|

|

市場調査レポート

商品コード

1458397

プロバイオティクスの世界市場:製品タイプ別、成分別、エンドユーザー別、流通チャネル別、地域別 - 2029年までの予測Probiotics Market by Product Type (Functional Food & Beverages (FnB), Dietary Supplements, and Feed), Ingredient (Bacteria and Yeast), End User (Human and Animal), Distribution Channel and Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| プロバイオティクスの世界市場:製品タイプ別、成分別、エンドユーザー別、流通チャネル別、地域別 - 2029年までの予測 |

|

出版日: 2024年03月21日

発行: MarketsandMarkets

ページ情報: 英文 342 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

世界のプロバイオティクスの市場規模は、予測期間中にCAGR 8.2%で拡大し、2024年の712億米ドルから2029年までに1,057億米ドルに達すると予測されています。

栄養補助食品は、プロバイオティクスを毎日の養生法に取り入れるための、簡単で手間のかからない手段を消費者に提供します。錠剤からカプセル、チュアブルタイプまで、さまざまな形態のサプリメントがあり、これらのサプリメントは調理の必要がなく、室温で簡単に保管できるため、ペースの速い現代のライフスタイルの需要に応えています。この利便性は、腸の健康を強化するための手軽な解決策を求める多忙な人々に強く支持され、栄養補助食品サプリメントの持続的な需要を牽引しています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2024年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 検討単位 | 金額(米ドル)、数量(キロトン) |

| セグメント | 製品タイプ別、成分別、流通チャネル別、エンドユーザー別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、南米、その他の地域 |

さらに、栄養補助食品の魅力は利便性だけでなく、正確な投与機能をも包含しているため、消費者は特定の健康上の懸念に対処するためにプロバイオティクスの摂取量を調整することができます。明確なプロバイオティクス菌株を含む的を絞った製剤により、消費者は消化器系の健康を効果的に管理し、免疫機能をサポートし、さらには精神的な健康を促進することができます。栄養補助食品の分野では、プロバイオティクスとプレバイオティクスやビタミンなどの補完成分を組み合わせた個別化処方が人気を集めており、技術革新がさらに進んでいます。

さらに、チュアブル錠やタイムリリース・カプセルなどの新たな進歩は、消費者の選択肢と有効性を高め、進化するプロバイオティクス市場の中で、栄養補助食品を積極的な健康管理の要として位置づけています。

当レポートでは、世界のプロバイオティクス市場について調査し、製品タイプ別、成分別、エンドユーザー別、流通チャネル別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- マクロ経済指標

- 市場力学

第6章 業界の動向

- イントロダクション

- バリューチェーン分析

- サプライチェーン分析

- 技術分析

- 価格分析

- エコシステム分析/市場マップ

- 顧客ビジネスに影響を与える動向/混乱

- 貿易データ分析

- 特許分析

- 主な会議とイベント

- 規制状況

- ポーターのファイブフォース分析

- ケーススタディ

- 主な利害関係者と購入基準

- 投資と資金調達のシナリオ

第7章 プロバイオティクス市場、製品タイプ別

- イントロダクション

- 機能性食品・飲料

- 栄養補助食品

- 飼料

第8章 プロバイオティクス市場、成分別

- イントロダクション

- 細菌

- 酵母

第9章 プロバイオティクス市場、流通チャネル別

- イントロダクション

- ハイパーマーケット/スーパーマーケット

- 薬局/ドラッグストア

- 専門店

- オンライン

- コンビニエンスストア/小規模小売店

第10章 プロバイオティクス市場、エンドユーザー別

- イントロダクション

- 人間

- 動物

第11章 プロバイオティクス市場、地域別

- イントロダクション

- 北米

- 欧州

- アジア太平洋

- 南米

- その他の地域

第12章 競合情勢

- 概要

- セグメント別収益分析

- 市場シェア分析

- 主要参入企業の戦略/強み

- 企業価値評価と財務指標

- ブランド/製品比較

- 企業評価マトリックス:主要参入企業

- 企業評価マトリックス:スタートアップ/中小企業

- 競合シナリオと動向

第13章 企業プロファイル

- 主要参入企業

- PROBI

- NESTLE

- ADM

- DANONE

- INTERNATIONAL FLAVORS & FRAGRANCES INC.

- YAKULT HONSHA CO., LTD.

- BIOGAIA

- MORINAGA MILK INDUSTRY CO., LTD.

- MEIJI HOLDINGS CO., LTD.

- LIFEWAY FOODS, INC.

- ADISSEO

- WINCLOVE PROBIOTICS

- AB-BIOTICS, S.A.

- APSEN FARMACEUTICA

- LALLEMAND

- スタートアップ/中小企業

- ELANCO

- NEXTFOODS, INC.

- I-HEALTH, INC.

- SUJA LIFE, LLC.

- RENEW LIFE FORMULAS, LLC

- BIOHM HEALTH

- SUN GENOMICS

- UNIQUE BIOTECH LTD

- SO GOOD SO YOU

- PROTOCOL FOR LIFE BALANCE

第14章 隣接市場と関連市場

第15章 付録

According to MarketsandMarkets, the Probiotics market is projected to reach USD 105.7 billion by 2029 from USD 71.2 billion by 2024, at a CAGR of 8.2% during the forecast period in terms of value. Dietary supplements present consumers with a straightforward and hassle-free means to integrate probiotics into their daily regimen. With formats ranging from tablets to capsules and chewable, these supplements require no preparation and can be easily stored at room temperature, catering to the demands of modern, fast-paced lifestyles. This convenience factor resonates strongly with busy individuals seeking an effortless solution to bolster gut health, thereby driving sustained demand for dietary probiotic supplements.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD), Volume (KT) |

| Segments | Product type, ingredient, distribution channel, end user, and region. |

| Regions covered | North America, Europe, Asia Pacific, South America, and Rest of the World |

Moreover, the appeal of dietary supplements extends beyond convenience to encompass precise dosing capabilities, allowing consumers to tailor their probiotic intake to address specific health concerns. Through targeted formulations containing distinct probiotic strains, consumers can effectively manage digestive health, support immune function, and even promote mental well-being. The realm of dietary supplements further thrives on innovation, with personalized formulations combining probiotics with complementary ingredients such as prebiotics or vitamins gaining traction.

Additionally, emerging advancements such as chewable tablets and timed-release capsules enhance consumer choice and efficacy, positioning dietary supplements as a cornerstone of proactive health management within the evolving probiotics market landscape.

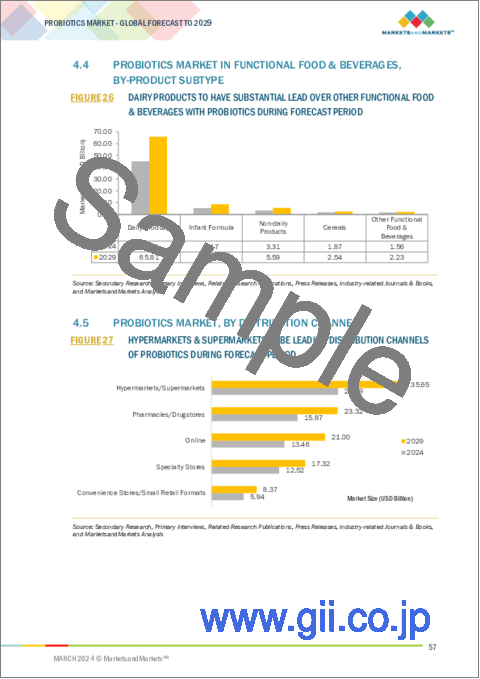

" By distribution channel, Online is estimated to grow with the highest CAGR during the forecast period."

