|

|

市場調査レポート

商品コード

1375098

北米のリグニン市場の2028年までの予測-地域別分析-タイプ、形態、用途別North America Lignin Market Forecast to 2028 - COVID-19 Impact and Regional Analysis - by Type, Form, and Application |

||||||

|

|

|||||||

| 北米のリグニン市場の2028年までの予測-地域別分析-タイプ、形態、用途別 |

|

出版日: 2023年08月22日

発行: The Insight Partners

ページ情報: 英文 127 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

北米リグニン市場は2022年に1億2,167万6,610米ドルと評価され、2028年には1億6,781万5,190米ドルに達すると予測され、2022年から2028年までのCAGRは5.5%と推定されます。

持続可能なバイオ製品を促進する政府の規制と取り組み

欧州各国の政府は、人の健康と環境をより確実に保護するため、パーソナルケア、動物飼料、農業など多くの加工産業において、化学物質を使用して製品を製造することにいくつかの規制を課しています。さらに、こうした規制は温室効果ガスの排出削減を目的としており、ポリマー製造企業は天然由来の原料開発への投資を増やす必要に迫られています。温室効果ガス(GHG)排出に関する意識の高まりが、バイオベースのポリマー製品に対する需要を急増させています。そのため、リグニンはフェノール、フェノール樹脂、乳化剤を製造するための中間体として使用されています。特に北米では、大気汚染と温室効果ガス排出を削減するための規制支援により、バイオ燃料の利用の重要性が高まっており、リグニン需要を押し上げています。各国政府は、リグニンをベースとしたバイオマテリアルの認知度向上と開発のために、いくつかのイニシアチブを採用しています。2020年、ミシガン州立大学は、接着剤、コーティング、エラストマー、発泡用途の持続可能なリグニン系樹脂を開発するため、米国食品農業研究所(米国農務省)から資金提供を受けた。したがって、持続可能なバイオ製品を促進するための政府の規制や取り組みが、リグニン市場の成長を後押ししています。

北米のリグニン市場概要

北米のリグニン市場は米国、カナダ、メキシコに区分されます。北米は、プラスチック・ポリマー、パルプ・製紙、飼料、塗料・コーティング、農薬など様々な最終用途産業からの需要が増加しているため、リグニンメーカーにとって多くの成長機会があります。これらの産業では、高分子量、理想的なガラス転移温度、良好な熱分解性、高いリグニン溶解性、生分解性、高い抗酸化性を有するリグノスルホン酸塩、クラフトリグニン、高純度リグニンの形態でリグニンが使用されています。製紙やバイオエタノール製造の製品別であるリグニンは、フェノール系接着剤の配合においてフェノールを完全に代替し、建築資材を低毒性にし、石油を代替することができます。さらに、この地域のさまざまな国の政府による高度なインフラ整備への支援と建設部門への投資の増加が、リグニン市場の成長を促進しています。例えば、2021年08月02日、米国ホワイトハウスの報告書によると、同法は港湾インフラと水路に170億米ドル、空港に250億米ドルを投資し、補修とメンテナンスの滞りに対処し、港湾と空港付近の混雑と排出を緩和し、電化とその他の低炭素技術を推進します。

北米リグニン市場の収益と2028年までの予測(千米ドル)

北米リグニン市場のセグメンテーション

北米のリグニン市場は、タイプ、形態、用途、国によって区分されます。タイプ別では、北米のリグニン市場はリグノスルホン酸塩、クラフトリグニン、高純度リグニン、その他に区分されます。2022年にはリグノスルホネートセグメントが最大の市場シェアを占めました。

北米のリグニン市場は形態によって固体と液体に二分されます。2022年には固体セグメントがより大きな市場シェアを占めました。

用途別では、北米リグニン市場はコンクリート添加剤、プラスチック・ポリマー、アスファルト、水処理、染料・顔料、活性炭、炭素繊維、その他に区分されます。2022年にはプラスチック・ポリマーセグメントが最大の市場シェアを占めました。

国別に見ると、北米リグニン市場は米国、カナダ、メキシコに区分されます。2022年の北米リグニン市場シェアは米国が独占。

Nippon Paper Industries Co Ltd、Borregaard ASA、Burgo Group SpA、Domsjo Fabriker AB、Sappi Ltd、Stora Enso Oyj、Suzano SA、The Dallas Group of America Inc、Tokyo Chemical Industry Co Ltd、West Fraser Timber Co Ltdが北米リグニン市場の主要企業です。

