|

|

市場調査レポート

商品コード

1494909

血糖モニタリングシステム市場の2030年までの予測:製品タイプ、技術、用途、流通チャネル、エンドユーザー、地域別の世界分析Blood Glucose Monitoring Systems Market Forecasts to 2030 - Global Analysis By Product Type, Technology, Application, Distribution Channel, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 血糖モニタリングシステム市場の2030年までの予測:製品タイプ、技術、用途、流通チャネル、エンドユーザー、地域別の世界分析 |

|

出版日: 2024年06月06日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、血糖モニタリングシステムの世界市場は2024年に180億2,000万米ドルを占め、予測期間中にCAGR 6.8%で成長し、2030年には267億4,000万米ドルに達すると予測されています。

血糖モニタリングシステムは、糖尿病患者の血糖値を測定・モニタリングするために設計された医療機器です。これらのシステムには通常、グルコースメーター、検査ストリップ、自己検査用ランセットのほか、リアルタイムのグルコース測定値を提供する連続グルコースモニタリングシステムが含まれます。正確なモニタリングは、薬物療法、食事療法、ライフスタイルのタイムリーな調整を促進することにより、糖尿病患者の病状管理に役立っています。

国際糖尿病連合(IDF)の推計によると、2021年には約5億3,700万人の成人が糖尿病を患っており、2045年には約7億8,300万人に達すると予測されています。

糖尿病有病率の上昇

糖尿病の世界の有病率の増加は、血糖モニタリングシステム市場の主要な促進要因です。糖尿病と診断される人の数が増え続けるにつれて、効果的なグルコースモニタリングソリューションの需要が高まっています。定期的な血糖モニタリングは糖尿病管理にとって極めて重要であり、患者はグルコースレベルを追跡し、食事、運動、薬物療法について十分な情報を得た上で意思決定を行い、合併症を予防することができます。糖尿病負担の増加とグルコースコントロールの重要性に対する意識の高まりが、先進的な血糖モニタリングシステムの採用に拍車をかけています。

高価な機器

このような高度な機器には高価な価格がついていることが多く、特に価格に敏感な市場や経済的に余裕のない患者の間では、利用しやすさや導入が制限される可能性があります。検査ストリップやセンサーなどの消耗品に関連する継続的な出費は、コスト負担をさらに増大させる。高額な初期費用と定期的な出費は、一部の患者やヘルスケアプロバイダーに高度なグルコースモニタリング技術の採用を躊躇させ、市場拡大の妨げとなる可能性があります。

在宅ヘルスケアの拡大

糖尿病のような慢性疾患の遠隔モニタリングや自己管理に対する嗜好の高まりに伴い、自宅で簡単に使用できるユーザーフレンドリーで接続性の高い血糖モニタリング機器に対する需要が高まっています。血糖モニタリングシステムを遠隔医療プラットフォームやモバイルヘルスアプリケーションと統合することで、患者はリアルタイムでヘルスケアプロバイダーと血糖値データを共有することができ、遠隔診察や個別化された治療調整が容易になります。在宅ヘルスケアサービスの拡大とデジタルヘルス技術の採用は、高度な血糖モニタリングシステムの普及を促進すると予想されます。

製品の偽造

偽造デバイス、検査ストリップ、センサーは、患者の安全性を損ない、不正確なグルコース測定値をもたらし、不適切な治療決定や健康への悪影響につながる可能性があります。偽造品は、必要な品質管理および規制当局の承認を得ていない可能性があり、その使用は正規の血糖モニタリングシステムに対する患者の信頼を損なう可能性があります。メーカーは、模倣品の脅威に直面する中で、知的財産を保護し、製品の真正性を確保するという課題に直面しています。

COVID-19の影響:

COVID-19の大流行は、糖尿病の遠隔モニタリングと自己管理の重要性を浮き彫りにしました。閉鎖されヘルスケア施設へのアクセスが減少する中、多くの患者が自宅でのグルコースモニタリングに頼って病状を管理しています。パンデミックは、接続型血糖モニタリングシステムを含む遠隔医療や遠隔モニタリングソリューションの採用を加速させました。しかし、パンデミックはサプライチェーンを混乱させ、製品の発売や規制当局の承認の遅れにつながり、市場の成長に一時的な影響を与えました。

