|

|

市場調査レポート

商品コード

1372565

北米の静注用免疫グロブリン市場規模・予測、地域シェア、動向、成長機会分析レポート:タイプ別、用途別、流通チャネル別、エンドユーザー別、国別North America Intravenous Immunoglobulin Market Size and Forecasts, Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Type, Application, Distribution Channel, End User, and Country |

||||||

|

|

|||||||

|

|||||||

| 北米の静注用免疫グロブリン市場規模・予測、地域シェア、動向、成長機会分析レポート:タイプ別、用途別、流通チャネル別、エンドユーザー別、国別 |

|

出版日: 2023年10月10日

発行: The Insight Partners

ページ情報: 英文 107 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

北米の静注用免疫グロブリン市場規模は2022年に50億4,200万米ドルと評価され、2030年には87億4,700万米ドルに達すると予測され、2022年から2030年までのCAGRは7.1%を記録すると推定されます。北米の静注用免疫グロブリン市場成長の主因は、免疫グロブリン使用の増加と免疫不全疾患の有病率の上昇です。

静注用免疫グロブリン市場の成長に向けた新製品の上市と承認機会

近年、北米の静注用免疫グロブリン市場では様々な市場開拓が行われています。市場各社は新製品を上市し、規制当局の承認を求めています。2023年4月、研究開発型バイオ医薬品のリーダーである武田薬品工業株式会社は、米国食品医薬品局(FDA)から、2~16歳の小児における原発性免疫不全症(PI)の治療薬としてHYQVIAの使用を拡大するための生物製剤追加承認申請(sBLA)の承認を取得しました。HYQVIAの免疫グロブリン皮下注(ScIG)のみ、毎月の投与が可能です。2022年、カナダ保健省は、免疫不全のカナダ人に対する新しい免疫グロブリン(IG)治療薬であるHYQVIAを承認しました。2021年2月、ファイザー社が慢性炎症性脱髄性多発神経炎(CIDP)治療薬PANZYGA(10%液状免疫グロブリン製剤)のsBLA承認を取得。

タイプ別洞察

北米の静注用免疫グロブリン市場は、タイプ別にIgG、IgA、IgM、その他に区分されます。2022年には、IgGセグメントが最大のシェアを占め、2022~2030年に最も速いCAGRを記録すると予測されています。

用途別洞察

北米の静注用免疫グロブリン市場は、用途別に免疫不全症、慢性炎症性脱髄性多発ニューロパチー、特発性血小板減少性紫斑病、多巣性運動ニューロパチー、低ガンマグロブリン血症、ギラン・バレー症候群、特異的抗体欠損症、炎症性ミオパチー、重症筋無力症、その他に分類されます。2022年には、免疫不全症分野が最大の市場シェアを占め、2022~2030年に最も高いCAGRを記録すると予測されています。

流通チャネルに基づく洞察

流通チャネルに基づき、北米の静注用免疫グロブリン市場は病院薬局、小売薬局、その他に区分されます。2022年には、病院薬局セグメントが最大のシェアを占め、2022~2030年に最も速いCAGRを記録すると予想されます。

エンドユーザーに基づく洞察

エンドユーザーに基づくと、北米の静注用免疫グロブリン市場は病院、専門クリニック、その他に分類されます。2022年には、病院セグメントが最大のシェアを占め、2022~2030年に最速のCAGRを記録する見込みです。

自己免疫疾患の患者は、免疫グロブリンの静脈注射で治療されます。自己免疫疾患は、免疫系が誤って自己の組織や細胞を攻撃する疾患です。健康な細胞に対するこの異常な免疫反応により、慢性的な炎症、臓器やシステムの損傷が生じる。疲労、関節痛、筋力低下、皮疹、神経障害などは、自己免疫疾患の典型的な徴候や症状の一部です。ギラン・バレー症候群(GBS)、重症筋無力症(MS)、関節リウマチ(RA)、全身性エリテマトーデス(LE)、免疫性血小板減少症(ITP)などの自己免疫疾患の症状は、IVIG療法によって緩和することができます。この治療法の利点には、症状の迅速な緩和と長期にわたる効果の持続があり、患者の生活の質の向上につながります。

