|

|

市場調査レポート

商品コード

1803136

EV用バッテリー交換の世界市場:将来予測 (2032年まで) - バッテリーの種類別・車種別・ステーションの種類別・バッテリー容量別・サービスモデル別・エンドユーザー別・地域別の分析EV Battery Swapping Market Forecasts to 2032 - Global Analysis By Battery Type (Lithium-Ion, Lead-Acid and Emerging Technologies), Vehicle Type, Station Type, Battery Capacity, Service Model, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| EV用バッテリー交換の世界市場:将来予測 (2032年まで) - バッテリーの種類別・車種別・ステーションの種類別・バッテリー容量別・サービスモデル別・エンドユーザー別・地域別の分析 |

|

出版日: 2025年09月07日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界のEV用バッテリー交換市場は2025年に31億米ドルを占め、2032年には149億米ドルに達すると予測されています。

EV用バッテリー交換とは、バッテリーが消耗した電気自動車(EV)用バッテリーを、再充電を待つのではなく、指定された交換ステーションで満充電のものと素早く交換するプロセスです。この方法によってダウンタイムが短縮され、車両の継続的な運転が可能になり、EVに関連する航続距離不安にも対処できます。交換ステーションは多くの場合、利便性を考慮して戦略的に配置され、個人と商用フリート両方の使用をサポートします。この方法はまた、バッテリーの集中管理を可能にし、バッテリーの寿命、安全性、性能監視を向上させます。バッテリーの所有権を車両から切り離すことで、初期費用を抑え、電気モビリティの全体的な導入と効率を高めることができます。

充電時間の短縮と利便性の向上

バッテリー交換の効率化は、個人消費者だけでなく、商用フリートオペレーターをも魅了し、EVの全体的な普及を後押しします。戦略的な場所に交換ステーションがあることで、利便性が向上し、長距離移動がより現実的になります。航続距離への不安が軽減されることで、より多くのドライバーが従来型自動車から移行する動機付けとなります。プロセスが迅速化することで、電気自動車を運行する企業のダウンタイムが最小化され、業務パフォーマンスが最適化されます。これらの利点が相まって、EV用バッテリー交換市場の成長と拡大に寄与しています。

バッテリー標準化の欠如

EVメーカーごとにバッテリーのサイズ、形状、化学物質が異なるため、普遍的な交換ステーションの導入は困難です。このような断片化は、ステーションが複数のバッテリータイプに対応しなければならないため、インフラコストを増加させます。また、ドライバーが互換性のある交換ポイントを見つけられない可能性があるため、消費者の普及も制限されます。さらに、多様なバッテリーの在庫管理は、ロジスティクスと業務効率を複雑にします。全体として、標準化がなければ、バッテリー交換の拡張性と利便性は制限されたままです。

都市車両の電動化と共有モビリティ

排出量を削減し、大気環境を改善するため、都市では電気バス、タクシー、配送車両の導入が進んでいます。これらの車両は高速で効率的なバッテリー・ソリューションを必要とするため、交換ステーションは長い充電時間に代わる魅力的な選択肢となっています。eスクーターやライドヘイリングEVのような共有モビリティサービスは、迅速なバッテリー交換による継続的な車両利用可能性から利益を得ています。拡張性と信頼性の高い交換インフラに対する需要は、都市モビリティの激化に伴って高まっています。全体として、車両電化と共有モビリティは、迅速で便利、かつ費用対効果の高いバッテリー交換ソリューションに対する継続的なニーズを生み出しています。

バッテリーの劣化とライフサイクル管理

頻繁な交換は消耗を早め、バッテリー全体の寿命を縮め、交換コストを増加させます。メーカーは、使用履歴の異なるバッテリーを標準化する難しさに直面しています。消費者は、交換されたバッテリーの一貫性のない性能によって信頼を失う可能性があります。複数のバッテリーの健康状態データを管理するには、複雑な監視システムが必要です。これらの要因が相まって、市場導入が遅れ、交換インフラの大規模展開が制限されます。