Online channels are poised to experience significant growth in the distribution of probiotics, outpacing traditional brick-and-mortar outlets. According to data from the U.S. Food and Drug Administration (FDA) released in October 2022, online sales of dietary supplements, including probiotics, have witnessed a substantial surge, particularly among younger demographics. This trend is propelled by several factors, including the unparalleled convenience offered by online retailers, allowing consumers to browse and purchase probiotics from the comfort of their homes at any time, thus eliminating the need for physical store visits.

Moreover, e-commerce platforms boast a wider product selection compared to traditional stores, offering diverse probiotic brands, formulations, and international options, catering to varied consumer preferences. This shift towards online channels is further reinforced by government initiatives such as India's Digital India program, which aims to facilitate safe and secure online transactions for health and wellness products, including probiotics.

Furthermore, subscription models and personalized recommendations offered by online retailers enhance consumer engagement and loyalty. Consumers can opt for subscription services for recurring probiotic deliveries, ensuring a steady supply of products. Advanced e-commerce platforms leverage user data to provide personalized recommendations tailored to individual needs and health goals

"Europe will significantly contribute towards market growth during the forecast period."

Europe is positioned as a pivotal contributor to the burgeoning probiotics market throughout the forecasted period. Spearheaded by prominent industry leaders such as Probi (Sweden), Nestle (Switzerland), AB-Biotics, S.A. (Belgium), Danone (France), BioGaia (Sweden), and Adisseo (France) with headquarters and robust market presence in the region, Europe stands as a stronghold of innovation and consumer engagement. For instance, in December 2023 Eurobarometer survey conducted by the European Commission highlighted a burgeoning understanding of the gut microbiome's pivotal role in overall well-being. This heightened awareness translates into a surging demand for diverse probiotic products, spanning from digestive health aids to immune-boosting supplements and solutions for mental well-being, thus fueling market expansion.

Moreover, Europe benefits from a supportive regulatory landscape established by the European Union (EU), mandating stringent scientific substantiation of health claims associated with probiotics. This regulatory rigor ensures a level of quality and transparency within the market, bolstering consumer confidence and fostering sustained market growth.

Break-up of Primaries:

By Company Type: Tier1-40%, Tier 2-32%, Tier 3- 28%

By Designation: C-level-45%, D-level - 33%, and Others- 22%

By Region: North America - 15%, Europe - 20%, Asia Pacific - 40%, South America-12%, RoW - 13%,

Others include sales managers, territory managers, and product managers.

Leading players profiled in this report:

- Probi (Sweden)

- Nestle (Switzerland)

- ADM (US)

- Danone (France)

- International Flavors & Fragrances Inc. (US)

- Yakult Honsha Co., Ltd. (Japan)

- BioGaia (Sweden)

- MORINAGA MILK INDUSTRY CO., LTD. (Japan)

- Meiji Holdings Co., Ltd. (Japan)

- Lifeway Foods, Inc. (US)

- Adisseo (France)

- Winclove Probiotics (US)

- AB-Biotics, S.A. (Belgium)

- Apsen Farmaceutica (Brazil)

- Lallemand (Canada)

- Elanco (US)

- NextFoods, Inc.(US)

- i-Health, Inc. (US)

- Suja Life LLC. (US)

- Renew Life Formulas LLC. (US)

- BIOHM Health (US)

- Sun Genomics (US)

- Unique Biotech Ltd (India)

- So Good So You (US)

- Protocol For Life Balance (US)

The study includes an in-depth competitive analysis of these key players in the Probiotics market with their company profiles, recent developments, and key market strategies.

Research Coverage:

The report segments the Probiotics market on the basis of product type, ingredient, distribution channel, end user, and region. In terms of insights, this report has focused on various levels of analyses-the competitive landscape, end-use analysis, and company profiles, which together comprise and discuss views on the emerging & high-growth segments of the global Probiotics market, high-growth regions, countries, government initiatives, drivers, restraints, opportunities, and challenges.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall probiotics market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Health benefits associated with probiotic-fortified foods), restraints (High R&D costs for developing new probiotic strains), opportunities (Replacement of pharmaceutical agents by probiotics), and challenges (Complexities in integrating probiotics in functional foods) influencing the growth of the Probiotics market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the Probiotics market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the Probiotics market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the Probiotics market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players Probi (Sweden), Nestle (Switzerland), ADM (US), Danone (France), International Flavors & Fragrances Inc. (US), and Yakult Honsha Co., Ltd. (Japan), among others in the Probiotics market strategies. The report also helps stakeholders understand the Probiotics market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- FIGURE 1 PROBIOTICS MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 REGIONS COVERED

- FIGURE 2 PROBIOTICS MARKET SEGMENTATION, BY REGION

- 1.3.4 YEARS CONSIDERED

- FIGURE 3 STUDY PERIODS CONSIDERED

- 1.4 UNITS CONSIDERED

- 1.4.1 CURRENCY (VALUE UNIT)

- TABLE 1 USD EXCHANGE RATES CONSIDERED, 2019-2022

- 1.4.2 VOLUME UNIT

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

- 1.7 RECESSION IMPACT ANALYSIS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 4 PROBIOTICS MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- FIGURE 5 KEY DATA FROM SECONDARY SOURCES

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key primary insights

- FIGURE 6 KEY INSIGHTS FROM PRIMARY SOURCES

- 2.1.2.2 Breakdown of Primary Interviews

- FIGURE 7 BREAKDOWN OF PRIMARY INTERVIEWS, BY COMPANY TYPE, DESIGNATION, AND REGION

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- FIGURE 8 PROBIOTICS MARKET: BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Supply side analysis

- FIGURE 9 PROBIOTICS MARKET SIZE CALCULATION STEPS AND THEIR CORRESPONDING SOURCES: SUPPLY SIDE

- FIGURE 10 PROBIOTICS MARKET: TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- FIGURE 11 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 RESEARCH LIMITATIONS

- FIGURE 12 RESEARCH LIMITATIONS & ASSOCIATED RISKS

- 2.6 RECESSION IMPACT ON PROBIOTICS MARKET

- 2.6.1 RECESSION MACROECONOMIC INDICATORS

- FIGURE 13 INDICATORS OF RECESSION

- FIGURE 14 GLOBAL INFLATION RATE, 2011-2022

- FIGURE 15 GLOBAL GDP, 2011-2022 (USD TRILLION)

- FIGURE 16 RECESSION INDICATORS AND THEIR IMPACT ON PROBIOTICS MARKET

- FIGURE 17 PROBIOTICS MARKET: EARLIER FORECAST VS RECESSION IMPACT FORECAST, 2024

3 EXECUTIVE SUMMARY

- TABLE 2 PROBIOTICS MARKET SNAPSHOT, 2024 VS. 2029

- FIGURE 18 PROBIOTICS MARKET, BY INGREDIENT, 2024 VS. 2029 (USD BILLION)

- FIGURE 19 PROBIOTICS MARKET, BY PRODUCT TYPE, 2024 VS. 2029 (USD BILLION)

- FIGURE 20 PROBIOTICS MARKET, BY END USER, 2024 VS. 2029 (USD BILLION)

- FIGURE 21 PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL, 2024 VS. 2029 (USD BILLION)

