|

|

市場調査レポート

商品コード

1511268

鉱山テーリング管理の世界市場、2030年までの予測:タイプ別、鉱物タイプ別、採掘方法別、用途別、エンドユーザー別、地域別Mining Tailings Management Market Forecasts to 2030 - Global Analysis By Type (Conventional Tailings, Thickened Tailings, Paste Tailings, Filter Tailings and Other Types), Mineral Type, Mining Method, Application, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 鉱山テーリング管理の世界市場、2030年までの予測:タイプ別、鉱物タイプ別、採掘方法別、用途別、エンドユーザー別、地域別 |

|

出版日: 2024年07月06日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の鉱山テーリング管理市場は2024年に171億米ドルを占め、予測期間中のCAGRは6.6%で成長し、2030年には252億米ドルに達する見込みです。

鉱山テーリング管理とは、鉱業会社が採掘作業中に発生する廃棄物を処理・処分するために使用する戦略、技術、プロセスを指します。テーリング(鉱滓)として知られるこれらの廃棄物は、粉砕された岩石、化学物質、採掘プロセスからのその他の残留物から構成されることが多いです。テーリングは環境汚染を防ぐため、安全な施設に保管しなければなりません。そのため、テーリングダムを建設したり、その他の封じ込め構造を使用したりすることが多いです。

資源効率と循環経済の重視

効率性と循環経済の原則は、鉱山テーリング管理に革命をもたらしています。センサーを使った選別やリサイクルのような先進技術によって、鉱業会社は鉱滓から貴重な鉱物を回収し、廃棄物や環境への影響を減らすことができます。水の再利用や再生可能エネルギーの統合は、資源効率をさらに高めます。循環型経済モデルは、材料の継続的な利用を促進し、かつては廃棄物とみなされていたものを貴重な資源に変えます。

技術的専門知識とインフラの限界

市場では、テーリングダムの安定性、水管理、環境影響緩和などの課題に取り組む上で、技術的専門知識が重要な役割を果たします。しかし、不十分な鉱滓貯蔵施設、時代遅れの設備、高度なモニタリング技術への限られたアクセスといったインフラの制限が、効果的な管理手法の妨げとなっています。こうしたギャップを埋めるには、鉱業における持続可能な鉱山テーリング管理のために、熟練した人材、最新のインフラ、革新的なソリューションへの投資が必要です。

金属・鉱物需要の高まり

市場では金属と鉱物の需要が急増しています。この動向は、資源採掘と環境保護における持続可能な慣行に対するニーズの高まりに後押しされています。利害関係者は、採掘廃棄物を効率的に管理し、鉱滓から貴重な物質を抽出するための革新的な技術と戦略に投資しています。このシフトは、責任ある採鉱慣行と循環型経済に対する業界の広範な焦点を反映したものであり、このセクターに大きな成長機会をもたらしています。

高い導入コスト

同市場は、導入コストの高さによる大きなハードルに直面しています。このコストには、モニタリングシステム、封じ込め構造、環境修復対策など、鉱滓処分のための高度な技術が含まれます。さらに、厳しい規制の遵守が費用をさらに増大させます。企業は、これらのソリューションの研究、開発、運用展開に多額の資金を割かなければならず、業界への参入と拡大の大きな障壁となっています。

COVID-19の影響:

COVID-19の大流行は鉱山テーリング管理市場に大きな影響を与えました。サプライチェーンの混乱、労働力不足、プロジェクトの遅延が顕著な課題でした。企業は操業停止による操業上の制約に直面し、鉱山テーリング管理戦略に影響を与えました。しかし、この危機は業界のデジタル変革を加速させ、遠隔監視と自動化ソリューションを促進しました。環境問題への懸念と規制の圧力は依然として残っており、持続可能な鉱滓処理方法の革新を促しています。

予測期間中、ペーストセグメントが最大となる見込み

予測期間中、ペーストセグメントが最大となる見込みです。従来のテーリングとは異なり、ペーストテーリングはバインダーと混合してより固い一貫性を形成し、含水量を減らして環境への影響を最小限に抑えます。この技術により、封じ込めが改善され、テーリングダム破損のリスクが低減され、安全性と長期安定性が向上します。環境への関心が高まる中、ペーストテーリングは、責任ある採鉱慣行と効率的な資源利用に向けた革新的なアプローチです。

予測期間中、再処理部門のCAGRが最も高くなると予想されます。

再処理セグメントは、予測期間中に最も高いCAGRが見込まれます。高度な技術と手法を採用することで、再処理は以前に廃棄された鉱滓から貴重な鉱物や金属を抽出することを可能にします。これは廃棄物を最小限に抑えることで環境への影響を減らすだけでなく、資源回収を通じて経済的な機会ももたらします。鉱山テーリング管理市場における再処理分野は、持続可能性の目標と資源の効率的利用に対する需要の高まりに後押しされ、大きな成長を遂げています。