目次

第1章 イントロダクション

第2章 キーポイント

第3章 調査手法

- 調査範囲

- 調査手法

- データ収集

- 一次インタビュー

- 仮説の策定

- マクロ経済要因分析

- 基礎数値の作成

- データの三角測量

- 国レベルのデータ

第4章 北米リグニン市場情勢

- 市場概要

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力:新規参入の脅威

- 競争企業間の敵対関係の強さ

- 代替品の脅威

- エコシステム分析

- 原材料

- 生産プロセス

- 最終用途産業

- 専門家の見解

第5章 北米リグニン市場:主要市場力学

- 市場促進要因

- 複数の最終用途産業からのリグニン需要の増大

- 持続可能なバイオ製品を促進するための政府の規制と取り組み

- 市場抑制要因

- リグニンの代替品の入手可能性

- 市場機会

- 炭素繊維生産へのリグニンの採用

- 今後の動向

- 新興国市場の主な参入企業による戦略的発展への取り組み

- 促進要因と抑制要因の影響分析

第6章 リグニン北米市場分析

- 北米リグニン市場:2028年までの数量と予測

第7章 北米リグニン市場分析:タイプ別

- イントロダクション

- リグニン市場:タイプ別(2021年、2028年)

- リグノスルホン酸塩

- クラフトリグニン

- 高純度リグニン

- その他

第8章 北米リグニン市場分析:形態別

- イントロダクション

- リグニン市場:形態別(2021年、2028年)

- 固体

- 液体

第9章 北米リグニン市場の分析:用途別

- イントロダクション

- リグニン市場:用途別(2021年、2028年)

- コンクリート添加剤

- プラスチックとポリマー

- ビチューメン

- 水処理

- 染料・顔料

- 活性炭

- 炭素繊維

- その他

第10章 北米リグニン市場:国別分析

- 北米

第11章 業界情勢

- イントロダクション

- 市場イニシアティブ

- パートナーシップとコラボレーション

第12章 企業プロファイル

- Nippon Paper Industries Co Ltd

- Borregaard ASA

- Burgo Group SpA

- Domsjo Fabriker AB

- Sappi Ltd

- Stora Enso Oyj

- Suzano SA

- The Dallas Group of America Inc

- Tokyo Chemical Industry Co Ltd

- West Fraser Timber Co Ltd

第13章 付録

List Of Tables

- Table 1. North America Lignin Market -Volume and Forecast to 2028 (Tons)

- Table 2. North America Lignin Market -Revenue and Forecast to 2028 (US$ Thousand)

- Table 3. US Lignin Market, by Type - Revenue and Forecast to 2028 (US$ Thousand)

- Table 4. US Lignin Market, by Type - Volume and Forecast to 2028 (Tons)

- Table 5. US Lignin Market, by Form - Revenue and Forecast to 2028 (US$ Thousand)

- Table 6. US Lignin Market, by Application - Revenue and Forecast to 2028 (US$ Thousand)

- Table 7. Canada: Lignin Market, by Type - Revenue and Forecast to 2028 (US$ Thousand)

- Table 8. Canada: Lignin Market, by Type - Volume and Forecast to 2028 (Tons)

- Table 9. Canada Lignin Market, by Form - Revenue and Forecast to 2028 (US$ Thousand)

- Table 10. Canada Lignin Market, by Application - Revenue and Forecast to 2028 (US$ Thousand)

- Table 11. Mexico Lignin Market, by Type - Revenue and Forecast to 2028 (US$ Thousand)

- Table 12. Mexico Lignin Market, by Type - Volume and Forecast to 2028 (Tons)

- Table 13. Mexico Lignin Market, by Form - Revenue and Forecast to 2028 (US$ Thousand)

- Table 14. Mexico Lignin Market, by Application - Revenue and Forecast to 2028 (US$ Thousand)

- Table 15. Glossary of Terms, Lignin Market

List Of Figures

- Figure 1. North America Lignin Market Segmentation

- Figure 2. North America Lignin Market Segmentation - By Country

- Figure 3. North America Lignin Market Overview

- Figure 4. North America Lignin Market, By Form

- Figure 5. US Lignin Market, by Country

- Figure 6. North America Porter's Five Forces Analysis: Lignin Market

- Figure 7. Ecosystem: North America Lignin Market

- Figure 8. North America Expert Opinion

- Figure 9. North America Lignin Market: Impact Analysis of Drivers and Restraints

- Figure 10. North America Lignin Market - Volume and Forecast to 2028 (Tons)

- Figure 11. North America Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- Figure 12. North America Lignin Market Revenue Share, By Type (2021 and 2028)