予測期間中、自己血糖モニタリングシステム部門が最大となる見込み

予測期間中、自己血糖測定システム分野が市場を独占すると予想されます。これらのシステムは広く入手可能で、使いやすく、手頃な価格であることが大きな市場シェアの要因となっています。これらの機器により、患者は自宅や外出先で血糖値を簡便にチェックすることができ、糖尿病管理についてタイムリーな意思決定を行うことができます。多くの国で自己血糖測定システムに対する償還政策が確立されており、患者やヘルスケアプロバイダーがこれらの機器に慣れ親しんでいることが、市場での優位性をさらに支えています。

妊娠糖尿病セグメントは予測期間中に最も高いCAGRが見込まれる

妊娠中に発症する妊娠糖尿病は、血糖モニタリングシステム市場で最も急成長するセグメントとなる見込みです。母体年齢の上昇、肥満、座りがちなライフスタイルなどの要因によって、世界中で妊娠糖尿病の有病率が増加していることが、この患者集団における効果的な血糖モニタリングソリューションの需要に拍車をかけています。さらに、妊娠糖尿病の早期診断と早期管理の重要性に対する意識の高まりが、このセグメントの急成長を促進すると予想されます。

最大のシェアを占める地域

北米が血糖モニタリングシステム市場で最大のシェアを占めると予想されます。糖尿病有病率の高さ、確立されたヘルスケアインフラ、血糖モニタリング機器に対する有利な償還政策が、この地域の支配的地位に貢献しています。主要市場プレイヤーの存在、高度な技術力、糖尿病管理の重視が北米の市場成長をさらに後押ししています。

CAGRが最も高い地域:

アジア太平洋地域は、予測期間中に血糖モニタリングシステム市場で最も高い成長率を記録すると予測されます。この地域は、急速な都市化、ライフスタイルの変化、肥満率の増加などの要因によって、糖尿病人口が大きく増加しており、大きな市場機会をもたらしています。中国やインドのような国々は、膨大な数の患者を抱え、医療インフラが改善されているため、市場成長に大きく貢献すると予想されます。

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 製品分析

- 技術分析

- 用途分析

- エンドユーザー分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の血糖モニタリングシステム市場:製品タイプ別

- 自己血糖測定システム

- 血糖値測定器

- 血糖値検査ストリップ

- ランセットと穿刺器具

- 持続血糖モニタリングシステム

- センサー

- 送信機

- 受信機

第6章 世界の血糖モニタリングシステム市場:技術別

- 侵襲的血糖モニタリング

- 非侵襲性血糖モニタリング

第7章 世界の血糖モニタリングシステム市場:用途別

- 1型糖尿病

- 2型糖尿病

- 妊娠糖尿病

第8章 世界の血糖モニタリングシステム市場:流通チャネル別

- 小売薬局

- 病院薬局

- オンライン薬局

第9章 世界の血糖モニタリングシステム市場:エンドユーザー別

- 病院と診療所

- 在宅ケア環境

- 診断センター

- その他のエンドユーザー

第10章 世界の血糖モニタリングシステム市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第11章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第12章 企業プロファイリング

- Roche Diagnostics

- Abbott Laboratories

- Medtronic plc

- Dexcom, Inc.

- Ascensia Diabetes Care

- Johnson & Johnson

- B. Braun Melsungen AG

- ARKRAY, Inc.

- Terumo Corporation

- Ypsomed Holding AG

- Nipro Corporation

- Sanofi

- Nova Biomedical

- Trividia Health, Inc.

- AgaMatrix, Inc.

- Echo Therapeutics, Inc.

- GlySens Incorporated

- i-SENS, Inc.

- Bionime Corporation

- DarioHealth Corp.

List of Tables

- Table 1 Global Blood Glucose Monitoring Systems Market Outlook, By Region (2022-2030) ($MN)

- Table 2 Global Blood Glucose Monitoring Systems Market Outlook, By Product Type (2022-2030) ($MN)

- Table 3 Global Blood Glucose Monitoring Systems Market Outlook, By Self-Monitoring Blood Glucose Systems (2022-2030) ($MN)

- Table 4 Global Blood Glucose Monitoring Systems Market Outlook, By Blood Glucose Meters (2022-2030) ($MN)

- Table 5 Global Blood Glucose Monitoring Systems Market Outlook, By Blood Glucose Test Strips (2022-2030) ($MN)

- Table 6 Global Blood Glucose Monitoring Systems Market Outlook, By Lancets and Lancing Devices (2022-2030) ($MN)

