|

|

市場調査レポート

商品コード

1558262

化学品包装市場の2030年までの予測:包装タイプ、素材、流通チャネル、エンドユーザー、地域別の世界分析Chemical Packaging Market Forecasts to 2030 - Global Analysis By Packaging Type, Material, Distribution Channel, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 化学品包装市場の2030年までの予測:包装タイプ、素材、流通チャネル、エンドユーザー、地域別の世界分析 |

|

出版日: 2024年09月06日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の化学品包装市場は2024年に165億2,000万米ドルを占め、予測期間中のCAGRは5.2%で成長し、2030年には227億3,000万米ドルに達する見込みです。

化学品包装とは、化学物質や関連物質を封じ込め、保護し、輸送するために使用される材料や方法を指します。安全性、安定性、規制基準の遵守を確保するために、適切な容器や包装ソリューションを選択することが含まれます。化学物質包装は、製品の完全性を維持し、取り扱いと輸送時の安全性を高め、適切な表示と情報伝達を確保する上で重要な役割を果たします。

米国化学工業協会(American Chemistry Council)によると、有機化学品、無機化学品、プラスチック樹脂、合成ゴム、製造繊維を含む基礎化学品は、パンデミックの初期段階で世界生産量が1.4%増加し、COVID-19による実質的な影響は見られません。

特殊化学品に対する需要の増加

特殊化学品は、その安定性、有効性、安全性を維持するために、特定の包装材料や設計を必要とすることが多いです。この需要は、高性能プラスチック、バリアフィルム、特殊容器などの革新的な包装技術や材料の開発を促しています。医薬品、農業、エレクトロニクスなどの産業が特殊化学物質の使用を拡大するにつれて、安全でコンプライアンスが高く、効率的なパッケージング・ソリューションの必要性が高まっています。その結果、包装メーカーは技術革新と製品ラインナップの拡充に努め、市場全体の成長に拍車をかけています。

化学反応のリスク

化学物質包装における化学反応のリスクは、包装材料が含有化学物質と悪影響を及ぼし、劣化や汚染につながる場合に生じます。これは、化学的特性と包装材料との不適合から生じる可能性があり、例えば、反応によって漏出、腐食、化学組成の変化などが引き起こされます。こうした問題は製品の安全性と有効性を損ない、規制への不適合や経済的損失につながる可能性があります。こうしたリスクは、運営経費を押し上げ、サプライチェーンに潜在的な混乱を引き起こすことによって、市場の成長を妨げる可能性があります。

包装技術の革新

スマートセンサーや温度制御システムなどの先端技術は、化学的条件の監視と管理を改善し、製品の安定性と規制へのコンプライアンスを確保します。生分解性プラスチックや高度なバリアフィルムなどの素材における革新は、環境への懸念に対処し、持続可能なソリューションを求める消費者の需要に応えます。さらに、改良されたクロージャーやタンパーエビデント機能など、パッケージングデザインの開発は、保護を強化し、汚染を防止します。これらの進歩は、より優れた性能を提供し、規制要件を満たし、進化する業界のニーズに対応することで、市場の成長を促進しています。

高い包装コスト

化学物質包装は、安全性、コンプライアンス、化学的相互作用からの保護を確保するための特殊な材料や設計が必要なため、しばしば高いコストがかかります。これには、高度なバリア材料、改ざん防止機能、安全なクロージャーなどが含まれます。これらのパッケージング・ソリューションに求められる複雑さと精密さは、生産コストと材料コストを押し上げます。高いパッケージングコストは、中小企業にとって購入しやすい価格を制限し、利益率を低下させ、化学製品の総コストを増加させることにより、市場の成長を妨げる可能性があります。

COVID-19の影響

COVID-19の大流行は、サプライチェーンを混乱させ、材料費を増加させ、生産に遅れを生じさせることで、化学品包装市場に影響を与えました。その結果、医薬品と除菌セクターの包装ソリューションに対する需要が高まりました。eコマースへのシフトと、安全性と衛生のための保護包装の使用の増加は、市場力学にさらに影響を与えました。しかし、パンデミックはまた、産業界が新たな健康と環境の優先事項に適応するにつれて、持続可能で革新的なパッケージング技術の採用を加速させました。

予測期間中はドラムセグメントが最大になると予測される

予測期間中、ドラム缶分野が最大になると予測されます。ドラム包装は、液体や粉体の大量貯蔵や輸送に理想的で、漏れや汚染に対する強固な保護を提供します。ドラム缶は、取り扱い、積み重ね、環境条件に耐えるように設計されています。多くの場合、安全性とコンプライアンスを確保するために、安全なクロージャーと改ざん防止シールを備えています。ドラム包装は、その耐久性と大量管理における効率性により、化学製造、医薬品、農業などの産業で広く使用されています。