最大のシェアを占める地域

予測期間中、北米が最大の市場シェアを占めると予測されます。この分野の企業は、環境への影響を最小限に抑え、操業効率を高めるために、鉱滓脱水システム、ジオポリマー技術、遠隔監視ソリューションなどの先進技術に多額の投資を行っています。不適切な鉱滓処理がもたらす長期的な影響に対する認識が高まる中、革新的で環境に優しい鉱山テーリング管理ソリューションに対する需要は、この地域全体で拡大し続けています。

CAGRが最も高い地域:

アジア太平洋地域は鉱業活動が盛んであり、環境の持続可能性への関心が高まっているため、予測期間中、CAGRが最も高くなると予測されます。同市場では、水の消費と環境汚染のリスクを低減する乾式煙突式鉱滓など、鉱山テーリング管理の革新的技術が増加しています。これらの技術は、規制を遵守し、持続可能性を向上させるために、この地域の鉱業会社で採用が進んでいます。

無料のカスタマイズサービス:

本レポートをご購読のお客様は、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレーヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 用途分析

- エンドユーザー分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の鉱山テーリング管理市場:タイプ別

- 従来型

- Thickened

- ペースト

- フィルター

- その他

第6章 世界の鉱山テーリング管理市場:鉱物タイプ別

- 金

- 銅

- 鉄鉱石

- 石炭

- 希土類元素(REE)

第7章 世界の鉱山テーリング管理市場:採掘方法別

- 露天採掘

- 地下採掘

- 砂鉱採掘

第8章 世界の鉱山テーリング管理市場:用途別

- 表面処理

- 地下処理

- 再処理

- 再生

- その他

第9章 世界の鉱山テーリング管理市場:エンドユーザー別

- 鉱業

- 建設

- エネルギー

- その他

第10章 世界の鉱山テーリング管理市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東・アフリカ

第11章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第12章 企業プロファイリング

- Vale

- BHP

- Rio Tinto

- Anglo American

- Glencore

- Freeport-McMoRan

- Newmont

- Teck Resources

- Southern Copper Corporation

- Codelco

- Hindustan Zinc Limited

- Antofagasta Minerals

- China Shenhua Energy

- Norilsk Nickel

- MMC Norilsk Nickel

- Barrick Gold

- Goldcorp

List of Tables

- Table 1 Global Mining Tailings Management Market Outlook, By Region (2022-2030) ($MN)

- Table 2 Global Mining Tailings Management Market Outlook, By Type (2022-2030) ($MN)

- Table 3 Global Mining Tailings Management Market Outlook, By Conventional Tailings (2022-2030) ($MN)

- Table 4 Global Mining Tailings Management Market Outlook, By Thickened Tailings (2022-2030) ($MN)

- Table 5 Global Mining Tailings Management Market Outlook, By Paste Tailings (2022-2030) ($MN)

- Table 6 Global Mining Tailings Management Market Outlook, By Filter Tailings (2022-2030) ($MN)

- Table 7 Global Mining Tailings Management Market Outlook, By Other Types (2022-2030) ($MN)

- Table 8 Global Mining Tailings Management Market Outlook, By Mineral Type (2022-2030) ($MN)

- Table 9 Global Mining Tailings Management Market Outlook, By Gold (2022-2030) ($MN)

- Table 10 Global Mining Tailings Management Market Outlook, By Copper (2022-2030) ($MN)

- Table 11 Global Mining Tailings Management Market Outlook, By Iron Ore (2022-2030) ($MN)

- Table 12 Global Mining Tailings Management Market Outlook, By Coal (2022-2030) ($MN)

- Table 13 Global Mining Tailings Management Market Outlook, By Rare Earth Elements (REE) (2022-2030) ($MN)

- Table 14 Global Mining Tailings Management Market Outlook, By Mining Method (2022-2030) ($MN)

- Table 15 Global Mining Tailings Management Market Outlook, By Open Pit Mining (2022-2030) ($MN)

- Table 16 Global Mining Tailings Management Market Outlook, By Underground Mining (2022-2030) ($MN)

- Table 17 Global Mining Tailings Management Market Outlook, By Placer Mining (2022-2030) ($MN)

- Table 18 Global Mining Tailings Management Market Outlook, By Application (2022-2030) ($MN)

- Table 19 Global Mining Tailings Management Market Outlook, By Surface Disposal (2022-2030) ($MN)

- Table 20 Global Mining Tailings Management Market Outlook, By Underground Disposal (2022-2030) ($MN)

