マイクロLEDのディスプレイおよび非ディスプレイ用途の市場分析 (2025年)

2025 Micro LED Display and Non-Display Application Market Analysis- 発行

- TrendForce

- 発行日

- ページ情報

- 英文 119 Pages

- 納期

- 即日から翌営業日

- 商品コード

- 1742160

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

- 電子部品/半導体関連専門 電子部品/半導体関連専門を専門とする市場調査会社です。

概要

【インサイト】マイクロLEDはディスプレイを超えて拡大、透明・非ディスプレイ用途で新たな可能性を切り拓く

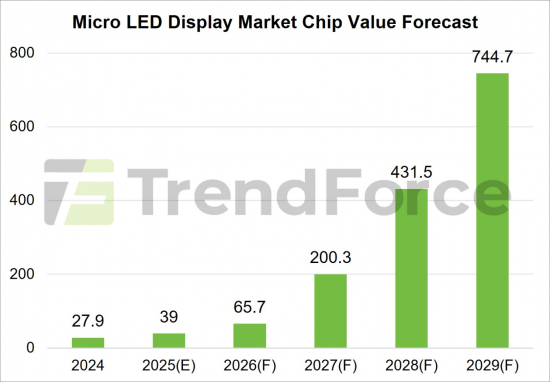

ディスプレイ分野におけるマイクロLED技術の現在の開発は、設計および生産改善による製造コストの最適化と、独自のニッチ市場の特定という2つの主要課題に焦点を当てていると報告されています。マイクロLEDのディスプレイ用途におけるチップの市場規模は2029年には7億4,000万米ドルに達し、2024年から2029年までのCAGRは93%に達すると予測されています。

大型ディスプレイにおけるコスト改善が進行中

現在、マイクロLEDのディスプレイ関連市場の大部分は、大型ディスプレイによって構成されており、Samsungがこの分野で主導的地位を占めています。今後の成長には、いくつかの重要な製造工程のブレークスルーだけでなく、中国のチップ製造業者とブランド製造業者の協業によるチップの小型化の推進が必要とされます。これにより、量産型マイクロLED大型ディスプレイのコスト優位性がさらに強化される見込みです。

また、AIの進展によりヘッドマウントデバイスの利用シーンが拡大していることや、スマートドライビングエコシステムの発展によって先進的な車載ディスプレイへの需要が高まっていることから、この2つの分野は今後のマイクロLEDディスプレイ市場の主要な柱となると予測されています。

TrendForceは、マイクロLED大型ディスプレイの業界標準として、一般的に4K以上の解像度が求められていると指摘していますが、現在商業化されて量産可能なピクセルピッチは依然として0.5mmにとどまっています。Mini LEDのビデオウォールとの差別化を進めるためにも、さらなるピクセルピッチの縮小が不可欠であり、加えてドライバ接続部の低歩留まりやパネル接合部 (シーム) の問題といった課題の克服も求められています。

コスト最適化の取り組みは、製造プロセスを簡素化して歩留まりを改善し、接合部を減らすことで組立工程を削減できるバックプレーン側にもシフトしています。これらの工夫はトータルコストの削減に寄与します。

マイクロLEDの際立った特性である高輝度、高コントラスト、高透明性は、引き続き製造業者からの投資を集めており、これらの特性により、マイクロLEDは車載ウィンドウ向け透明ディスプレイや、AR-HUD、P-HUDといったシステムへの統合が可能となります。これにより、運転者および同乗者に対し、仮想情報と現実情報のシームレスな統合に対する需要に応えることができます。さらに、マイクロLEDをシリコン基板と組み合わせることで、ARグラス向けのニアアイディスプレイにおいて強力なソリューションが提供可能となり、マイクロLEDは次世代メタバース対応型ヘッドマウントデバイスの基準技術としての地位を築きつつあります。

当レポートでは、マイクロLEDのディスプレイおよび非ディスプレイ用途の市場を調査し、マイクロLEDの技術開発の動向、マイクロLEDのディスプレイおよび非ディスプレイ用途の市場規模の推移・予測、マイクロLED透明ディスプレイの動向、主要製造業者のプロファイルなどをまとめています。

