|

|

市場調査レポート

商品コード

1530875

自動車部品の世界市場予測(~2030年): 製品タイプ、車両タイプ、地域別の分析Automotive Components Market Forecasts to 2030 - Global Analysis By Product Type, Vehicle Type and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 自動車部品の世界市場予測(~2030年): 製品タイプ、車両タイプ、地域別の分析 |

|

出版日: 2024年08月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

世界の自動車部品の市場規模は、2024年に2兆1,118億5,000万米ドルを占め、予測期間中にCAGR7.5%で成長し、2030年には3兆2,592億2,000万米ドルに達すると予測されています。 自動車部品とは、自動車を構成し、その機能性、安全性、性能を確保するために不可欠な部品を指します。

これらの部品は、エンジンやトランスミッションシステムから、ブレーキ、ステアリング、サスペンションシステムに至るまで、幅広い部品を含んでいます。各部品は、自動車の全体的な動作と完全性において重要な役割を果たしています。自動車部品は、自動車の機能性、安全性、性能にとって不可欠なものです。エンジンやトランスミッションから最小の電気センサーに至るまで、各部品は重要な役割を果たしています。一般的にガソリンやディーゼルを動力源とするエンジンは、燃料を機械的エネルギーに変換し、車両を推進します。

環境と持続可能性の動向

環境と持続可能性の動向は、より環境に優しく効率的なソリューションに向けた技術革新を促進することで、自動車部品業界に大きな影響を与えています。自動車メーカーや部品メーカーは、燃費を向上させるための軽量素材の使用、電気自動車やハイブリッド車技術の開発、使用済み自動車のリサイクルプログラムの実施など、二酸化炭素排出量を削減するための手法を採用するようになってきています。このような動向は、自動車部品の設計と生産プロセスを再構築しつつあります。

原材料価格の変動

原材料価格の変動は、自動車部品業界にとって大きな課題となります。原材料は生産コストのかなりの部分を占めるため、突然の価格上昇はコスト予測と収益性を混乱させる可能性があります。この変動は、計画や調達から価格設定や在庫管理まで、様々な段階でメーカーに影響を与えます。自動車部品は、供給元が限られた特定の材料を必要とするため、価格変動の影響をさらに悪化させる可能性があります。こうしたリスクを軽減するため、企業はヘッジ戦略やサプライヤーとの長期契約に頼ることが多いですが、こうした手段は急激な価格高騰や予期せぬサプライチェーンの混乱に対して万全ではありません。その結果、こうした不安定さが技術革新やテクノロジーへの投資を妨げ、製品開発や品質に影響を及ぼす可能性があります。

自動運転技術の進歩

自動運転技術の進歩は、より高いレベルの精度、信頼性、統合性を要求することで、自動車部品を大きく変化させています。従来の機械システムは、自動車が自律的に環境を認識し対応できるようにする高度な電子システムやセンサーベースのシステムによって補強され、あるいは置き換えられつつあります。センサー(LiDAR、レーダー、カメラなど)、アクチュエーター、コンピューティング・ユニットなどの主要コンポーネントは、車両がリアルタイムでナビゲートし、意思決定し、他の車両やインフラと通信することを可能にする上で極めて重要になっています。この進化は自動車業界全体のイノベーションを促進し、従来の自動車メーカー、ハイテク企業、エレクトロニクスやソフトウェアを専門とするサプライヤー間のコラボレーションを促進しています。

知的財産権

知的財産権(IPR)は、イノベーションと競争を制限する可能性があるため、自動車部品業界に課題をもたらす可能性があります。知的財産権は、自動車部品にとって重要な技術や設計を含む企業の創作や発明を保護する一方で、中小メーカーや新興企業の市場参入を妨げる障壁につながる可能性もあります。例えば、多数の特許が重複する技術をカバーする特許の藪は、新しい自動車部品を開発しようとする企業にとって、法的な複雑さとコストを増大させる可能性があります。しかし、特許の取得や権利行使に時間がかかるため、新製品の市場導入が遅れ、技術革新が遅れる可能性があります。

COVID-19の影響:

COVID-19の流行は自動車部品分野に大きな影響を与えました。当初、広範囲に及ぶ操業停止とサプライチェーンの混乱が世界中の生産スケジュールを狂わせ、半導体や電子部品などの必須部品の不足につながりました。これは自動車製造を遅らせただけでなく、需要増と供給制限によるコスト増をもたらしました。消費者需要の変動と金融不安により、自動車メーカーは生産計画と在庫管理戦略の見直しを余儀なくされました。

予測期間中、冷却システムセグメントが最大となる見込み

冷却システムセグメントは、エンジン温度を調整し、最適な性能と寿命を確保することで、予測期間中に最大となる見込みです。ラジエーター、クーラントホース、ウォーターポンプ、サーモスタットなど様々な部品で構成されるこのシステムは、エンジンからの放熱を効果的に管理し、運転効率を維持します。先進的な材料と設計革新により、これらの部品は継続的に改良され、耐久性、効率、環境への配慮が強化されています。

予測期間中にCAGRが最も高くなると予想されるのは乗用車セグメントです。

乗用車セグメントは、予測期間中に最も高いCAGRが見込まれます。効率性、安全性、快適性に対する消費者の要求が高まるにつれて、自動車部品メーカーは技術革新を余儀なくされます。このセグメントは特に、電気推進システム、自律走行機能などの高度な安全機能、強化されたインフォテインメント・システムなどの最先端技術の開発に影響を与えています。エンジニアや設計者は、乗用車に合わせた軽量素材、効率的なエンジン、スマート・コネクティビティ・ソリューションの統合に注力しています。

最大のシェアを占める地域

予測期間中、北米が市場で最大のシェアを占めました。同地域では、近代化された製造施設、効率的な物流ネットワーク、先進的な研究開発センターなどのインフラが整備されています。これらの地域開発により、生産サイクルの迅速化、品質管理の強化、製造プロセスにおける自動化やAIなどの最先端技術の採用が可能になります。さらに、改善されたインフラはジャスト・イン・タイムのサプライチェーンをサポートし、地域全体の輸送と在庫管理に関連するリードタイムとコストを削減します。これにより、北米のメーカーは市場の需要や技術の進歩に迅速に対応できるようになり、世界市場での競争力が高まります。

CAGRが最も高い地域:

欧州は予測期間中、収益性の高い成長を維持すると予測されています。メーカー、サプライヤー、テクノロジー企業間の戦略的提携を通じて、この地域全体で電気自動車や自律走行車のような最先端技術の開発に向けた動向が明確になっています。こうした提携により、専門知識やリソースの共有が促進され、地域全体で先進的な自動車部品の開発と展開が加速しています。パートナーシップにより、企業はより広範な市場にアクセスし、互いの流通網を活用し、生産工程を合理化することができます。

無料のカスタマイズサービス:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場企業の包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 製品分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の自動車部品市場:製品タイプ別

- ボディとシャーシ

- 冷却システム

- エンジン部品

- サスペンションとブレーキ

第6章 世界の自動車部品市場:車両タイプ別

- 小型商用車

- 乗用車

- 三輪車

- 二輪車

第7章 世界の自動車部品市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東・アフリカ

第8章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第9章 企業プロファイリング

- Bosch Automotive Steering GmbH

- Continental AG

- Delphi Technologies

- Denso Corporation

- Infineon Technologies AG

- Magna International Inc

- Mahle GmbH

- Robert Bosch GmbH

- Sumitomo Electric Industries

- Visteon Corporation

- Yazaki Corporation

List of Tables

- Table 1 Global Automotive Components Market Outlook, By Region (2022-2030) ($MN)

- Table 2 Global Automotive Components Market Outlook, By Product Type (2022-2030) ($MN)

- Table 3 Global Automotive Components Market Outlook, By Body & Chassis (2022-2030) ($MN)

- Table 4 Global Automotive Components Market Outlook, By Cooling System (2022-2030) ($MN)

- Table 5 Global Automotive Components Market Outlook, By Engine Components (2022-2030) ($MN)

- Table 6 Global Automotive Components Market Outlook, By Suspension & Braking (2022-2030) ($MN)