- Table 21 Global Mining Tailings Management Market Outlook, By Reprocessing (2022-2030) ($MN)

- Table 22 Global Mining Tailings Management Market Outlook, By Reclamation (2022-2030) ($MN)

- Table 23 Global Mining Tailings Management Market Outlook, By Other Applications (2022-2030) ($MN)

- Table 24 Global Mining Tailings Management Market Outlook, By End User (2022-2030) ($MN)

- Table 25 Global Mining Tailings Management Market Outlook, By Mining (2022-2030) ($MN)

- Table 26 Global Mining Tailings Management Market Outlook, By Construction (2022-2030) ($MN)

- Table 27 Global Mining Tailings Management Market Outlook, By Energy (2022-2030) ($MN)

- Table 28 Global Mining Tailings Management Market Outlook, By Other End Users (2022-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Mining Tailings Management Market is accounted for $17.1 billion in 2024 and is expected to reach $25.2 billion by 2030 growing at a CAGR of 6.6% during the forecast period. Mining tailings management refers to the strategies, techniques, and processes used by mining companies to handle and dispose of the waste materials generated during mining operations. These waste materials, known as tailings, often consist of ground-up rock, chemicals, and other residues from the extraction process. Tailings must be stored in secure facilities to prevent environmental contamination. This often involves constructing tailings dams or using other containment structures.

Market Dynamics:

Driver:

Focus on resource efficiency and circular economy

Efficiency and circular economy principles are revolutionizing mining tailings management. Through advanced technologies like sensor-based sorting and recycling, mining companies can recover valuable minerals from tailings, reducing waste and environmental impact. Reusing water and integrating renewable energy sources further enhance resource efficiency. Circular economy models promote the continual use of materials, turning what was once considered waste into valuable resources.

Restraint:

Technical expertise and infrastructure limitations

In the market, technical expertise plays a crucial role in addressing challenges like tailings dam stability, water management, and environmental impact mitigation. However, infrastructure limitations, such as inadequate tailings storage facilities, outdated equipment, and limited access to advanced monitoring technologies, hinder effective management practices. Bridging these gaps requires investments in skilled personnel, modern infrastructure, and innovative solutions for sustainable tailings management in the mining industry.

Opportunity:

Rising demand for metals and minerals

The market is experiencing a surge in demand for metals and minerals. This trend is driven by the growing need for sustainable practices in resource extraction and environmental protection. Stakeholders are investing in innovative technologies and strategies to efficiently manage mining waste and extract valuable materials from tailings. This shift reflects a broader industry focus on responsible mining practices and the circular economy, driving significant growth opportunities in the sector.

Threat:

High cost of implementation

The market faces significant hurdles due to the high cost of implementation. This cost encompasses advanced technologies for tailings disposal, including monitoring systems, containment structures, and environmental remediation measures. Additionally, compliance with stringent regulations further escalates expenses. Companies must allocate substantial financial resources for research, development, and operational deployment of these solutions, posing a substantial barrier to entry and expansion within the industry.

Covid-19 Impact:

The COVID-19 pandemic significantly impacted the Mining Tailings Management market. Supply chain disruptions, labor shortages, and project delays were notable challenges. Companies faced operational constraints due to lockdowns, impacting tailings management strategies. However, the crisis also accelerated digital transformation in the industry, promoting remote monitoring and automation solutions. Environmental concerns and regulatory pressures remained, driving innovation in sustainable tailings disposal methods.

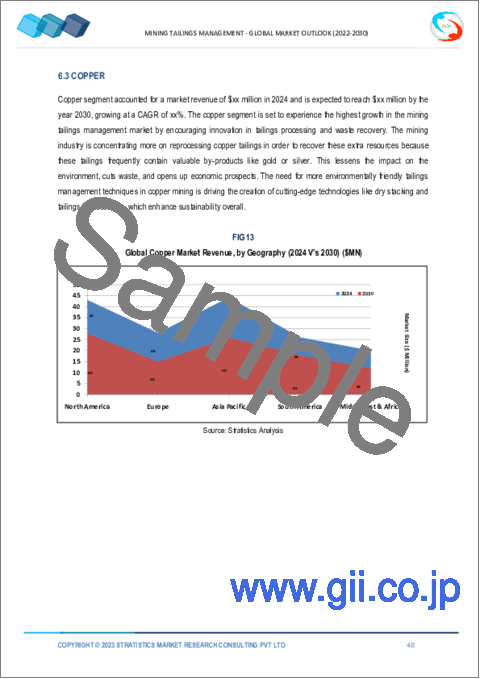

The paste tailings segment is expected to be the largest during the forecast period

The paste tailings are expected to be the largest during the forecast period. Unlike traditional tailings, paste tailings are mixed with a binder to form a more solid consistency, reducing water content and minimizing environmental impact. This technology allows for better containment and reduces the risk of tailings dam failures, enhancing safety and long-term stability. With increasing environmental concerns, paste tailings represent an innovative approach towards responsible mining practices and efficient resource utilization.