COVID-19の影響:

COVID-19の大流行は、サプライチェーンの中断、工場の操業停止、インフラ整備の遅れを引き起こし、EV用バッテリー交換市場を大きく混乱させました。移動が制限されたことで、電気自動車の需要が減少し、特に都市部では交換ソリューションの導入が遅れました。しかし、この危機はまた、輸送における効率的で、非接触で、時間を節約できるソリューションの必要性を浮き彫りにし、フリートや配送サービス向けのバッテリー交換への関心を押し上げました。パンデミック後の復興は、この市場の回復力を強化するための新たな投資、政府支援、技術革新を促進しています。

予測期間中、二輪車セグメントが最大になる見込み

二輪車セグメントは、都市部での電動スクーターや二輪車の採用率が高いことから、予測期間中に最大の市場シェアを占めると予想されます。短距離の通勤が頻繁に行われるため、長い充電時間に比べてバッテリー交換が便利なソリューションとなっています。電動二輪車に対する政府の奨励金や補助金の増加が市場の需要を押し上げます。二輪車のバッテリーサイズがコンパクトなため、交換インフラの展開がより迅速でコスト効率が高いです。持続可能なモビリティに対する意識の高まりが二輪車の普及をさらに加速させ、バッテリー交換エコシステムを推進しています。

予測期間中、自動化ステーション分野のCAGRが最も高くなる見込み

予測期間中、自動化ステーション・セグメントは、運用効率の向上と人的ミスの最小化により、最も高い成長率を記録すると予測されます。これらのステーションは、より迅速なバッテリー交換を可能にし、EVユーザーの利便性を高め、車両のダウンタイムを短縮します。高度なロボット工学とAIの統合により、バッテリーの取り扱いと在庫管理が最適化され、サービス全体の信頼性が向上します。自動化されたシステムは拡張性をサポートするため、事業者はネットワークの適用範囲を迅速に拡大し、EV普及率の上昇に対応することができます。さらに、長期的な運用コストを削減し、フリート事業者や個人消費者にとって、バッテリー交換がより経済的に魅力的なソリューションとなります。

最大のシェアを占める地域:

予測期間中、急速な都市化、政府のインセンティブ、クリーンモビリティ重視の高まりにより、アジア太平洋が最大の市場シェアを占めると予想されます。中国やインドなどの主要国では、自動車メーカーとテクノロジー・プロバイダーのコラボレーションに支えられ、バッテリー交換ネットワークの開拓が進んでいます。高度なインフラ、EVの高い普及率、スマートシティ構想との統合が展開を加速しています。新たな動向としては、AIベースのバッテリー管理、サブスクリプション・モデル、相互運用性標準などが挙げられます。課題としては、標準化やグリッド管理などが挙げられますが、消費者の意識の高まりや持続可能な輸送の目標が引き続きこの地域の成長を後押ししています。

CAGRが最も高い地域:

予測期間中、中東・アフリカ地域は、再生可能エネルギー投資と都市電化イニシアチブの拡大により、最も高いCAGRを示すと予想されます。民間部門と公的部門が協力して、主要都市に試験的な交換ネットワークを構築しています。厳しい気候と長距離移動の要件が、弾力性のあるバッテリーソリューションの設計と展開を形作っています。政府の規制や持続可能性目標が、特にバスやタクシーの車両電化を後押ししています。市場の成長は、信頼性が高く、迅速で費用対効果の高いバッテリー交換システムの実現を目指した戦略的パートナーシップ、技術移転、インフラ開拓によって支えられています。

無料のカスタマイズサービス

当レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加企業の包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域区分

