|

|

市場調査レポート

商品コード

1657231

DevOpsにおける生成AIの世界市場:2034年までの機会と戦略Generative AI In DevOps Global Market Opportunities And Strategies To 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| DevOpsにおける生成AIの世界市場:2034年までの機会と戦略 |

|

出版日: 2025年02月17日

発行: The Business Research Company

ページ情報: 英文 294 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

世界のDevOpsにおける生成AI市場は、2019年に3億6,454万米ドルと評価され、2024年までCAGR38.00%以上で成長しました。

インターネット普及率の増加

インターネット普及率の増加は、過去の実績期間中、DevOpsにおける生成AI市場の成長を後押ししました。インターネット普及率の増加により、開発および運用ワークフローに生成AIを統合するために不可欠なクラウドベースのツールやコラボレーションプラットフォームへのアクセスが強化されました。この接続性により、シームレスなデータ共有、リアルタイム分析、自動化が可能になり、DevOps市場の効率化と普及が促進されます。例えば、シンガポールを拠点とするオンラインレファレンスライブラリーであるDataReportalによると、2022年10月、世界で合計50億7,000万人がインターネットを利用しており、これは世界総人口の63.5%に相当します。インターネットユーザーも増え続けており、過去12ヶ月で世界の接続人口は1億7,000万人以上増加したとのデータもあります。さらに、ITU(国際通信連合)によると、世界全体で、インターネットに接続できる世帯の割合は2018年の54.7%から2019年には57%に増加しました。2019年には約45億人がインターネットにアクセスできるようになりました。FacebookによるInternet.orgなどの取り組みもインターネット普及率の上昇に貢献しました。したがって、インターネット普及率の増加は、DevOpsにおける生成AI市場の成長を後押ししました。

目次

第1章 エグゼクティブサマリー

- DevOpsにおける生成AI-市場の魅力とマクロ経済情勢

第2章 目次

第3章 表一覧

第4章 図一覧

第5章 レポート構成

第6章 市場の特徴

- 一般的な市場の定義

- 概要

- DevOpsにおける生成AI市場の定義とセグメンテーション

- 市場セグメンテーション:コンポーネント別

- ソリューション

- サービス

- 市場セグメンテーション:展開別

- オンプレミス

- クラウドベース

- 市場セグメンテーション:用途別

- テスト

- 展開

- 監視

- メンテナンス

- その他の用途

第7章 主要な市場動向

- DevOpsの自動化とスケーラビリティを強化するAIインフラの進歩

- 革新的な生成AIプロダクションスタックによるDevOpsの自動化とスケーラビリティ強化

- AIを活用したDevSecOpsプラットフォームによるクラウドネイティブアプリケーションのセキュリティと開発効率の向上

第8章 DevOpsにおける生成AI市場:マクロ経済シナリオ

- COVID-19の影響: DevOpsにおける生成AI市場

- ウクライナ戦争の影響: DevOpsにおける生成AI市場

- 高インフレの影響: DevOpsにおける生成AI市場

第9章 世界の市場規模と成長

- 市場規模

- 市場成長実績、2019~2024年

- 市場促進要因、2019~2024年

- 市場抑制要因、2019~2024年

- 市場成長予測,、2024~2029年、2034年

- 市場促進要因、2024~2029年

- 市場抑制要因、2024~2029年

第10章 世界のDevOpsにおける生成AI市場:セグメンテーション

- 世界のDevOpsにおける生成AI市場:コンポーネント別、実績と予測、2019~2024年、2029年、2034年

- 世界のDevOpsにおける生成AI市場:展開別、実績と予測、2019~2024年、2029年、2034年

- 世界のDevOpsにおける生成AI市場:用途別、実績と予測、2019~2024年、2029年、2034年

第11章 DevOpsにおける生成AI市場:地域・国別分析

- 世界のDevOpsにおける生成AI市場:地域別、実績と予測、2019~2024年、2029年、2034年

- 世界のDevOpsにおける生成AI市場:国別、実績と予測、2019~2024年、2029年、2034年

第12章 アジア太平洋市場

第13章 西欧市場

第14章 東欧市場

第15章 北米市場

第16章 南米市場

第17章 中東市場

第18章 アフリカ市場

第19章 競合情勢と企業プロファイル

- 企業プロファイル

- Microsoft Corporation

- Alphabet Inc(Google LLC)