目次

第1章 マイクロLEDディスプレイ市場の分析

- 市場規模の分析:大型ディスプレイ

- 市場規模の分析:ウェアラブルディスプレイ

- 市場規模の分析:ヘッドマウントデバイス

- 市場規模の分析:車載ディスプレイ

- 市場規模の分析

- ウエハ需要の分析

第2章 マイクロLED技術の開発

- モジュールの大型化

- マイクロLEDモジュール大型化/タイル化の削減

- マイクロLEDモジュール大型化の利点 (1/2) - タイル化の省略

- マイクロLEDモジュール大型化の利点 (2/2) - コストおよび商業的メリット

- モジュールサイズとタイルサイズの関係

- 経済的に最適なモジュールサイズの決定

- マイクロLEDモジュール大型化における課題

- マイクロLEDのタイル化:大型モジュール vs 小型モジュール

- タイル型ディスプレイ

- タイル接合部における技術的課題

- マイクロLEDタイル化の商業戦略:ピクセルピッチの観点から

- マイクロLEDタイル型ディスプレイにおける商業化可能な最小サイズ:UHD (超高精細)

- マイクロLEDタイル型ディスプレイにおける商業化可能な最大サイズ:経済的タイル化の観点から

- 商業化された大型マイクロLEDディスプレイに最も適したサイズ

- ガラス:サファイアベースのCOCの潜在的競合素材

- マイクロLEDの放熱に関する課題

- マイクロLEDのPPIに関する課題

- 高効率マイクロLED実現への宣言:達成は目前

- マイクロLED業界動向 (1/2) :専門用途ディスプレイへの展開

- マイクロLED業界動向 (2/2) :ARに注力するマイクロLED企業

第3章 マイクロLED透明ディスプレイ

- 透過型ディスプレイの2つの方式:ダイレクトビュー方式とマイクロディスプレイ投影方式

- ダイレクトビュー方式と投影方式の主な違い (1/2) :視野角

- ダイレクトビュー方式と投影方式の主な違い (2/2) :焦点の問題

- 透明ダイレクトビュー型ディスプレイの課題:鮮やかさと実在感のトレードオフ関係

- 2種類の透明ディスプレイのベンチマーク比較

- 透明ダイレクトビュー型ディスプレイのSWOT分析

- 用途別にみた透明ダイレクトビュー型ディスプレイのSWOT分析

- 透明ダイレクトビュー型ディスプレイの開発動向分析

- 透明ディスプレイ用途を選定する際の考慮点

- 各種透明ディスプレイによる技術原理の違い

- JDI、LCDで透明ディスプレイ市場に再参戦

- 透明ディスプレイの応用事例

- 透明ディスプレイにおける輝度と透過率のパラドックス

- マイクロLED透明ディスプレイ

- 各種透明ディスプレイ技術の比較

- 量産された透明ディスプレイの価格比較

第4章 マイクロLED製造業者の動向

- 2025年のマイクロLED企業の製造能力分析

- PlayNitride

- Ennostar

- HC Semitek

- AUO

- Innolux

- Extremely PQ

- Tianma

- BOE

- LGD

- Samsung

- Hisense

- Hongshi

- VueReal

- Aledia

付録

目次

[Insight] Micro LED Expands Beyond Displays, Unlocking New Opportunities in Transparent and Non-Display Applications

TrendForce's latest report, "2025 Micro LED Display and Non-Display Application Market Analysis", reveals that the current development of Micro LED technology in the display sector focuses on two key challenges: optimizing manufacturing costs through design and production improvements, and identifying unique niche markets.

TrendForce forecasts that the chip market value for Micro LED display applications will reach US$740 million by 2029, with a CAGR of 93% from 2024 to 2029.

Cost improvements continue for large-sized displays

Presently, the bulk of Micro LED's display-related market value is driven by large-sized displays, where Samsung holds a leading position. Future growth will rely not only on breakthrough across several critical manufacturing processes but also on collaborations between Chinese chipmakers and brand manufacturers to push chip miniaturization. This will further enhance cost advantages for mass-produced Micro LED large-sized displays.

Additionally, as AI broadens the application scenarios for head-mounted devices and as smart driving ecosystems drive up demand for advanced automotive displays, these two sectors are expected to become major pillars of Micro LED display market value in the years ahead.

TrendForce notes that the industry standard for Micro LED large-sized displays is typically 4K resolution or higher; however, the currently commercialized, mass-producible pixel pitch remains at 0.5 mm. Continued efforts to reduce pixel pitch are essential to further differentiate Micro LED from Mini LED video wall , along with overcoming challenges like low yield rates in driver connections and issues with panel seams.

Cost optimization is also shifting toward the backplane, where simplifying the manufacturing process can improve yields, and reducing the number of seams can cut down assembly steps. This contributes to overall cost reductions.

Micro LED's standout characteristics-high brightness, high contrast, and high transparency-continue to attract investment from manufacturers. These features enable Micro LED to integrate into transparent displays for automotive windows or as part of AR-HUD or P-HUD systems, meeting the growing demand for seamless integration of virtual and real-world information for drivers and passengers. Additionally, combining Micro LED with silicon substrates offers a robust solution for near-eye displays in AR glasses, positioning Micro LED as a benchmark for next-generation metaverse-focused head-mounted devices.