- FIGURE 22 PROBIOTICS MARKET SHARE (VALUE), BY REGION, 2023

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES IN PROBIOTICS MARKET

- FIGURE 23 HEALTH BENEFITS ASSOCIATED WITH PROBIOTIC-FORTIFIED FOODS & BEVERAGES TO PROPEL MARKET

- 4.2 ASIA PACIFIC: PROBIOTICS MARKET, BY PRODUCT TYPE AND COUNTRY

- FIGURE 24 CHINA AND FUNCTIONAL FOOD & BEVERAGES TO ACCOUNT FOR LARGEST SEGMENTAL SHARES IN ASIA PACIFIC PROBIOTICS MARKET IN 2023

- 4.3 PROBIOTICS MARKET, BY PRODUCT TYPE

- FIGURE 25 FUNCTIONAL FOOD & BEVERAGES SEGMENT TO DOMINATE AMONG PROBIOTIC PRODUCT TYPES IN MARKET DURING FORECAST PERIOD

- 4.4 PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY-PRODUCT SUBTYPE

- FIGURE 26 DAIRY PRODUCTS TO HAVE SUBSTANTIAL LEAD OVER OTHER FUNCTIONAL FOOD & BEVERAGES WITH PROBIOTICS DURING FORECAST PERIOD

- 4.5 PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL

- FIGURE 27 HYPERMARKETS & SUPERMARKETS TO BE LEADING DISTRIBUTION CHANNELS OF PROBIOTICS DURING FORECAST PERIOD

- 4.6 PROBIOTICS MARKET, BY END USER

- FIGURE 28 HUMAN END USE TO COMMAND LION'S SHARE OVER ANIMAL END USE OF PROBIOTICS DURING STUDY PERIOD

- 4.7 PROBIOTICS MARKET, BY INGREDIENT

- FIGURE 29 BACTERIAL PROBIOTICS TO DOMINATE MARKET DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INCREASE IN RETAIL SALES

- FIGURE 30 US: RETAIL AND FOOD SERVICE SALES, 2016-2022 (USD BILLION)

- 5.2.2 GROWTH OPPORTUNITIES IN DEVELOPING REGIONS SUCH AS ASIA PACIFIC AND SOUTH AMERICA

- FIGURE 31 ASIA: ANNUAL GDP GROWTH RATE, BY COUNTRY, 2022

- 5.3 MARKET DYNAMICS

- FIGURE 32 MARKET DYNAMICS

- 5.3.1 DRIVERS

- 5.3.1.1 Rise in awareness on health benefits associated with probiotic-fortified foods

- 5.3.1.2 Participation of international bodies in R&D of probiotic products

- 5.3.1.3 Technological advancements in probiotic products

- 5.3.2 RESTRAINTS

- 5.3.2.1 High R&D costs for developing new probiotic strains

- 5.3.2.2 Instances of allergic reactions to some probiotic supplements

- 5.3.2.3 Stress factors affecting probiotic efficacy

- 5.3.3 OPPORTUNITIES

- 5.3.3.1 Ban on use of Antibiotic Growth Promoters (AGPs) in feed in EU

- 5.3.3.2 Replacement of pharmaceutical agents by probiotics

- 5.3.3.3 Use of yeast probiotics as antibiotics or growth promoters

- 5.3.4 CHALLENGES

- 5.3.4.1 Complexities in integrating probiotics in functional foods

- 5.3.4.2 Intolerance of probiotics to stomach acid and bile

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 VALUE CHAIN ANALYSIS

- FIGURE 33 VALUE CHAIN ANALYSIS OF PROBIOTICS MARKET

- 6.2.1 RESEARCH & PRODUCT DEVELOPMENT

- 6.2.2 SOURCING

- 6.2.3 PRODUCTION & PROCESSING

- 6.2.4 PACKAGING & STORAGE

- 6.2.5 DISTRIBUTION, SALES, AND MARKETING

- 6.3 SUPPLY CHAIN ANALYSIS

- FIGURE 34 SUPPLY CHAIN ANALYSIS OF PROBIOTICS MARKET

- 6.4 TECHNOLOGY ANALYSIS

- 6.4.1 KEY TECHNOLOGIES

- 6.4.1.1 Multi-layer embedding

- 6.4.1.2 Microencapsulated powder for probiotication in food products

- 6.4.2 COMPLEMENTARY TECHNOLOGY

- 6.4.2.1 Probiotics and artificial intelligence

- 6.4.1 KEY TECHNOLOGIES

- 6.5 PRICING ANALYSIS

- 6.5.1 AVERAGE SELLING PRICE TRENDS OF KEY PLAYERS, BY FUNCTIONAL FOOD & BEVERAGES

- TABLE 3 AVERAGE SELLING PRICE TRENDS OF KEY PLAYERS, BY FUNCTIONAL FOOD & BEVERAGE PRODUCT, 2024 (USD/TON)

- 6.5.2 AVERAGE SELLING PRICE TRENDS, BY PRODUCT TYPE

- FIGURE 35 AVERAGE SELLING PRICE TRENDS, BY PRODUCT TYPE, 2022-2024 (USD/TON)

- FIGURE 36 AVERAGE SELLING PRICE TRENDS, BY PRODUCT TYPE, 2021-2024 (USD/TON)

- TABLE 4 AVERAGE SELLING PRICE TRENDS FOR FUNCTIONAL FOOD & BEVERAGES, BY REGION, 2022-2024 (USD/TON)

- TABLE 5 AVERAGE SELLING PRICE TRENDS FOR DIETARY SUPPLEMENTS, BY REGION, 2022-2024 (USD/TON)

- TABLE 6 AVERAGE SELLING PRICE TRENDS FOR FEED, BY REGION, 2022-2024 (USD/TON)

- 6.6 ECOSYSTEM ANALYSIS/MARKET MAP

- 6.6.1 SUPPLY-SIDE ANALYSIS

- 6.6.2 DEMAND SIDE ANALYSIS

- FIGURE 37 PROBIOTICS MARKET MAPPING

- FIGURE 38 ECOSYSTEM MAPPING OF PROBIOTICS MARKET

- TABLE 7 PROBIOTICS MARKET: SUPPLY CHAIN (ECOSYSTEM)

- 6.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 39 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 6.8 TRADE DATA ANALYSIS

- TABLE 8 EXPORT DATA OF HS CODE 300290 FOR KEY COUNTRIES, 2021-2023 (KG)

- TABLE 9 IMPORT DATA OF HS CODE 300290 FOR KEY COUNTRIES, 2021-2023 (KG)

- 6.9 PATENT ANALYSIS

- FIGURE 40 NUMBER OF PATENTS GRANTED BETWEEN 2013 AND 2023

- FIGURE 41 TOP 10 INVENTORS WITH HIGHEST NUMBER OF PATENT DOCUMENTS

- TABLE 10 KEY PATENTS IN PROBIOTICS MARKET, 2023-2024

- 6.10 KEY CONFERENCES & EVENTS

- 6.11 REGULATORY LANDSCAPE

- 6.11.1 PERTINENT REGULATORY FACTORS

- 6.11.1.1 North america

- 6.11.1.1.1 US

- 6.11.1.1.2 Canada

- 6.11.1.2 Europe

- 6.11.1.3 Asia pacific

- 6.11.1.3.1 Japan

- 6.11.1.3.2 Australia and New Zealand

- 6.11.1.3.3 India

- 6.11.1.4 South america

- 6.11.1.4.1 Brazil

- 6.11.1.5 Row

- 6.11.1.5.1 Middle East

- 6.11.1.5.2 Africa (South Africa)

- 6.11.1.1 North america

- 6.11.2 REGULATORY BODIES, GOVERNMENT AGENCIES, & OTHER ORGANIZATIONS

- TABLE 12 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.11.1 PERTINENT REGULATORY FACTORS