- Table 7 Global Automotive Components Market Outlook, By Vehicle Type (2022-2030) ($MN)

- Table 8 Global Automotive Components Market Outlook, By Light Commercial Vehicles (2022-2030) ($MN)

- Table 9 Global Automotive Components Market Outlook, By Passenger Cars (2022-2030) ($MN)

- Table 10 Global Automotive Components Market Outlook, By Three-Wheelers (2022-2030) ($MN)

- Table 11 Global Automotive Components Market Outlook, By Two-Wheelers (2022-2030) ($MN)

- Table 12 North America Automotive Components Market Outlook, By Country (2022-2030) ($MN)

- Table 13 North America Automotive Components Market Outlook, By Product Type (2022-2030) ($MN)

- Table 14 North America Automotive Components Market Outlook, By Body & Chassis (2022-2030) ($MN)

- Table 15 North America Automotive Components Market Outlook, By Cooling System (2022-2030) ($MN)

- Table 16 North America Automotive Components Market Outlook, By Engine Components (2022-2030) ($MN)

- Table 17 North America Automotive Components Market Outlook, By Suspension & Braking (2022-2030) ($MN)

- Table 18 North America Automotive Components Market Outlook, By Vehicle Type (2022-2030) ($MN)

- Table 19 North America Automotive Components Market Outlook, By Light Commercial Vehicles (2022-2030) ($MN)

- Table 20 North America Automotive Components Market Outlook, By Passenger Cars (2022-2030) ($MN)

- Table 21 North America Automotive Components Market Outlook, By Three-Wheelers (2022-2030) ($MN)

- Table 22 North America Automotive Components Market Outlook, By Two-Wheelers (2022-2030) ($MN)

- Table 23 Europe Automotive Components Market Outlook, By Country (2022-2030) ($MN)

- Table 24 Europe Automotive Components Market Outlook, By Product Type (2022-2030) ($MN)

- Table 25 Europe Automotive Components Market Outlook, By Body & Chassis (2022-2030) ($MN)

- Table 26 Europe Automotive Components Market Outlook, By Cooling System (2022-2030) ($MN)

- Table 27 Europe Automotive Components Market Outlook, By Engine Components (2022-2030) ($MN)

- Table 28 Europe Automotive Components Market Outlook, By Suspension & Braking (2022-2030) ($MN)

- Table 29 Europe Automotive Components Market Outlook, By Vehicle Type (2022-2030) ($MN)

- Table 30 Europe Automotive Components Market Outlook, By Light Commercial Vehicles (2022-2030) ($MN)

- Table 31 Europe Automotive Components Market Outlook, By Passenger Cars (2022-2030) ($MN)

- Table 32 Europe Automotive Components Market Outlook, By Three-Wheelers (2022-2030) ($MN)

- Table 33 Europe Automotive Components Market Outlook, By Two-Wheelers (2022-2030) ($MN)

- Table 34 Asia Pacific Automotive Components Market Outlook, By Country (2022-2030) ($MN)

- Table 35 Asia Pacific Automotive Components Market Outlook, By Product Type (2022-2030) ($MN)

- Table 36 Asia Pacific Automotive Components Market Outlook, By Body & Chassis (2022-2030) ($MN)

- Table 37 Asia Pacific Automotive Components Market Outlook, By Cooling System (2022-2030) ($MN)

- Table 38 Asia Pacific Automotive Components Market Outlook, By Engine Components (2022-2030) ($MN)

- Table 39 Asia Pacific Automotive Components Market Outlook, By Suspension & Braking (2022-2030) ($MN)

- Table 40 Asia Pacific Automotive Components Market Outlook, By Vehicle Type (2022-2030) ($MN)

- Table 41 Asia Pacific Automotive Components Market Outlook, By Light Commercial Vehicles (2022-2030) ($MN)

- Table 42 Asia Pacific Automotive Components Market Outlook, By Passenger Cars (2022-2030) ($MN)

- Table 43 Asia Pacific Automotive Components Market Outlook, By Three-Wheelers (2022-2030) ($MN)

- Table 44 Asia Pacific Automotive Components Market Outlook, By Two-Wheelers (2022-2030) ($MN)

