|

|

市場調査レポート

商品コード

1636773

変電所オートメーションおよび統合市場の2030年までの予測: コンポーネント別、通信プロトコル別、技術別、用途別、エンドユーザー別、地域別の世界分析Power Substation Automation & Integration Market Forecasts to 2030 - Global Analysis By Component (Hardware, Software, Services and Other Components), Communication Protocol, Technology, Application, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 変電所オートメーションおよび統合市場の2030年までの予測: コンポーネント別、通信プロトコル別、技術別、用途別、エンドユーザー別、地域別の世界分析 |

|

出版日: 2025年01月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の変電所オートメーションおよび統合市場は2024年に49億9,000万米ドルを占め、2030年には73億3,000万米ドルに達すると予測され、予測期間中のCAGRは6.6%です。

最先端技術を利用して変電所業務を自動化・最適化することは、変電所オートメーションおよび統合として知られています。送配電ネットワークの有効性、信頼性、安全性を向上させるため、制御システム、通信技術、保護装置、監視システムが統合されます。自動化と統合は、リアルタイムのデータ監視、遠隔制御、変電所と制御センター間の円滑な通信を容易にすることで、送電網の安定性を高め、ダウンタイムを減らし、再生可能エネルギー源の統合を容易にします。

信頼性が高く効率的な電力システムに対する需要の増加

世界の電力使用量の増加に伴い、電力プロバイダーや電力会社は、電力の安定的かつ継続的な供給を保証する必要に迫られています。遠隔制御、リアルタイムの監視、迅速な問題特定を可能にするオートメーションは、変電所の効率を向上させ、停電やダウンタイムの可能性を低減します。商業、住宅、産業部門における電力需要の増加に対応するため、自動化ソリューションはリソース配分を最適化し、人的ミスを減らし、送電網の全体的な信頼性を向上させます。

高い初期コスト

インテリジェント・エレクトロニクス・デバイス(IED)、プログラマブル・ロジック・コントローラ(PLC)、通信ネットワークは、既存の変電所の近代化や新しい自動化設備の建設に必要な高性能ハードウェアの一例です。これらの機器にはコストがかかります。さらに、これらの要素をレガシー・システムと統合するには、特別な知識が必要となるため、さらに費用がかさみます。これらの技術の導入は、財政的な制約に頻繁に直面する中小規模の電力会社にとっては困難です。特に資金力の乏しい貧しい国々では、長期的な運用・保守上のメリットがあるにもかかわらず、多額の先行投資が採用を妨げる可能性があります。

サイバーセキュリティへの注目の高まり

変電所の自動化やネットワーク化が進むにつれ、ハッキング、データ漏洩、不正アクセスなどのサイバー脅威の影響を受けやすくなっています。電力系統の完全性と信頼性を維持するには、個人情報を保護し、作業技術の安全性を確保する必要があります。自動化されたシステムを保護するため、政府や電力会社は、侵入検知システム、ファイアウォール、暗号化などの最先端のサイバーセキュリティ・ソリューションに資金を費やしています。悪意ある攻撃を防ぐだけでなく、厳しい規制基準を満たし、安全で継続的な電力供給を保証するためにも、サイバーセキュリティを重視する必要があります。

熟練労働者の不足

この分野がスマートグリッドや賢い電気製品のような最先端技術を取り入れるにつれて、特定の訓練や経験を積んだ専門家の必要性が高まっています。しかし、これらのシステムの効率的な展開と維持管理は、資格のある労働者の継続的な不足によって妨げられています。このギャップを埋め、従業員が現代のオートメーションや変電所エンジニアリング技術の複雑さに適応できるようにするには、シミュレーションベースのトレーニングや体験学習を重視した総合的なトレーニングプログラムがどうしても必要です。

COVID-19の影響

COVID-19の大流行は、サプライチェーンを混乱させ、インフラプロジェクトを遅延させ、電力会社の予算配分を変更させることで、電力変電所オートメーション&インテグレーション市場に大きな影響を与えました。ロックダウンや制限によって重要部品の生産と納入が遅れ、労働力不足がプロジェクトの遂行を妨げました。しかし、パンデミックはまた、回復力があり遠隔操作可能な電力システムの必要性を浮き彫りにし、自動化への関心を高めました。政府と電力会社は、送電網の信頼性を高め、パンデミック後の状況の中で変化するエネルギー需要に適応するため、近代化への取り組みを優先し始めました。