- Amazon Web Services Inc

- International Business Machines Corporation(IBM)

- Oracle Corporation

第20章 その他の大手企業と革新的企業

- NVIDIA Corporation

- Cisco Systems Inc

- Capgemini SE

- OpenAI

- NetApp Inc

- Dell Technologies Inc

- Cognizant Technology Solutions Corporation

- Intellias

- CloudBees Inc

- Wipro Limited

- 10Clouds

- Yellow Systems

- InData Labs

- ThirdEye Data

- SoluLab

第21章 競合ベンチマーキング

第22章 競合ダッシュボード

第23章 主要な合併と買収

- Nvidia Acquires OctoAI For$250 Million To Strengthen Enterprise AI And Generative AI Solutions

- Jfrog Acquires Qwak For$230 Million To Enhance MlOps Capabilities And Strengthen AI-Driven DevOps Platform

- Cisco Acquires Splunk For$28 Billion To Enhance AI-Driven Solutions In Security, IT Operations And Cloud Services

第24章 機会と戦略

- 世界のDevOpsにおける生成AI市場2029年:新たな機会を提供する国

- 世界のDevOpsにおける生成AI市場2029年:新たな機会を提供するセグメント

- 世界のDevOpsにおける生成AI市場2029:成長戦略

- 市場動向に基づく戦略

- 競合の戦略

第25章 DevOpsにおける生成AI市場:結論と提言

- 結論

- 提言

- 製品

- 場所

- 価格

- プロモーション

- 人々

第26章 付録

Generative Artificial Intelligence (AI) in development and operations (DevOps) refers to the integration of AI models capable of producing new content, such as code, configurations or test cases, into the DevOps lifecycle. This integration aims to enhance automation, efficiency and innovation in software development and operational processes.

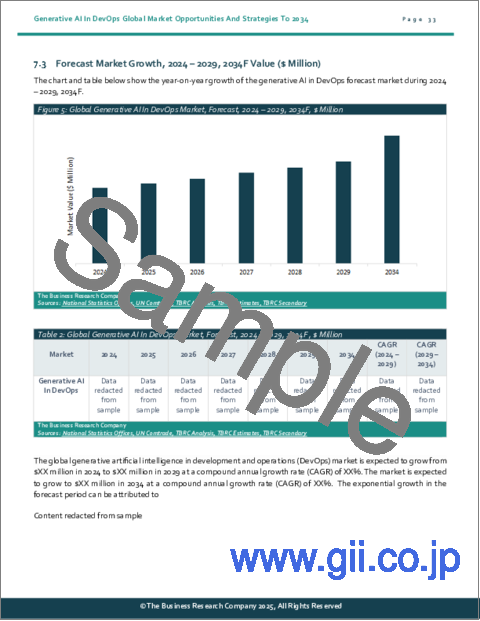

The global generative artificial intelligence in development and operations (DevOps) market was valued at $364.54 million in 2019 which grew till 2024 at a compound annual growth rate (CAGR) of more than 38.00%.

Increasing Internet Penetration

Increasing internet penetration boosted the growth of generative AI in DevOps market during the historic period. The increase in internet penetration has enhanced access to cloud-based tools and collaborative platforms, which are essential for integrating generative artificial intelligence into development and operations workflows. This connectivity enables seamless data sharing, real-time analysis and automation, driving efficiency and adoption in the development and operations market. For instance, in October 2022, according to DataReportal, a Singapore-based online reference library, a total of 5.07 billion people around the world used the internet, equivalent to 63.5% of the world's total population. Internet users continue to grow too, with the data indicating that the world's connected population grew by more than 170 million in the past 12 months. Additionally, according to the ITU (International Telecommunication Union), globally, the percentage of households with internet access increased from 54.7% in 2018 to 57% in 2019. About 4.5 billion people had access to the internet in 2019. Initiatives such as Internet.org by Facebook also contributed to the rise in internet penetration. Therefore, increasing internet penetration boosted the growth of generative AI in DevOps market.