- Table 45 South America Automotive Components Market Outlook, By Country (2022-2030) ($MN)

- Table 46 South America Automotive Components Market Outlook, By Product Type (2022-2030) ($MN)

- Table 47 South America Automotive Components Market Outlook, By Body & Chassis (2022-2030) ($MN)

- Table 48 South America Automotive Components Market Outlook, By Cooling System (2022-2030) ($MN)

- Table 49 South America Automotive Components Market Outlook, By Engine Components (2022-2030) ($MN)

- Table 50 South America Automotive Components Market Outlook, By Suspension & Braking (2022-2030) ($MN)

- Table 51 South America Automotive Components Market Outlook, By Vehicle Type (2022-2030) ($MN)

- Table 52 South America Automotive Components Market Outlook, By Light Commercial Vehicles (2022-2030) ($MN)

- Table 53 South America Automotive Components Market Outlook, By Passenger Cars (2022-2030) ($MN)

- Table 54 South America Automotive Components Market Outlook, By Three-Wheelers (2022-2030) ($MN)

- Table 55 South America Automotive Components Market Outlook, By Two-Wheelers (2022-2030) ($MN)

- Table 56 Middle East & Africa Automotive Components Market Outlook, By Country (2022-2030) ($MN)

- Table 57 Middle East & Africa Automotive Components Market Outlook, By Product Type (2022-2030) ($MN)

- Table 58 Middle East & Africa Automotive Components Market Outlook, By Body & Chassis (2022-2030) ($MN)

- Table 59 Middle East & Africa Automotive Components Market Outlook, By Cooling System (2022-2030) ($MN)

- Table 60 Middle East & Africa Automotive Components Market Outlook, By Engine Components (2022-2030) ($MN)

- Table 61 Middle East & Africa Automotive Components Market Outlook, By Suspension & Braking (2022-2030) ($MN)

- Table 62 Middle East & Africa Automotive Components Market Outlook, By Vehicle Type (2022-2030) ($MN)

- Table 63 Middle East & Africa Automotive Components Market Outlook, By Light Commercial Vehicles (2022-2030) ($MN)

- Table 64 Middle East & Africa Automotive Components Market Outlook, By Passenger Cars (2022-2030) ($MN)

- Table 65 Middle East & Africa Automotive Components Market Outlook, By Three-Wheelers (2022-2030) ($MN)

- Table 66 Middle East & Africa Automotive Components Market Outlook, By Two-Wheelers (2022-2030) ($MN)

According to Stratistics MRC, the Global Automotive Components Market is accounted for $2,111.85 billion in 2024 and is expected to reach $3,259.22 billion by 2030 growing at a CAGR of 7.5% during the forecast period. Automotive components refer to the essential parts that make up a vehicle, ensuring its functionality, safety, and performance. These components encompass a wide range of parts, from the engine and transmission systems to the braking, steering, and suspension systems. Each component plays a crucial role in the overall operation and integrity of the vehicle. Automotive components are integral to the functionality, safety, and performance of vehicles. From the engine and transmission to the smallest electrical sensors, each part plays a crucial role. Engines, typically powered by gasoline or diesel, convert fuel into mechanical energy, propelling the vehicle.

Market Dynamics:

Driver:

Environmental and sustainability trends

Environmental and sustainability trends are significantly influencing the automotive components industry by driving innovation towards more eco-friendly and efficient solutions. Automakers and component manufacturers are increasingly adopting practices that reduce carbon footprints, such as using lightweight materials to improve fuel efficiency, developing electric and hybrid vehicle technologies, and implementing recycling programs for end-of-life vehicles. These trends are reshaping the design and production processes of automotive components

Restraint:

Fluctuations in raw material prices

Fluctuations in raw material prices pose significant challenges for the automotive components industry. As raw materials account for a substantial portion of production costs, sudden price increases can disrupt cost projections and profitability. This volatility affects manufacturers at various stages: from planning and procurement to pricing and inventory management. Automotive components require specific materials that may have limited suppliers, further exacerbating the impact of price fluctuations. To mitigate these risks, companies often resort to hedging strategies or long-term contracts with suppliers, but these measures are not foolproof against sharp price spikes or unexpected supply chain disruptions. Consequently, such instability can hinder investment in innovation and technology, impacting product development and quality.