予測期間中、医薬品分野のCAGRが最も高くなる見込み

医薬品分野は、予測期間中に最も高いCAGR成長が見込まれます。医薬品では、化学品包装によって医薬品有効成分(API)や完成品の安全な封じ込めと輸送が保証されます。薬剤の有効性、安定性、純度を維持するために、特殊な材料や設計が必要となります。先進パッケージングはまた、投与量の正確性をサポートし、保存期間を延長し、全体的な医薬品の品質と信頼性を高めます。

最大のシェアを占める地域

アジア太平洋地域の化学品包装市場は、産業活動の拡大と化学製品の生産量増加に牽引され、予測期間中に最大のシェアを占めると予測されます。急速な工業化、都市化、中間層の急増が、化学薬品、ひいては包装ソリューションの需要拡大に寄与しています。同地域では環境の持続可能性への関心が高まっており、環境に優しいパッケージング材料の先進化が進んでいます。主要国には中国、インド、日本が含まれ、これらはこの市場拡大に大きく貢献しています。

CAGRが最も高い地域:

北米地域は、確立された化学産業と安全な化学物質の取り扱いに関する厳しい規制要件に牽引され、予測期間中に最も高い成長を遂げると考えられています。この地域は技術革新とテクノロジーに重点を置いており、先進パッケージング・ソリューションの開発を促進しています。持続可能でリサイクル可能な包装材料へのシフトと相まって、特殊化学品や高機能化学品に対する需要の増加が市場の成長を支えています。大手化学メーカーの存在と拡大する製薬・農業セクターは、北米の化学品包装市場の堅調な拡大にさらに貢献しています。

無料のカスタマイズサービス

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- エンドユーザー分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の化学品包装市場:包装タイプ別

- ドラム

- 容器・バケツ

- 中間バルクコンテナ(IBC)

- トートバッグ&タンクトップ

- 缶・ボトル

- バレル

- その他の包装タイプ

第6章 世界の化学品包装市場:素材別

- プラスチック

- ポリエチレン(PE)

- ポリプロピレン(PP)

- ポリエチレンテレフタレート(PET)

- ポリ塩化ビニル(PVC)

- ガラス

- 金属

- 紙・板紙

- 複合材料

- その他の素材

第7章 世界の化学品包装市場:流通チャネル別

- 直接販売

- 販売代理店

- 小売り

- eコマース

- その他の流通チャネル

第8章 世界の化学品包装市場:エンドユーザー別

- 化学・石油化学製品

- 医薬品

- 農業

- 食品・飲料

- 塗料とコーティング

- 洗剤・洗浄剤

- 化粧品・パーソナルケア

- その他のエンドユーザー

第9章 世界の化学品包装市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第10章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第11章 企業プロファイリング

- Amcor

- Berry Global

- Sealed Air Corporation

- Crown Holdings

- Bemis Company, Inc.

- Sonoco Products Company

- Greif Inc.

- International Paper

- Mondi Group

- Reynolds Group Holdings

- WestRock

- RPC Group

- Silgan Holdings

- Clondalkin Group

- Scholle IPN

- 2M Group

- Crocco SpA SB

List of Tables

- Table 1 Global Chemical Packaging Market Outlook, By Region (2022-2030) ($MN)

- Table 2 Global Chemical Packaging Market Outlook, By Packaging Type (2022-2030) ($MN)

- Table 3 Global Chemical Packaging Market Outlook, By Drums (2022-2030) ($MN)

- Table 4 Global Chemical Packaging Market Outlook, By Pails & Buckets (2022-2030) ($MN)

- Table 5 Global Chemical Packaging Market Outlook, By Intermediate Bulk Containers (IBCs) (2022-2030) ($MN)

- Table 6 Global Chemical Packaging Market Outlook, By Totes & Tanks (2022-2030) ($MN)

- Table 7 Global Chemical Packaging Market Outlook, By Cans & Bottles (2022-2030) ($MN)

- Table 8 Global Chemical Packaging Market Outlook, By Barrels (2022-2030) ($MN)

- Table 9 Global Chemical Packaging Market Outlook, By Other Packaging Types (2022-2030) ($MN)

- Table 10 Global Chemical Packaging Market Outlook, By Material (2022-2030) ($MN)