Intermountain Healthcareによると、自己免疫疾患および免疫介在性疾患は2,350万人から5,000万人の米国人に影響を及ぼしています。米国疾病予防管理センターによると、関節リウマチ(RA)は自己免疫性関節炎の中で最も多く、米国の成人の4人に1人が関節炎を患っています。米国重症筋無力症財団によると、重症筋無力症(MG)の有病率は米国人口10万人当たり14~20人と推定されています。カナダでは、重症筋無力症の罹患率は100万人年当たり23人、有病率は100万人当たり263人と推定され、この数字は過去数十年間安定しています。

免疫グロブリン使用の増加が北米の静注用免疫グロブリン市場を強化

血漿由来の免疫グロブリンは、自己免疫疾患や炎症性疾患などの治療に使用されます。自己免疫疾患や急性炎症性疾患に加えて、原発性免疫不全症(PIDD)、慢性炎症性脱髄性多発神経炎(CIDP)、多巣性運動ニューロパチー(MMN)などが、免疫グロブリンで治療される慢性・急性疾患です。免疫グロブリンはまた、感染症、皮膚疾患、リウマチ・腎疾患、心臓疾患の管理にも使用されるようになってきています。このように、静注用免疫グロブリンの需要は、様々な疾患の治療にこれらの抗体が使用されるようになるにつれて増加しています。

Takeda Pharmaceutical Co Ltd、Grifols SA、Pfizer Inc.、ADMA Biologics, Inc.、Bio Products Laboratory Ltd.、Octapharma AG、Kedrion SpA.、CSL Ltd.、LFB Group、Prothya Biosolutions B.V.などは、静注用免疫グロブリン市場で事業を展開している大手企業です。

北米の静注用免疫グロブリン市場に関する報告書を作成する際に参照した主な一次情報源および二次情報源としては、Myasthenia Gravis Foundation of America、Journal of Allergy and Clinical Immunology、Genetic and Rare Diseases Information Center、Immune Deficiency Foundation、GBS Foundation、Centers for Disease Control and Preventionなどがあります。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 静注用免疫グロブリン市場:地域別

- 主要洞察

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 静注用免疫グロブリン市場情勢

- イントロダクション

- PEST分析

- 世界のPEST分析

第5章 静注用免疫グロブリン市場-主要産業力学

- 市場促進要因

- 免疫グロブリン使用量の増加

- 免疫不全疾患の有病率の上昇

- 市場抑制要因

- 治療費の高騰

- 市場機会

- 新製品の上市と承認

- 今後の動向

- IVIG候補の強力なパイプライン

- 影響分析

第6章 静注用免疫グロブリン市場-北米市場分析

- 静注用免疫グロブリン市場の売上高、2022年~2030年

第7章 北米静注用免疫グロブリン市場:2030年までの収益と予測:タイプ別

- イントロダクション

- 静注用免疫グロブリン市場2022年・2030年タイプ別売上高シェア(%)

- IgG

- IgA

- IgM

- その他

第8章 北米静注用免疫グロブリン市場:2030年までの収益と予測:用途別

- イントロダクション

- 静注用免疫グロブリン市場2022年・2030年用途別売上高シェア(%)

- 免疫不全症

- 慢性炎症性脱髄性多発神経炎

- 特発性血小板減少性紫斑病

- 多巣性運動神経障害

- 低ガンマグロブリン血症

- ギラン・バレー症候群

- 特異的抗体欠損症

- 炎症性ミオパチー

- 重症筋無力症

- その他

第9章 北米静注用免疫グロブリン市場:2030年までの収益と予測:流通チャネル別

- イントロダクション

- 静注用免疫グロブリン市場2022年・2030年流通チャネル別売上高シェア(%)