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序論

- 概要

- ステークホルダー

- 分析範囲

- 分析手法

- データマイニング

- データ分析

- データ検証

- 分析アプローチ

- 分析資料

- 一次調査資料

- 二次調査情報源

- 前提条件

第3章 市場動向の分析

- 促進要因

- 抑制要因

- 市場機会

- 脅威

- エンドユーザー分析

- 新興市場

- 新型コロナウイルス感染症 (COVID-19) の影響

第4章 ポーターのファイブフォース分析

- サプライヤーの交渉力

- バイヤーの交渉力

- 代替製品の脅威

- 新規参入企業の脅威

- 企業間競争

第5章 世界のEV用バッテリー交換市場:バッテリーの種類別

- リチウムイオン

- 鉛蓄電池

- 新興技術

第6章 世界のEV用バッテリー交換市場:車種別

- 二輪車

- 三輪車

- 乗用車

- 商用車

- その他の車種

第7章 世界のEV用バッテリー交換市場:ステーションの種類別

- 手動交換ステーション

- 自動交換ステーション

- モバイル交換ユニット

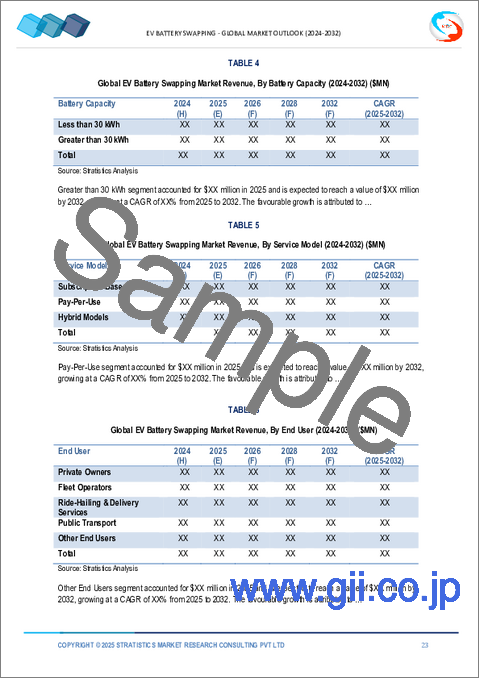

第8章 世界のEV用バッテリー交換市場:バッテリー容量別

- 30kWh未満

- 30kWh以上

第9章 世界のEV用バッテリー交換市場:サービスモデル別

- サブスクリプションベース

- 従量課金制

- ハイブリッドモデル

第10章 世界のEV用バッテリー交換市場:エンドユーザー別

- 個人所有者

- フリートオペレーター

- 配車・配達サービス

- 公共交通機関

- その他のエンドユーザー

第11章 世界のEV用バッテリー交換市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東・アフリカ

第12章 主な動向

- 契約、事業提携・協力、合弁事業

- 企業合併・買収 (M&A)

- 新製品の発売

- 事業拡張

- その他の主要戦略

第13章 企業プロファイリング

- NIO

- Gogoro

- Ample

- Aulton

- CATL

- SUN Mobility

- Battery Smart

- Voltia

- EM3ev

- TYCORUN

- China Tower

- Scin Power

- Tiger New Energy

- Ampersand

- Terra

- KYMCO

- Selex Motors

- EHuanDian

List of Tables

- Table 1 Global EV Battery Swapping Market Outlook, By Region (2024-2032) ($MN)

- Table 2 Global EV Battery Swapping Market Outlook, By Battery Type (2024-2032) ($MN)

- Table 3 Global EV Battery Swapping Market Outlook, By Lithium-Ion (2024-2032) ($MN)

- Table 4 Global EV Battery Swapping Market Outlook, By Lead-Acid (2024-2032) ($MN)

- Table 5 Global EV Battery Swapping Market Outlook, By Emerging Technologies (2024-2032) ($MN)

- Table 6 Global EV Battery Swapping Market Outlook, By Vehicle Type (2024-2032) ($MN)

- Table 7 Global EV Battery Swapping Market Outlook, By Two-Wheelers (2024-2032) ($MN)

- Table 8 Global EV Battery Swapping Market Outlook, By Three-Wheelers (2024-2032) ($MN)

- Table 9 Global EV Battery Swapping Market Outlook, By Passenger Cars (2024-2032) ($MN)

- Table 10 Global EV Battery Swapping Market Outlook, By Commercial Vehicles (2024-2032) ($MN)