- Table 11 Global Chemical Packaging Market Outlook, By Plastic (2022-2030) ($MN)

- Table 12 Global Chemical Packaging Market Outlook, By Polyethylene (PE) (2022-2030) ($MN)

- Table 13 Global Chemical Packaging Market Outlook, By Polypropylene (PP) (2022-2030) ($MN)

- Table 14 Global Chemical Packaging Market Outlook, By Polyethylene Terephthalate (PET) (2022-2030) ($MN)

- Table 15 Global Chemical Packaging Market Outlook, By Polyvinyl Chloride (PVC) (2022-2030) ($MN)

- Table 16 Global Chemical Packaging Market Outlook, By Glass (2022-2030) ($MN)

- Table 17 Global Chemical Packaging Market Outlook, By Metal (2022-2030) ($MN)

- Table 18 Global Chemical Packaging Market Outlook, By Paper & Paperboard (2022-2030) ($MN)

- Table 19 Global Chemical Packaging Market Outlook, By Composites (2022-2030) ($MN)

- Table 20 Global Chemical Packaging Market Outlook, By Other Materials (2022-2030) ($MN)

- Table 21 Global Chemical Packaging Market Outlook, By Distribution Channel (2022-2030) ($MN)

- Table 22 Global Chemical Packaging Market Outlook, By Direct Sales (2022-2030) ($MN)

- Table 23 Global Chemical Packaging Market Outlook, By Distributors (2022-2030) ($MN)

- Table 24 Global Chemical Packaging Market Outlook, By Retail (2022-2030) ($MN)

- Table 25 Global Chemical Packaging Market Outlook, By E-commerce (2022-2030) ($MN)

- Table 26 Global Chemical Packaging Market Outlook, By Other Distribution Channels (2022-2030) ($MN)

- Table 27 Global Chemical Packaging Market Outlook, By End User (2022-2030) ($MN)

- Table 28 Global Chemical Packaging Market Outlook, By Chemicals & Petrochemicals (2022-2030) ($MN)

- Table 29 Global Chemical Packaging Market Outlook, By Pharmaceuticals (2022-2030) ($MN)

- Table 30 Global Chemical Packaging Market Outlook, By Agriculture (2022-2030) ($MN)

- Table 31 Global Chemical Packaging Market Outlook, By Food & Beverages (2022-2030) ($MN)

- Table 32 Global Chemical Packaging Market Outlook, By Paints & Coatings (2022-2030) ($MN)

- Table 33 Global Chemical Packaging Market Outlook, By Detergents & Cleaning Products (2022-2030) ($MN)

- Table 34 Global Chemical Packaging Market Outlook, By Cosmetics & Personal Care (2022-2030) ($MN)

- Table 35 Global Chemical Packaging Market Outlook, By Other End Users (2022-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Chemical Packaging Market is accounted for $16.52 billion in 2024 and is expected to reach $22.73 billion by 2030 growing at a CAGR of 5.2% during the forecast period. Chemical packaging refers to the materials and methods used to contain, protect, and transport chemicals and related substances. It involves selecting appropriate containers and packaging solutions to ensure safety, stability, and compliance with regulatory standards. Chemical packaging plays a crucial role in maintaining product integrity, enhancing safety during handling and transport, and ensuring proper labeling and information dissemination.

According to the American Chemistry Council, basic chemicals, including organic chemicals, inorganics chemicals, plastic resins, synthetic rubber, and manufactured fibers, witnessed a global production increase of 1.4% during the initial phases of the pandemic and have not seen a substantial impact due to COVID-19.

Market Dynamics:

Driver:

Increased demand for specialty chemicals

Specialty chemicals often require specific packaging materials and designs to maintain their stability, effectiveness, and safety. This demand prompts the development of innovative packaging technologies and materials, such as high-performance plastics, barrier films, and specialized containers. As industries like pharmaceuticals, agriculture, and electronics expand their use of specialty chemicals, the need for secure, compliant, and efficient packaging solutions grows. Consequently, packaging manufacturers are driven to innovate and expand their offerings, fueling overall market growth.

Restraint:

Risk of chemical reactions

The risk of chemical reactions in chemical packaging arises when packaging materials interact adversely with the contained chemicals, leading to degradation or contamination. This can result from incompatibilities between the chemical properties and the packaging material, such as reactions causing leaks, corrosion, or changes in chemical composition. These issues compromise product safety and efficacy, potentially leading to regulatory non-compliance and financial losses. Such risks can hamper market growth by driving up operational expenses, and causing potential disruptions in the supply chain.