- 病院薬局

- 小売薬局

- その他

第10章 北米静注用免疫グロブリン市場:2030年までの収益と予測:エンドユーザー別

- イントロダクション

- 静注用免疫グロブリン市場2022年・2030年エンドユーザー別売上高シェア(%)

- 病院

- 専門クリニック

- その他

第11章 北米の静注用免疫グロブリン市場-地域別分析

- 北米

- 米国

- カナダ

- メキシコ

第12章 北米の静注用免疫グロブリン市場:業界情勢

- イントロダクション

- 北米の静注用免疫グロブリン市場における成長戦略

- 無機的成長戦略

- 概要

- 有機的成長戦略

- 概要

第13章 企業プロファイル

- Takeda Pharmaceutical Co Ltd

- Grifols SA

- Pfizer Inc

- ADMA Biologics, Inc.

- Bio Products Laboratory Ltd.

- Octapharma AG

- Kedrion SpA

- CSL Ltd

- LFB Group

- Prothya Biosolutions B.V.

第14章 付録

List Of Tables

- Table 1. North America Intravenous Immunoglobulin Market Segmentation

- Table 2. North America Intravenous Immunoglobulin Market, by Type - Revenue and Forecast to 2030 (US$ Million)

- Table 3. North America Intravenous Immunoglobulin Market, by Application- Revenue and Forecast to 2030 (US$ Million)

- Table 4. North America Intravenous Immunoglobulin Market, by Distribution Channel- Revenue and Forecast to 2030 (US$ Million)

- Table 5. North America Intravenous Immunoglobulin Market, by End User- Revenue and Forecast to 2030 (US$ Million)

- Table 6. US Intravenous Immunoglobulin Market, by Type - Revenue and Forecast to 2030 (US$ Million)

- Table 7. US Intravenous Immunoglobulin Market, by Application- Revenue and Forecast to 2030 (US$ Million)

- Table 8. US Intravenous Immunoglobulin Market, by Distribution Channel- Revenue and Forecast to 2030 (US$ Million)

- Table 9. US Intravenous Immunoglobulin Market, by End User- Revenue and Forecast to 2030 (US$ Million)

- Table 10. Canada Intravenous Immunoglobulin Market, by Type- Revenue and Forecast to 2030 (US$ Million)

- Table 11. Canada Intravenous Immunoglobulin Market, by Application- Revenue and Forecast to 2030 (US$ Million)

- Table 12. Canada Intravenous Immunoglobulin Market, by Distribution Channel- Revenue and Forecast to 2030 (US$ Million)

- Table 13. Canada Intravenous Immunoglobulin Market, by End User- Revenue and Forecast to 2030 (US$ Million)

- Table 14. Mexico Intravenous Immunoglobulin Market, by Type- Revenue and Forecast to 2030 (US$ Million)

- Table 15. Mexico Intravenous Immunoglobulin Market, by Application- Revenue and Forecast to 2030 (US$ Million)

- Table 16. Mexico Intravenous Immunoglobulin Market, by Distribution Channel- Revenue and Forecast to 2030 (US$ Million)

- Table 17. Mexico Intravenous Immunoglobulin Market, by End User- Revenue and Forecast to 2030 (US$ Million)

- Table 18. Recent Inorganic Growth Strategies in the North America Intravenous Immunoglobulin Market

- Table 19. Recent Organic Growth Strategies in North America Intravenous Immunoglobulin Market

- Table 20. Glossary of Terms, North America Intravenous Immunoglobulin Market

List Of Figures

- Figure 1. Intravenous Immunoglobulin Market Segmentation, By Geography

- Figure 2. Global - PEST Analysis

- Figure 3. Intravenous Immunoglobulin Market - Key Industry Dynamics

- Figure 4. Impact Analysis of Drivers and Restraints

- Figure 5. Intravenous Immunoglobulin Market Revenue (US$ Mn), 2022 - 2030

- Figure 6. Intravenous Immunoglobulin Market Revenue Share, by Type, 2022 & 2030 (%)