- Table 11 Global EV Battery Swapping Market Outlook, By Other Vehicle Types (2024-2032) ($MN)

- Table 12 Global EV Battery Swapping Market Outlook, By Station Type (2024-2032) ($MN)

- Table 13 Global EV Battery Swapping Market Outlook, By Manual Swapping Stations (2024-2032) ($MN)

- Table 14 Global EV Battery Swapping Market Outlook, By Automated Swapping Stations (2024-2032) ($MN)

- Table 15 Global EV Battery Swapping Market Outlook, By Mobile Swapping Units (2024-2032) ($MN)

- Table 16 Global EV Battery Swapping Market Outlook, By Battery Capacity (2024-2032) ($MN)

- Table 17 Global EV Battery Swapping Market Outlook, By Less than 30 kWh (2024-2032) ($MN)

- Table 18 Global EV Battery Swapping Market Outlook, By Greater than 30 kWh (2024-2032) ($MN)

- Table 19 Global EV Battery Swapping Market Outlook, By Service Model (2024-2032) ($MN)

- Table 20 Global EV Battery Swapping Market Outlook, By Subscription-Based (2024-2032) ($MN)

- Table 21 Global EV Battery Swapping Market Outlook, By Pay-Per-Use (2024-2032) ($MN)

- Table 22 Global EV Battery Swapping Market Outlook, By Hybrid Models (2024-2032) ($MN)

- Table 23 Global EV Battery Swapping Market Outlook, By End User (2024-2032) ($MN)

- Table 24 Global EV Battery Swapping Market Outlook, By Private Owners (2024-2032) ($MN)

- Table 25 Global EV Battery Swapping Market Outlook, By Fleet Operators (2024-2032) ($MN)

- Table 26 Global EV Battery Swapping Market Outlook, By Ride-Hailing & Delivery Services (2024-2032) ($MN)

- Table 27 Global EV Battery Swapping Market Outlook, By Public Transport (2024-2032) ($MN)

- Table 28 Global EV Battery Swapping Market Outlook, By Other End Users (2024-2032) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global EV Battery Swapping Market is accounted for $3.1 billion in 2025 and is expected to reach $14.9 billion by 2032 growing at a CAGR of 25% during the forecast period. EV battery swapping is a process in which a depleted electric vehicle (EV) battery is quickly exchanged for a fully charged one at a designated swapping station, rather than waiting to recharge the battery. This approach reduces downtime, enabling continuous vehicle operation and addressing range anxiety associated with EVs. Swapping stations are often strategically located for convenience, supporting both individual and commercial fleet usage. The method also allows for centralized battery management, improving battery life, safety, and performance monitoring. By decoupling battery ownership from the vehicle, it can lower upfront costs and enhance the overall adoption and efficiency of electric mobility.

Market Dynamics:

Driver:

Reduced charging time and enhanced convenience

Efficiency in battery swapping attracts individual consumers as well as commercial fleet operators, boosting overall EV adoption. Availability of swapping stations in strategic locations enhances convenience, making long-distance travel more practical. Reduced range anxiety motivates more drivers to shift from conventional vehicles. The faster process minimizes downtime for businesses operating electric fleets, optimizing operational performance. Combined, these advantages contribute to the growth and expansion of the EV battery swapping market.

Restraint:

Lack of battery standardization

Different EV manufacturers use varied battery sizes, shapes, and chemistries, making universal swapping stations difficult to implement. This fragmentation increases infrastructure costs as stations must accommodate multiple battery types. It also limits consumer adoption since drivers may not find compatible swapping points. Additionally, managing inventory for diverse batteries complicates logistics and operational efficiency. Overall, without standardization, the scalability and convenience of battery swapping remain restricted.