Advancements In AI Infrastructure For Enhanced DevOps Automation And Scalability

Major companies in the generative AI in DevOps market are focusing on developing innovative solutions to enhance AI model training and deployment efficiency, driving advancements in automation and scalability for DevOps processes. For instance, in September 2024, Intel Corporation, a US-based technology company and manufacturer of semiconductor products, launched Xeon 6, with Performance-cores (P-cores) and Gaudi 3 AI, specialized hardware accelerators, to meet the growing demand for cost-effective AI infrastructure. The Xeon 6 delivers twice the performance of its predecessor, offering increased core count, doubled memory bandwidth and AI acceleration capabilities. The Gaudi 3 AI accelerator is specifically optimized for large-scale generative AI, offering 64 Tensor processor cores and eight matrix multiplication engines for deep neural network computations. It also includes 128 gigabytes of HBM2e memory for training and inference and 24 200 Gigabit Ethernet ports for scalable networking. Intel has also announced a collaboration with IBM, a US-based technology company, to deploy Intel Gaudi 3 AI accelerators as a service on IBM Cloud, aiming to lower the total cost of ownership, while enhancing performance. Intel's robust x86 infrastructure and extensive open ecosystem position it to support enterprises in building high-value AI systems with optimal TCO (Total Cost of Ownership) and performance per watt.

The global generative AI in DevOps market is fairly fragmented, with a large number of small players operating in the market. The top ten competitors in the market made up to 15.8% of the total market in 2023.

Generative AI In DevOps Global Market Opportunities And Strategies To 2034 from The Business Research Company provides the strategists; marketers and senior management with the critical information they need to assess the global generative AI in DevOps market as it emerges from the COVID-19 shut down.

Reasons to Purchase

- Gain a truly global perspective with the most comprehensive report available on this market covering 15 geographies.

- Understand how the market is being affected by the coronavirus and how it is likely to emerge and grow as the impact of the virus abates.

- Create regional and country strategies on the basis of local data and analysis.

- Identify growth segments for investment.

- Outperform competitors using forecast data and the drivers and trends shaping the market.

- Understand customers based on the latest market research findings.

- Benchmark performance against key competitors.

- Utilize the relationships between key data sets for superior strategizing.

- Suitable for supporting your internal and external presentations with reliable high-quality data and analysis.

Where is the largest and fastest-growing market for generative AI in DevOps? How does the market relate to the overall economy; demography and other similar markets? What forces will shape the market going forward? The generative AI in DevOps market global report from The Business Research Company answers all these questions and many more.

The report covers market characteristics; size and growth; segmentation; regional and country breakdowns; competitive landscape; market shares; trends and strategies for this market. It traces the market's history and forecasts market growth by geography. It places the market within the context of the wider generative AI in DevOps market; and compares it with other markets.

The report covers the following chapters

- Introduction and Market Characteristics- Brief introduction to the segmentations covered in the market, definitions and explanations about the segment by component, by deployment mode and by application.

- Key Trends- Highlights the major trends shaping the global market. This section also highlights likely future developments in the market.

- Macro-Economic Scenario- The report provides an analysis of the impact of the COVID-19 pandemic, impact of the Russia-Ukraine war and impact of rising inflation on global and regional markets, providing strategic insights for businesses in the generative AI in DevOps market.

- Global Market Size And Growth- Global historic (2019-2024) and forecast (2024-2029, 2034F) market values and drivers and restraints that support and control the growth of the market in the historic and forecast periods.