Transparent displays hold great promise; non-display applications open new doors

Micro LED technology also shows strong potential in transparent display applications. These can be categorized into direct-view and micro-projection systems, with the key differences lying in viewing angels and focal distance management. In terms of use case, transparent direct-view displays are better suited for public environments where content is viewed by multiple people, and Micro LED's combination of high brightness and high transparency makes it an ideal technology.

Meanwhile, micro-projection systems hold greater promise in privacy-sensitive personal electronic devices, where Micro LED offers ultra-miniaturized light engine solutions and is seen as the best option for micro-display technology in AR applications. Overall, Micro LED has significant room for expansion across diverse transparent display segments by developing both TFT and CMOS backplane platforms.

TrendForce emphasizes that the immediate priority for the Micro LED industry is to scale up the market quickly in order to realize economic efficiencies. As a result, non-display sectors have increasingly become important avenues for growth in addition to focusing on display applications.

These non-display opportunities span a wide range, including optical communication applications accelerated by AI, biotechnology-related medical uses, and industrial production areas such as 3D printing and photopolymerization. Ongoing innovations in these areas are adding further momentum to Micro LED's market expansion.

Table of Contents

Chapter 1. Micro LED Display Market Analysis

- 2025-2029 Micro LED Market Value Analysis-Large-sized Displays

- 2025-2029 Micro LED Market Value Analysis-Wearable Displays

- 2025-2029 Micro LED Market Value Analysis-Head-mounted Devices

- 2025-2029 Micro LED Market Value Analysis-Automotive Displays

- 2025-2029 Micro LED Market Value Analysis

- 2025-2029 Micro LED Wafer Demand Analysis

Chapter 2. Micro LED Technology Development

- 2.1. Module Enlargement

- Micro LED Module Enlargement/Reduced Tiling

- Enlarging Micro LED Modules Advantages (1/2) - Tiling Omitted

- Enlarging Micro LED Modules Advantages (2/2) - Cost and Commercial Benefits

- Relationships between Module Size and Tiling Size

- Deciding Economic Module Size

- Micro LED Module Enlargement Challenges

- Micro LED Tiling: Large Modules vs. Small Modules

- 2.2. Tiling Display

- Tiling Seams Technical Challenges

- Micro LED Tiling Commercial Strategies : A Pixel Pitch Perspective

- Lower Limit of Commercialization Size for Micro LED-tiled Displays: UHD

- Upper Limit of Commercialization Size for Micro LED-tiled Displays: Economic Tiling

- Most Suitable Sizes for Commercialized Large-sized Micro LED Displays

- Glass: A Potential Competitor to Sapphire-based COC

- Micro LED Heat Dissipation Challenges

- Micro LED PPI Challenges

- Manifesto for Achieving High-Efficiency Micro LED is Within Reach

- Micro LED Industrial Trends (1/2): Towards Specialized Display

- Micro LED Industrial Trends (2/2): Micro LED Enterprises to Focus on AR

Chapter 3. Micro LED Transparent Display

- Two Systems for See-through Displays: Direct-view and Micro display Projection

- Key Differences between Direct-view and Projection Systems (1/2): Viewing Angle

- Key Differences between Direct-view and Projection Systems (2/2): Focus Issues

- Transparent Direct-View Displays Challenges : Mutually Exclusive Relationship between Vitality and Reality

- Benchmarks between the Two Types of Transparent Displays

- Transparent Direct-view Displays SWOT Analysis

- Transparent Direct-view Displays across Different Applications SWOT Analysis

- Transparent Direct-view Displays Development Trend Analysis

- Things to Consider When Selecting Transparent Display Applications

- Technology Principles by Different Transparent Displays

- JDI Brings LCD Back to Transparent Display Competition

- Transparent Display Application Cases

- The Brightness-Transmittance Paradox in Transparent Displays

- Micro LED Transparent Displays

- Comparison between Different Transparent Display Technologies

- Prices of Mass-produced Transparent Displays

Chapter 4. Micro LED Manufacturer Dynamic

- 2025 Micro LED Player Capacity Analysis.

- PlayNitride

- Ennostar

- HC Semitek

- AUO

- Innolux

- Extremely PQ

- Tianma

- BOE

- LGD

- Samsung

- Hisense

- Hongshi

- VueReal

- Aledia

Appendix

- Intel-Samsung Patent Sale

- Advancing non-display Micro LED Technology Development - Avicena

- 発行日

- 発行

- TrendForce

- ページ情報

- 英文 119 Pages

- 納期

- 即日から翌営業日