Opportunity:

Urban fleet electrification and shared mobility

Cities are increasingly adopting electric buses, taxis, and delivery fleets to reduce emissions and improve air quality. These fleets require fast and efficient battery solutions, making swapping stations an attractive alternative to long charging times. Shared mobility services, such as e-scooters and ride-hailing EVs, benefit from continuous vehicle availability through quick battery swaps. The demand for scalable and reliable swapping infrastructure grows as urban mobility intensifies. Overall, fleet electrification and shared mobility create a recurring need for fast, convenient, and cost-effective battery swapping solutions.

Threat:

Battery degradation and lifecycle management

Frequent swapping accelerates wear, reducing overall battery lifespan and increasing replacement costs. Manufacturers face difficulty in standardizing batteries with varying usage histories. Consumers may lose confidence due to inconsistent performance of swapped batteries. Managing state-of-health data across multiple batteries requires complex monitoring systems. These factors collectively slow market adoption and limit large-scale deployment of swapping infrastructure.

Covid-19 Impact:

The Covid-19 pandemic significantly disrupted the EV battery swapping market by causing supply chain interruptions, factory shutdowns, and delays in infrastructure development. Restrictions on mobility reduced demand for electric vehicles and slowed adoption of swapping solutions, particularly in urban areas. However, the crisis also highlighted the need for efficient, contactless, and time-saving solutions in transportation, pushing interest in battery swapping for fleet and delivery services. Post-pandemic recovery is fostering renewed investment, government support, and technological innovation to strengthen resilience in this market.

The two-wheelers segment is expected to be the largest during the forecast period

The two-wheelers segment is expected to account for the largest market share during the forecast period due to the high adoption of electric scooters and motorcycles in urban areas. Frequent short-distance commutes make battery swapping a convenient solution compared to long charging times. Rising government incentives and subsidies for electric two-wheelers boost market demand. Compact battery sizes in two-wheelers allow faster and more cost-effective swapping infrastructure deployment. Increased awareness of sustainable mobility further accelerates two-wheeler adoption, propelling the battery swapping ecosystem.

The automated stations segment is expected to have the highest CAGR during the forecast period

Over the forecast period, the automated stations segment is predicted to witness the highest growth rate due to increased operational efficiency, and minimizing human error. These stations enable faster battery replacement, enhancing convenience for EV users and reducing vehicle downtime. Integration of advanced robotics and AI optimizes battery handling and inventory management, improving overall service reliability. Automated systems support scalability, allowing operators to expand network coverage quickly and meet rising EV adoption. Additionally, they lower long-term operational costs, making battery swapping a more economically attractive solution for fleet operators and individual consumers.

Region with largest share:

During the forecast period, the Asia-Pacific region is expected to hold the largest market share by rapid urbanization, government incentives, and a growing emphasis on clean mobility. Key countries like China and India are pioneering battery swapping networks, supported by collaborations between automakers and technology providers. Advanced infrastructure, high EV adoption, and integration with smart city initiatives accelerate deployment. Emerging trends include AI-based battery management, subscription models, and interoperability standards. Challenges include standardization and grid management, but increasing consumer awareness and sustainable transport goals continue to propel growth across the region.

Region with highest CAGR:

Over the forecast period, the Middle East & Africa region is anticipated to exhibit the highest CAGR by growing renewable energy investments and urban electrification initiatives. Private and public sectors are collaborating to establish pilot swapping networks in major cities. Harsh climates and long-distance travel requirements shape the design and deployment of resilient battery solutions. Government regulations and sustainability targets are encouraging fleet electrification, especially for buses and taxis. Market growth is supported by strategic partnerships, technology transfer, and infrastructure development aimed at enabling reliable, fast, and cost-effective battery exchange systems.

Key players in the market

Some of the key players in EV Battery Swapping Market include NIO, Gogoro, Ample, Aulton, CATL, SUN Mobility, Battery Smart, Voltia, EM3ev, TYCORUN, China Tower, Scin Power, Tiger New Energy, Ampersand, Terra, KYMCO, Selex Motors and EHuanDian.

Key Developments:

In March 2025, Ample partnered with MMC and MFTBC to deploy modular battery-swapping stations across Tokyo, targeting commercial fleet electrification. Supported by Tokyo's environmental agency, the initiative enhances urban sustainability, reduces emissions, and accelerates clean mobility infrastructure development.