- Figure 7. IgG: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 8. IgA: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 9. IgM: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 10. Others: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 11. Intravenous Immunoglobulin Market Revenue Share, by Application, 2022 & 2030 (%)

- Figure 12. Immunodeficiency Diseases: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 13. Chronic Inflammatory Demyelinating Polyneuropathy: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 14. Idiopathic Thrombocytopenic Purpura: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 15. Multifocal Motor Neuropathy: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 16. Hypogammaglobulinemia: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 17. Guillain-Barre Syndrome: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 18. Specific Antibody Deficiency: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 19. Inflammatory Myopathies: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 20. Myasthenia Gravis: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 21. Others: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 22. Intravenous Immunoglobulin Market Revenue Share, by Route of Administration, 2022 & 2030 (%)

- Figure 23. Hospital Pharmacy: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 24. Retail Pharmacy: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 25. Others: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 26. Intravenous Immunoglobulin Market Revenue Share, Species, 2022 & 2030 (%)

- Figure 27. Hospitals: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 28. Specialty Clinics: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 29. Others: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 30. North America: Intravenous Immunoglobulin Market, by Key Country - Revenue (2022) (US$ Million)

- Figure 31. North America Intravenous Immunoglobulin Market Revenue and Forecast to 2030 (US$ Mn)

- Figure 32. North America Intravenous Immunoglobulin Market, By Key Countries, 2022 and 2030 (%)

- Figure 33. US Intravenous Immunoglobulin Market Revenue and Forecast to 2030 (US$ Mn)

- Figure 34. Canada Intravenous Immunoglobulin Market Revenue and Forecast to 2030 (US$ Mn)

- Figure 35. Mexico Intravenous Immunoglobulin Market Revenue and Forecast to 2030 (US$ Mn)

- Figure 36. Growth Strategies in North America Intravenous Immunoglobulin Market

The North America intravenous immunoglobulin market size was valued at US$ 5.042 Bn in 2022 and is expected to reach US$ 8.747 Bn by 2030; it is estimated to record a CAGR of 7.1% from 2022 to 2030. The North America intravenous immunoglobulin market growth is primarily driven by increase in use of immunoglobulins and rising prevalence of immunodeficiency diseases

New Product Launches and Approvals Opportunity for Growth of Intravenous Immunoglobulin Market

In recent years, there have been various developments in the intravenous immunoglobulin market in North America. Market players have been launching new products and seeking regulatory approvals for their offerings. In April 2023, Takeda Pharmaceutical Company Limited, an R&D-driven biopharmaceutical leader, received a supplemental Biologics License Application (sBLA) approval from the US Food and Drug Administration (FDA) to expand the use of HYQVIA to treat primary immunodeficiencies (PI) in children belonging to the age group of 2-16 years. Only HYQVIA's subcutaneous immune globulin (ScIG) infusion allows for monthly administration. In 2022, Health Canada approved HyQvia, a new Immunoglobulin (IG) treatment for Canadians with immune deficiencies. In February 2021, Pfizer Inc. received an sBLA approval for PANZYGA (10% liquid intravenous immunoglobulin preparation) to treat chronic inflammatory demyelinating polyneuropathy (CIDP)

Type-Based Insights

The North America intravenous immunoglobulin market, by type, is segmented into IgG, IgA, IgM, and others. In 2022, the IgG segment held the largest share and is expected to record the fastest CAGR during 2022-2030.

Application-Based Insights

Based on application, the North America intravenous immunoglobulin market is classified into immunodeficiency diseases, chronic inflammatory demyelinating polyneuropathy, idiopathic thrombocytopenic purpura, multifocal motor neuropathy, hypogammaglobulinemia, Guillain-Barre syndrome, specific antibody deficiency, inflammatory myopathies, myasthenia gravis, and others. In 2022, the immunodeficiency diseases segment held the largest market share, and it is expected to register the highest CAGR during 2022-2030.

