|

|

市場調査レポート

商品コード

1343613

二次電池用バインダー技術の開発状況と見通し<2023> Development Status and Outlook of Binder Technology for Secondary Batteries |

||||||

|

|

|||||||

|

|||||||

| 二次電池用バインダー技術の開発状況と見通し |

|

出版日: 2023年08月21日

発行: SNE Research

ページ情報: 英文 237 Pages

納期: お問合せ

|

- 全表示

- 概要

- 目次

リチウムイオン電池(LIB)は、その高いエネルギー密度と容量密度から、電気自動車やハイブリッド機器におけるエネルギー貯蔵需要の増大に対応するもっとも有望なエネルギー貯蔵デバイスの1つであり、二酸化炭素削減に向けたグリーンエネルギー活用への関心の高まりとともに、その利用が急速に拡大しています。

新しいエネルギー貯蔵デバイスと電気自動車の急速な開発の後、LIBの需要は安定して増加しており、電気自動車用電池の市場規模は2025年の1,960億米ドルから2030年に4,010億米ドルに達し、CAGRで21%の成長が予測されています。

LIBの特性は電極に大きく依存しており、優れた電池性能を達成するためには電極構造の最適化が最優先課題です。現在、負極と正極の活物質が、商業化されたLIBや研究において大きな関心をもって調査および検討されている一方で、電極の完全性を維持し、低い重量分率(≦5wt%)で電気化学プロセスを支える不活性なバインダーは、活物質や導電体とともに電極の性能において重要な位置を占めていますが、その重要性に比べてあまり注目されていません。

バインダーは電極のごく小さな部分ですが、電極の全体的な性能を決定する上で重要な役割を果たしています。バインダーは、負極活物質と正極活物質を集電体のそれぞれの極板に接着させ、耐久性を高める役割を担っています。バインダーは、(1)電解液中で電気化学的に安定であること(2)柔軟で不溶性であること(3)特に正極バインダーでは酸化による腐食に耐性があることが必須です。

したがって、活物質と導電体を集電体に効果的に接続し、充放電時の良好な電極構造を確保するための体積膨張に対応するためには、高い接着強度と弾性を有する機能性バインダーが必要となります。近年、バインダーのスクリーニングや設計に関する知見が深まるにつれ、研究の焦点は機械的安定化の観点から、構造的支持と同時に電気化学的な利点をもたらす多機能性へと移行しつつあります。

近年、シリコン正極材料の採用が進むにつれて、バインダーがリチウム化反応に大きな影響を及ぼし、電極容量とサイクル性の向上に役立つことが研究で示されたことから、新世代の研究が進行しています。従来のバインダーは、正極にフッ素樹脂のPVDF(ポリフッ化ビニリデン)、負極に合成ゴムのSBR(スチレンブタジエンゴム)やCMC(カルボキシルメチルセルロース)が主に使われますが、体積変化が大きいためシリコン負極には適さません。

正極材にはPTFE(ポリテトラフルオロエチレン)バインダーが使用されており、負極材にはPAA(ポリアクリル酸)やPI(ポリイミド)などの水系バインダーが注目されています。

PAAやPIなどのバインダーは水系バインダーであり、水系溶媒を電解質として用いるシリコン負極材料に使用されます。これらのバインダーは、従来のバインダーと比較して、引張強度が高く、密着性に優れ、シリコン負極材の体積膨張に強く、活物質を包んで安定したSEI(固体電解質界面)層を形成することができます。

正極材用次世代バインダーであるPTFEは、疎水性で耐薬品性・耐熱性に優れ、乾式電極プロセスや全固体電池での利用が予測されています。

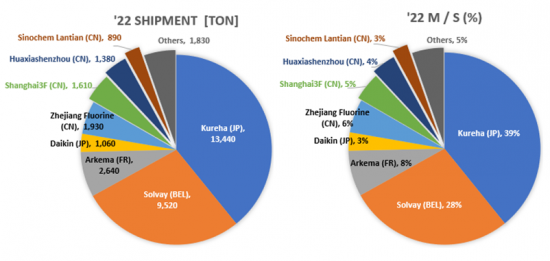

PVDFバインダーは日本のKureha、ベルギーのSolvay、フランスのArkema、SBRバインダーは日本のZeonが生産しており、いずれも海外生産比率の高い高価なものです。