- Figure 13. Lignosulfonates: North America Lignin Market - Volume and Forecast To 2028 (Tons)

- Figure 14. Lignosulfonates: North America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 15. Kraft Lignin: North America Lignin Market - Volume and Forecast To 2028 (Tons)

- Figure 16. Kraft Lignin: North America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 17. High Purity Lignin: North America Lignin Market - Volume and Forecast To 2028 (Tons)

- Figure 18. High Purity Lignin: North America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 19. Others: North America Lignin Market - Volume and Forecast To 2028 (Tons)

- Figure 20. Others: North America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 21. North America Lignin Market Revenue Share, By Form (2021 and 2028)

- Figure 22. Solid: North America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 23. Liquid: North America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 24. North America Lignin Market Revenue Share, By Application (2021 and 2028)

- Figure 25. Concrete Additives: North America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 26. Plastics and Polymers: North America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 27. Bitumen: North America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 28. Water Treatment: North America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 29. Dyes and Pigments: North America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 30. Activated Carbon: North America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 31. Carbon Fiber: North America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 32. Others: North America Lignin Market - Revenue and Forecast To 2028 (US$ Thousand)

- Figure 33. North America: Lignin Market, by Key Country - Revenue (2021) (US$ Million)

- Figure 34. North America: Lignin Market Revenue Share, by Key Country (2021 and 2028)

- Figure 35. US: Lignin Market -Revenue and Forecast to 2028 (US$ Thousand)

- Figure 36. US: Lignin Market -Volume and Forecast to 2028 (Tons)

- Figure 37. Canada: Lignin Market-Revenue and Forecast to 2028 (US$ Thousand)

- Figure 38. Canada: Lignin Market-Volume and Forecast to 2028 (Tons)

- Figure 39. Mexico: Lignin Market-Revenue and Forecast to 2028 (US$ Thousand)

- Figure 40. Mexico: Lignin Market-Volume and Forecast to 2028 (Tons)

The North America lignin market was valued at US$ 1,21,676.61 thousand in 2022 and is expected to reach US$ 1,67,815.19 thousand by 2028; it is estimated to grow at a CAGR of 5.5% from 2022 to 2028.

Government Regulations and Initiatives to Promote Sustainable and Bio-Products

Governments of various European countries have imposed a few regulations on using chemicals to manufacture products in many processing industries, such as personal care, animal feed, and agriculture, to ensure better protection of human health and the environment. Moreover, these regulations are set to reduce greenhouse emissions and have compelled polymer manufacturing companies to increase investments in developing naturally derived raw materials. Rising awareness regarding greenhouse gas (GHG) emissions has surged the demand for bio-based polymer products. Thus, lignin is being used as an intermediate for manufacturing phenol, phenolic resins, and emulsifying agents. The increasing importance of using biofuels, especially in North America, on account of regulatory support to reduce air pollution and GHG emissions is boosting the demand for lignin. Governments of various countries are adopting several initiatives to increase the awareness and development of lignin-based biomaterials. In 2020, Michigan State University received funding from the National Institute of Food and Agriculture (United States Department of Agriculture) to develop sustainable lignin-based resins for adhesive, coating, elastomer, and foam applications. Therefore, government regulations and initiatives to promote sustainable and bio-products are driving the lignin market growth.

North America Lignin Market Overview

The lignin market in North America is segmented into the US, Canada, and Mexico. North America holds many growth opportunities for lignin manufacturers owing to increasing demand from various end-use industries such as plastics & polymers, pulp & paper, animal feed, paints & coatings, and pesticides. These industries use lignin in the form of lignosulphonates, kraft lignin, and high purity lignin as they possess high molecular weight, ideal glass transition temperature, good thermal decomposition, high lignin solubility, biodegradability, and high antioxidant properties. Lignin - a byproduct of paper and bioethanol production- can thoroughly replace phenol in a phenolic adhesive formulation, make building materials less toxic, and replace petroleum. Additionally, support from government of various countries in the region for advanced infrastructural setup and rising investment in the construction sector are driving the growth of lignin market. For instance, on August 02, 2021, according to the White House report, the legislation invested US$ 17 billion in port infrastructure and waterways, and US$ 25 billion in airports to address repair and maintenance backlogs, facilitate congestion and emissions near ports and airports, and push electrification and other low-carbon technologies.