Distribution Channel -Based Insights

Based on distribution channel, the North America intravenous immunoglobulin market is segmented into hospital pharmacy, retail pharmacy, and others. In 2022, the hospital pharmacy segment held the largest share, and it is expected to record the fastest CAGR during 2022-2030.

End User - Based Insights

Based on end user, the North America intravenous immunoglobulin market is classified into hospitals, specialty clinics, and others. In 2022, the hospitals segment held the largest share, and it is expected to register the fastest CAGR during 2022-2030.

Patients with autoimmune diseases are treated with intravenous immunoglobulins. Autoimmune diseases are conditions wherein the immune system accidentally attacks its own tissues or cells. Chronic inflammation, and organ and system damage result from this aberrant immune reaction against healthy cells. Fatigue, joint pain, muscle weakness, skin rashes, and neurological disturbances are a few of the typical signs and symptoms of autoimmune diseases. Symptoms of autoimmune diseases such as Guillain-Barre syndrome (GBS), myasthenia gravis (MS), rheumatoid arthritis (RA), systemic lupus erythematosus (LE), and immune thrombocytopenia (ITP) can be alleviated with the IVIG therapy. Benefits of this therapy include the rapid relief of symptoms and long-lasting effects, leading to improved quality of life among patients.

According to the Intermountain Healthcare, autoimmune and immune-mediated diseases and conditions affect 23.5-50 million Americans. According to the Centers for Disease Control and Prevention, rheumatoid arthritis (RA) is the most prevalent type of autoimmune arthritis, and 1 in 4 adults in the US has arthritis. As per the Myasthenia Gravis Foundation of America, Inc., the prevalence of myasthenia gravis (MG) is estimated at 14-20 per 100,000 of the US population. In Canada, the incidence of MG is estimated to be 23 per 1 million person-years, with a prevalence of 263 per 1 million people, and the numbers have been stable over the past few decades.

Increase in Use of Immunoglobulins Bolsters North America Intravenous Immunoglobulins Market

Plasma-derived immunoglobulins are used for treating autoimmune and inflammatory disorders, among others. In addition to autoimmune and acute inflammatory conditions, primary immune deficiency disease (PIDD), chronic inflammatory demyelinating polyneuropathy (CIDP), and multifocal motor neuropathy (MMN) are the chronic and acute conditions that are treated with immunoglobulins. Immunoglobulins are also increasingly used to manage infectious diseases, dermatological conditions, rheumatological/nephrological conditions, and heart disease. Thus, the demand for intravenous immunoglobulins is rising with the surging use of these antibodies for treating various conditions.

Takeda Pharmaceutical Co Ltd; Grifols SA; Pfizer Inc.; ADMA Biologics, Inc.; Bio Products Laboratory Ltd; Octapharma AG; Kedrion SpA.; CSL Ltd.; LFB Group; and Prothya Biosolutions B.V are among the leading companies operating in the intravenous immunoglobulin market.

A few of the major primary and secondary sources referred to while preparing the report on the North America intravenous immunoglobulin market are the Myasthenia Gravis Foundation of America, Journal of Allergy and Clinical Immunology, Genetic and Rare Diseases Information Center, Immune Deficiency Foundation, GBS Foundation, Centers for Disease Control and Prevention

Reasons to Buy:

- Save and reduce time carrying out entry-level research by identifying the growth, size, leading players and segments in the North America intravenous immunoglobulin market.

- Highlights key business priorities in order to assist companies to realign their business strategies.

- The key findings and recommendations highlight crucial progressive industry trends in the North America intravenous immunoglobulin market, thereby allowing players across the value chain to develop effective long-term strategies.

- Develop/modify business expansion plans by using substantial growth offering developed and emerging markets.