予測期間中、ハードウェア・セグメントが最大になる見込み

送電網の近代化を支える高度で信頼性の高いインフラの必要性から、ハードウェア・セグメントが最大と推定されます。インテリジェント電子デバイス(IED)、プログラマブルロジックコントローラ(PLC)、センサなどのハードウェアコンポーネントは、変電所のリアルタイム監視、制御、保護に不可欠です。さらに、送電網の信頼性向上と自動化の推進がハードウェア需要を加速し、シームレスなエネルギー配給を保証しています。

予測期間中、送電変電所セグメントのCAGRが最も高くなる見込み

長距離を効率的に送電する必要性が高まっていることから、トランスミッション分野は予測期間中に最も高いCAGRを記録すると予想されます。太陽光や風力などの再生可能エネルギーを送電網に統合するためには、安定したエネルギー供給のための高度な送電用変電設備が必要となります。さらに、送電網の近代化、送電網の信頼性向上、遠隔監視機能の推進が、配電を最適化するための自動送電変電所の採用を後押ししています。

最大のシェアを占める地域

アジア太平洋地域は、急速な都市化、工業化、エネルギー需要の急増により、予測期間中最大の市場シェアを占めると予想されます。このため、信頼性が高く効率的な電力供給を確保するために、老朽化した送電網の近代化が必要となっています。さらに、太陽光発電や風力発電などの再生可能エネルギー源の普及が進んでいるため、柔軟で適応性の高い送電網が必要とされており、これは高度な変電所自動化システムによって効果的に管理することができます。

CAGRが最も高い地域:

予測期間中、北米地域が最も高いCAGRを記録すると予測されます。これは、同地域が送電網の近代化イニシアチブに注力していることと、再生可能エネルギー源の普及が進んでいることから、高度な送電網管理ソリューションが必要とされているためです。さらに、エネルギー効率と持続可能性が重視されるようになり、送電網の信頼性と回復力の向上を目的とした規制が強化されたことで、高度な変電所自動化システムの需要が高まっています。

無料のカスタマイズサービス

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかを提供いたします:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 技術分析

- 用途分析

- エンドユーザー分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の変電所オートメーションおよび統合市場:コンポーネント別

- ハードウェア

- 制御システム

- 保護装置

- 通信システム

- センサーと計測機器

- ソフトウェア

- SCADAシステム

- エネルギー管理ソフトウェア(EMS)

- 資産管理ソフトウェア

- サービス

- メンテナンスとサポート

- コンサルティングサービス

- システム統合サービス

- その他のコンポーネント

第6章 世界の変電所オートメーションおよび統合市場:通信プロトコル別

- Modbus

- DNP3

- IEC61850規格

- OPCC

第7章 世界の変電所オートメーションおよび統合市場:技術別

- 監視とデータ収集

- 保護と制御

- 流通システムの自動化

- 通信

- サイバーセキュリティ技術

第8章 世界の変電所オートメーションおよび統合市場:用途別

- 送電変電所

- 配電変電所

- 発電変電所

- その他の用途

第9章 世界の変電所オートメーションおよび統合市場:エンドユーザー別

- 産業部門

- 商業部門

- ユーティリティプロバイダー

- 再生可能エネルギー

- 鉱業

- その他のエンドユーザー

第10章 世界の変電所オートメーションおよび統合市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第11章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第12章 企業プロファイリング

- Siemens AG

- Schneider Electric

- General Electric(GE)

- ABB Ltd.

- Eaton Corporation

- Honeywell International Inc.

- Rockwell Automation, Inc.

- Mitsubishi Electric Corporation

- Emerson Electric Co.

- Cisco Systems, Inc.

- ZIV Automation

- Alstom

- Toshiba Corporation

- Bharat Heavy Electricals Limited(BHEL)

- S&C Electric Company

- Hitachi, Ltd.

