|

|

市場調査レポート

商品コード

1494924

航空宇宙用ファスナーの2030年までの市場予測:製品タイプ、材料、航空機タイプ、用途、エンドユーザー、地域別の世界分析Aerospace Fasteners Market Forecasts to 2030 - Global Analysis By Product Type, Material, Aircraft Type, Application, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 航空宇宙用ファスナーの2030年までの市場予測:製品タイプ、材料、航空機タイプ、用途、エンドユーザー、地域別の世界分析 |

|

出版日: 2024年06月06日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、航空宇宙ファスナーの世界市場は2024年に75億米ドルを占め、予測期間中にCAGR 8.3%で成長し、2030年には121億米ドルに達する見込みです。

航空宇宙用ファスナーは、航空機のさまざまな部品を組み立て、固定するために使用される特殊な部品であり、構造的完全性と安全性を確保します。チタン、アルミニウム、ステンレス鋼のような高強度材料から作られるこれらのファスナーには、ボルト、ネジ、リベット、ナットが含まれます。これらは、航空機の性能と信頼性を維持するために重要な、高い応力、温度変化、振動などの過酷な条件に耐えるように設計されています。

国際航空運送協会(IATA)によると、航空旅客数は2024年までに40億人に達するとしています。また、米連邦航空局は、米国の航空旅客数が2038年までに12億8,000万人に達すると予測しています。

航空機保有台数の増加

航空機保有台数の増加は、航空宇宙用ファスナー市場の重要な促進要因です。世界の航空旅客数の増加が続く中、航空会社は増大する需要に対応するために航空機を拡大しています。この拡大により、新しい航空機の組み立てと保守のために、より大量の航空宇宙用ファスナーが必要となります。さらに、老朽化した航空機の新型機への置き換えがファスナー需要をさらに押し上げ、市場の成長を促進し、拡大する航空機の安全性と信頼性を確保しています。

原材料価格の変動

原材料価格の変動は、航空宇宙用ファスナー市場に大きな抑制要因となっています。アルミニウム、チタン、スチールなどの主要材料の価格は、市場力学、地政学的要因、サプライチェーンの混乱によって変動する可能性があります。こうした変動は航空宇宙用ファスナーの生産コストに影響を及ぼし、エンドユーザーの価格上昇につながる可能性があります。メーカーは収益性と競合を維持する上で課題に直面する可能性があり、これが市場の成長と新技術への投資の妨げになる可能性があります。

軽量材料の採用

軽量材料の採用は、航空宇宙用ファスナー市場に大きな機会をもたらします。航空宇宙産業が燃費の向上と排出ガスの削減に重点を置いているため、チタンや複合材料のような先端材料で作られたファスナーに対する需要が高まっています。これらの材料は高い強度対重量比を提供し、航空機の性能を高め、全体的な重量を軽減します。軽量で高性能なファスナーの開発に投資するメーカーは、この動向を利用し、技術革新と市場拡大を促進することができます。

厳しい規制基準

航空宇宙産業は高度に規制されており、ファスナーを含むすべての部品に厳しい安全性と性能要件が課されています。これらの基準を遵守するには、厳格な試験、認証プロセス、品質管理措置の遵守が必要です。これらの基準を満たせない場合、製品のリコール、法的責任、市場での評判の低下を招く可能性があります。また、コンプライアンスにかかる高いコストと複雑さが新規参入を阻み、市場の成長を制限することもあります。

COVID-19の影響:

COVID-19の流行は航空宇宙用ファスナー市場に大きな影響を与えました。世界の封鎖と旅行制限により、航空旅行が大幅に減少し、その結果、新しい航空機とメンテナンス・サービスの需要が減少しました。この景気後退は、航空宇宙用ファスナーの生産と販売に影響を与えました。しかし、産業が回復し、航空旅行が再開するにつれて、航空機の近代化と安全対策の強化の必要性によって、市場は回復すると予想されます。