- Scrutinize in-depth market trends and outlook coupled with the factors driving the North America intravenous immunoglobulin market, as well as those hindering it.

- Enhance the decision-making process by understanding the strategies that underpin security interest with respect to client products, segmentation, pricing and distribution.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Intravenous Immunoglobulin Market, by Geography

- 2.2 Key Insights

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Intravenous Immunoglobulin Market Landscape

- 4.1 Overview

- 4.2 PEST Analysis

- 4.2.1 Global PEST Analysis

5. Intravenous Immunoglobulin Market - Key Industry Dynamics

- 5.1 Market Drivers:

- 5.1.1 Increase in Use of Immunoglobulins

- 5.1.2 Rising Immunodeficiency Disease Prevalence

- 5.2 Market Restraints

- 5.2.1 High Cost of Therapy

- 5.3 Market Opportunities

- 5.3.1 New Product Launches and Approvals

- 5.4 Future Trends

- 5.4.1 Strong Pipeline of IVIG Candidates

- 5.5 Impact Analysis:

6. Intravenous Immunoglobulin Market - North America Market Analysis

- 6.1 Intravenous Immunoglobulin Market Revenue (US$ Mn), 2022 - 2030

7. North America Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 - by Type

- 7.1 Overview

- 7.2 Intravenous Immunoglobulin Market Revenue Share, by Type, 2022 & 2030 (%)

- 7.3 IgG

- 7.3.1 Overview

- 7.3.2 IgG: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- 7.4 IgA

- 7.4.1 Overview

- 7.4.2 IgA: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

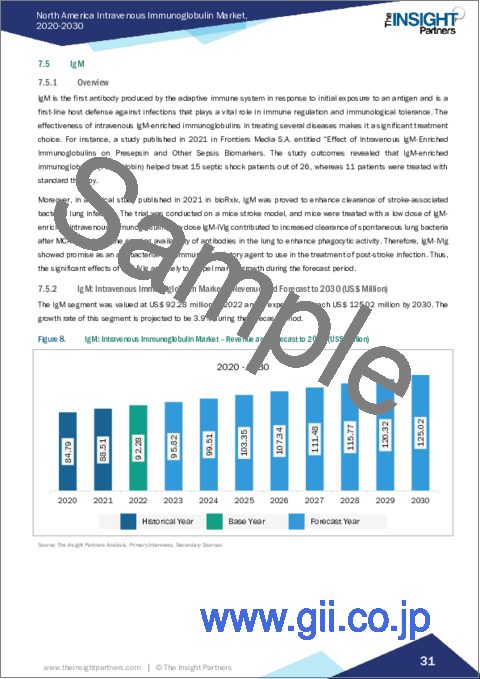

- 7.5 IgM

- 7.5.1 Overview

- 7.5.2 IgM: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- 7.6 Others

- 7.6.1 Overview

- 7.6.2 Others: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

8. North America Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 - by Application

- 8.1 Overview

- 8.2 Intravenous Immunoglobulin Market Revenue Share, by Application, 2022 & 2030 (%)

- 8.3 Immunodeficiency Diseases

- 8.3.1 Overview

- 8.3.2 Immunodeficiency Diseases: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- 8.4 Chronic Inflammatory Demyelinating Polyneuropathy

- 8.4.1 Overview

- 8.4.2 Chronic Inflammatory Demyelinating Polyneuropathy: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- 8.5 Idiopathic Thrombocytopenic Purpura

- 8.5.1 Overview

- 8.5.2 Idiopathic Thrombocytopenic Purpura: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- 8.6 Multifocal Motor Neuropathy

- 8.6.1 Overview

- 8.6.2 Multifocal Motor Neuropathy: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- 8.7 Hypogammaglobulinemia

- 8.7.1 Overview

- 8.7.2 Hypogammaglobulinemia: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- 8.8 Guillain-Barre Syndrome