- Regional And Country Analysis- Historic (2019-2024) and forecast (2024-2029, 2034F) market values and growth and market share comparison by region and country.

- Market Segmentation- Contains the market values (2019-2024) (2024-2029, 2034F) and analysis for each segment by component, by deployment mode and by application in the market. Historic (2019-2024) and forecast (2024-2029) and (2029-2034) market values and growth and market share comparison by region market.

- Regional Market Size and Growth- Regional market size (2024), historic (2019-2024) and forecast (2024-2029, 2034F) market values and growth and market share comparison of countries within the region. This report includes information on all the regions Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East and Africa and major countries within each region.

- Competitive Landscape- Details on the competitive landscape of the market, estimated market shares and company profiles of the leading players.

- Other Major And Innovative Companies Details on the company profiles of other major and innovative companies in the market.

- Competitive Benchmarking- Briefs on the financials comparison between major players in the market.

- Competitive Dashboard- Briefs on competitive dashboard of major players.

- Key Mergers and Acquisitions- Information on recent mergers and acquisitions in the market is covered in the report. This section gives key financial details of mergers and acquisitions which have shaped the market in recent years.

- Market Opportunities And Strategies- Describes market opportunities and strategies based on findings of the research, with information on growth opportunities across countries, segments and strategies to be followed in those markets.

- Conclusions And Recommendations- This section includes recommendations for generative AI in DevOps providers in terms of product/service offerings geographic expansion, marketing strategies and target groups.

- Appendix- This section includes details on the NAICS codes covered, abbreviations and currencies codes used in this report.

Markets Covered:

- 1) By Component: Solutions; Services

- 2) By Deployment Mode: On-Premise; Cloud-Based

- 3) By Application: Testing; Deployment; Monitoring; Maintenance; Other Applications

- Companies Mentioned: Microsoft Corporation; Alphabet Inc. (Google LLC); Amazon Web Services Inc.; International Business Machines Corporation; Oracle Corporation

- Countries: China; Australia; India; Indonesia; Japan; South Korea; USA; Canada; Brazil; France; Germany; UK; Italy; Spain; Russia

- Regions: Asia-Pacific; Western Europe; Eastern Europe; North America; South America; Middle East; Africa

- Time-series: Five years historic and ten years forecast.

- Data: Ratios of market size and growth to related markets; GDP proportions; expenditure per capita; generative AI in DevOps indicators comparison.

- Data segmentations: country and regional historic and forecast data; market share of competitors; market segments.

- Sourcing and Referencing: Data and analysis throughout the report is sourced using end notes.

Table of Contents

1 Executive Summary

- 1.1 Generative AI In DevOps - Market Attractiveness And Macro economic Landscape

2 Table Of Contents

3 List Of Tables

4 List Of Figures

5 Report Structure

6 Market Characteristics

- 6.1 General Market Definition

- 6.2 Summary

- 6.3 Generative Artificial Intelligence In Development And Operations (DevOps) Market Definition And Segmentations

- 6.4 Market Segmentation By Component

- 6.4.1 Solutions

- 6.4.2 Services

- 6.5 Market Segmentation By Deployment Mode

- 6.5.1 On-Premise

- 6.5.2 Cloud-based

- 6.6 Market Segmentation By Application

- 6.6.1 Testing

- 6.6.2 Deployment

- 6.6.3 Monitoring

- 6.6.4 Maintenance

- 6.6.5 Other Applications

7 Major Market Trends

- 7.1 Advancements In AI Infrastructure For Enhanced DevOps Automation And Scalability

- 7.2 Innovative Generative AI Production Stack Enhances DevOps Automation And Scalability

- 7.3 AI-Powered DevSecOps Platform Enhances Security And Developer Efficiency For Cloud-Native Applications