予測期間中、リベット・セグメントが最大になる見込み

リベット・セグメントは、航空機組立におけるその広範な使用により、航空宇宙ファスナー市場を独占すると予想されます。リベットは、航空機の構造的完全性にとって不可欠な強固で信頼性の高い接合部を提供します。リベットは、胴体、翼、制御面などの重要な部分に広く使用されています。リベットの需要は、新しい航空機の継続的な生産と定期的なメンテナンスと修理の必要性によって牽引され、市場での優位性を確保しています。

防衛分野が予測期間中最も高いCAGRを持つと予測される

航空宇宙ファスナー市場では、防衛分野が最もCAGRが高いと予測されています。この成長の原動力は、世界の防衛予算の増加と軍用機の近代化です。戦闘機や輸送機を含む高度な軍用機の需要には、過酷な条件に耐える高性能ファスナーが必要です。新しい防衛技術への投資と老朽化した軍用機の更新が、このセグメントの航空宇宙用ファスナーの需要をさらに押し上げています。

最大のシェアを持つ地域

北米は、航空宇宙産業が発達しており、ボーイングやロッキード・マーチンなどの大手航空機メーカーが存在するため、航空宇宙用ファスナー市場を独占する立場にあります。同地域は技術革新に重点を置いており、国防支出も豊富で、民間航空機の需要が高いことが市場シェア上位に寄与しています。さらに、確立されたサプライチェーンと強固なインフラが航空宇宙用ファスナーの生産と流通を支えており、北米の市場支配力を確実なものにしています。

CAGRが最も高い地域:

アジア太平洋地域は、航空旅行の増加、国防費の増加、航空機製造能力の拡大により、航空宇宙用ファスナー市場の急成長が見込まれています。中国、インド、日本などの国々は、航空宇宙産業に多額の投資を行っており、ファスナーの需要増につながっています。この地域の中間層の増加と都市化も民間航空機の需要増に貢献しており、アジア太平洋市場の成長見通しをさらに後押ししています。

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご提供いたします:

- 企業プロファイル

- 追加市場企業の包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 製品分析

- 用途分析

- エンドユーザー分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の航空宇宙用ファスナー市場:製品タイプ