Opportunity:

Advancement of self-driving technology

The advancement of self-driving technology is profoundly transforming automotive components by demanding higher levels of precision, reliability, and integration. Traditional mechanical systems are being augmented or replaced by sophisticated electronic and sensor-based systems that enable vehicles to perceive and respond to their environment autonomously. Key components such as sensors (like LiDAR, radar, and cameras), actuators, and computing units have become pivotal in enabling vehicles to navigate, make decisions, and communicate with other vehicles and infrastructure in real-time. This evolution is driving innovation across the automotive industry, fostering collaborations between traditional automakers, tech companies, and suppliers specializing in electronics and software.

Threat:

Intellectual property rights

Intellectual property rights (IPR) can pose challenges to the automotive components industry due to their potential to restrict innovation and competition. While IPR protects the creations and inventions of companies, including technologies and designs crucial for automotive components, it can also lead to barriers that stifle smaller manufacturers or startups from entering the market. For instance, patent thickets, where numerous patents cover overlapping technologies, can increase legal complexities and costs for companies seeking to develop new automotive components. However, the lengthy process of obtaining and enforcing patents can delay the introduction of new products to the market, slowing down innovation.

Covid-19 Impact:

The COVID-19 pandemic significantly impacted the automotive components sector. Initially, widespread lockdowns and supply chain disruptions disrupted production schedules across the globe, leading to shortages of essential components such as semiconductors and electronics. This not only slowed down vehicle manufacturing but also resulted in increased costs due to higher demand and limited supply. Fluctuating consumer demand and financial uncertainties forced automotive manufacturers to recalibrate their production plans and inventory management strategies.

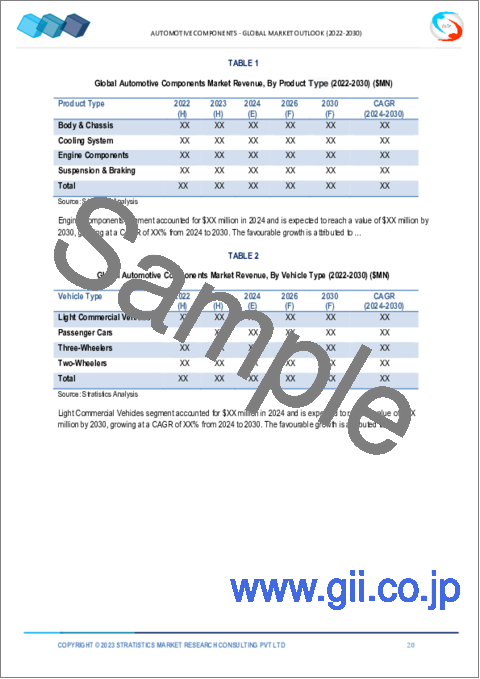

The Cooling System segment is expected to be the largest during the forecast period

Cooling System segment is expected to be the largest during the forecast period by regulating engine temperature and ensuring optimal performance and longevity. Comprising various components such as radiators, coolant hoses, water pumps, and thermostats, this system effectively manages heat dissipation from the engine to maintain operational efficiency. Advanced materials and design innovations continuously improve these components, enhancing their durability, efficiency and environmental friendliness.

The Passenger Cars segment is expected to have the highest CAGR during the forecast period

Passenger Cars segment is expected to have the highest CAGR during the forecast period. As consumer demand for efficiency, safety, and comfort increases, manufacturers of automotive components are compelled to innovate. This segment specifically influences the development of cutting-edge technologies such as electric propulsion systems, advanced safety features like autonomous driving capabilities, and enhanced infotainment systems. Engineers and designers focus on integrating lightweight materials, efficient engines, and smart connectivity solutions tailored for passenger vehicles.