- 8.8.1 Overview

- 8.8.2 Guillain-Barre Syndrome: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- 8.9 Specific Antibody Deficiency

- 8.9.1 Overview

- 8.9.2 Specific Antibody Deficiency: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- 8.10 Inflammatory Myopathies

- 8.10.1 Overview

- 8.10.2 Inflammatory Myopathies: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- 8.11 Myasthenia Gravis

- 8.11.1 Overview

- 8.11.2 Myasthenia Gravis: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- 8.12 Others

- 8.12.1 Overview

- 8.12.2 Others: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

9. North America Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 - by Distribution Channel

- 9.1 Overview

- 9.2 Intravenous Immunoglobulin Market Revenue Share, by Route of Administration, 2022 & 2030 (%)

- 9.3 Hospital Pharmacy

- 9.3.1 Overview

- 9.3.2 Hospital Pharmacy: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- 9.4 Retail Pharmacy

- 9.4.1 Overview

- 9.4.2 Retail Pharmacy: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- 9.5 Others

- 9.5.1 Overview

- 9.5.2 Others: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

10. North America Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 - by End User

- 10.1 Overview

- 10.2 Intravenous Immunoglobulin Market Revenue Share, by Species, 2022 & 2030 (%)

- 10.3 Hospitals

- 10.3.1 Overview

- 10.3.2 Hospitals: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- 10.4 Specialty Clinics

- 10.4.1 Overview

- 10.4.2 Specialty Clinics: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

- 10.5 Others

- 10.5.1 Overview

- 10.5.2 Others: Intravenous Immunoglobulin Market - Revenue and Forecast to 2030 (US$ Million)

11. North America Intravenous Immunoglobulin Market - Geographical Analysis

- 11.1 North America Intravenous Immunoglobulin Market, Revenue and Forecast To 2030

- 11.1.1 Overview

- 11.1.2 North America Intravenous Immunoglobulin Market Revenue and Forecast to 2030 (US$ Mn)

- 11.1.3 North America: Intravenous Immunoglobulin Market, by Type, 2020-2030 (US$ Million)

- 11.1.4 North America: Intravenous Immunoglobulin Market, by Application, 2020-2030 (US$ Million)

- 11.1.5 North America: Intravenous Immunoglobulin Market, by Distribution Channel, 2020-2030 (US$ Million)

- 11.1.6 North America: Intravenous Immunoglobulin Market, by End User, 2020-2030 (US$ Million)

- 11.1.7 North America Intravenous Immunoglobulin Market, by Country

- 11.1.7.1 US

- 11.1.7.1.1 Overview

- 11.1.7.1.2 US Intravenous Immunoglobulin Market Revenue and Forecast to 2030 (US$ Mn)

- 11.1.7.1.3 US: Intravenous Immunoglobulin Market, by Type, 2020-2030 (US$ Million)

- 11.1.7.1.4 US: Intravenous Immunoglobulin Market, by Application, 2020-2030 (US$ Million)

- 11.1.7.1.5 US: Intravenous Immunoglobulin Market, by Distribution Channel, 2020-2030 (US$ Million)

- 11.1.7.1.6 US: Intravenous Immunoglobulin Market, by End User, 2020-2030 (US$ Million)

- 11.1.7.2 Canada

- 11.1.7.2.1 Overview

- 11.1.7.2.2 Canada Intravenous Immunoglobulin Market Revenue and Forecast to 2030 (US$ Mn)

- 11.1.7.2.3 Canada: Intravenous Immunoglobulin Market, by Type, 2020-2030 (US$ Million)

- 11.1.7.2.4 Canada: Intravenous Immunoglobulin Market, by Application, 2020-2030 (US$ Million)

- 11.1.7.2.5 Canada: Intravenous Immunoglobulin Market, by Distribution Channel, 2020-2030 (US$ Million)

- 11.1.7.2.6 Canada: Intravenous Immunoglobulin Market, by End User, 2020-2030 (US$ Million)