- リベット

- ブラインドリベット

- ソリッドシャンクリベット

- 電球ブラインドリベット

- ネジ

- ハイロックネジ

- ショルダースクリュー

- ソケットヘッドキャップスクリュー

- 板金ネジ

- ナットとボルト

- ロックナット

- せん断ボルト

- ウィングナット

- その他の製品タイプ

第6章 世界の航空宇宙用ファスナー市場:材料別

- 高強度鋼合金

- チタン合金

- インコネル合金

- ステンレス鋼

- アルミニウム合金

- 複合材料

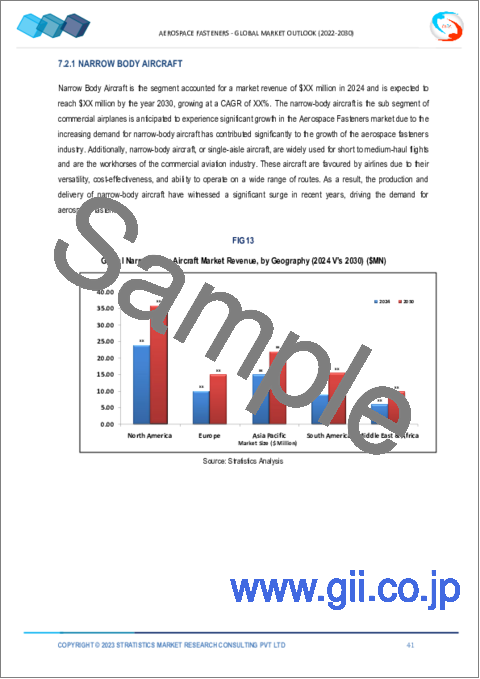

第7章 世界の航空宇宙用ファスナー市場:航空機タイプ別

- 民間航空機

- ナローボディ機

- ワイドボディ機

- 地域輸送機

- ビジネスジェット

- 軍用機

第8章 世界の航空宇宙用ファスナー市場:用途別

- 航空機胴体と組み立て

- エンジンナセルとパイロン

- 着陸装置システム

- 内装構造と助手席

- その他の用途

第9章 世界の航空宇宙用ファスナー市場:エンドユーザー別

- 商業航空

- 防衛

第10章 世界の航空宇宙用ファスナー市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東・アフリカ

第11章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第12章 企業プロファイリング

- Arconic Inc.

- Precision Castparts Corp.

- LISI Aerospace

- Bollhoff Group

- Stanley Black & Decker, Inc.

- 3V Fasteners Company, Inc.

- KLX Inc.

- TriMas Corporation

- SPS Technologies LLC

- Berkshire Hathaway Inc.

- Ho-Ho-Kus Inc.

- The Boeing Company

- Airbus SE

- Lockheed Martin

- Wesco Aircraft Holdings, Inc.

- National Aerospace Fasteners Corporation

- Precision Aerospace Components

- Anixter International Inc.

List of Tables

- Table 1 Global Aerospace Fasteners Market Outlook, By Region (2022-2030) ($MN)

- Table 2 Global Aerospace Fasteners Market Outlook, By Product Type (2022-2030) ($MN)

- Table 3 Global Aerospace Fasteners Market Outlook, By Rivets (2022-2030) ($MN)

- Table 4 Global Aerospace Fasteners Market Outlook, By Blind Rivets (2022-2030) ($MN)

- Table 5 Global Aerospace Fasteners Market Outlook, By Solid Shank Rivets (2022-2030) ($MN)

- Table 6 Global Aerospace Fasteners Market Outlook, By Bulblind Rivets (2022-2030) ($MN)

- Table 7 Global Aerospace Fasteners Market Outlook, By Screws (2022-2030) ($MN)

- Table 8 Global Aerospace Fasteners Market Outlook, By Hi-Lok Screws (2022-2030) ($MN)

- Table 9 Global Aerospace Fasteners Market Outlook, By Shoulder Screws (2022-2030) ($MN)

- Table 10 Global Aerospace Fasteners Market Outlook, By Socket Head Cap Screws (2022-2030) ($MN)

- Table 11 Global Aerospace Fasteners Market Outlook, By Sheet Metal Screws (2022-2030) ($MN)

- Table 12 Global Aerospace Fasteners Market Outlook, By Nuts & Bolts (2022-2030) ($MN)

- Table 13 Global Aerospace Fasteners Market Outlook, By Locknuts (2022-2030) ($MN)

- Table 14 Global Aerospace Fasteners Market Outlook, By Shear Bolts (2022-2030) ($MN)

- Table 15 Global Aerospace Fasteners Market Outlook, By Wing Nuts (2022-2030) ($MN)

- Table 16 Global Aerospace Fasteners Market Outlook, By Other Product Types (2022-2030) ($MN)

- Table 17 Global Aerospace Fasteners Market Outlook, By Material (2022-2030) ($MN)

- Table 18 Global Aerospace Fasteners Market Outlook, By High-Strength Steel Alloys (2022-2030) ($MN)

- Table 19 Global Aerospace Fasteners Market Outlook, By Titanium Alloys (2022-2030) ($MN)

- Table 20 Global Aerospace Fasteners Market Outlook, By Inconel Alloys (2022-2030) ($MN)

- Table 21 Global Aerospace Fasteners Market Outlook, By Stainless Steel (2022-2030) ($MN)

- Table 22 Global Aerospace Fasteners Market Outlook, By Aluminum Alloys (2022-2030) ($MN)

- Table 23 Global Aerospace Fasteners Market Outlook, By Composite Materials (2022-2030) ($MN)