- Table 7 Global Blood Glucose Monitoring Systems Market Outlook, By Continuous Glucose Monitoring Systems (2022-2030) ($MN)

- Table 8 Global Blood Glucose Monitoring Systems Market Outlook, By Sensors (2022-2030) ($MN)

- Table 9 Global Blood Glucose Monitoring Systems Market Outlook, By Transmitters (2022-2030) ($MN)

- Table 10 Global Blood Glucose Monitoring Systems Market Outlook, By Receivers (2022-2030) ($MN)

- Table 11 Global Blood Glucose Monitoring Systems Market Outlook, By Technology (2022-2030) ($MN)

- Table 12 Global Blood Glucose Monitoring Systems Market Outlook, By Invasive Blood Glucose Monitoring

- Table 13 Global Blood Glucose Monitoring Systems Market Outlook, By Non-Invasive Blood Glucose Monitoring (2022-2030) ($MN)

- Table 14 Global Blood Glucose Monitoring Systems Market Outlook, By Application (2022-2030) ($MN)

- Table 15 Global Blood Glucose Monitoring Systems Market Outlook, By Type 1 Diabetes (2022-2030) ($MN)

- Table 16 Global Blood Glucose Monitoring Systems Market Outlook, By Type 2 Diabetes (2022-2030) ($MN)

- Table 17 Global Blood Glucose Monitoring Systems Market Outlook, By Gestational Diabetes (2022-2030) ($MN)

- Table 18 Global Blood Glucose Monitoring Systems Market Outlook, By Distribution Channel (2022-2030) ($MN)

- Table 19 Global Blood Glucose Monitoring Systems Market Outlook, By Retail Pharmacies (2022-2030) ($MN)

- Table 20 Global Blood Glucose Monitoring Systems Market Outlook, By Hospital Pharmacies (2022-2030) ($MN)

- Table 21 Global Blood Glucose Monitoring Systems Market Outlook, By Online Pharmacies (2022-2030) ($MN)

- Table 22 Global Blood Glucose Monitoring Systems Market Outlook, By End User (2022-2030) ($MN)

- Table 23 Global Blood Glucose Monitoring Systems Market Outlook, By Hospitals and Clinics (2022-2030) ($MN)

- Table 24 Global Blood Glucose Monitoring Systems Market Outlook, By Home Care Settings (2022-2030) ($MN)

- Table 25 Global Blood Glucose Monitoring Systems Market Outlook, By Diagnostic Centers (2022-2030) ($MN)

- Table 26 Global Blood Glucose Monitoring Systems Market Outlook, By Other End Users (2022-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Blood Glucose Monitoring Systems Market is accounted for $18.02 billion in 2024 and is expected to reach $26.74 billion by 2030 growing at a CAGR of 6.8% during the forecast period. Blood glucose monitoring systems are medical devices designed to measure and monitor the blood glucose levels of individuals with diabetes. These systems typically include glucose meters, testing strips, and lancets for self-testing, as well as continuous glucose monitoring systems that provide real-time glucose readings. Accurate monitoring helps diabetic patients manage their condition by facilitating timely adjustments to medication, diet, and lifestyle.

According to the estimations of the International Diabetes Federation (IDF), in 2021, around 537 million adults had diabetes and it is projected to reach around 783 million by 2045.

Market Dynamics:

Driver:

Rising prevalence of diabetes

The increasing global prevalence of diabetes is a major driver for the blood glucose monitoring systems market. As the number of people diagnosed with diabetes continues to rise, the demand for effective glucose monitoring solutions grows. Regular blood glucose monitoring is crucial for diabetes management, enabling patients to track their glucose levels, make informed decisions about their diet, exercise, and medication, and prevent complications. The rising diabetes burden, coupled with growing awareness about the importance of glucose control, is fueling the adoption of advanced blood glucose monitoring systems.

Restraint:

High cost of devices

These sophisticated devices often come with a premium price tag, which may limit their accessibility and adoption, especially in price-sensitive markets and among patients with limited financial resources. The ongoing expenses related to consumables, such as test strips and sensors, further add to the cost burden. The high upfront costs and recurring expenses may deter some patients and healthcare providers from embracing advanced glucose monitoring technologies, thus hindering market expansion.