- Wipro Limited

- Rolta India Limited

- Larsen & Toubro Limited

- Koch Industries, Inc.

List of Tables

- Table 1 Global Power Substation Automation & Integration Market Outlook, By Region (2022-2030) ($MN)

- Table 2 Global Power Substation Automation & Integration Market Outlook, By Component (2022-2030) ($MN)

- Table 3 Global Power Substation Automation & Integration Market Outlook, By Hardware (2022-2030) ($MN)

- Table 4 Global Power Substation Automation & Integration Market Outlook, By Control Systems (2022-2030) ($MN)

- Table 5 Global Power Substation Automation & Integration Market Outlook, By Protection Devices (2022-2030) ($MN)

- Table 6 Global Power Substation Automation & Integration Market Outlook, By Communication Systems (2022-2030) ($MN)

- Table 7 Global Power Substation Automation & Integration Market Outlook, By Sensors and Instrumentation (2022-2030) ($MN)

- Table 8 Global Power Substation Automation & Integration Market Outlook, By Software (2022-2030) ($MN)

- Table 9 Global Power Substation Automation & Integration Market Outlook, By SCADA Systems (2022-2030) ($MN)

- Table 10 Global Power Substation Automation & Integration Market Outlook, By Energy Management Software (EMS) (2022-2030) ($MN)

- Table 11 Global Power Substation Automation & Integration Market Outlook, By Asset Management Software (2022-2030) ($MN)

- Table 12 Global Power Substation Automation & Integration Market Outlook, By Services (2022-2030) ($MN)

- Table 13 Global Power Substation Automation & Integration Market Outlook, By Maintenance and Support (2022-2030) ($MN)

- Table 14 Global Power Substation Automation & Integration Market Outlook, By Consulting Services (2022-2030) ($MN)

- Table 15 Global Power Substation Automation & Integration Market Outlook, By System Integration Services (2022-2030) ($MN)

- Table 16 Global Power Substation Automation & Integration Market Outlook, By Other Components (2022-2030) ($MN)

- Table 17 Global Power Substation Automation & Integration Market Outlook, By Communication Protocol (2022-2030) ($MN)

- Table 18 Global Power Substation Automation & Integration Market Outlook, By Modbus (2022-2030) ($MN)

- Table 19 Global Power Substation Automation & Integration Market Outlook, By DNP3 (2022-2030) ($MN)

- Table 20 Global Power Substation Automation & Integration Market Outlook, By IEC 61850 (2022-2030) ($MN)

- Table 21 Global Power Substation Automation & Integration Market Outlook, By OPC (2022-2030) ($MN)

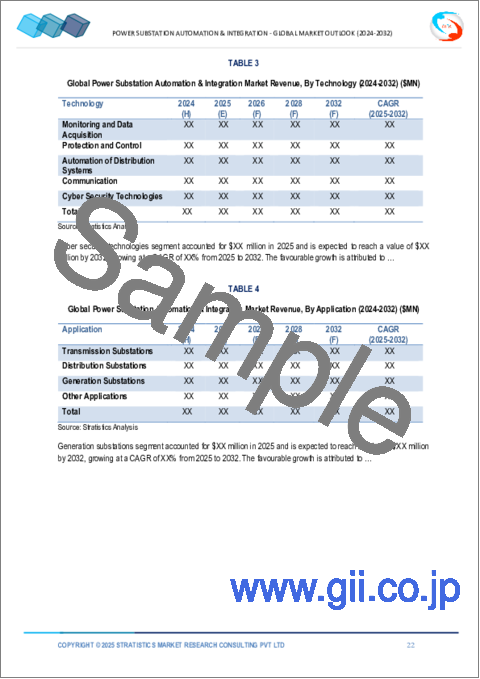

- Table 22 Global Power Substation Automation & Integration Market Outlook, By Technology (2022-2030) ($MN)

- Table 23 Global Power Substation Automation & Integration Market Outlook, By Monitoring and Data Acquisition (2022-2030) ($MN)

- Table 24 Global Power Substation Automation & Integration Market Outlook, By Protection and Control (2022-2030) ($MN)