- Table 24 Global Aerospace Fasteners Market Outlook, By Aircraft Type (2022-2030) ($MN)

- Table 25 Global Aerospace Fasteners Market Outlook, By Commercial Airplanes (2022-2030) ($MN)

- Table 26 Global Aerospace Fasteners Market Outlook, By Narrow Body Aircraft (2022-2030) ($MN)

- Table 27 Global Aerospace Fasteners Market Outlook, By Wide Body Aircraft (2022-2030) ($MN)

- Table 28 Global Aerospace Fasteners Market Outlook, By Regional Transport Aircraft (2022-2030) ($MN)

- Table 29 Global Aerospace Fasteners Market Outlook, By Business Jets (2022-2030) ($MN)

- Table 30 Global Aerospace Fasteners Market Outlook, By Military Aircraft (2022-2030) ($MN)

- Table 31 Global Aerospace Fasteners Market Outlook, By Application (2022-2030) ($MN)

- Table 32 Global Aerospace Fasteners Market Outlook, By Aircraft Fuselage & Assembly (2022-2030) ($MN)

- Table 33 Global Aerospace Fasteners Market Outlook, By Engine Nacelles & Pylons (2022-2030) ($MN)

- Table 34 Global Aerospace Fasteners Market Outlook, By Landing Gear Systems (2022-2030) ($MN)

- Table 35 Global Aerospace Fasteners Market Outlook, By Interior Structures & Passenger Seats (2022-2030) ($MN)

- Table 36 Global Aerospace Fasteners Market Outlook, By Other Applications (2022-2030) ($MN)

- Table 37 Global Aerospace Fasteners Market Outlook, By End User (2022-2030) ($MN)

- Table 38 Global Aerospace Fasteners Market Outlook, By Commercial Aviation (2022-2030) ($MN)

- Table 39 Global Aerospace Fasteners Market Outlook, By Defense (2022-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Aerospace Fasteners Market is accounted for $7.5 billion in 2024 and is expected to reach $12.1 billion by 2030 growing at a CAGR of 8.3% during the forecast period. Aerospace fasteners are specialized components used to assemble and secure various parts of an aircraft, ensuring structural integrity and safety. Made from high-strength materials like titanium, aluminum, and stainless steel, these fasteners include bolts, screws, rivets, and nuts. They are designed to withstand extreme conditions, such as high stress, temperature variations, and vibration, which are crucial for maintaining aircraft performance and reliability.

According to the International Air Transport Association (IATA), it states that the overall number of air passengers will reach 4 billion by 2024. And, the Federal Aviation Administration forecasted that the number of United States airline passengers will reach 1.28 billion by 2038.

Market Dynamics:

Driver:

Increasing aircraft fleet size

The increasing aircraft fleet size is a significant driver for the aerospace fasteners market. As global air travel continues to rise, airlines are expanding their fleets to meet the growing demand. This expansion necessitates a higher volume of aerospace fasteners for the assembly and maintenance of new aircraft. Additionally, the replacement of aging aircraft with newer models further boosts the demand for fasteners, driving market growth and ensuring the safety and reliability of the expanding fleet.

Restraint:

Volatility in raw material prices

Volatility in raw material prices poses a significant restraint to the aerospace fasteners market. The prices of key materials such as aluminum, titanium, and steel can fluctuate due to market dynamics, geopolitical factors, and supply chain disruptions. These fluctuations can impact the cost of production for aerospace fasteners, leading to increased prices for end-users. Manufacturers may face challenges in maintaining profitability and competitiveness, which can hinder market growth and investment in new technologies.

Opportunity:

Adoption of lightweight materials

The adoption of lightweight materials presents a substantial opportunity for the aerospace fasteners market. As the aerospace industry focuses on improving fuel efficiency and reducing emissions, there is a growing demand for fasteners made from advanced materials like titanium and composites. These materials offer high strength-to-weight ratios, enhancing aircraft performance and reducing overall weight. Manufacturers investing in the development of lightweight, high-performance fasteners can capitalize on this trend, driving innovation and market expansion.