8 Generative AI In DevOps Market - Macro Economic Scenario

- 8.1 COVID-19 Impact On The Generative AI In DevOps Market

- 8.2 Impact Of The War In Ukraine On The Generative AI In DevOps Market

- 8.3 Impact Of High Inflation On The Generative AI In DevOps Market

9 Global Market Size and Growth

- 9.1 Market Size

- 9.2 Historic Market Growth, 2019 - 2024, Value ($ Million)

- 9.2.1 Market Drivers 2019 - 2024

- 9.2.2 Market Restraints 2019 - 2024

- 9.3 Forecast Market Growth, 2024 - 2029, 2034F Value ($ Million)

- 9.3.1 Market Drivers 2024 - 2029

- 9.3.2 Market Restraints 2024 - 2029

10 Global Generative AI In DevOps Market Segmentation

- 10.1 Global Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 10.2 Global Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 10.3 Global Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

11 Generative AI In DevOps Market, Regional and Country Analysis

- 11.1 Global Generative AI In DevOps Market, By Region, Historic and Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 11.2 Global Generative AI In DevOps Market, By Country, Historic and Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

12 Asia-Pacific Market

- 12.1 Summary

- 12.1.1 Market Overview

- 12.1.2 Region Information

- 12.1.3 Market Information

- 12.1.4 Background Information

- 12.1.5 Government Initiatives

- 12.1.6 Regulations

- 12.1.7 Regulatory Bodies

- 12.1.8 Major Associations

- 12.1.9 Taxes Levied

- 12.1.10 Corporate Tax Structure

- 12.1.11 Investments

- 12.1.12 Major Companies

- 12.2 Asia-Pacific Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.3 Asia-Pacific Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.4 Asia-Pacific Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.5 Asia-Pacific Generative AI In DevOps Market: Country Analysis

- 12.6 China Market

- 12.7 Summary

- 12.7.1 Market Overview

- 12.7.2 Country Information

- 12.7.3 Market Information

- 12.7.4 Background Information

- 12.7.5 Government Initiatives

- 12.7.6 Regulations

- 12.7.7 Regulatory Bodies

- 12.7.8 Major Associations

- 12.7.9 Taxes Levied

- 12.7.10 Corporate Tax Structure

- 12.7.11 Investments

- 12.7.12 Major Companies

- 12.8 China Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.9 China Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.1 China Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.11 India Market

- 12.12 India Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.13 India Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.14 India Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.15 Japan Market

- 12.16 Japan Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.17 Japan Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.18 Japan Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.19 Australia Market

- 12.2 Australia Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.21 Australia Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.22 Australia Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.23 Indonesia Market

- 12.24 Indonesia Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.25 Indonesia Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.26 Indonesia Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.27 South Korea Market

- 12.28 South Korea Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.29 South Korea Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 12.3 South Korea Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

13 Western Europe Market

- 13.1 Summary

- 13.1.1 Market Overview

- 13.1.2 Region Information

- 13.1.3 Market Information

- 13.1.4 Background Information

- 13.1.5 Government Initiatives

- 13.1.6 Regulations

- 13.1.7 Regulatory Bodies

- 13.1.8 Major Associations

- 13.1.9 Taxes Levied

- 13.1.10 Corporate tax structure

- 13.1.11 Investments

- 13.1.12 Major Companies

- 13.2 Western Europe Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.3 Western Europe Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.4 Western Europe Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.5 Western Europe Generative AI In DevOps Market: Country Analysis

- 13.6 UK Market

- 13.7 UK Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.8 UK Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.9 UK Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.1 Germany Market

- 13.11 Germany Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.12 Germany Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.13 Germany Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.14 France Market

- 13.15 France Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.16 France Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.17 France Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.18 Italy Market

- 13.19 Italy Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.2 Italy Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.21 Italy Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.22 Spain Market

- 13.23 Spain Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.24 Spain Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 13.25 Spain Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

14 Eastern Europe Market

- 14.1 Summary

- 14.1.1 Market Overview

- 14.1.2 Region Information

- 14.1.3 Market Information

- 14.1.4 Background Information

- 14.1.5 Government Initiatives

- 14.1.6 Regulations

- 14.1.7 Regulatory Bodies

- 14.1.8 Major Associations

- 14.1.9 Taxes Levied

- 14.1.10 Corporate Tax Structure

- 14.1.11 Major companies

- 14.2 Eastern Europe Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 14.3 Eastern Europe Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 14.4 Eastern Europe Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 14.5 Eastern Europe Generative AI In DevOps Market: Country Analysis