In October 2024, NIO MENA, launched with CYVN Holdings, aims to expand battery-swapping and autonomous tech across MENA. It includes an Abu Dhabi R&D hub and joint ventures with Egyptian firms to establish localized EV production and smart mobility infrastructure.

In June 2024, SUN Mobility and IndianOil launched a 50:50 joint venture to build 10,000 battery swap stations across 40+ Indian cities within three years, focusing on 2W, 3W, and small 4W EVs using SUN's BaaS platform.

Battery Types Covered:

- Lithium-Ion

- Lead-Acid

- Emerging Technologies

Vehicle Types Covered:

- Two-Wheelers

- Three-Wheelers

- Passenger Cars

- Commercial Vehicles

- Other Vehicle Types

Station Types Covered:

- Manual Swapping Stations

- Automated Swapping Stations

- Mobile Swapping Units

Battery Capacities Covered:

- Less than 30 kWh

- Greater than 30 kWh

Service Models Covered:

- Subscription-Based

- Pay-Per-Use

- Hybrid Models

End Users Covered:

- Private Owners

- Fleet Operators

- Ride-Hailing & Delivery Services

- Public Transport

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2024, 2025, 2026, 2028, and 2032

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 End User Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global EV Battery Swapping Market, By Battery Type

- 5.1 Introduction

- 5.2 Lithium-Ion

- 5.3 Lead-Acid

- 5.4 Emerging Technologies

6 Global EV Battery Swapping Market, By Vehicle Type

- 6.1 Introduction

- 6.2 Two-Wheelers

- 6.3 Three-Wheelers

- 6.4 Passenger Cars

- 6.5 Commercial Vehicles

- 6.6 Other Vehicle Types

7 Global EV Battery Swapping Market, By Station Type

- 7.1 Introduction

- 7.2 Manual Swapping Stations

- 7.3 Automated Swapping Stations

- 7.4 Mobile Swapping Units

8 Global EV Battery Swapping Market, By Battery Capacity

- 8.1 Introduction

- 8.2 Less than 30 kWh

- 8.3 Greater than 30 kWh

9 Global EV Battery Swapping Market, By Service Model

- 9.1 Introduction

- 9.2 Subscription-Based

- 9.3 Pay-Per-Use

- 9.4 Hybrid Models

10 Global EV Battery Swapping Market, By End User

- 10.1 Introduction

- 10.2 Private Owners

- 10.3 Fleet Operators

- 10.4 Ride-Hailing & Delivery Services

- 10.5 Public Transport

- 10.6 Other End Users

11 Global EV Battery Swapping Market, By Geography

- 11.1 Introduction

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.2.3 Mexico

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 Italy

- 11.3.4 France

- 11.3.5 Spain

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 Japan

- 11.4.2 China

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 New Zealand

- 11.4.6 South Korea

- 11.4.7 Rest of Asia Pacific

- 11.5 South America

- 11.5.1 Argentina

- 11.5.2 Brazil

- 11.5.3 Chile

- 11.5.4 Rest of South America

- 11.6 Middle East & Africa

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 Qatar

- 11.6.4 South Africa

- 11.6.5 Rest of Middle East & Africa

12 Key Developments

- 12.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 12.2 Acquisitions & Mergers

- 12.3 New Product Launch

- 12.4 Expansions

- 12.5 Other Key Strategies

13 Company Profiling

- 13.1 NIO

- 13.2 Gogoro

- 13.3 Ample

- 13.4 Aulton

- 13.5 CATL

- 13.6 SUN Mobility

- 13.7 Battery Smart

- 13.8 Voltia

- 13.9 EM3ev

- 13.10 TYCORUN

- 13.11 China Tower

- 13.12 Scin Power

- 13.13 Tiger New Energy

- 13.14 Ampersand

- 13.15 Terra

- 13.16 KYMCO

- 13.17 Selex Motors

- 13.18 EHuanDian