正極バインダーは韓国のChemtrosが生産しており、負極バインダーは韓国のHansol Chemicalが現地化に成功し、Samsung SDIとSK Onに供給しているほか、LG Chem.とKumho Petrochemicalも正極バインダーを供給しています。

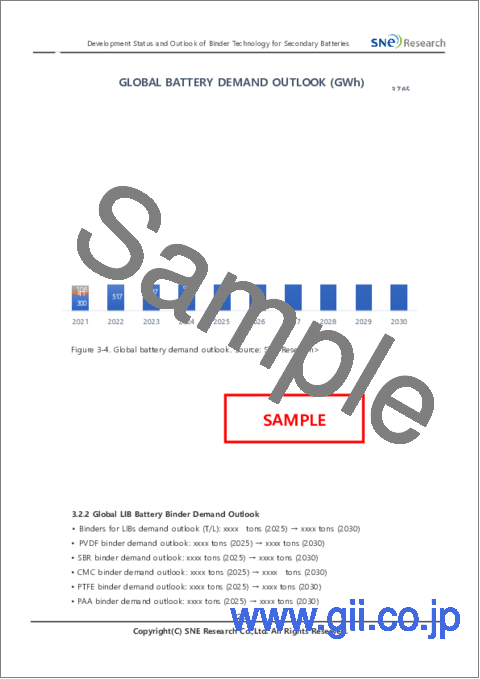

世界のリチウムイオン電池用バインダー需要は、2025年の8.9万トンから2030年に23.2万トンに増加し、2030年の金額は約4兆4,000億ウォンになると予測されています。

当レポートでは、世界の二次電池用バインダー市場について調査分析し、バインダーの概要、開発事例と設計や合成における注意事項、LIBのほかLi-S電池や全固体電池を含む次世代電池用バインダーの開発状況などの情報を提供しています。

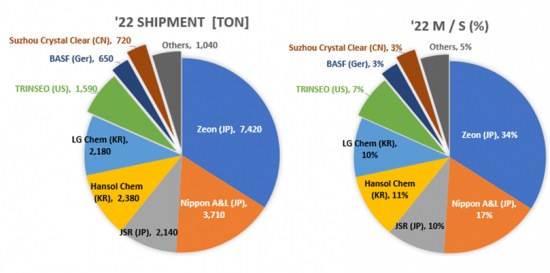

[PVDFバインダーメーカーの出荷台数・M/S]

[SBRバインダーメーカーの出荷台数・M/S]

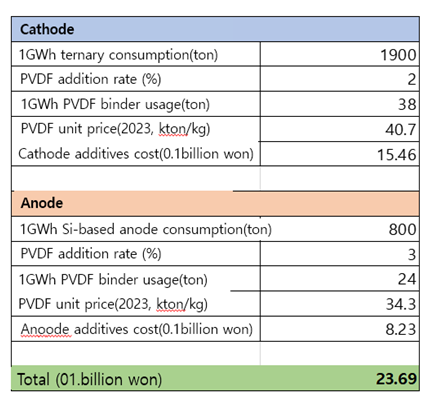

[Tesla向け4680セルのバインダーコスト分析]

- 正極:NCM811、負極:Siシリーズ

- 1GWhセルに対するPVDF正極バインダー消費とコスト約38トン、15億4,600万ウォン

- 1GWhセルに対する負極バインダー消費とコスト約24トン、8億2,300万ウォン

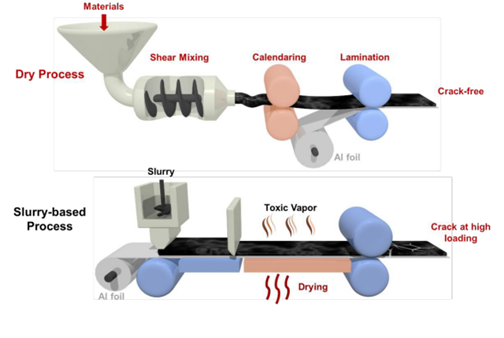

[電極製造に用いる乾式および湿式プロセスの概略図]

目次

第1章 バインダーの概要

- イントロダクション

- 定義、役割、要件

- 役割と特徴

- 要件

- カテゴリと種類

- 種類

- 動作の仕組み

第2章 バインダーの種類と研究開発の実践

- 正極用バインダー

- 非水系バインダー

- PVDF正極用バインダー産業の状況

- (CMC+SBR)正極用バインダー産業の状況

- 水系バインダー

- その他のバインダー

- 陽極用バインダー

- 挿入可能な陽極用バインダー

- 合金陽極用バインダー

- 次世代電池用バインダー(1)