- 14.6 Russia Market

- 14.7 Russia Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 14.8 Russia Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 14.9 Russia Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

15 North America Market

- 15.1 Summary

- 15.1.1 Market Overview

- 15.1.2 Region Information

- 15.1.3 Market Information

- 15.1.4 Background Information

- 15.1.5 Government Initiatives

- 15.1.6 Regulations

- 15.1.7 Regulatory Bodies

- 15.1.8 Major Associations

- 15.1.9 Taxes Levied

- 15.1.10 Corporate Tax Structure

- 15.1.11 Investments

- 15.1.12 Major Companies

- 15.2 North America Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 15.3 North America Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 15.4 North America Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 15.5 North America Generative AI In DevOps Market: Country Analysis

- 15.6 USA Market

- 15.7 Summary

- 15.7.1 Market Overview

- 15.7.2 Country Information

- 15.7.3 Market Information

- 15.7.4 Background Information

- 15.7.5 Government Initiatives

- 15.7.6 Regulations

- 15.7.7 Regulatory Bodies

- 15.7.8 Major Associations

- 15.7.9 Taxes Levied

- 15.7.10 Corporate Tax Structure

- 15.7.11 Investments

- 15.7.12 Major Companies

- 15.8 USA Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 15.9 USA Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 15.1 USA Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 15.11 Canada Market

- 15.12 Canada Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 15.13 Canada Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 15.14 Canada Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

16 South America Market

- 16.1 Summary

- 16.1.1 Market Overview

- 16.1.2 Region Information

- 16.1.3 Market Information

- 16.1.4 Background Information

- 16.1.5 Government Initiatives

- 16.1.6 Regulations

- 16.1.7 Regulatory Bodies

- 16.1.8 Major Associations

- 16.1.9 Taxes Levied

- 16.1.10 Corporate Tax Structure

- 16.1.11 Major Companies

- 16.2 South America Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 16.3 South America Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 16.4 South America Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 16.5 South America Generative AI In DevOps Market: Country Analysis

- 16.6 Brazil Market

- 16.7 Brazil Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 16.8 Brazil Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 16.9 Brazil Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

17 Middle East Market

- 17.1 Summary

- 17.1.1 Market Overview

- 17.1.2 Region Information

- 17.1.3 Market Information

- 17.1.4 Background Information

- 17.1.5 Government Initiatives

- 17.1.6 Regulations

- 17.1.7 Regulatory Bodies

- 17.1.8 Major Associations

- 17.1.9 Taxes Levied

- 17.1.10 Corporate Tax Structure

- 17.1.11 Investments

- 17.1.12 Major Companies

- 17.2 Middle East Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 17.3 Middle East Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 17.4 Middle East Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

18 Africa Market

- 18.1 Summary

- 18.1.1 Market Overview

- 18.1.2 Region Information

- 18.1.3 Market Information

- 18.1.4 Background Information

- 18.1.5 Government Initiatives

- 18.1.6 Regulations

- 18.1.7 Regulatory Bodies

- 18.1.8 Major Associations

- 18.1.9 Taxes Levied

- 18.1.10 Corporate Tax Structure

- 18.1.11 Major Companies

- 18.2 Africa Generative AI In DevOps Market, Segmentation By Component, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 18.3 Africa Generative AI In DevOps Market, Segmentation By Deployment Mode, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

- 18.4 Africa Generative AI In DevOps Market, Segmentation By Application, Historic And Forecast, 2019 - 2024, 2029F, 2034F, Value ($ Million)

19 Competitive Landscape And Company Profiles

- 19.1 Company Profiles

- 19.2 Microsoft Corporation

- 19.2.1 Company Overview

- 19.2.2 Products And Services

- 19.2.3 Business Strategy

- 19.2.4 Financial Overview

- 19.3 Alphabet Inc (Google LLC)