Opportunity:

Innovations in packaging technologies

Advanced technologies, such as smart sensors and temperature-control systems, improve the monitoring and management of chemical conditions, ensuring product stability and compliance with regulations. Innovations in materials, like biodegradable plastics and advanced barrier films, address environmental concerns and meet consumer demand for sustainable solutions. Furthermore, developments in packaging design, including improved closures and tamper-evident features, enhance protection and prevent contamination. These advancements drive market growth by offering better performance, meeting regulatory requirements, and responding to evolving industry needs.

Threat:

High packaging costs

Chemical packaging often incurs high costs due to the need for specialized materials and designs that ensure safety, compliance, and protection against chemical interactions. These include advanced barrier materials, tamper-evident features, and secure closures. The complexity and precision required for these packaging solutions drive up production and material costs. High packaging costs can hamper market growth by limiting affordability for smaller companies, reducing profit margins, and increasing the overall cost of chemical products.

Covid-19 Impact

The covid-19 pandemic impacted the chemical packaging market by disrupting supply chains, increasing material costs, and causing delays in production. It led to heightened demand for packaging solutions in the pharmaceutical and sanitization sectors. The shift towards e-commerce and increased use of protective packaging for safety and hygiene further influenced market dynamics. However, the pandemic also accelerated the adoption of sustainable and innovative packaging technologies as industries adapted to new health and environmental priorities.

The drums segment is expected to be the largest during the forecast period

The drums segment is estimated to be the largest during the forecast period. Drum packaging is ideal for bulk storage and transportation of liquids and powders, offering robust protection against leaks and contamination. Drums are designed to withstand handling, stacking, and environmental conditions. They often feature secure closures and tamper-evident seals to ensure safety and compliance. Drum packaging is widely used across industries, including chemical manufacturing, pharmaceuticals, and agriculture, due to its durability and efficiency in managing large volumes.

The pharmaceuticals segment is expected to have the highest CAGR during the forecast period

The pharmaceuticals segment is anticipated to witness the highest CAGR growth during the forecast period. In pharmaceuticals, chemical packaging ensures the safe containment and transport of active pharmaceutical ingredients (APIs) and finished products. It involves using specialized materials and designs to maintain drug efficacy, stability, and purity. Advanced packaging also supports dose accuracy and extends shelf life, enhancing overall pharmaceutical product quality and reliability.

Region with largest share:

The chemical packaging market in the Asia-Pacific region is projected to witness largest share during the forecast period driven by expanding industrial activities and increasing chemical production. Rapid industrialization, urbanization, and a burgeoning middle class contribute to rising demand for chemicals and, consequently, packaging solutions. The region's growing focus on environmental sustainability is leading to advancements in eco-friendly packaging materials. Key countries include China, India, and Japan, which are significant contributors to this expanding market.

Region with highest CAGR:

North America region is attributed to witness the highest growth during the forecast period driven by a well-established chemical industry and stringent regulatory requirements for safe chemical handling. The region's focus on innovation and technology fosters the development of advanced packaging solutions. Increased demand for specialty and high-performance chemicals, coupled with a shift towards sustainable and recyclable packaging materials, supports market growth. The presence of major chemical manufacturers and the expanding pharmaceutical and agricultural sectors further contribute to the robust expansion of the chemical packaging market in North America.

Key players in the market

Some of the key players profiled in the Chemical Packaging Market include Amcor, Berry Global, Sealed Air Corporation, Crown Holdings, Bemis Company, Inc., Sonoco Products Company, Greif Inc., International Paper, Mondi Group, Reynolds Group Holdings, WestRock, RPC Group, Silgan Holdings, Clondalkin Group, Scholle IPN, 2M Group and Crocco SpA SB.

Key Developments:

In July 2024, 2M Group of Companies has launched a new packaging focused business unit, Sustainable Packaging Technologies, to promote its growing portfolio of biomaterial technologies. From enhancing the shelf life of goods to reducing waste, or meeting regulatory requirements, Sustainable Packaging Technologies will use its expertise and technology partnerships to help its clients achieve their environmental goals.

In June 2024, Crocco together with Versalis, Eni's chemical company, have launched a collaboration to produce packaging film made from raw materials partly derived from the recycling of post-consumer plastics, targeting mass production for the large-scale retail market. The production of packaging containing material derived from chemical recycling also promotes more efficient resource management, contributing to a marked decrease in the use of virgin resources and aligns with Versalis' circular economy and sustainability goals.