Region with largest share:

North America region commanded the largest share of the market during the extrapolated period. Upgraded infrastructure includes modernized manufacturing facilities, efficient logistics networks, and advanced research and development centers across the region. These regional developments enable quicker production cycles, enhanced quality control and the ability to adopt cutting-edge technologies such as automation and AI in manufacturing processes. Moreover, improved infrastructure supports just-in-time supply chains, reducing lead times and costs associated with transportation and inventory management throughout the region. This fosters a competitive edge in the global market by allowing North American manufacturers to respond swiftly to market demands and technological advancements.

Region with highest CAGR:

Europe region is projected to hold profitable growth over the forecast period. Through strategic alliances between manufacturers, suppliers and technology firms, there is a clear trend towards developing cutting-edge technologies such as electric and autonomous vehicles across the region. These collaborations facilitate the sharing of expertise and resources, accelerating the development and deployment of advanced automotive components throughout the region. Partnerships enable companies to access broader markets, leverage each other's distribution networks, and streamline production processes, thereby reducing costs and improving overall product quality across the region

Key players in the market

Some of the key players in Automotive Components market include Bosch Automotive Steering GmbH, Continental AG, Delphi Technologies, Denso Corporation, Infineon Technologies AG, Magna International Inc, Mahle GmbH, Robert Bosch GmbH, Sumitomo Electric Industries, Visteon Corporation and Yazaki Corporation.

Key Developments:

In February 2024, AEQUITA SE & Co. KGaA, a Munich-based industrial conglomerate, has formally agreed to purchase the Brake Components division from Robert Bosch GmbH. This acquisition encompasses Buderus Guss GmbH and Robert Bosch Lollar Guss GmbH, highlighting AEQUITA's commitment to enhancing its automotive sector capabilities. The Brake Components business, renowned for its coated high-performance brake discs, serves prestigious international OEMs and is supported by approximately 900 employees across three German locations.

In December 2022, Sumitomo Invests MAD 2 Billion in Nine Automotive Projects in Morocco. Rabat - Japanese company Sumitomo Electric Industries has signed an agreement with Morocco's Ministry of Industry and Trade to invest nearly MAD 2 billion ($190 million) in Morocco's automotive ecosystem.

Product Types Covered:

- Body & Chassis

- Cooling System

- Engine Components

- Suspension & Braking

Vehicle Types Covered:

- Light Commercial Vehicles

- Passenger Cars

- Three-Wheelers

- Two-Wheelers

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2022, 2023, 2024, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Product Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Automotive Components Market, By Product Type

- 5.1 Introduction

- 5.2 Body & Chassis

- 5.3 Cooling System

- 5.4 Engine Components

- 5.5 Suspension & Braking

6 Global Automotive Components Market, By Vehicle Type

- 6.1 Introduction

- 6.2 Light Commercial Vehicles

- 6.3 Passenger Cars

- 6.4 Three-Wheelers

- 6.5 Two-Wheelers

7 Global Automotive Components Market, By Geography

- 7.1 Introduction

- 7.2 North America

- 7.2.1 US

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 Italy

- 7.3.4 France

- 7.3.5 Spain

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 Japan

- 7.4.2 China

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 New Zealand

- 7.4.6 South Korea

- 7.4.7 Rest of Asia Pacific

- 7.5 South America

- 7.5.1 Argentina

- 7.5.2 Brazil

- 7.5.3 Chile

- 7.5.4 Rest of South America

- 7.6 Middle East & Africa

- 7.6.1 Saudi Arabia

- 7.6.2 UAE

- 7.6.3 Qatar

- 7.6.4 South Africa

- 7.6.5 Rest of Middle East & Africa

8 Key Developments

- 8.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 8.2 Acquisitions & Mergers

- 8.3 New Product Launch

- 8.4 Expansions

- 8.5 Other Key Strategies

9 Company Profiling

- 9.1 Bosch Automotive Steering GmbH

- 9.2 Continental AG

- 9.3 Delphi Technologies

- 9.4 Denso Corporation

- 9.5 Infineon Technologies AG

- 9.6 Magna International Inc

- 9.7 Mahle GmbH

- 9.8 Robert Bosch GmbH

- 9.9 Sumitomo Electric Industries

- 9.10 Visteon Corporation

- 9.11 Yazaki Corporation