- 19.3.1 Company Overview

- 19.3.2 Products And Services

- 19.3.3 Business Strategy

- 19.3.4 Financial Overview

- 19.4 Amazon Web Services Inc

- 19.4.1 Company Overview

- 19.4.2 Products And Services

- 19.4.3 Business Strategy

- 19.4.4 Financial Overview

- 19.5 International Business Machines Corporation (IBM)

- 19.5.1 Company Overview

- 19.5.2 Products And Services

- 19.5.3 Business Strategy

- 19.5.4 Financial Overview

- 19.6 Oracle Corporation

- 19.6.1 Company Overview

- 19.6.2 Products And Services

- 19.6.3 Business Strategy

- 19.6.4 Financial Overview

20 Other Major And Innovative Companies

- 20.1 NVIDIA Corporation

- 20.1.1 Company Overview

- 20.1.2 Products and Services

- 20.2 Cisco Systems Inc

- 20.2.1 Company Overview

- 20.2.2 Products and Services

- 20.3 Capgemini SE

- 20.3.1 Company Overview

- 20.3.2 Products and Services

- 20.4 OpenAI

- 20.4.1 Company Overview

- 20.4.2 Products and Services

- 20.5 NetApp Inc

- 20.5.1 Company Overview

- 20.5.2 Products and Services

- 20.6 Dell Technologies Inc

- 20.6.1 Company Overview

- 20.6.2 Products and Services

- 20.7 Cognizant Technology Solutions Corporation

- 20.7.1 Company Overview

- 20.7.2 Products And Services

- 20.8 Intellias

- 20.8.1 Company Overview

- 20.8.2 Products And Services

- 20.9 CloudBees Inc

- 20.9.1 Company Overview

- 20.9.2 Products And Services

- 20.1 Wipro Limited

- 20.10.1 Company Overview

- 20.10.2 Products And Services

- 20.11 10Clouds

- 20.11.1 Company Overview

- 20.11.2 Products And Services

- 20.12 Yellow Systems

- 20.12.1 Company Overview

- 20.12.2 Products And Services

- 20.13 InData Labs

- 20.13.1 Company Overview

- 20.13.2 Products And Services

- 20.14 ThirdEye Data

- 20.14.1 Company Overview

- 20.14.2 Products And Services

- 20.15 SoluLab

- 20.15.1 Company Overview

- 20.15.2 Products And Services

21 Competitive Benchmarking

22 Competitive Dashboard

23 Key Mergers And Acquisitions

- 23.1 Nvidia Acquires OctoAI For $250 Million To Strengthen Enterprise AI And Generative AI Solutions

- 23.2 Jfrog Acquires Qwak For $230 Million To Enhance MlOps Capabilities And Strengthen AI-Driven DevOps Platform

- 23.3 Cisco Acquires Splunk For $28 Billion To Enhance AI-Driven Solutions In Security, IT Operations And Cloud Services

24 Opportunities And Strategies

- 24.1 Global Generative AI In DevOps Market In 2029 - Countries Offering Most New Opportunities

- 24.2 Global Generative AI In DevOps Market In 2029 - Segments Offering Most New Opportunities

- 24.3 Global Generative AI In DevOps Market In 2029 - Growth Strategies

- 24.3.1 Market Trend Based Strategies

- 24.3.2 Competitor Strategies

25 Generative AI In DevOps Market, Conclusions And Recommendations

- 25.1 Conclusions

- 25.2 Recommendations

- 25.2.1 Product

- 25.2.2 Place

- 25.2.3 Price

- 25.2.4 Promotion

- 25.2.5 People

26 Appendix

- 26.1 Geographies Covered

- 26.2 Market Data Sources

- 26.3 Research Methodology

- 26.4 Currencies

- 26.5 The Business Research Company

- 26.6 Copyright and Disclaimer