- 11.1.7.3 Mexico

- 11.1.7.3.1 Overview

- 11.1.7.3.2 Mexico Intravenous Immunoglobulin Market Revenue and Forecast to 2030 (US$ Mn)

- 11.1.7.3.3 Mexico: Intravenous Immunoglobulin Market, by Type, 2020-2030 (US$ Million)

- 11.1.7.3.4 Mexico: Intravenous Immunoglobulin Market, by Application, 2020-2030 (US$ Million)

- 11.1.7.3.5 Mexico: Intravenous Immunoglobulin Market, by Distribution Channel, 2020-2030 (US$ Million)

- 11.1.7.3.6 Mexico: Intravenous Immunoglobulin Market, by End User, 2020-2030 (US$ Million)

- 11.1.7.1 US

12. North America Intravenous Immunoglobulin Market - Industry Landscape

- 12.1 Overview

- 12.2 Growth Strategies in North America Intravenous Immunoglobulin Market

- 12.3 Inorganic Growth Strategies

- 12.3.1 Overview

- 12.4 Organic Growth Strategies

- 12.4.1 Overview

13. Company Profiles

- 13.1 Takeda Pharmaceutical Co Ltd

- 13.1.1 Key Facts

- 13.1.2 Business Description

- 13.1.3 Products and Services

- 13.1.4 Financial Overview

- 13.1.5 SWOT Analysis

- 13.1.6 Key Developments

- 13.2 Grifols SA

- 13.2.1 Key Facts

- 13.2.2 Business Description

- 13.2.3 Products and Services

- 13.2.4 Financial Overview

- 13.2.5 SWOT Analysis

- 13.2.6 Key Developments

- 13.3 Pfizer Inc

- 13.3.1 Key Facts

- 13.3.2 Business Description

- 13.3.3 Products and Services

- 13.3.4 Financial Overview

- 13.3.5 SWOT Analysis

- 13.3.6 Key Developments

- 13.4 ADMA Biologics, Inc.

- 13.4.1 Key Facts

- 13.4.2 Business Description

- 13.4.3 Products and Services

- 13.4.4 Financial Overview

- 13.4.5 SWOT Analysis

- 13.4.6 Key Developments

- 13.5 Bio Products Laboratory Ltd.

- 13.5.1 Key Facts

- 13.5.2 Business Description

- 13.5.3 Products and Services

- 13.5.4 Financial Overview

- 13.5.5 SWOT Analysis

- 13.5.6 Key Developments

- 13.6 Octapharma AG

- 13.6.1 Key Facts

- 13.6.2 Business Description

- 13.6.3 Products and Services

- 13.6.4 Financial Overview

- 13.6.5 SWOT Analysis

- 13.6.6 Key Developments

- 13.7 Kedrion SpA

- 13.7.1 Key Facts

- 13.7.2 Business Description

- 13.7.3 Products and Services

- 13.7.4 Financial Overview

- 13.7.5 SWOT Analysis

- 13.7.6 Key Developments

- 13.8 CSL Ltd

- 13.8.1 Key Facts

- 13.8.2 Business Description

- 13.8.3 Products and Services

- 13.8.4 Financial Overview

- 13.8.5 SWOT Analysis

- 13.8.6 Key Developments

- 13.9 LFB Group

- 13.9.1 Key Facts

- 13.9.2 Business Description

- 13.9.3 Products and Services

- 13.9.4 Financial Overview

- 13.9.5 SWOT Analysis

- 13.9.6 Key Developments

- 13.10 Prothya Biosolutions B.V.

- 13.10.1 Key Facts

- 13.10.2 Business Description

- 13.10.3 Products and Services

- 13.10.4 Financial Overview

- 13.10.5 SWOT Analysis

- 13.10.6 Key Developments

14. Appendix

- 14.1 About Us

- 14.2 Glossary of Terms