- Table 25 Global Power Substation Automation & Integration Market Outlook, By Automation of Distribution Systems (2022-2030) ($MN)

- Table 26 Global Power Substation Automation & Integration Market Outlook, By Communication (2022-2030) ($MN)

- Table 27 Global Power Substation Automation & Integration Market Outlook, By Cyber Security Technologies (2022-2030) ($MN)

- Table 28 Global Power Substation Automation & Integration Market Outlook, By Application (2022-2030) ($MN)

- Table 29 Global Power Substation Automation & Integration Market Outlook, By Transmission Substations (2022-2030) ($MN)

- Table 30 Global Power Substation Automation & Integration Market Outlook, By Distribution Substations (2022-2030) ($MN)

- Table 31 Global Power Substation Automation & Integration Market Outlook, By Generation Substations (2022-2030) ($MN)

- Table 32 Global Power Substation Automation & Integration Market Outlook, By Other Applications (2022-2030) ($MN)

- Table 33 Global Power Substation Automation & Integration Market Outlook, By End User (2022-2030) ($MN)

- Table 34 Global Power Substation Automation & Integration Market Outlook, By Industrial Sector (2022-2030) ($MN)

- Table 35 Global Power Substation Automation & Integration Market Outlook, By Commercial Sector (2022-2030) ($MN)

- Table 36 Global Power Substation Automation & Integration Market Outlook, By Utility Providers (2022-2030) ($MN)

- Table 37 Global Power Substation Automation & Integration Market Outlook, By Renewable Energy (2022-2030) ($MN)

- Table 38 Global Power Substation Automation & Integration Market Outlook, By Mining (2022-2030) ($MN)

- Table 39 Global Power Substation Automation & Integration Market Outlook, By Other End Users (2022-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above

According to Stratistics MRC, the Global Power Substation Automation & Integration Market is accounted for $4.99 billion in 2024 and is expected to reach $7.33 billion by 2030 growing at a CAGR of 6.6% during the forecast period. Automating and optimizing electrical substation operations through the use of cutting-edge technologies is known as power substation automation and integration. To improve the effectiveness, dependability, and security of power transmission and distribution networks, control systems, communication technologies, protection devices, and monitoring systems are integrated. Automation and integration increase grid stability, decrease downtime, and make it easier to integrate renewable energy sources by facilitating real-time data monitoring, remote control, and smooth communication between substations and control centers.

Market Dynamics:

Driver:

Increased demand for reliable and efficient power systems

Power providers and utilities are under pressure to guarantee a steady and continuous supply of electricity as global power usage climbs. By enabling remote control, real-time monitoring, and quicker problem identification, automation improves substation efficiency and lowers the likelihood of outages and downtime. To satisfy the increasing demand for electricity in the commercial, residential, and industrial sectors, automated solutions also optimize resource allocation, lower human error, and increase the overall reliability of the power grid.

Restraint:

High initial costs

Intelligent electronic devices (IEDs), programmable logic controllers (PLCs), and communication networks are examples of high-performance hardware that is necessary for modernizing existing substations or constructing new automated facilities. These gadgets can be costly. Furthermore, integrating these elements with legacy systems necessitates specific knowledge, which raises expenses even more. Adoption of these technologies is challenging for small and medium-sized utilities, who frequently face financial constraints. The large upfront expenditures may prevent adoption, especially in poorer nations with low financial resources, even though there will be long-term operational and maintenance benefits.

Opportunity:

Growing focus on cybersecurity

Substations are more susceptible to cyber-threats including hacking, data breaches, and illegal access as they get more automated and networked. Maintaining the integrity and dependability of the power system depends on safeguarding private information and making sure that working technologies are secure. To protect their automated systems, governments and utilities are spending money on cutting-edge cybersecurity solutions, such as intrusion detection systems, firewalls, and encryption. In addition to preventing malicious attacks, this emphasis on cybersecurity is necessary to meet strict regulatory standards and guarantee safe and continuous electricity delivery.