North America Lignin Market Revenue and Forecast to 2028 (US$ Thousand)

North America Lignin Market Segmentation

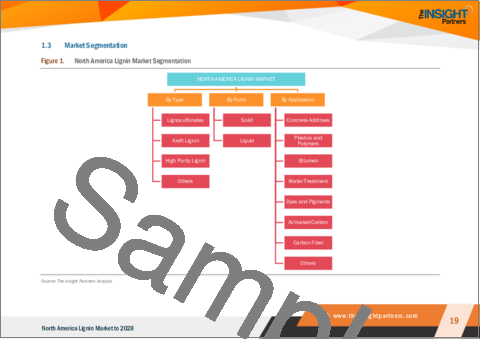

The North America lignin market is segmented based on type, form, application, and country. Based on type, the North America lignin market is segmented into lignosulfonates, kraft lignin, high purity lignin, and others. The lignosulfonates segment held the largest market share in 2022.

Based on form, the North America lignin market is bifurcated into solid and liquid. The solid segment held a larger market share in 2022.

Based on application, the North America lignin market is segmented into concrete additives, plastics and polymers, bitumen, water treatment, dyes and pigments, activated carbon, carbon fiber, and others. The plastics and polymers segment held the largest market share in 2022.

Based on country, the North America lignin market is segmented into the US, Canada, and Mexico. The US dominated the North America lignin market share in 2022.

Nippon Paper Industries Co Ltd; Borregaard ASA; Burgo Group SpA; Domsjo Fabriker AB; Sappi Ltd; Stora Enso Oyj; Suzano SA; The Dallas Group of America Inc; Tokyo Chemical Industry Co Ltd; and West Fraser Timber Co Ltd are the leading companies operating in the North America lignin market.

Reasons to Buy:

- Save and reduce time carrying out entry-level research by identifying the growth, size, leading players, and segments in the North America lignin market.

- Highlights key business priorities in order to assist companies to realign their business strategies

- The key findings and recommendations highlight crucial progressive industry trends in the North America lignin market, thereby allowing players across the value chain to develop effective long-term strategies

- Develop/modify business expansion plans by using substantial growth offering developed and emerging markets

- Scrutinize in-depth North America market trends and outlook coupled with the factors driving the North America lignin market, as well as those hindering it

- Enhance the decision-making process by understanding the strategies that underpin commercial interest with respect to client products, segmentation, pricing, and distribution

Table Of Contents

1. Introduction

- 1.1 Study Scope

- 1.2 The Insight Partners Research Report Guidance

- 1.3 Market Segmentation

- 1.3.1 North America Lignin Market, by Type

- 1.3.2 North America Lignin Market, by Form

- 1.3.3 North America Lignin Market, by Application

- 1.3.4 North America Lignin Market, by Country

2. Key Takeaways

3. Research Methodology

- 3.1 Scope of the Study

- 3.2 Research Methodology

- 3.2.1 Data Collection:

- 3.2.2 Primary Interviews:

- 3.2.3 Hypothesis formulation:

- 3.2.4 Macro-economic factor analysis:

- 3.2.5 Developing base number:

- 3.2.6 Data Triangulation:

- 3.2.7 Country level data:

4. North America Lignin Market Landscape

- 4.1 Market Overview

- 4.2 Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants:

- 4.2.2 Bargaining Power of Suppliers:

- 4.2.3 Bargaining Power of Buyers:

- 4.2.4 Intensity of Competitive Rivalry:

- 4.2.5 Threat of Substitutes:

- 4.3 Ecosystem Analysis

- 4.3.1 Raw Materials

- 4.3.2 Production Process

- 4.3.3 End-Use Industries

- 4.4 Expert Opinion

5. North America Lignin Market - Key Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Growing Demand of Lignin from Several End-Use Industries

- 5.1.2 Government Regulations and Initiatives to Promote Sustainable and Bio-Products

- 5.2 Market Restraints

- 5.2.1 Availability of Substitutes for Lignin

- 5.3 Market Opportunities

- 5.3.1 Adoption of Lignin for Carbon Fiber Production

- 5.4 Future Trends

- 5.4.1 Strategic Development Initiatives by Key Market Players

- 5.5 Impact Analysis of Drivers and Restraints

6. Lignin - North America Market Analysis

- 6.1 North America Lignin Market -Volume and Forecast to 2028 (Tons)

- 6.2 North America Lignin Market -Revenue and Forecast to 2028 (US$ Thousand)

7. North America Lignin Market Analysis - By Type

- 7.1 Overview

- 7.2 North America Lignin Market, By Type (2021 and 2028)

- 7.3 Lignosulfonates

- 7.3.1 Overview

- 7.3.2 Lignosulfonates: Lignin Market - Volume and Forecast to 2028 (Tons)

