|

|

市場調査レポート

商品コード

1774033

レアアース業界動向:中国対米国および2025年の世界の展望Rare Earth Industry Dynamics: China vs US and 2025 Global Outlook |

||||||

|

|||||||

| レアアース業界動向:中国対米国および2025年の世界の展望 |

|

出版日: 2025年06月17日

発行: TrendForce

ページ情報: 英文 19 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 目次

概要

家電、通信、自動車、産業オートメーション、ロボット工学、再生可能エネルギー、原子力、ヘルスケア、軍事、航空宇宙、航空分野など、レアアースから作られる主要部品や材料は、事実上どこにでもあります。その重要性は疑う余地がありません。

サンプル

当レポートでは、レアアースサプライチェーンの川上、川中、川下セグメントを包括的に分析しています。また、この業界における中国の支配的な役割を検証し、米国とその同盟国がどのように対応策を練っているかを探ります。

主なハイライト

- レアアースは、エレクトロニクス、エネルギー、防衛など、さまざまな分野で重要な役割を担っています。

- 当レポートでは、川上、川中、川下というバリューチェーン全体を検証しています。

- 業界における中国の優位性についても考察します。

- 米国と同盟国の対応策を探ります。

目次

第1章 レアアースは広く利用されており、石油に劣らず重要である

第2章 中国はレアアースの生産と埋蔵量で世界をリードし、レアアースの主要供給国である

第3章 中国はレアアースの上流・中流サプライチェーンで大きな優位性を持つ

第4章 中国のレアアース輸出規制は広範囲に及ぶ影響を及ぼし、米国はサプライチェーンのギャップを埋めるのに3~5年かかる見通し

第5章 TRIの視点

Overview

Key components and materials made from rare earth elements are virtually ubiquitous-found across consumer electronics, telecommunications, automotive, industrial automation, robotics, renewable energy, nuclear power, healthcare, military, aerospace, and aviation sectors. Their importance is beyond question.

SAMPLE VIEW

This report provides a comprehensive analysis of the upstream, midstream, and downstream segments of the rare earth supply chain. It also examines China's dominant role within this industry and explores how the US and its allies are strategizing to respond.

Key Highlights:

- Rare earth elements are critical in diverse sectors, including electronics, energy, and defense.

- The report examines the entire value chain: upstream, midstream, and downstream.

- China's dominance in the industry is discussed.

- Strategies from the US and allies in response are explored.

Table of Contents

1. Rare Earth Elements Are Widely Used and No Less Critical Than Oil

- Figure 1: Rare Earth Elements Include Scandium, Yttrium, and the Lanthanide Series

- Table 1: Rare Earth Element-Based Components, Materials, and Their End Applications

2. China Leads the Way in Rare Earth Production and Reserves, and Is the Primary Supplier of Heavy Rare Earth Elements

- Table 2: Rare Earth Deposit Types and Production Sites

- Figure 2: Share of Global Rare Earth Production by Country/Region in 2024

- Table 3: 2024 Rare Earth Production by Country/Region

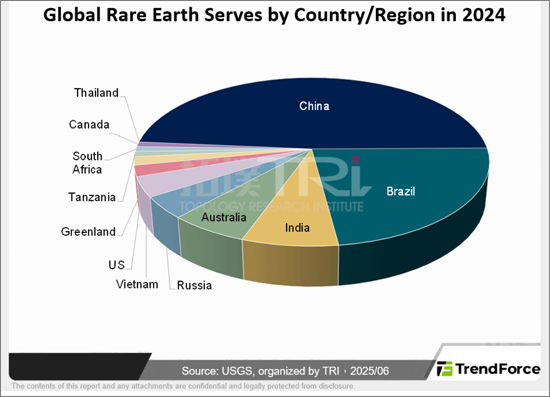

- Figure 3: Share of Global Rare Earth Reserves by Country/Region in 2024

- Table 4: Rare Earth Reserves by Country/Region

3. China Holds Significant Advantages in the Upstream and Midstream Rare Earth Supply Chain

- Figure 4: Overview of the Global Rare Earth Supply Chain

4. China's Rare Earth Export Controls Have Far-Reaching Impacts; US Will Need 3-5 Years to Fill Supply Chain Gaps

- Figure 5: Restricted Items under China's Ministry of Commerce and General Administration of Customs Announcement No. 18

- Table 5: Rare Earth Resources Response Strategies of the US and Its Allies

- Table 6: Estimated Timeline of the Impact of China's Rare Earth Export Controls on the Global Downstream Supply Chain