Packaging Types Covered:

- Drums

- Pails & Buckets

- Intermediate Bulk Containers (IBCs)

- Totes & Tanks

- Cans & Bottles

- Barrels

- Other Packaging Types

Materials Covered:

- Plastic

- Glass

- Metal

- Paper & Paperboard

- Composites

- Other Materials

Distribution Channels Covered:

- Direct Sales

- Distributors

- Retail

- E-commerce

- Other Distribution Channels

End Users Covered:

- Chemicals & Petrochemicals

- Pharmaceuticals

- Agriculture

- Food & Beverages

- Paints & Coatings

- Detergents & Cleaning Products

- Cosmetics & Personal Care

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2022, 2023, 2024, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 End User Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Chemical Packaging Market, By Packaging Type

- 5.1 Introduction

- 5.2 Drums

- 5.3 Pails & Buckets

- 5.4 Intermediate Bulk Containers (IBCs)

- 5.5 Totes & Tanks

- 5.6 Cans & Bottles

- 5.7 Barrels

- 5.8 Other Packaging Types

6 Global Chemical Packaging Market, By Material

- 6.1 Introduction

- 6.2 Plastic

- 6.2.1 Polyethylene (PE)

- 6.2.2 Polypropylene (PP)

- 6.2.3 Polyethylene Terephthalate (PET)

- 6.2.4 Polyvinyl Chloride (PVC)

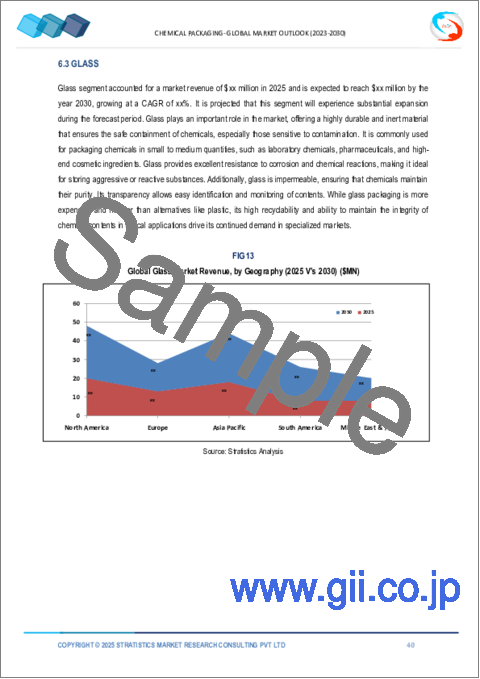

- 6.3 Glass

- 6.4 Metal

- 6.5 Paper & Paperboard

- 6.6 Composites

- 6.7 Other Materials

7 Global Chemical Packaging Market, By Distribution Channel

- 7.1 Introduction

- 7.2 Direct Sales

- 7.3 Distributors

- 7.4 Retail

- 7.5 E-commerce

- 7.6 Other Distribution Channels

8 Global Chemical Packaging Market, By End User

- 8.1 Introduction

- 8.2 Chemicals & Petrochemicals

- 8.3 Pharmaceuticals

- 8.4 Agriculture

- 8.5 Food & Beverages

- 8.6 Paints & Coatings

- 8.7 Detergents & Cleaning Products

- 8.8 Cosmetics & Personal Care

- 8.9 Other End Users

9 Global Chemical Packaging Market, By Geography

- 9.1 Introduction

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 Italy

- 9.3.4 France

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 China

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 New Zealand

- 9.4.6 South Korea

- 9.4.7 Rest of Asia Pacific

- 9.5 South America

- 9.5.1 Argentina

- 9.5.2 Brazil

- 9.5.3 Chile

- 9.5.4 Rest of South America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 Qatar

- 9.6.4 South Africa

- 9.6.5 Rest of Middle East & Africa

10 Key Developments

- 10.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 10.2 Acquisitions & Mergers

- 10.3 New Product Launch

- 10.4 Expansions

- 10.5 Other Key Strategies

11 Company Profiling

- 11.1 Amcor

- 11.2 Berry Global

- 11.3 Sealed Air Corporation

- 11.4 Crown Holdings

- 11.5 Bemis Company, Inc.

- 11.6 Sonoco Products Company

- 11.7 Greif Inc.

- 11.8 International Paper

- 11.9 Mondi Group

- 11.10 Reynolds Group Holdings

- 11.11 WestRock

- 11.12 RPC Group

- 11.13 Silgan Holdings

- 11.14 Clondalkin Group

- 11.15 Scholle IPN

- 11.16 2M Group

- 11.17 Crocco SpA SB