Threat:

Stringent regulatory standards

The aerospace industry is highly regulated, with strict safety and performance requirements for all components, including fasteners. Compliance with these standards involves rigorous testing, certification processes, and adherence to quality control measures. Failure to meet these standards can result in product recalls, legal liabilities, and loss of market reputation. The high cost and complexity of compliance can also deter new entrants and limit market growth.

Covid-19 Impact:

The Covid-19 pandemic had a profound impact on the aerospace fasteners market. The global lockdowns and travel restrictions led to a significant decline in air travel, resulting in reduced demand for new aircraft and maintenance services. This downturn affected the production and sales of aerospace fasteners. However, as the industry recovers and air travel resumes, the market is expected to rebound, driven by the need for fleet modernization and increased safety measures.

The rivets segment is expected to be the largest during the forecast period

The rivets segment is expected to dominate the aerospace fasteners market due to their extensive use in aircraft assembly. Rivets provide strong, reliable joints that are essential for the structural integrity of aircraft. They are widely used in critical areas such as fuselage, wings, and control surfaces. The demand for rivets is driven by the continuous production of new aircraft and the need for regular maintenance and repairs, ensuring their prominence in the market.

The defense segment is expected to have the highest CAGR during the forecast period

The defense segment is projected to have the highest CAGR in the aerospace fasteners market. This growth is driven by increasing defense budgets and the modernization of military fleets worldwide. The demand for advanced military aircraft, including fighter jets and transport planes, necessitates high-performance fasteners that can withstand extreme conditions. Investments in new defense technologies and the replacement of aging military aircraft further boost the demand for aerospace fasteners in this segment.

Region with largest share:

North America is positioned to dominate the aerospace fasteners market due to its advanced aerospace industry and the presence of major aircraft manufacturers like Boeing and Lockheed Martin. The region's strong focus on innovation, extensive defense spending, and high demand for commercial aircraft contribute to its leading market share. Additionally, the well-established supply chain and robust infrastructure support the production and distribution of aerospace fasteners, ensuring North America's dominance in the market.

Region with highest CAGR:

The Asia Pacific region anticipates rapid growth in the aerospace fasteners market, driven by increasing air travel, rising defense expenditures, and expanding aircraft manufacturing capabilities. Countries like China, India, and Japan are investing heavily in their aerospace industries, leading to higher demand for fasteners. The region's growing middle class and urbanization also contribute to the increased demand for commercial aircraft, further boosting the market's growth prospects in Asia Pacific.

Key players in the market

Some of the key players in Aerospace Fasteners Market include Arconic Inc., Precision Castparts Corp., LISI Aerospace, Bollhoff Group, Stanley Black & Decker, Inc., 3V Fasteners Company, Inc., KLX Inc., TriMas Corporation, SPS Technologies LLC, Berkshire Hathaway Inc., Ho-Ho-Kus Inc., The Boeing Company, Airbus SE, Lockheed Martin, Wesco Aircraft Holdings, Inc., National Aerospace Fasteners Corporation, Precision Aerospace Components and Anixter International Inc.

Key Developments:

In May 2024, Boeing announced plans to invest in several Quebec-based enterprises, including a $110 million anchor investment for an Aerospace Development Centre in the new Espace Aero Innovation Zone. The investments are part of Boeing's Industrial and Technological Benefits commitment to Canada for its selection of Boeing's P-8A Poseidon to fulfill its long-term multi-mission aircraft role.

In May 2024, Airbus has announced plans to establish a Tech Hub in Japan. The new initiative is designed to develop partnerships in the country to advance research, technology and innovation in aerospace and push boundaries to prepare for the next generation of aircraft. The new Airbus Tech Hub, coordinated from Tokyo, will focus on three key research areas, including the development of new materials, decarbonisation technologies, robotics and automation.