- リチウム硫黄(Li-S)電池用バインダー

- 乾式プロセス用バインダー

- 次世代電池用バインダー(2)

- 固体電解質用バインダー

第3章 バインダー市場

- バインダー市場の全体の見通し

- 世界のLIB向けPVDF市場の見通し

- 世界の電池市場の需要

- 世界のLIB電池用バインダーの需要の見通し

- LIB電池用バインダーの価格の見通し

- LIB電池用バインダーの市場規模の見通し

- 世界のLFP電池需要と正極材料需要の見通し

- LFP電池用PTFEの価格と市場見通し

- LFP電池用PTFEバインダーの使用

- シリコンベース正極用バインダーの市場見通し

- シリコンベース負極材料市場の見通し

- シリコン負極向けPAAバインダー市場の見通し

- Tesla向け4680電池に対するバインダーコストの分析

- PVDFバインダーメーカーの出荷台数とM/S

- SBRバインダーメーカーの出荷台数とM/S

- CMCバインダーメーカーの出荷台数とM/S

第4章 バインダーメーカーの状況

- [1] Arkema

- [2] BASF SE

- [3] Solvay

- [4] Kureha

- [5] ZEON

- [6] JSR

- [7] Fujian Blue Ocean Black Stone

- [8] Dupont

- [9] Ashland Inc

- [10] MTI Corp.

- [11] TRINSEO

- [12] Xinxiang Jinbang Power Technology

- [13] Lihong Fine Chemical

- [14] Chemtros

- [15] Hansol Chemical

- [16] Kumho Petrochemical

- [17] Daikin Industry

- [18] Nanografi Nano Technology

- [19] Nippon Paper Group

- [20] APV Engineered Coatings LLC

- [21] Sichuan Indigo Materials Science & Technology

- [22] Guangzhou Songbai Chemical Co

- [23] Nippon A&L Inc

- [24] Daicel Miraizu Ltd

- [25] Sinochem Group Co

- [26] Ube Corp.

- [27] AOT Battery Equipment Technology

- [28] Shanghai 3F New Materials

- [29] GL Chem

第5章 付録(参考)

第6章 参考材料

Lithium-ion batteries (LIBs) are one of the most promising energy storage devices to address the growing demand for energy storage in electric vehicles and hybrid devices due to their high energy and power density, and their use is increasing rapidly with the growing interest in utilizing green energy for carbon reduction.

According to SNE Research, after the rapid development of new energy storage devices and electric vehicles, the demand for LIBs has been steadily increasing, and the electric vehicle battery market size is expected to grow from $196B in '25 to $401B in '30, with a CAGR of 21%.

The characteristics of LIBs are highly dependent on the electrodes, and optimizing the electrode structure is a top priority to achieve superior battery performance. While the active materials of the anode and cathode are currently being studied and examined with great interest in commercialized LIBs as well as in research, the inactive binder, which maintains the integrity of the electrode and supports the electrochemical process at a low weight fraction (≤5wt%), occupies a critical position in the performance of the electrode along with the active materials and conductors, but has received less attention compared to its importance.

Although binders are a very small part of the electrode, they play a critical role in determining the overall performance of the electrode. The binder is responsible for the adhesion of the anode and cathode active materials to the respective pole plates of the collector and for their durability. The binder must be (1) electrochemically stable in the electrolyte, (2) flexible and insoluble, and (3) resistant to corrosion by oxidation, especially for cathode binders.

Therefore, a functional binder with high bond strength and elasticity is required to effectively connect the active material and the conductor to the collector and accommodate volume expansion to ensure good electrode structure during charge and discharge. Recently, with more insights into binder screening and design, the focus of research is shifting from a mechanical stabilization perspective to multifunctionality that provides electrochemical benefits as well as structural support.