Threat:

Lack of skilled workforce

The need for experts with specific training and experience has increased as the sector embraces cutting-edge technology like smart grids and clever electrical products. However, the efficient deployment and upkeep of these systems are hampered by ongoing shortages of qualified workers. Comprehensive training programs that emphasize simulation-based training and experiential learning are desperately needed to close this gap and help employees adjust to the complexity of contemporary automation and substation engineering technology.

Covid-19 Impact

The COVID-19 pandemic significantly impacted the Power Substation Automation & Integration market by disrupting supply chains, delaying infrastructure projects, and causing budget reallocations in utilities. Lockdowns and restrictions slowed the production and delivery of critical components, while workforce shortages hindered project execution. However, the pandemic also underscored the need for resilient and remote-operable power systems, driving interest in automation. Governments and utilities began prioritizing modernization efforts to enhance grid reliability and adapt to changing energy demands in a post-pandemic landscape.

The hardware segment is expected to be the largest during the forecast period

The hardware segment is estimated to be the largest, due to the need for advanced and reliable infrastructure to support the modernization of power grids. Hardware components such as intelligent electronic devices (IEDs), programmable logic controllers (PLCs), and sensors are crucial for real-time monitoring, control, and protection of substations. Additionally, the push for improved grid reliability and automation accelerates hardware demand, ensuring seamless energy distribution.

The transmission substations segment is expected to have the highest CAGR during the forecast period

The transmission substations segment is anticipated to witness the highest CAGR during the forecast period, due to the growing need for efficient electricity transmission across long distances. The integration of renewable energy sources, such as solar and wind, into the grid necessitates advanced transmission substations for stable energy flow. Additionally, the push for grid modernization, enhanced grid reliability, and remote monitoring capabilities fuels the adoption of automated transmission substations for optimized power distribution.

Region with largest share:

Asia Pacific is expected to have the largest market share during the forecast period due to rapid urbanization, industrialization, and a surge in energy demand. This necessitates the modernization of aging power grids to ensure reliable and efficient power delivery. Furthermore, the increasing penetration of renewable energy sources, such as solar and wind power, requires flexible and adaptable grids, which can be effectively managed through advanced substation automation systems.

Region with highest CAGR:

During the forecast period, the North America region is anticipated to register the highest CAGR, owing to the region's focus on grid modernization initiatives, coupled with the increasing penetration of renewable energy sources, necessitates advanced grid management solutions. Furthermore, the growing emphasis on energy efficiency and sustainability, along with stringent regulations aimed at improving grid reliability and resilience, are driving the demand for sophisticated substation automation systems.

Key players in the market

Some of the key players profiled in the Power Substation Automation & Integration Market include Siemens AG, Schneider Electric, General Electric (GE), ABB Ltd., Eaton Corporation, Honeywell International Inc., Rockwell Automation, Inc., Mitsubishi Electric Corporation, Emerson Electric Co., Cisco Systems, Inc., ZIV Automation, Alstom, Toshiba Corporation, Bharat Heavy Electricals Limited (BHEL), S&C Electric Company, Hitachi, Ltd., Wipro Limited, Rolta India Limited, Larsen & Toubro Limited, and Koch Industries, Inc.

Key Developments:

In November 2024, Rockwell Automation, Inc. the world's largest company dedicated to industrial automation and digital transformation, introduces FactoryTalk(R) Analytics(TM) VisionAI(TM), a cutting-edge inspection solution that leverages artificial intelligence (AI) and machine learning to revolutionize quality control in manufacturing.

In October 2024, Schneider Electric has formed a strategic partnership with Noida International Airport to introduce building and energy management solutions. Through this collaboration, Schneider Electric will roll out complete building management solutions, comprising Electrical SCADA and Advanced Distribution Management System, aimed at significantly boosting the airport's operational efficiency and sustainability.

In April 2024, GE announced its official launch as an independent public company defining the future of flight, following the completion of the GE Vernova spin-off. GE Aerospace will trade on the New York Stock Exchange (NYSE) under the ticker "GE".