In May 2023, Arconic Corp (ARNC.N), opens new tab has agreed to be bought by Apollo Global Management Inc (APO.N), opens new tab in a take-private deal valued at about $5.2 billion, the U.S. aerospace supplier said. Apollo will pay $30 for each Arconic share held, representing a premium of 35.6% as of close on Feb. 27, a day before reports of deal talks emerged. The deal, which is expected to close in the second half of the year, has an equity value of about $3 billion.

Product Types Covered:

- Rivets

- Screws

- Nuts & Bolts

- Other Product Types

Materials Covered:

- High-Strength Steel Alloys

- Aluminum Alloys

- Composite Materials

Aircraft Types Covered:

- Commercial Airplanes

- Regional Transport Aircraft

- Business Jets

- Military Aircraft

Applications Covered:

- Aircraft Fuselage & Assembly

- Engine Nacelles & Pylons

- Landing Gear Systems

- Interior Structures & Passenger Seats

- Other Applications

End Users Covered:

- Commercial Aviation

- Defense

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2022, 2023, 2024, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Product Analysis

- 3.7 Application Analysis

- 3.8 End User Analysis

- 3.9 Emerging Markets

- 3.10 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Aerospace Fasteners Market, By Product Type

- 5.1 Introduction

- 5.2 Rivets

- 5.2.1 Blind Rivets

- 5.2.2 Solid Shank Rivets

- 5.2.3 Bulblind Rivets

- 5.3 Screws

- 5.3.1 Hi-Lok Screws

- 5.3.2 Shoulder Screws

- 5.3.3 Socket Head Cap Screws

- 5.3.4 Sheet Metal Screws

- 5.4 Nuts & Bolts

- 5.4.1 Locknuts

- 5.4.2 Shear Bolts

- 5.4.3 Wing Nuts

- 5.5 Other Product Types

6 Global Aerospace Fasteners Market, By Material

- 6.1 Introduction

- 6.2 High-Strength Steel Alloys

- 6.2.1 Titanium Alloys

- 6.2.2 Inconel Alloys

- 6.2.3 Stainless Steel

- 6.3 Aluminum Alloys

- 6.4 Composite Materials

7 Global Aerospace Fasteners Market, By Aircraft Type

- 7.1 Introduction

- 7.2 Commercial Airplanes

- 7.2.1 Narrow Body Aircraft

- 7.2.2 Wide Body Aircraft

- 7.3 Regional Transport Aircraft

- 7.4 Business Jets

- 7.5 Military Aircraft

8 Global Aerospace Fasteners Market, By Application

- 8.1 Introduction

- 8.2 Aircraft Fuselage & Assembly

- 8.3 Engine Nacelles & Pylons

- 8.4 Landing Gear Systems

- 8.5 Interior Structures & Passenger Seats

- 8.6 Other Applications

9 Global Aerospace Fasteners Market, By End User

- 9.1 Introduction

- 9.2 Commercial Aviation

- 9.3 Defense

10 Global Aerospace Fasteners Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.5 South America

- 10.5.1 Argentina

- 10.5.2 Brazil

- 10.5.3 Chile

- 10.5.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 Arconic Inc.

- 12.2 Precision Castparts Corp.

- 12.3 LISI Aerospace

- 12.4 Bollhoff Group

- 12.5 Stanley Black & Decker, Inc.

- 12.6 3V Fasteners Company, Inc.

- 12.7 KLX Inc.

- 12.8 TriMas Corporation

- 12.9 SPS Technologies LLC

- 12.10 Berkshire Hathaway Inc.

- 12.11 Ho-Ho-Kus Inc.

- 12.12 The Boeing Company

- 12.13 Airbus SE

- 12.14 Lockheed Martin

- 12.15 Wesco Aircraft Holdings, Inc.

- 12.16 National Aerospace Fasteners Corporation

- 12.17 Precision Aerospace Components

- 12.18 Anixter International Inc.