- 6.12 PORTER'S FIVE FORCES ANALYSIS

- TABLE 15 PROBIOTICS MARKET: PORTER'S FIVE FORCES ANALYSIS

- 6.12.1 THREAT OF NEW ENTRANTS

- 6.12.2 THREAT OF SUBSTITUTES

- 6.12.3 BARGAINING POWER OF SUPPLIERS

- 6.12.4 BARGAINING POWER OF BUYERS

- 6.12.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.13 CASE STUDIES

- 6.13.1 ADM: PROMOTED METABOLIC HEALTH WITH BIFIDOBACTERIUM ANIMALIS SUBSP. LACTIS CECT 8145 BPL1

- 6.13.2 MAGNITUDE BIOSCIENCES AND AB BIOTEK HNH: PROBIOTIC DEVELOPMENT WITH ETHICAL AND HIGH-THROUGHPUT TESTING

- 6.14 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 42 INFLUENCE OF STAKEHOLDERS IN BUYING PROCESS FOR KEY PRODUCT TYPE

- TABLE 16 INFLUENCE OF STAKEHOLDERS IN BUYING PROCESS FOR TOP THREE PRODUCT TYPES

- 6.14.2 BUYING CRITERIA

- TABLE 17 KEY CRITERIA FOR SELECTING SUPPLIERS/VENDORS, BY PRODUCT TYPE

- FIGURE 43 KEY CRITERIA FOR SELECTING SUPPLIERS/VENDORS, BY PRODUCT TYPE

- 6.15 INVESTMENT AND FUNDING SCENARIO

- FIGURE 44 INVESTMENT AND FUNDING SCENARIO

7 PROBIOTICS MARKET, BY PRODUCT TYPE

- 7.1 INTRODUCTION

- FIGURE 45 PROBIOTICS MARKET, BY PRODUCT TYPE, 2024 VS. 2029 (USD BILLION)

- TABLE 18 PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD BILLION)

- TABLE 19 PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD BILLION)

- TABLE 20 PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (KT)

- TABLE 21 PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (KT)

- 7.2 FUNCTIONAL FOOD & BEVERAGES

- FIGURE 46 US: PREFERRED SOURCES OF PROBIOTICS CONSUMPTION, 2022

- TABLE 22 PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY REGION, 2020-2023 (USD BILLION)

- TABLE 23 PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY REGION, 2024-2029 (USD BILLION)

- TABLE 24 PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY REGION, 2020-2023 (KT)

- TABLE 25 PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY REGION, 2024-2029 (KT)

- TABLE 26 PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY PRODUCT SUBTYPE, 2020-2023 (USD BILLION)

- TABLE 27 PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY PRODUCT SUBTYPE, 2024-2029 (USD BILLION)

- 7.2.1 DAIRY PRODUCTS

- 7.2.1.1 Popularity of dairy products and high compatibility with probiotics

- 7.2.2 NONDAIRY BEVERAGES

- 7.2.2.1 Need to cater to increasing lactose-intolerant consumers

- 7.2.3 INFANT FORMULA

- 7.2.3.1 Rise in consumption of fortified infant nutrition

- 7.2.4 CEREALS

- 7.2.4.1 Rise in demand for ready-to-eat food items with changing consumer lifestyles

- 7.2.5 OTHER FUNCTIONAL FOOD & BEVERAGES

- 7.3 DIETARY SUPPLEMENTS

- TABLE 28 PROBIOTICS MARKET IN DIETARY SUPPLEMENTS, BY REGION, 2020-2023 (USD BILLION)

- TABLE 29 PROBIOTICS MARKET IN DIETARY SUPPLEMENTS, BY REGION, 2024-2029 (USD BILLION)

- TABLE 30 PROBIOTICS MARKET IN DIETARY SUPPLEMENTS, BY REGION, 2020-2023 (KT)

- TABLE 31 PROBIOTICS MARKET IN DIETARY SUPPLEMENTS, BY REGION, 2024-2029 (KT)

- TABLE 32 PROBIOTICS MARKET IN DIETARY SUPPLEMENTS, BY PRODUCT SUBTYPE, 2020-2023 (USD BILLION)

- TABLE 33 PROBIOTICS MARKET IN DIETARY SUPPLEMENTS, BY PRODUCT SUBTYPE, 2024-2029 (USD BILLION)

- 7.3.1 TABLETS

- 7.3.1.1 High shelf-life, affordability, and wide range of dosage patterns

- 7.3.2 CAPSULES

- 7.3.2.1 Rapid absorption of nutrients and highly customizable

- 7.3.3 POWDERS

- 7.3.3.1 Easy release of active ingredients and high stability

- 7.3.4 LIQUIDS

- 7.3.4.1 Easy consumption, greater homogeneity, and high absorption in bloodstreams

- 7.3.5 SOFT GELS

- 7.3.5.1 Relatively low cost and improved bioavailability

- 7.3.6 GEL CAPS

- 7.3.6.1 Pure-protein, benign oral dosage form

- 7.4 FEED

- 7.4.1 RISE IN TREND FOR PROVIDING PETS WITH HIGH-QUALITY AND HEALTHY WET AND DRY MEALS

- TABLE 34 PROBIOTICS MARKET IN FEED, BY REGION, 2020-2023 (USD BILLION)

- TABLE 35 PROBIOTICS MARKET IN FEED, BY REGION, 2024-2029 (USD BILLION)

- TABLE 36 PROBIOTICS MARKET IN FEED, BY REGION, 2020-2023 (KT)

- TABLE 37 PROBIOTICS MARKET IN FEED, BY REGION, 2024-2029 (KT)

8 PROBIOTICS MARKET, BY INGREDIENT

- 8.1 INTRODUCTION

- TABLE 38 DIVERSITY OF PROBIOTICS

- TABLE 39 HEALTH BENEFITS OF PROBIOTIC MICROORGANISMS

- FIGURE 47 PROBIOTICS MARKET, BY INGREDIENT, 2024 VS. 2029 (USD BILLION)

- TABLE 40 PROBIOTICS MARKET, BY INGREDIENT, 2020-2023 (USD BILLION)

- TABLE 41 PROBIOTICS MARKET, BY INGREDIENT, 2024-2029 (USD BILLION)

- 8.2 BACTERIA

- TABLE 42 BACTERIAL PROBIOTICS MARKET, BY REGION, 2020-2023 (USD BILLION)

- TABLE 43 BACTERIAL PROBIOTICS MARKET, BY REGION, 2024-2029 (USD BILLION)

- TABLE 44 BACTERIAL PROBIOTICS MARKET, BY TYPE, 2020-2023 (USD BILLION)

- TABLE 45 BACTERIAL PROBIOTICS MARKET, BY TYPE, 2024-2029 (USD BILLION)

- 8.2.1 LACTOBACILLI

- 8.2.1.1 Lactobacillus acidophilus

- 8.2.1.1.1 Rise in consumption of fermented foods, cheese, and yogurt

- 8.2.1.2 Lactobacillus rhamnosus

- 8.2.1.2.1 Ability to endure harsh gut conditions and reduced risk of antibiotic-associated intestinal symptoms

- 8.2.1.3 Lactobacillus casei

- 8.2.1.3.1 Broad-spectrum action against diseases caused by gastrointestinal pathogenic bacteria

- 8.2.1.4 Lactobacillus reuteri

- 8.2.1.4.1 Opportunities in preventive and therapeutic avenues against inflammatory diseases

- 8.2.1.1 Lactobacillus acidophilus

- 8.2.2 BIFIDOBACTERIUM

- 8.2.2.1 Benefits against chronic ailments, especially in infant gut health

- 8.2.3 STREPTOCOCCUS THERMOPHILUS

- 8.2.3.1 Growing application of Streptococcus thermophilus in food and feed industries