Opportunity:

Expansion of home healthcare

With the increasing preference for remote monitoring and self-management of chronic conditions like diabetes, there is a rising demand for user-friendly and connected glucose monitoring devices that can be easily used at home. The integration of blood glucose monitoring systems with telemedicine platforms and mobile health applications enables patients to share their glucose data with healthcare providers in real-time, facilitating remote consultations and personalized treatment adjustments. The expansion of home healthcare services and the adoption of digital health technologies are expected to drive the uptake of advanced blood glucose monitoring systems.

Threat:

Product counterfeiting

Counterfeit devices, test strips, and sensors can compromise patient safety and lead to inaccurate glucose readings, potentially resulting in improper treatment decisions and adverse health outcomes. Counterfeit products may lack the necessary quality control and regulatory approvals, and their use can erode patient trust in legitimate blood glucose monitoring systems. Manufacturers face the challenge of protecting their intellectual property and ensuring the authenticity of their products in the face of counterfeit threats.

Covid-19 Impact:

The Covid-19 pandemic has highlighted the importance of remote monitoring and self-management of diabetes. With lockdowns and reduced access to healthcare facilities, many patients have relied on home-based glucose monitoring to manage their condition. The pandemic has accelerated the adoption of telemedicine and remote monitoring solutions, including connected blood glucose monitoring systems. However, the pandemic has also disrupted supply chains and led to delays in product launches and regulatory approvals, temporarily affecting market growth.

The self-monitoring blood glucose systems segment is expected to be the largest during the forecast period

The self-monitoring blood glucose systems segment is expected to dominate the market during the forecast period. The widespread availability, ease of use, and affordability of these systems contribute to their large market share. These devices enable patients to conveniently check their blood glucose levels at home or on the go, empowering them to make timely decisions about their diabetes management. The established reimbursement policies for self-monitoring blood glucose systems in many countries and the familiarity of patients and healthcare providers with these devices further support their dominant position in the market.

The gestational diabetes segment is expected to have the highest CAGR during the forecast period

The Gestational diabetes, which occurs during pregnancy, is expected to be the fastest-growing segment in the blood glucose monitoring systems market. The increasing prevalence of gestational diabetes worldwide, driven by factors such as rising maternal age, obesity, and sedentary lifestyles, is fueling the demand for effective glucose monitoring solutions in this patient population. Additionally, growing awareness about the importance of early diagnosis and management of gestational diabetes is expected to drive the rapid growth of this segment.

Region with largest share:

North America is expected to hold the largest share of the blood glucose monitoring systems market. The high prevalence of diabetes, well-established healthcare infrastructure, and favorable reimbursement policies for glucose monitoring devices contribute to the region's dominant position. The presence of key market players, advanced technological capabilities, and a strong emphasis on diabetes management further support market growth in North America.

Region with highest CAGR:

The Asia Pacific region is projected to experience the highest growth rate in the blood glucose monitoring systems market during the forecast period. The region's large and growing diabetes population, driven by factors such as rapid urbanization, changing lifestyles, and increasing obesity rates, presents a significant market opportunity. Countries like China and India, with their vast patient pools and improving healthcare infrastructure, are expected to be major contributors to market growth.

Key players in the market

Some of the key players in Blood Glucose Monitoring Systems Market include Roche Diagnostics, Abbott Laboratories, Medtronic plc, Dexcom, Inc., Ascensia Diabetes Care, Johnson & Johnson, B. Braun Melsungen AG, ARKRAY, Inc., Terumo Corporation, Ypsomed Holding AG, Nipro Corporation, Sanofi, Nova Biomedical, Trividia Health, Inc., AgaMatrix, Inc., Echo Therapeutics, Inc., GlySens Incorporated, i-SENS, Inc., Bionime Corporation and DarioHealth Corp.

Key Developments:

In October 2023, Terumo Corporation announced that it has agreed with U.S.-based Dexcom, Inc (Dexcom) to cease the distribution agreement for Dexcom's Continuous Glucose Monitoring Systems (CGM) in Japan. This decision was made in accordance with Dexcom's change in marketing strategy to shift from indirect distribution to direct sales in certain key markets, excluding the U.S.

In April 2023, Dexcom announced that the FDA cleared Stelo by Dexcom, the first glucose biosensor that doesn't require a prescription, making it easier for people with Type 2 diabetes not using insulin to access leading CGM technology.

In May 2022, Abbott announced the U.S. Food and Drug Administration (FDA) cleared its next-generation FreeStyle Libre 3 system for use by people four years and older6 living with diabetes. "The FreeStyle Libre 3 system is a direct result of listening to our customers - and giving them the innovation and sensing technology they've been looking for," said Jared Watkin, senior vice president of Abbott's diabetes care business.