The reprocessing segment is expected to have the highest CAGR during the forecast period

The reprocessing segment is expected to have the highest CAGR during the forecast period. By employing advanced technologies and methodologies, reprocessing enables the extraction of valuable minerals and metals from previously discarded tailings. This not only reduces environmental impact by minimizing waste but also presents economic opportunities through resource recovery. The reprocessing segment within the mining tailings management market is experiencing significant growth, driven by sustainability goals and the increasing demand for efficient resource utilization

Region with largest share:

North America is projected to hold the largest market share during the forecast period. Companies in this sector are investing heavily in advanced technologies such as tailings dewatering systems, geopolymer technology, and remote monitoring solutions to minimize environmental impact and enhance operational efficiency. With increasing awareness about the long-term consequences of improper tailings disposal, the demand for innovative and eco-friendly tailings management solutions continues to grow across the region.

Region with highest CAGR:

Asia Pacific is projected to hold the highest CAGR over the forecast period due to the region's extensive mining activities and the growing focus on environmental sustainability. he market has seen a rise in innovative technologies for tailings management, such as dry stack tailings, which reduce water consumption and the risk of environmental contamination. These technologies are increasingly being adopted by mining companies in the region to comply with regulations and improve their sustainability credentials.

Key players in the market

Some of the key players in Mining Tailings Management market include Vale, BHP, Rio Tinto, Anglo American, Glencore, Freeport-McMoRan, Newmont, Teck Resources, Southern Copper Corporation, Codelco, Hindustan Zinc Limited, Antofagasta Minerals, China Shenhua Energy, Norilsk Nickel, MMC Norilsk Nickel, Barrick Gold and Goldcorp.

Key Developments:

In March 2024, Anglo American and Nittetsu Mining (Nittetsu) have signed a memorandum of understanding to collaborate on a variety of commercial and sustainability initiatives to further advance sustainable mining practices in the copper industry.

Types Covered:

- Conventional Tailings

- Thickened Tailings

- Paste Tailings

- Filter Tailings

- Other Types

Mineral Types Covered:

- Gold

- Copper

- Iron Ore

- Coal

- Rare Earth Elements (REE)

Mining Methods Covered:

- Open Pit Mining

- Underground Mining

- Placer Mining

Applications Covered:

- Surface Disposal

- Underground Disposal

- Reprocessing

- Reclamation

- Other Applications

End Users Covered:

- Mining

- Construction

- Energy

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2022, 2023, 2024, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 End User Analysis

- 3.8 Emerging Markets

- 3.9 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Mining Tailings Management Market, By Type

- 5.1 Introduction

- 5.2 Conventional Tailings

- 5.3 Thickened Tailings

- 5.4 Paste Tailings

- 5.5 Filter Tailings

- 5.6 Other Types

6 Global Mining Tailings Management Market, By Mineral Type

- 6.1 Introduction

- 6.2 Gold

- 6.3 Copper

- 6.4 Iron Ore

- 6.5 Coal

- 6.6 Rare Earth Elements (REE)

7 Global Mining Tailings Management Market, By Mining Method

- 7.1 Introduction

- 7.2 Open Pit Mining

- 7.3 Underground Mining

- 7.4 Placer Mining

8 Global Mining Tailings Management Market, By Application

- 8.1 Introduction

- 8.2 Surface Disposal

- 8.3 Underground Disposal

- 8.4 Reprocessing

- 8.5 Reclamation

- 8.6 Other Applications

9 Global Mining Tailings Management Market, By End User

- 9.1 Introduction

- 9.2 Mining

- 9.3 Construction

- 9.4 Energy

- 9.5 Other End Users

10 Global Mining Tailings Management Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.5 South America

- 10.5.1 Argentina

- 10.5.2 Brazil

- 10.5.3 Chile

- 10.5.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 Vale

- 12.2 BHP

- 12.3 Rio Tinto

- 12.4 Anglo American

- 12.5 Glencore

- 12.6 Freeport-McMoRan

- 12.7 Newmont

- 12.8 Teck Resources

- 12.9 Southern Copper Corporation

- 12.10 Codelco

- 12.11 Hindustan Zinc Limited

- 12.12 Antofagasta Minerals

- 12.13 China Shenhua Energy

- 12.14 Norilsk Nickel

- 12.15 MMC Norilsk Nickel

- 12.16 Barrick Gold

- 12.17 Goldcorp