- 8.3 YEAST

- TABLE 46 YEAST-BASED PROBIOTICS MARKET, BY REGION, 2020-2023 (USD BILLION)

- TABLE 47 YEAST-BASED PROBIOTICS MARKET, BY REGION, 2024-2029 (USD BILLION)

- TABLE 48 YEAST-BASED PROBIOTICS MARKET, BY TYPE, 2020-2023 (USD BILLION)

- TABLE 49 YEAST-BASED PROBIOTICS MARKET, BY TYPE, 2024-2029 (USD BILLION)

- TABLE 50 BENEFICIAL EFFECTS OF YEAST

- 8.3.1 SACCHAROMYCES BOULARDII

- 8.3.1.1 GI stress-resistance key in maintaining gut flora balance

- 8.3.2 OTHER YEASTS

9 PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL

- 9.1 INTRODUCTION

- FIGURE 48 PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL, 2024 VS. 2029 (USD BILLION)

- TABLE 51 PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL, 2020-2023 (USD BILLION)

- TABLE 52 PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL, 2024-2029 (USD BILLION)

- 9.2 HYPERMARKETS/SUPERMARKETS

- 9.2.1 EXPANSION OF SUPERMARKETS IN ASIA PACIFIC

- TABLE 53 PROBIOTICS MARKET IN HYPERMARKETS/SUPERMARKETS, BY REGION, 2020-2023 (USD BILLION)

- TABLE 54 PROBIOTICS MARKET IN HYPERMARKETS/SUPERMARKETS, BY REGION, 2024-2029 (USD BILLION)

- 9.3 PHARMACIES/DRUGSTORES

- 9.3.1 RISE IN AWARENESS FOR PROBIOTIC SUPPLEMENTS IN DEVELOPED COUNTRIES TO POPULARIZE PHARMACIES

- TABLE 55 PROBIOTICS MARKET IN PHARMACIES/DRUGSTORES, BY REGION, 2020-2023 (USD BILLION)

- TABLE 56 PROBIOTICS MARKET IN PHARMACIES/DRUGSTORES, BY REGION, 2024-2029 (USD BILLION)

- 9.4 SPECIALTY STORES

- 9.4.1 PROBIOTIC SALES FUELED BY PROPER STORAGE AND TRANSPARENT LABELING

- TABLE 57 PROBIOTICS MARKET IN SPECIALTY STORES, BY REGION, 2020-2023 (USD BILLION)

- TABLE 58 PROBIOTICS MARKET IN SPECIALTY STORES, BY REGION, 2024-2029 (USD BILLION)

- 9.5 ONLINE

- 9.5.1 ONLINE SALES SURGE DUE TO CONVENIENCE, HEALTH FOCUS, AND STRONG BRAND LOYALTY AMONG CONSUMERS

- TABLE 59 PROBIOTICS MARKET IN ONLINE CHANNELS, BY REGION, 2020-2023 (USD BILLION)

- TABLE 60 PROBIOTICS MARKET IN ONLINE CHANNELS, BY REGION, 2024-2029 (USD BILLION)

- 9.6 CONVENIENCE STORES/SMALL RETAIL FORMATS

- 9.6.1 EASY ACCESS FOR CONSUMERS ENCOURAGING PURCHASE

- TABLE 61 PROBIOTICS MARKET IN CONVENIENCE STORES/SMALL RETAIL FORMATS, BY REGION, 2020-2023 (USD BILLION)

- TABLE 62 PROBIOTICS MARKET IN CONVENIENCE STORES/SMALL RETAIL FORMATS, BY REGION, 2024-2029 (USD BILLION)

10 PROBIOTICS MARKET, BY END USER

- 10.1 INTRODUCTION

- FIGURE 49 HUMAN CONSUMPTION TO DOMINATE MARKET FROM 2024 TO 2029 (USD BILLION)

- TABLE 63 PROBIOTICS MARKET, BY END USER, 2020-2023 (USD BILLION)

- TABLE 64 PROBIOTICS MARKET, BY END USER, 2024-2029 (USD BILLION)

- 10.2 HUMAN

- 10.2.1 RISING TREND OF CONSUMING FUNCTIONAL FOODS DUE TO HEALTH CONSCIOUSNESS

- FIGURE 50 FREQUENCY OF PROBIOTIC CONSUMPTION AMONG USERS

- TABLE 65 PROBIOTICS MARKET FOR HUMAN USE, BY REGION, 2020-2023 (USD BILLION)

- TABLE 66 PROBIOTICS MARKET FOR HUMAN USE, BY REGION, 2024-2029 (USD BILLION)

- 10.3 ANIMAL

- 10.3.1 BAN ON SYNTHETIC ANTIBIOTICS TO BOOST MARKET IN FEED

- TABLE 67 BENEFITS ASSOCIATED WITH ADMINISTRATION OF PROBIOTICS IN ANIMAL FEED

- TABLE 68 PROBIOTICS MARKET FOR ANIMAL USE, BY REGION, 2020-2023 (USD BILLION)

- TABLE 69 PROBIOTICS MARKET FOR ANIMAL USE, BY REGION, 2024-2029 (USD BILLION)

11 PROBIOTICS MARKET, BY REGION

- 11.1 INTRODUCTION

- FIGURE 51 RAPIDLY GROWING MARKETS TO EMERGE AS NEW HOT SPOTS

- TABLE 70 PROBIOTICS MARKET, BY REGION, 2020-2023 (USD BILLION)

- TABLE 71 PROBIOTICS MARKET, BY REGION, 2024-2029 (USD BILLION)

- TABLE 72 PROBIOTICS MARKET, BY REGION, 2020-2023 (KT)

- TABLE 73 PROBIOTICS MARKET, BY REGION, 2024-2029 (KT)

- 11.2 NORTH AMERICA

- 11.2.1 NORTH AMERICA: RECESSION IMPACT ANALYSIS

- FIGURE 52 NORTH AMERICA: INFLATION DATA, BY KEY COUNTRY, 2017-2022

- FIGURE 53 NORTH AMERICA: RECESSION IMPACT ANALYSIS

- TABLE 74 NORTH AMERICA: PROBIOTICS MARKET, BY COUNTRY, 2020-2023 (USD BILLION)

- TABLE 75 NORTH AMERICA: PROBIOTICS MARKET, BY COUNTRY, 2024-2029 (USD BILLION)

- TABLE 76 NORTH AMERICA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD BILLION)

- TABLE 77 NORTH AMERICA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD BILLION)

- TABLE 78 NORTH AMERICA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (KT)

- TABLE 79 NORTH AMERICA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (KT)

- TABLE 80 NORTH AMERICA: PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY PRODUCT SUBTYPE, 2020-2023 (USD BILLION)

- TABLE 81 NORTH AMERICA: PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY PRODUCT SUBTYPE, 2024-2029 (USD BILLION)

- TABLE 82 NORTH AMERICA: PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL, 2020-2023 (USD BILLION)

- TABLE 83 NORTH AMERICA: PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL, 2024-2029 (USD BILLION)

- TABLE 84 NORTH AMERICA: PROBIOTICS MARKET, BY END USER, 2020-2023 (USD BILLION)

- TABLE 85 NORTH AMERICA: PROBIOTICS MARKET, BY END USER, 2024-2029 (USD BILLION)

- TABLE 86 NORTH AMERICA: PROBIOTICS MARKET, BY INGREDIENT, 2020-2023 (USD BILLION)