Product Types Covered:

- Self-Monitoring Blood Glucose Systems

- Continuous Glucose Monitoring Systems

Technologies Covered:

- Invasive Blood Glucose Monitoring

- Non-Invasive Blood Glucose Monitoring

Applications Covered:

- Type 1 Diabetes

- Type 2 Diabetes

- Gestational Diabetes

Distribution Channels Covered:

- Retail Pharmacies

- Hospital Pharmacies

- Online Pharmacies

End Users Covered:

- Hospitals and Clinics

- Home Care Settings

- Diagnostic Centers

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2022, 2023, 2024, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

3.6 Product Analysis

- 3.7 Technology Analysis

- 3.8 Application Analysis

- 3.9 End User Analysis

- 3.10 Emerging Markets

- 3.11 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Blood Glucose Monitoring Systems Market, By Product Type

- 5.1 Introduction

- 5.2 Self-Monitoring Blood Glucose Systems

- 5.2.1 Blood Glucose Meters

- 5.2.2 Blood Glucose Test Strips

- 5.2.3 Lancets and Lancing Devices

- 5.3 Continuous Glucose Monitoring Systems

- 5.3.1 Sensors

- 5.3.2 Transmitters

- 5.3.3 Receivers

6 Global Blood Glucose Monitoring Systems Market, By Technology

- 6.1 Introduction

- 6.2 Invasive Blood Glucose Monitoring

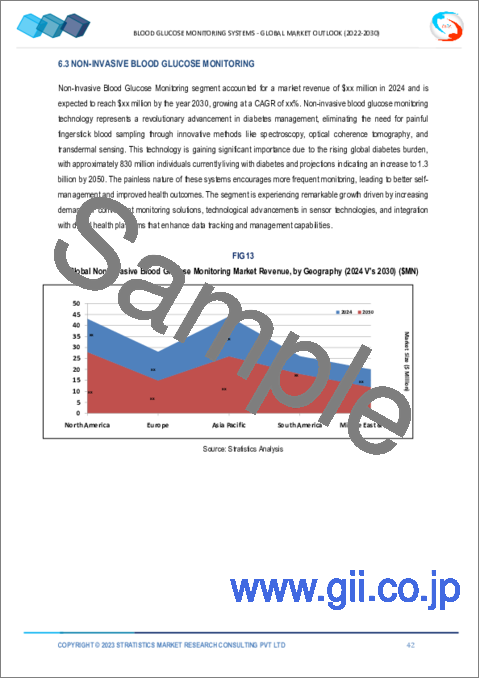

- 6.3 Non-Invasive Blood Glucose Monitoring

7 Global Blood Glucose Monitoring Systems Market, By Application

- 7.1 Introduction

- 7.2 Type 1 Diabetes

- 7.3 Type 2 Diabetes

- 7.4 Gestational Diabetes

8 Global Blood Glucose Monitoring Systems Market, By Distribution Channel

- 8.1 Introduction

- 8.2 Retail Pharmacies

- 8.3 Hospital Pharmacies

- 8.4 Online Pharmacies

9 Global Blood Glucose Monitoring Systems Market, By End User

- 9.1 Introduction

- 9.2 Hospitals and Clinics

- 9.3 Home Care Settings

- 9.4 Diagnostic Centers

- 9.5 Other End Users

10 Global Blood Glucose Monitoring Systems Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.5 South America

- 10.5.1 Argentina

- 10.5.2 Brazil

- 10.5.3 Chile

- 10.5.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 Roche Diagnostics

- 12.2 Abbott Laboratories

- 12.3 Medtronic plc

- 12.4 Dexcom, Inc.

- 12.5 Ascensia Diabetes Care

- 12.6 Johnson & Johnson

- 12.7 B. Braun Melsungen AG

- 12.8 ARKRAY, Inc.

- 12.9 Terumo Corporation

- 12.10 Ypsomed Holding AG

- 12.11 Nipro Corporation

- 12.12 Sanofi

- 12.13 Nova Biomedical

- 12.14 Trividia Health, Inc.

- 12.15 AgaMatrix, Inc.

- 12.16 Echo Therapeutics, Inc.

- 12.17 GlySens Incorporated

- 12.18 i-SENS, Inc.

- 12.19 Bionime Corporation

- 12.20 DarioHealth Corp.