Components Covered:

- Hardware

- Software

- Services

- Other Components

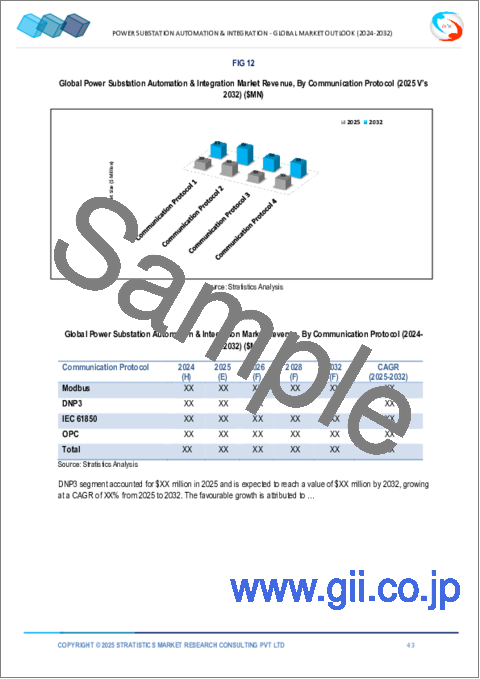

Communication Protocols Covered:

- Modbus

- DNP3

- IEC 61850

- OPC

Technologies Covered:

- Monitoring and Data Acquisition

- Protection and Control

- Automation of Distribution Systems

- Communication

- Cyber Security Technologies

Applications Covered:

- Transmission Substations

- Distribution Substations

- Generation Substations

- Other Applications

End Users Covered:

- Industrial Sector

- Commercial Sector

- Utility Providers

- Renewable Energy

- Mining

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2022, 2023, 2024, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Technology Analysis

- 3.7 Application Analysis

- 3.8 End User Analysis

- 3.9 Emerging Markets

- 3.10 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Power Substation Automation & Integration Market, By Component

- 5.1 Introduction

- 5.2 Hardware

- 5.2.1 Control Systems

- 52.2 Protection Devices

- 5.2.2 Communication Systems

- 53.2 Sensors and Instrumentation

- 5.3 Software

- 5.3.1 SCADA Systems

- 5.3.2 Energy Management Software (EMS)

- 5.3.3 Asset Management Software

- 5.4 Services

- 5.4.1 Maintenance and Support

- 5.4.2 Consulting Services

- 5.4.3 System Integration Services

- 5.5 Other Components

6 Global Power Substation Automation & Integration Market, By Communication Protocol

- 6.1 Introduction

- 6.2 Modbus

- 6.3 DNP3

- 6.4 IEC 61850

- 6.5 OPC

7 Global Power Substation Automation & Integration Market, By Technology

- 7.1 Introduction

- 7.2 Monitoring and Data Acquisition

- 7.3 Protection and Control

- 7.4 Automation of Distribution Systems

- 7.5 Communication

- 7.6 Cyber Security Technologies

8 Global Power Substation Automation & Integration Market, By Application

- 8.1 Introduction

- 8.2 Transmission Substations

- 8.3 Distribution Substations

- 8.4 Generation Substations

- 8.5 Other Applications

9 Global Power Substation Automation & Integration Market, By End User

- 9.1 Introduction

- 9.2 Industrial Sector

- 9.3 Commercial Sector

- 9.4 Utility Providers

- 9.5 Renewable Energy

- 9.6 Mining

- 9.7 Other End Users

10 Global Power Substation Automation & Integration Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.5 South America

- 10.5.1 Argentina

- 10.5.2 Brazil

- 10.5.3 Chile

- 10.5.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 Siemens AG

- 12.2 Schneider Electric

- 12.3 General Electric (GE)

- 12.4 ABB Ltd.

- 12.5 Eaton Corporation

- 12.6 Honeywell International Inc.

- 12.7 Rockwell Automation, Inc.

- 12.8 Mitsubishi Electric Corporation

- 12.9 Emerson Electric Co.

- 12.10 Cisco Systems, Inc.

- 12.11 ZIV Automation

- 12.12 Alstom

- 12.13 Toshiba Corporation

- 12.14 Bharat Heavy Electricals Limited (BHEL)

- 12.15 S&C Electric Company

- 12.16 Hitachi, Ltd.

- 12.17 Wipro Limited

- 12.18 Rolta India Limited

- 12.19 Larsen & Toubro Limited

- 12.20 Koch Industries, Inc.