- TABLE 87 NORTH AMERICA: PROBIOTICS MARKET, BY INGREDIENT, 2024-2029 (USD BILLION)

- 11.2.2 US

- 11.2.2.1 Rise in digestive health awareness

- TABLE 88 US: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 89 US: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.2.3 CANADA

- 11.2.3.1 Demand for high-quality and innovative feed products to accelerate probiotics production and consumption

- TABLE 90 CANADA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 91 CANADA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.2.4 MEXICO

- 11.2.4.1 Consumer inclination toward healthy diets

- TABLE 92 MEXICO: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 93 MEXICO: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.3 EUROPE

- FIGURE 54 EUROPE: MARKET SNAPSHOT

- 11.3.1 EUROPE: RECESSION IMPACT ANALYSIS

- FIGURE 55 EUROPE: INFLATION DATA, BY KEY COUNTRY, 2017-2022

- FIGURE 56 EUROPE: RECESSION IMPACT ANALYSIS

- TABLE 94 EUROPE: PROBIOTICS MARKET, BY COUNTRY, 2020-2023 (USD BILLION)

- TABLE 95 EUROPE: PROBIOTICS MARKET, BY COUNTRY, 2024-2029 (USD BILLION)

- TABLE 96 EUROPE: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD BILLION)

- TABLE 97 EUROPE: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD BILLION)

- TABLE 98 EUROPE: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (KT)

- TABLE 99 EUROPE: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (KT)

- TABLE 100 EUROPE: PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY PRODUCT SUBTYPE, 2020-2023 (USD BILLION)

- TABLE 101 EUROPE: PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY PRODUCT SUBTYPE, 2024-2029 (USD BILLION)

- TABLE 102 EUROPE: PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL, 2020-2023 (USD BILLION)

- TABLE 103 EUROPE: PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL, 2024-2029 (USD BILLION)

- TABLE 104 EUROPE: PROBIOTICS MARKET, BY END USER, 2020-2023 (USD BILLION)

- TABLE 105 EUROPE: PROBIOTICS MARKET, BY END USER, 2024-2029 (USD BILLION)

- TABLE 106 EUROPE: PROBIOTICS MARKET, BY INGREDIENT, 2020-2023 (USD BILLION)

- TABLE 107 EUROPE: PROBIOTICS MARKET, BY INGREDIENT, 2024-2029 (USD BILLION)

- 11.3.2 RUSSIA

- 11.3.2.1 Highly regulated probiotic landscape

- TABLE 108 RUSSIA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 109 RUSSIA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.3.3 UK

- 11.3.3.1 Shift toward natural foods that support digestive health

- TABLE 110 UK: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 111 UK: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.3.4 ITALY

- 11.3.4.1 Preference for cheese and awareness about health benefits of probiotics

- TABLE 112 ITALY: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 113 ITALY: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.3.5 GERMANY

- 11.3.5.1 Preference for probiotic yogurts and yogurt drinks and opportunity for use in poultry feed

- TABLE 114 GERMANY: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 115 GERMANY: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.3.6 SPAIN

- 11.3.6.1 Growing interest in health and wellness products among consumers to spur investment by companies

- TABLE 116 SPAIN: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 117 SPAIN: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.3.7 REST OF EUROPE

- TABLE 118 REST OF EUROPE: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 119 REST OF EUROPE: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.4 ASIA PACIFIC

- FIGURE 57 ASIA PACIFIC: MARKET SNAPSHOT

- 11.4.1 ASIA PACIFIC: RECESSION IMPACT ANALYSIS

- FIGURE 58 ASIA PACIFIC: INFLATION DATA, BY KEY COUNTRY, 2017-2022

- FIGURE 59 ASIA PACIFIC: RECESSION IMPACT ANALYSIS

- TABLE 120 ASIA PACIFIC: PROBIOTICS MARKET, BY COUNTRY/REGION, 2020-2023 (USD BILLION)

- TABLE 121 ASIA PACIFIC: PROBIOTICS MARKET, BY COUNTRY/REGION, 2024-2029 (USD BILLION)

- TABLE 122 ASIA PACIFIC: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD BILLION)

- TABLE 123 ASIA PACIFIC: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD BILLION)

- TABLE 124 ASIA PACIFIC: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (KT)

- TABLE 125 ASIA PACIFIC: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (KT)

- TABLE 126 ASIA PACIFIC: PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY PRODUCT SUBTYPE, 2020-2023 (USD BILLION)

- TABLE 127 ASIA PACIFIC: PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY PRODUCT SUBTYPE, 2024-2029 (USD BILLION)

- TABLE 128 ASIA PACIFIC: PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL, 2020-2023 (USD BILLION)

- TABLE 129 ASIA PACIFIC: PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL, 2024-2029 (USD BILLION)

- TABLE 130 ASIA PACIFIC: PROBIOTICS MARKET, BY END USER, 2020-2023 (USD BILLION)

- TABLE 131 ASIA PACIFIC: PROBIOTICS MARKET, BY END USER, 2024-2029 (USD BILLION)

- TABLE 132 ASIA PACIFIC: PROBIOTICS MARKET, BY INGREDIENT, 2020-2023 (USD BILLION)

- TABLE 133 ASIA PACIFIC: PROBIOTICS MARKET, BY INGREDIENT, 2024-2029 (USD BILLION)

- 11.4.2 CHINA

- 11.4.2.1 Strategic moves by players to tap high sales potential of probiotics

- TABLE 134 CHINA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 135 CHINA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.4.3 JAPAN

- 11.4.3.1 Focus on digestive well-being of aging population

- TABLE 136 JAPAN: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 137 JAPAN: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.4.4 INDIA

- 11.4.4.1 Increased focus on women's nutrition and post-COVID-19 consumer preference for functional food

- TABLE 138 INDIA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 139 INDIA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.4.5 AUSTRALIA & NEW ZEALAND

- 11.4.5.1 Aging population and consumer awareness to drive clinical trials and retail sales

- TABLE 140 AUSTRALIA & NEW ZEALAND: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 141 AUSTRALIA & NEW ZEALAND: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.4.6 REST OF ASIA PACIFIC

- TABLE 142 REST OF ASIA PACIFIC: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 143 REST OF ASIA PACIFIC: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.5 SOUTH AMERICA

- 11.5.1 SOUTH AMERICA: RECESSION IMPACT ANALYSIS

- FIGURE 60 SOUTH AMERICA: INFLATION DATA, BY COUNTRY, 2017-2022

- FIGURE 61 SOUTH AMERICA: RECESSION IMPACT ANALYSIS

- TABLE 144 SOUTH AMERICA: PROBIOTICS MARKET, BY COUNTRY, 2020-2023 (USD BILLION)

- TABLE 145 SOUTH AMERICA: PROBIOTICS MARKET, BY COUNTRY, 2024-2029 (USD BILLION)

- TABLE 146 SOUTH AMERICA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD BILLION)

- TABLE 147 SOUTH AMERICA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD BILLION)

- TABLE 148 SOUTH AMERICA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (KT)

- TABLE 149 SOUTH AMERICA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (KT)

- TABLE 150 SOUTH AMERICA: PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY PRODUCT SUBTYPE, 2020-2023 (USD BILLION)

- TABLE 151 SOUTH AMERICA: PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY PRODUCT SUBTYPE, 2024-2029 (USD BILLION)

- TABLE 152 SOUTH AMERICA: PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL, 2020-2023 (USD BILLION)

- TABLE 153 SOUTH AMERICA: PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL, 2024-2029 (USD BILLION)