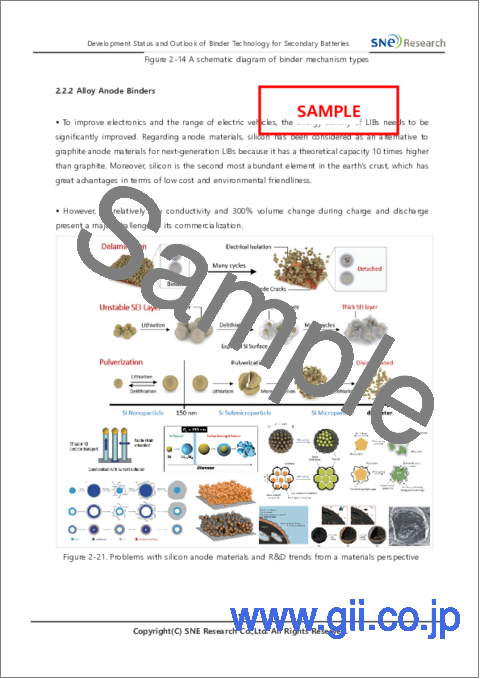

Recently, with the increasing adoption of silicon cathode materials, a new generation of research is underway, as studies have shown that binders have a significant impact on the lithiation reaction, helping to improve electrode capacity and cycleability. Conventional binders mainly use PVDF (PolyVinyliDeneFluoride), a fluoroplastic, for the cathode and SBR (Styrene-Butadiene-Rubber) and CMC (Carboxyl Methyl Cellulose) binders, a synthetic rubber, for the anode, but they are not suitable for use in silicon anodes due to large volume changes.

PTFE (PolyTetraFluoroEthylene) binders have been used for cathode materials, and water-based binders such as PAA (PolyAcrylicAcid) and PI (PolyImide) have been attracting attention for anode materials.

Binders such as PAA and PI are water-based binders, which are used in silicon anode materials that use water-based solvents as electrolytes. Compared to conventional binders, these binders have high tensile strength, high adhesion, and are resistant to volume expansion of silicon anode materials and form a stable SEI (Solid Electrolyte Interphase) layer by wrapping the active material.

PTFE, a next-generation binder for cathode materials, is a hydrophobic material with excellent chemical and heat resistance and is expected to gain attention in dry electrode processes and all-solid-state batteries.

PVDF binders are produced by Kureha in Japan, Solvay in Belgium, and Arkema in France, and SBR binders are produced by Zeon in Japan, all of which are expensive items with a high proportion of foreign production.

The cathode binder is produced by Korea's Chemtros, and for the anode binder, Korea's Hansol Chemical has successfully localized it and is supplying it to Samsung SDI and SK On, while LG Chem. and Kumho Petrochemical are also supplying cathode binders.

Meanwhile, SNE Research's global demand forecast for binders for lithium-ion batteries is expected to increase from 89,000 tons in 2025 to 232,000 tons in 2030, with a value of about KRW 4.4 trillion in 2030.

High-energy-density batteries are expected to place higher requirements on high-performance binders, and from this perspective, binder design should consider the following.

- (1) The binder content should be less than or equal to 3 wt% of the total electrode mass without losing mechanical strength and adhesion.

- (2) Simplification of synthesis using water-based and dry-based polymers from the perspective of low cost and sustainability.

- (3) Multifunctional polymer binders that can integrate all necessary functions into one polymer.

- (4) Deep insights into polymer dispersion and degradation mechanisms, and more.

In this report, SNE has summarized in detail the information available in the literature on the design, synthesis, and application of binders for lithium-ion battery electrodes and forecasted the demand and market for binders based on our forecasts for lithium-ion batteries, and quoted market size and forecasts from external research organizations in the appendix to help readers understand the overall scale.

Finally, by summarizing the status of binder manufacturers and their main products, we hope to provide a holistic insight for researchers and interested parties in this field, which will help to improve the performance of batteries, including their energy density, fast charging capability, and long-term life characteristics.

Strong points of this report:

- (1) Provides a general overview of the binder and contains rich technical content

- (2) Includes key points to consider in design and synthesis through examples of binder development.

- (3) Summarizes the development status and case analysis of binders not only for LIBs but also for next-generation batteries such as Li-S and all-solid-state batteries.

- (4) Provides objective figures on the binder market through objective binder market forecasts based on SNE Research's battery forecasts.

- (5) Detailed information on the development status and product status of major binder companies.

[Shipments and M/S of PVDF binder manufacturers]

[Shipments and M/S of SBR binder manufacturers]

[Binder cost analysis for 4680 cells for Tesla]

- Cathode: NCM811, Anode: Si series

- PVDF cathode binder consumption and cost for a 1 GWh cell: Approx. 38 tons, KRW 1.546 billion

- PAA anode binder consumption and cost for a 1 GWh cell: Approx. 24 tons, KRW 0.823 billion

[A schematic of the dry and wet processes for electrode fabrication]

Table of Contents

1. Binder Overview

- 1.1. Introduction

- 1.2. Definition, Role, and Requirements

- 1.2.1. Role and Features

- 1.2.2. Requirements

- 1.3. Categories and Types

- 1.3.1. Types

- 1.4. Operation Mechanism

2. Types of binders and R&D practices

- 2.1. Binders for Cathodes

- 2.1.1. Non-Aqueous Binders

- 2.1.2. Industry Status of PVDF Cathode Binders

- 2.1.3. (CMC+SBR) Industry Status of Anode Binders

- 2.1.4. Water-based Binders

- 2.1.5. Other binders

- 2.2. Binders for Anodes

- 2.2.1. Insertable Anode Binder

- 2.2.1.1. Binders for Graphite Electrodes

- 2.2.1.2. Anode Binder for LTO

- 2.2.2. Alloy Anode Binders

- 2.2.2.1. Linear Polymer Binders

- 2.2.2.2. Crosslinked Polymer Binders

- 2.2.2.3. Branched and Extra-Large Polymer Binders

- 2.2.2.4. Conductive Polymer Binders

- 2.2.1. Insertable Anode Binder

- 2.3. Binder for Next-Generation Batteries (1)

- 2.3.1. Binders for Lithium-Sulfur (Li-S) Batteries

- 2.3.2. Binders for Dry Process

- 2.4. Binder for Next-Generation Batteries (2)

- 2.4.1. Binders for Solid Electrolytes

- 2.4.1.1. Overview of All-Solid-State Batteries

- 2.4.1.2. Sulfide-based All-Solid-State Battery Technology

- 2.4.1.3. Manufacturing of All-Solid-State Cells and the Purpose of Binders

- 2.4.1.4. Binder Technology for Cathodes

- 2.4.1.4.1. Binder Technology for Wet Processes

- 2.4.1.4.2. Binder Technology for Dry Processes

- 2.4.1.5. Binder Technology for Electrolyte Layers

- 2.4.1.6. Binder Technology for Anodes

- 2.4.1.6.1. Binder Technology for Graphite-Based Anodes

- 2.4.1.6.2. Next Generation Binder Technology for Anodes

- 2.4.1. Binders for Solid Electrolytes

3. Binder Market

- 3.1. Overall Outlook for the Binders Market

- 3.2. PVDF Market Outlook for Global LIBs

- 3.2.1. Global Battery Market Demand

- 3.2.2. Global LIB Battery Binder Demand Outlook

- 3.2.3. LIB Battery Binder Price Outlook

- 3.2.4. LIB Battery Binder Market Size Outlook

- 3.2.5. Global LFP Battery Demand and Cathode Material Demand Outlook

- 3.2.6. PTFE for LFP Batteries Price and Market Outlook

- 3.2.7. PTFE Binder Usage for LFP Batteries

- 3.2.8. Market Outlook for Binders for Silicon-based Cathodes

- 3.2.9. Silicon-based Anode Material Market Outlook

- 3.2.10. PAA Binders for Silicon Anode Market Outlook

- 3.2.11. Binder cost analysis for 4680 batteries for Tesla

- 3.2.12. Shipments and M/S of PVDF Binder Manufacturers

- 3.2.13. Shipments and M/S of SBR Binder Manufacturers

- 3.2.14. Shipments and M/S of CMC Binder Manufacturers

4. Binder Manufacturer Status

- [1] Arkema

- [2] BASF SE

- [3] Solvay

- [4] Kureha

- [5] ZEON

- [6] JSR

- [7] Fujian Blue Ocean Black Stone

- [8] Dupont

- [9] Ashland Inc

- [10] MTI Corp.

- [11] TRINSEO

- [12] Xinxiang Jinbang Power Technology

- [13] Lihong Fine Chemical

- [14] Chemtros

- [15] Hansol Chemical

- [16] Kumho Petrochemical

- [17] Daikin Industry

- [18] Nanografi Nano Technology

- [19] Nippon Paper Group

- [20] APV Engineered Coatings LLC

- [21] Sichuan Indigo Materials Science & Technology

- [22] Guangzhou Songbai Chemical Co

- [23] Nippon A&L Inc

- [24] Daicel Miraizu Ltd

- [25] Sinochem Group Co

- [26] Ube Corp.

- [27] AOT Battery Equipment Technology

- [28] Shanghai 3F New Materials

- [29] GL Chem