments in the South America lignin market.

- Highlights key business priorities in order to assist companies to realign their business strategies

- The key findings and recommendations highlight crucial progressive industry trends in the South America lignin market, thereby allowing players across the value chain to develop effective long-term strategies

- Develop/modify business expansion plans by using substantial growth offering developed and emerging markets

- Scrutinize in-depth South America market trends and outlook coupled with the factors driving the South America lignin market, as well as those hindering it

- Enhance the decision-making process by understanding the strategies that underpin commercial interest with respect to client products, segmentation, pricing, and distribution

Table Of Contents

1. Introduction

- 1.1 Study Scope

- 1.2 The Insight Partners Research Report Guidance

- 1.3 Market Segmentation

- 1.3.1 South America Lignin Market, by Type

- 1.3.2 South America Lignin Market, by Form

- 1.3.3 South America Lignin Market, by Application

- 1.3.4 South America Lignin Market, by Country

2. Key Takeaways

3. Research Methodology

- 3.1 Scope of the Study

- 3.2 Research Methodology

- 3.2.1 Data Collection:

- 3.2.2 Primary Interviews:

- 3.2.3 Hypothesis formulation:

- 3.2.4 Macro-economic factor analysis:

- 3.2.5 Developing base number:

- 3.2.6 Data Triangulation:

- 3.2.7 Country level data:

4. South America Lignin Market Landscape

- 4.1 Market Overview

- 4.2 Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants:

- 4.2.2 Bargaining Power of Suppliers:

- 4.2.3 Bargaining Power of Buyers:

- 4.2.4 Intensity of Competitive Rivalry:

- 4.2.5 Threat of Substitutes:

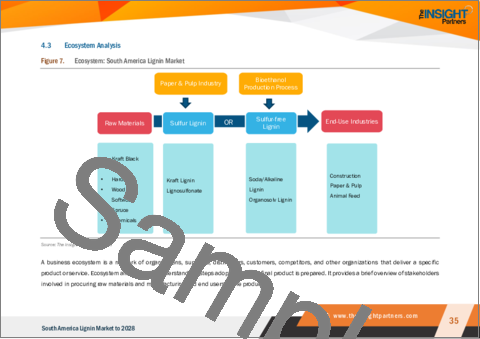

- 4.3 Ecosystem Analysis

- 4.3.1 Raw Materials

- 4.3.2 Production Process

- 4.3.3 End-Use Industries

- 4.4 Expert Opinion

5. South America Lignin Market - Key Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Growing Demand of Lignin from Several End-Use Industries

- 5.2 Market Restraints

- 5.2.1 Availability of Substitutes for Lignin

- 5.3 Market Opportunities

- 5.3.1 Adoption of Lignin for Carbon Fiber Production

- 5.4 Future Trends

- 5.4.1 Strategic Development Initiatives by Key Market Players

- 5.5 Impact Analysis of Drivers and Restraints

6. Lignin - South America Market Analysis

- 6.1 South America Lignin Market -Volume and Forecast to 2028 (Tons)

- 6.2 South America Lignin Market -Revenue and Forecast to 2028 (US$ Thousand)

7. South America Lignin Market Analysis - By Type

- 7.1 Overview

- 7.2 South America Lignin Market, By Type (2021 and 2028)

- 7.3 Lignosulfonates

- 7.3.1 Overview

- 7.3.2 Lignosulfonates: Lignin Market - Volume and Forecast to 2028 (Tons)

- 7.3.3 Lignosulfonates: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 7.4 Kraft Lignin

- 7.4.1 Overview

- 7.4.2 Kraft Lignin: Lignin Market - Volume and Forecast to 2028 (Tons)

- 7.4.3 Kraft Lignin: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 7.5 High Purity Lignin

- 7.5.1 Overview

- 7.5.2 High Purity Lignin: Lignin Market - Volume and Forecast to 2028 (Tons)

- 7.5.3 High Purity Lignin: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 7.6 Others

- 7.6.1 Overview

- 7.6.2 Others: Lignin Market - Volume and Forecast to 2028 (Tons)

- 7.6.3 Others: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

8. South America Lignin Market Analysis -By Form

- 8.1 Overview

- 8.2 Lignin Market, By Form (2021 and 2028)

- 8.3 Solid

- 8.3.1 Overview

- 8.3.2 Solid: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 8.4 Liquid

- 8.4.1 Overview

- 8.4.2 Liquid: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

9. South America Lignin Market Analysis - By Application

- 9.1 Overview

- 9.2 Lignin Market, By Application (2021 and 2028)

- 9.3 Concrete Additives

- 9.3.1 Overview

- 9.3.2 Concrete Additives: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 9.4 Plastics and Polymers

- 9.4.1 Overview

- 9.4.2 Plastics and Polymers: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 9.5 Bitumen

- 9.5.1 Overview

- 9.5.2 Bitumen: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 9.6 Water Treatment

- 9.6.1 Overview

- 9.6.2 Water Treatment: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 9.7 Dyes and Pigments

- 9.7.1 Overview

- 9.7.2 Dyes and Pigments: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 9.8 Activated Carbon

- 9.8.1 Overview

- 9.8.2 Activated Carbon: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 9.9 Carbon Fiber

- 9.9.1 Overview

- 9.9.2 Carbon Fiber: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 9.10 Others

- 9.10.1 Overview

- 9.10.2 Others: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

10. South America Lignin Market - by Country Analysis

- 10.1 South America: Lignin Market

- 10.1.1 South America: Lignin Market, by Key Country

- 10.1.1.1 Brazil: Lignin Market -Revenue and Forecast to 2028 (US$ Thousand)

- 10.1.1.2 Brazil: Lignin Market -Volume and Forecast to 2028 (Tons)

- 10.1.1.2.1 Brazil: Lignin Market, by Type

- 10.1.1.2.2 Brazil: Lignin Market, by Type

- 10.1.1.2.3 Brazil: Lignin Market, by Form

- 10.1.1.2.4 Brazil: Lignin Market, by Application

- 10.1.1.3 Argentina: Lignin Market -Revenue and Forecast to 2028 (US$ Thousand)

- 10.1.1.4 Argentina: Lignin Market -Volume and Forecast to 2028 (Tons)

- 10.1.1.4.1 Argentina: Lignin Market, by Type

- 10.1.1.4.2 Argentina: Lignin Market, by Type

- 10.1.1.4.3 Argentina: Lignin Market, by Form

- 10.1.1.4.4 Argentina: Lignin Market, by Application

- 10.1.1.5 Rest of South America: Lignin Market -Revenue and Forecast to 2028 (US$ Thousand)

- 10.1.1.6 Rest of South America: Lignin Market -Volume and Forecast to 2028 (Tons)

- 10.1.1.6.1 Rest of South America: Lignin Market, by Type

- 10.1.1.6.2 Rest of South America: Lignin Market, by Type

- 10.1.1.6.3 Rest of South America: Lignin Market, by Form

- 10.1.1.6.4 Rest of South America: Lignin Market, by Application

- 10.1.1 South America: Lignin Market, by Key Country

11. Industry Landscape

- 11.1 Overview

- 11.2 Market Initiative

- 11.3 Partnerships & Collaborations

12. Company Profiles

- 12.1 Nippon Paper Industries Co Ltd

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Borregaard ASA

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 Burgo Group SpA

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Domsjo Fabriker AB

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Sappi Ltd

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 Stora Enso Oyj

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 Suzano SA

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 The Dallas Group of America Inc

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

13. Appendix

- 13.1 About The Insight Partners

- 13.2 Glossary of Terms