- TABLE 154 SOUTH AMERICA: PROBIOTICS MARKET, BY END USER, 2020-2023 (USD BILLION)

- TABLE 155 SOUTH AMERICA: PROBIOTICS MARKET, BY END USER, 2024-2029 (USD BILLION)

- TABLE 156 SOUTH AMERICA: PROBIOTICS MARKET, BY INGREDIENT, 2020-2023 (USD BILLION)

- TABLE 157 SOUTH AMERICA: PROBIOTICS MARKET, BY INGREDIENT, 2024-2029 (USD BILLION)

- 11.5.2 BRAZIL

- 11.5.2.1 Rise in health awareness and meat exports to EU

- TABLE 158 BRAZIL: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 159 BRAZIL: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.5.3 ARGENTINA

- 11.5.3.1 Increase in industrialization of meat processing and dairy productivity

- TABLE 160 ARGENTINA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 161 ARGENTINA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.5.4 REST OF SOUTH AMERICA

- TABLE 162 REST OF SOUTH AMERICA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 163 REST OF SOUTH AMERICA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.6 REST OF THE WORLD (ROW)

- 11.6.1 ROW: RECESSION IMPACT ANALYSIS

- FIGURE 62 ROW: INFLATION DATA, BY SUBREGION, 2017-2022

- FIGURE 63 ROW: RECESSION IMPACT ANALYSIS

- TABLE 164 ROW: PROBIOTICS MARKET, BY REGION, 2020-2023 (USD BILLION)

- TABLE 165 ROW: PROBIOTICS MARKET, BY REGION, 2024-2029 (USD BILLION)

- TABLE 166 ROW: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD BILLION)

- TABLE 167 ROW: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD BILLION)

- TABLE 168 ROW: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (KT)

- TABLE 169 ROW: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (KT)

- TABLE 170 ROW: PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY PRODUCT SUBTYPE, 2020-2023 (USD BILLION)

- TABLE 171 ROW: PROBIOTICS MARKET IN FUNCTIONAL FOOD & BEVERAGES, BY PRODUCT SUBTYPE, 2024-2029 (USD BILLION)

- TABLE 172 ROW: PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL, 2020-2023 (USD BILLION)

- TABLE 173 ROW: PROBIOTICS MARKET, BY DISTRIBUTION CHANNEL, 2024-2029 (USD BILLION)

- TABLE 174 ROW: PROBIOTICS MARKET, BY END USER, 2020-2023 (USD BILLION)

- TABLE 175 ROW: PROBIOTICS MARKET, BY END USER, 2024-2029 (USD BILLION)

- TABLE 176 ROW: PROBIOTICS MARKET, BY INGREDIENT, 2020-2023 (USD BILLION)

- TABLE 177 ROW: PROBIOTICS MARKET, BY INGREDIENT, 2024-2029 (USD BILLION)

- 11.6.2 MIDDLE EAST

- 11.6.2.1 Demand for quality feed, high consumption of feed, and demand for yogurt

- TABLE 178 MIDDLE EAST: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 179 MIDDLE EAST: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- 11.6.3 AFRICA

- 11.6.3.1 Investments in pharmaceutical companies to increase with intra-African trade

- TABLE 180 AFRICA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 181 AFRICA: PROBIOTICS MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 SEGMENTAL REVENUE ANALYSIS

- FIGURE 64 SEGMENTAL REVENUE ANALYSIS OF KEY MARKET PLAYERS, 2018-2022 (USD BILLION)

- 12.3 MARKET SHARE ANALYSIS

- TABLE 182 PROBIOTICS MARKET: DEGREE OF COMPETITION (COMPETITIVE)

- 12.4 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- TABLE 183 STRATEGIES ADOPTED BY KEY PLAYERS IN PROBIOTICS MARKET

- 12.5 COMPANY VALUATION AND FINANCIAL METRICS

- FIGURE 65 PROBIOTICS MARKET: COMPANY VALUATION (USD BILLION)

- FIGURE 66 PROBIOTICS MARKET: EV/EBITDA, 2022 (USD BILLION)

- 12.6 BRAND/PRODUCT COMPARISON

- FIGURE 67 PROBIOTICS MARKET: BRAND/PRODUCT COMPARISON

- 12.6.1 DIVERSE PROBIOTIC SOLUTIONS FUELING MARKET GROWTH

- 12.6.1.1 Nestle Cerelac

- 12.6.1.2 Danone's Activia

- 12.6.1.3 Yakult

- 12.6.1.4 LG21 by Meiji Holding Inc.

- 12.6.1.5 HOWARU by IFF Health

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- FIGURE 68 PROBIOTICS MARKET: COMPANY EVALUATION MATRIX FOR KEY PLAYERS, 2023

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS

- 12.7.5.1 Overall company footprint

- FIGURE 69 PROBIOTICS MARKET: OVERALL COMPANY FOOTPRINT FOR KEY PLAYERS, 2023

- 12.7.5.2 Product type footprint

- TABLE 184 PROBIOTICS MARKET: PRODUCT TYPE FOOTPRINT FOR KEY PLAYERS, 2023

- 12.7.5.3 End user footprint

- TABLE 185 PROBIOTICS MARKET: END USER FOOTPRINT FOR KEY PLAYERS, 2023

- 12.7.5.4 Regional footprint

- TABLE 186 PROBIOTICS MARKET: REGIONAL FOOTPRINT FOR KEY PLAYERS, 2023

- 12.8 COMPANY EVALUATION MATRIX: STARTUP/SMES

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- FIGURE 70 PROBIOTICS MARKET: COMPANY EVALUATION MATRIX FOR STARTUPS/SMES, 2023

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES

- 12.8.5.1 Detailed list of key startup/smes

- TABLE 187 PROBIOTICS MARKET: KEY STARTUP/SMES, 2023

- 12.8.5.2 Competitive benchmarking of key startup/smes

- TABLE 188 PROBIOTICS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUP/SMES

- 12.9 COMPETITIVE SCENARIO AND TRENDS

- 12.9.1 PRODUCT LAUNCHES

- TABLE 189 PROBIOTICS MARKET: PRODUCT LAUNCHES, JANUARY 2019-FEBRUARY 2024

- 12.9.2 DEALS

- TABLE 190 PROBIOTICS MARKET: DEALS, JANUARY 2019-FEBRUARY 2024

- 12.9.3 OTHERS

- TABLE 191 PROBIOTICS MARKET: EXPANSIONS, JANUARY 2019-FEBRUARY 2024

- TABLE 192 PROBIOTICS MARKET: OTHERS, JANUARY 2019-FEBRUARY 2024

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

(Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats))**

- 13.1.1 PROBI

- TABLE 193 PROBI: BUSINESS OVERVIEW

- FIGURE 71 PROBI: COMPANY SNAPSHOT

- TABLE 194 PROBI: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 195 PROBI: PRODUCT LAUNCHES

- TABLE 196 PROBI: DEALS

- 13.1.2 NESTLE

- TABLE 197 NESTLE: BUSINESS OVERVIEW

- FIGURE 72 NESTLE: COMPANY SNAPSHOT

- TABLE 198 NESTLE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 199 NESTLE: PRODUCT LAUNCHES

- TABLE 200 NESTLE: DEALS

- 13.1.3 ADM

- TABLE 201 ADM: BUSINESS OVERVIEW

- FIGURE 73 ADM: COMPANY SNAPSHOT

- TABLE 202 ADM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 203 ADM: DEALS

- TABLE 204 ADM: EXPANSIONS

- 13.1.4 DANONE

- TABLE 205 DANONE: BUSINESS OVERVIEW

- FIGURE 74 DANONE: COMPANY SNAPSHOT

- TABLE 206 DANONE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 207 DANONE: PRODUCT LAUNCHES

- TABLE 208 DANONE: EXPANSIONS

- 13.1.5 INTERNATIONAL FLAVORS & FRAGRANCES INC.