- 7.3.3 Lignosulfonates: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 7.4 Kraft Lignin

- 7.4.1 Overview

- 7.4.2 Kraft Lignin: Lignin Market - Volume and Forecast to 2028 (Tons)

- 7.4.3 Kraft Lignin: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 7.5 High Purity Lignin

- 7.5.1 Overview

- 7.5.2 High Purity Lignin: Lignin Market - Volume and Forecast to 2028 (Tons)

- 7.5.3 High Purity Lignin: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 7.6 Others

- 7.6.1 Overview

- 7.6.2 Others: Lignin Market - Volume and Forecast to 2028 (Tons)

- 7.6.3 Others: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

8. North America Lignin Market Analysis -By Form

- 8.1 Overview

- 8.2 Lignin Market, By Form (2021 and 2028)

- 8.3 Solid

- 8.3.1 Overview

- 8.3.2 Solid: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 8.4 Liquid

- 8.4.1 Overview

- 8.4.2 Liquid: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

9. North America Lignin Market Analysis - By Application

- 9.1 Overview

- 9.2 Lignin Market, By Application (2021 and 2028)

- 9.3 Concrete Additives

- 9.3.1 Overview

- 9.3.2 Concrete Additives: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 9.4 Plastics and Polymers

- 9.4.1 Overview

- 9.4.2 Plastics and Polymers: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 9.5 Bitumen

- 9.5.1 Overview

- 9.5.2 Bitumen: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 9.6 Water Treatment

- 9.6.1 Overview

- 9.6.2 Water Treatment: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 9.7 Dyes and Pigments

- 9.7.1 Overview

- 9.7.2 Dyes and Pigments: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 9.8 Activated Carbon

- 9.8.1 Overview

- 9.8.2 Activated Carbon: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 9.9 Carbon Fiber

- 9.9.1 Overview

- 9.9.2 Carbon Fiber: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

- 9.10 Others

- 9.10.1 Overview

- 9.10.2 Others: Lignin Market - Revenue and Forecast to 2028 (US$ Thousand)

10. North America Lignin Market - by Country Analysis

- 10.1 North America: Lignin Market

- 10.1.1 North America: Lignin Market, by Key Country

- 10.1.1.1 US: Lignin Market -Revenue and Forecast to 2028 (US$ Thousand)

- 10.1.1.2 US: Lignin Market -Volume and Forecast to 2028 (Tons)

- 10.1.1.2.1 US: Lignin Market, by Type

- 10.1.1.2.2 US: Lignin Market, by Type

- 10.1.1.2.3 US: Lignin Market, by Form

- 10.1.1.2.4 US: Lignin Market, by Application

- 10.1.1.3 Canada: Lignin Market-Revenue and Forecast to 2028 (US$ Thousand)

- 10.1.1.4 Canada: Lignin Market-Volume and Forecast to 2028 (Tons)

- 10.1.1.4.1 Canada: Lignin Market, by Type

- 10.1.1.4.2 Canada: Lignin Market, by Type

- 10.1.1.4.3 Canada: Lignin Market, by Form

- 10.1.1.4.4 Canada: Lignin Market, by Application

- 10.1.1.5 Mexico: Lignin Market-Revenue and Forecast to 2028 (US$ Thousand)

- 10.1.1.6 Mexico: Lignin Market-Volume and Forecast to 2028 (Tons)

- 10.1.1.6.1 Mexico: Lignin Market, by Type

- 10.1.1.6.2 Mexico: Lignin Market, by Type

- 10.1.1.6.3 Mexico: Lignin Market, by Form

- 10.1.1.6.4 Mexico: Lignin Market, by Application

- 10.1.1 North America: Lignin Market, by Key Country

11. Industry Landscape

- 11.1 Overview

- 11.2 Market Initiative

- 11.3 Partnerships & Collaborations

12. Company Profiles

- 12.1 Nippon Paper Industries Co Ltd

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Borregaard ASA

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 Burgo Group SpA

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Domsjo Fabriker AB

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Sappi Ltd

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 Stora Enso Oyj

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 Suzano SA

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 The Dallas Group of America Inc

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 Tokyo Chemical Industry Co Ltd

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

- 12.10 West Fraser Timber Co Ltd

- 12.10.1 Key Facts

- 12.10.2 Business Description

- 12.10.3 Products and Services

- 12.10.4 Financial Overview

- 12.10.5 SWOT Analysis

- 12.10.6 Key Developments

13. Appendix

- 13.1 About The Insight Partners

- 13.2 Glossary of Terms