世界のエレクトロニクス分野の需要の概要(2025年)

Overview of Global Electronics Sector's Demand in 2025- 発行

- TrendForce

- 発行日

- ページ情報

- 英文 5 Pages

- 納期

- 即日から翌営業日

- 商品コード

- 1794797

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

- 電子部品/半導体関連専門 電子部品/半導体関連専門を専門とする市場調査会社です。

概要

2025年、エレクトロニクス業界の動向は、「旺盛なAI需要、低調なコンシューマーデバイス、早期引き込みが季節性を消し去り、将来の成長は鈍化」と動向は分かれます。

インフォグラフィックス

主なハイライト

- 2025年、AI需要が急増する一方、民生用電子機器(スマートフォン、ノートパソコン、テレビ)の成長は停滞またはわずか。

- 関税と補助金の影響により早期に在庫が引き揚げられ、従来の販売ピークが混乱し、年後半のリスクが高まる。

- クラウド・プロバイダーは、関税の影響が少ないAIサーバーへの設備投資を拡大し、一般サーバーの予算を圧迫します。「AIは単独で成功。」

- エッジAIは勢いを失い、エンドデバイスは魅力的なAIアプリケーションを欠き、アップグレードを促進できず、消費者の関心も高まらない見込み。

- 2026年までに、業界は低成長別統合フェーズに入り、大半の製品は低調なまま、AIサーバーの勢いは弱まる。

- 関税の不確実性がPC OEMとサプライヤーの生産戦略に影響を与える。

目次

第1章 関税と補助金により需要が前倒しされ、伝統的なピークシーズンが混乱している

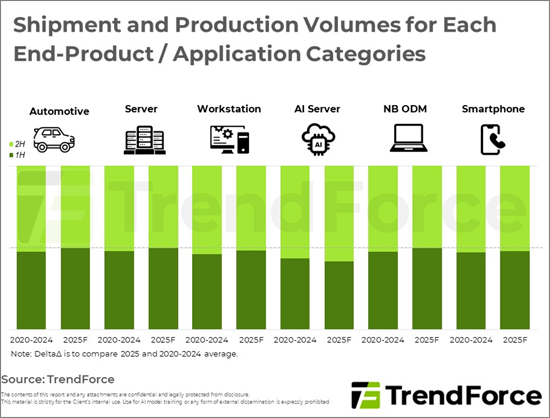

- 最終製品・用途別出荷・生産量-2025年上半期と2025年下半期の年間出荷量の分布と過去5年間の平均との比較

第2章 AIサーバーの需要は着実に増加しています。他のアプリケーションに比べて料金関連の不確実性の影響を受けにくく、CSPの設備投資増加の恩恵を受けている。

第3章 エッジAIの話題は沈静化しつつあるもの、代替波はまだ起こっていない模様。キラーアプリケーションは当面保留中。

第4章 2026年を見据えて - 成長鈍化の中、業界は低速成長と統合へ

目次

Product Code: TRi-0082

In 2025, the electronics industry sees diverging trends: strong AI demand, weak consumer devices, early pull-in erases seasonality, and future growth slows.

INFOGRAPHICS

Key Highlights:

- In 2025, AI demand surges while consumer electronics-smartphones, laptops, TVs-see stagnant or minimal growth.

- Tariff and subsidy impacts cause early inventory pull-in, disrupting traditional sales peaks and raising risks in the year's latter half.

- Cloud providers grow capital spending on AI servers, with less tariff impact, squeezing budgets for general servers. "AI alone thrives."

- Edge AI loses momentum; end devices lack compelling AI applications, failing to drive upgrades or noticeable consumer interest.

- By 2026, the industry enters a consolidation phase with slow growth, most products remain weak, and AI server momentum eases; breakthroughs needed for future cycles.

- Tariff uncertainty impacts PC OEMs' and suppliers' production strategies; DRAM supply-demand and other components merit close watch.

Table of Contents

1. Tariffs and Subsidies Have Caused Demand to Be Pulled Forward and Disrupts Traditional Peak Season

- Shipment and Production Volumes for Each End-Product / Application Categories - Distribution of Annual Shipments Between 1H25 and 2H25 vs. Averages of Previous Five Years

2. Demand Grows Steadily for AI Servers, Which Are Less Affected by Tariff-Related Uncertainties Compared with Other Applications and Have Benefited from CSPs' Increasing Capital Expenditure

3. Subsiding Topic of Edge AI Yet to Ignite Replacement Wave; Killer Applications Pending for the Time Being

4. Looking Ahead to 2026: Industry Enters Low-Speed Growth and Consolidation under Decelerating Increment

世界のエレクトロニクス分野の需要の概要(2025年)

- 発行日

- 発行

- TrendForce

- ページ情報

- 英文 5 Pages

- 納期

- 即日から翌営業日