- TABLE 209 INTERNATIONAL FLAVORS & FRAGRANCES INC.: BUSINESS OVERVIEW

- FIGURE 75 INTERNATIONAL FLAVORS & FRAGRANCES INC.: COMPANY SNAPSHOT

- TABLE 210 INTERNATIONAL FLAVORS & FRAGRANCES INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 211 INTERNATIONAL FLAVORS & FRAGRANCES INC.: DEALS

- TABLE 212 INTERNATIONAL FLAVORS & FRAGRANCES INC.: EXPANSIONS

- 13.1.6 YAKULT HONSHA CO., LTD.

- TABLE 213 YAKULT HONSHA CO., LTD.: BUSINESS OVERVIEW

- FIGURE 76 YAKULT HONSHA CO., LTD.: COMPANY SNAPSHOT

- TABLE 214 YAKULT HONSHA CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 215 YAKULT HONSHA CO., LTD.: PRODUCT LAUNCHES

- TABLE 216 YAKULT HONSHA CO., LTD.: DEALS

- TABLE 217 YAKULT HONSHA CO., LTD.: EXPANSIONS

- 13.1.7 BIOGAIA

- TABLE 218 BIOGAIA: BUSINESS OVERVIEW

- FIGURE 77 BIOGAIA: COMPANY SNAPSHOT

- TABLE 219 BIOGAIA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 220 BIOGAIA: PRODUCT LAUNCHES

- TABLE 221 BIOGAIA: DEALS

- TABLE 222 BIOGAIA: EXPANSIONS

- 13.1.8 MORINAGA MILK INDUSTRY CO., LTD.

- TABLE 223 MORINAGA MILK INDUSTRY CO., LTD.: BUSINESS OVERVIEW

- FIGURE 78 MORINAGA MILK INDUSTRY CO., LTD.: COMPANY SNAPSHOT

- TABLE 224 MORINAGA MILK INDUSTRY CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 225 MORINAGA MILK INDUSTRY CO., LTD.: PRODUCT LAUNCHES

- TABLE 226 MORINAGA MILK INDUSTRY CO., LTD.: OTHERS

- TABLE 227 MORINAGA MILK INDUSTRY CO., LTD.: EXPANSIONS

- 13.1.9 MEIJI HOLDINGS CO., LTD.

- TABLE 228 MEIJI HOLDINGS CO., LTD.: BUSINESS OVERVIEW

- FIGURE 79 MEIJI HOLDINGS CO., LTD.: COMPANY SNAPSHOT

- TABLE 229 MEIJI HOLDINGS CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 13.1.10 LIFEWAY FOODS, INC.

- TABLE 230 LIFEWAY FOODS, INC.: BUSINESS OVERVIEW

- FIGURE 80 LIFEWAY FOODS, INC.: COMPANY SNAPSHOT

- TABLE 231 LIFEWAY FOODS, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 232 LIFEWAY FOODS, INC.: DEALS

- 13.1.11 ADISSEO

- TABLE 233 ADISSEO: BUSINESS OVERVIEW

- FIGURE 81 ADISSEO: COMPANY SNAPSHOT

- TABLE 234 ADISSEO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 13.1.12 WINCLOVE PROBIOTICS

- TABLE 235 WINCLOVE PROBIOTICS: BUSINESS OVERVIEW

- TABLE 236 WINCLOVE PROBIOTICS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 237 WINCLOVE PROBIOTICS: DEALS

- TABLE 238 WINCLOVE PROBIOTICS: EXPANSIONS

- 13.1.13 AB-BIOTICS, S.A.

- TABLE 239 AB-BIOTICS, S.A.: BUSINESS OVERVIEW

- TABLE 240 AB-BIOTICS, S.A.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 241 AB-BIOTICS, S.A.: DEALS

- 13.1.14 APSEN FARMACEUTICA

- TABLE 242 APSEN FARMACEUTICA: BUSINESS OVERVIEW

- TABLE 243 APSEN FARMACEUTICA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 244 APSEN FARMACEUTICA: PRODUCT LAUNCHES

- TABLE 245 APSEN FARMACEUTICA: DEALS

- 13.1.15 LALLEMAND

- TABLE 246 LALLEMAND: BUSINESS OVERVIEW

- TABLE 247 LALLEMAND: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 248 LALLEMAND: DEALS

- TABLE 249 LALLEMAND: EXPANSIONS

- 13.2 STARTUP/SME PLAYERS

- 13.2.1 ELANCO

- TABLE 250 ELANCO: BUSINESS OVERVIEW

- FIGURE 82 ELANCO: COMPANY SNAPSHOT

- TABLE 251 ELANCO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 13.2.2 NEXTFOODS, INC.

- TABLE 252 NEXTFOODS, INC.: BUSINESS OVERVIEW

- TABLE 253 NEXTFOODS, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 254 NEXTFOODS, INC.: DEALS

- 13.2.3 I-HEALTH, INC.

- TABLE 255 I-HEALTH, INC.: BUSINESS OVERVIEW

- TABLE 256 I-HEALTH, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 13.2.4 SUJA LIFE, LLC.

- TABLE 257 SUJA LIFE, LLC.: BUSINESS OVERVIEW

- TABLE 258 SUJA LIFE, LLC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 259 SUJA LIFE, LLC.: DEALS

- 13.2.5 RENEW LIFE FORMULAS, LLC

- TABLE 260 RENEW LIFE FORMULAS, LLC.: BUSINESS OVERVIEW

- TABLE 261 RENEW LIFE FORMULAS, LLC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 13.2.6 BIOHM HEALTH

- TABLE 262 BIOHM HEALTH: BUSINESS OVERVIEW

- 13.2.7 SUN GENOMICS

- TABLE 263 SUN GENOMICS: BUSINESS OVERVIEW

- 13.2.8 UNIQUE BIOTECH LTD

- TABLE 264 UNIQUE BIOTECH LTD: BUSINESS OVERVIEW

- 13.2.9 SO GOOD SO YOU

- TABLE 265 SO GOOD SO YOU: BUSINESS OVERVIEW

- 13.2.10 PROTOCOL FOR LIFE BALANCE

- TABLE 266 PROTOCOL FOR LIFE BALANCE: BUSINESS OVERVIEW

- *Details on Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats) might not be captured in case of unlisted companies.

14 ADJACENT AND RELATED MARKETS

- 14.1 INTRODUCTION

- TABLE 267 ADJACENT MARKETS TO PROBIOTICS

- 14.2 RESEARCH LIMITATIONS

- 14.3 DIETARY SUPPLEMENT MARKET

- 14.3.1 MARKET DEFINITION

- 14.3.2 MARKET OVERVIEW

- TABLE 268 DIETARY SUPPLEMENTS MARKET, BY TYPE, 2018-2022 (USD MILLION)

- TABLE 269 DIETARY SUPPLEMENTS MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 14.4 BONE & JOINT HEALTH SUPPLEMENTS MARKET

- 14.4.1 MARKET DEFINITION

- 14.4.2 MARKET OVERVIEW

- TABLE 270 BONE & JOINT HEALTH SUPPLEMENTS MARKET, BY TYPE, 2017-2021 (USD MILLION)

- TABLE 271 BONE & JOINT HEALTH SUPPLEMENTS MARKET, BY TYPE, 2022-2027 (USD MILLION)

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS