|

|

市場調査レポート

商品コード

1489376

バッグインボックスの世界市場予測(~2030年):部品別、材料別、容量別、用途別、エンドユーザー別、地域別の世界分析Bag-in-Box Market Forecasts to 2030 - Global Analysis By Component (Bags, Boxes, Taps/Spigots, Caps/Closures, Handles, Fitments and Other Components), Material, Capacity, Application, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| バッグインボックスの世界市場予測(~2030年):部品別、材料別、容量別、用途別、エンドユーザー別、地域別の世界分析 |

|

出版日: 2024年06月06日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界のバッグインボックス市場は2023年に20億2,000万米ドルを占め、予測期間中のCAGRは5.8%で成長し、2030年には30億1,000万米ドルに達すると予測されています。

バッグインボックス(BiB)包装は液体貯蔵に革命を起こし、従来のボトルや缶に代わる便利で効率的な代替品を記載しています。BiBは、頑丈な段ボール箱に包まれた軟質な袋で構成され、折りたたみ可能なデザインによって保存期間を延ばし、鮮度を保ち、廃棄物を最小限に抑えます。サイズ、材料、ディスペンサー・オプションをカスタマイズできるバッグインボックスは、その実用性と持続可能性で消費者と商業者の両方のニーズに応え、世界の人気を獲得し続けています。

欧州食品安全機関によると、バッグインボックス容器の製造時に発生する二酸化炭素は、従来の包装に比べ8倍少ないといわれています。

ディスペンサー技術の進歩

バルブやタップの改良など、ディスペンサー技術の進歩により、正確な注出コントロールが可能になり、無駄を省き、製品の鮮度を保つことができます。これらの技術革新はユーザー体験を向上させ、バッグインボックス包装を消費者にとってより便利で実用的なものにします。さらに、これらのシステムにより、バッグインボックスソリューションの様々なディスペンサー機器への統合が容易になり、様々な業界への適用が拡大します。その結果、これらの技術が提供する強化された機能性と汎用性がバッグインボックス包装の採用を促進し、市場成長に寄与しています。

漏れと汚染のリスク

バッグインボックス包装における漏れや汚染のリスクは、主にシール不良、マテリアルハンドリングや輸送中のパンク、包装資材の不十分なバリア特性といった潜在的な問題に起因します。これらのリスクは製品の完全性を損ない、品質の劣化や消費者の健康被害の可能性につながります。こうした事故は消費者の信頼を損ない、ブランドの評判を傷つけ、製品回収につながります。その結果、製品の安全性と信頼性に対する懸念が市場成長の妨げとなっています。

カスタマイズに対する消費者の嗜好の変化

バッグインボックス包装は、特定の消費者のニーズや嗜好に合わせてデザイン、サイズ、機能性をカスタマイズできます。このカスタマイズにより、ブランドは製品を差別化し、ブランドの認知度を高め、ユニークな消費者体験を創造することができます。さらに、バッグインボックス包装の柔軟性は、パーソナライズされたブランディングやメッセージングを容易にし、消費者とのより強い結びつきを育み、最終的にはカスタマイズ可能な包装ソリューションに対する需要の増加を通じて市場の成長を促進します。

代替包装形態との競合

ボトルや缶のような従来の包装形態は、消費者の信頼と市場での存在感を確立していることが多く、バッグインボックス包装が特定のセグメントに浸透することを難しくしています。さらに、伝統的な包装形態に関連する名声や品質に対する認識が、一部の消費者がバッグインボックスソリューションの採用を躊躇させる可能性もあります。このような熾烈な競争は、市場シェアを効果的に獲得するための革新的なマーケティング戦略と差別化を必要とします。

COVID-19の影響

COVID-19の大流行はバッグインボックス市場に大きな影響を与えました。封鎖、規制、経済の不確実性がサプライチェーンの混乱を招き、生産と流通に影響を与えました。オンラインショッピングへのシフトやパッケージ商品への需要の増加など、消費者行動の変化が市場力学に影響を与えました。さらに、レストラン、バー、その他の外食施設の閉鎖は、特定のセグメントにおけるバッグインボックス包装の需要を減少させました。しかし、パンデミックは持続可能で衛生的な包装ソリューションの重要性を浮き彫りにし、パンデミック後のバッグインボックス包装の長期的な成長機会を促進する可能性もあります。

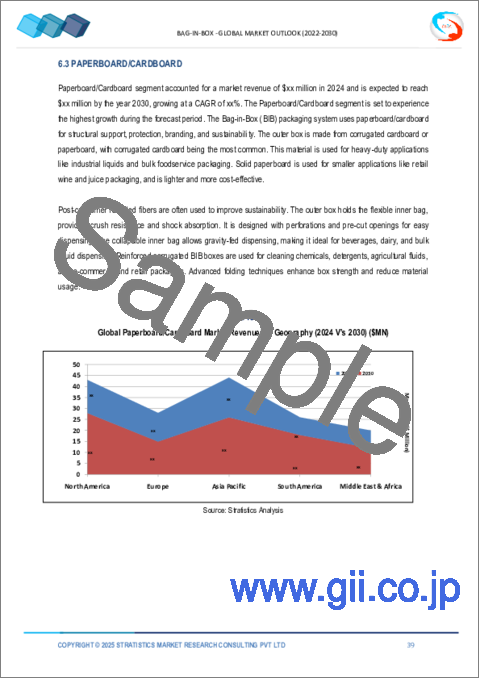

予測期間中、板紙/段ボールセグメントが最大になる見込み

板紙/ダンボールセグメントは有利な成長を遂げると推定されます。板紙/段ボール材料のバッグインボックスは、持続可能で汎用性の高い包装ソリューションを提供し、環境に優しい代替品への需要の高まりに応えます。再生可能な資源を利用するバッグインボックスは、プラスチックの使用量を最小限に抑えることで環境への影響を軽減します。また、優れたバリア性を備えているため、製品の鮮度を保ち、賞味期限を延長することができます。軽量で耐久性に優れているため、保管や輸送に便利で、消費者と企業の両方にアピールします。

予測期間中、飲食品セグメントのCAGRが最も高くなると予想されます。

飲食品セグメントは、その多用途性と実用性により、予測期間中に最も高いCAGR成長が見込まれます。包装の無菌設計は、製品の鮮度保持と保存期間の延長に役立ち、品質と味の完全性を保証します。軽量で積み重ねることができるため、保管や輸送が容易になり、物流コストが削減されます。さらに、バッグインボックス包装は、材料の使用量と廃棄物を最小限に抑えることで環境面でもメリットがあり、業界の持続可能性目標に合致しています。

最大のシェアを占める地域

予測期間中、アジア太平洋が最大の市場シェアを占めると予測されます。急速な都市化、消費者のライフスタイルの変化、可処分所得の増加が、便利で持ち運び可能な包装ソリューションへの需要を押し上げています。さらに、この地域の飲食品産業、特に中国やインドなどの新興経済圏の拡大が、バッグインボックスメーカーに大きなビジネス機会をもたらしています。さらに、環境の持続可能性に対する意識の高まりと、環境に優しい包装を推進する政府の取り組みが、市場の成長をさらに後押ししています。

CAGRが最も高い地域:

予測期間中、欧州のCAGRが最も高いと予測されます。この地域はワイン文化が強く、環境に優しい包装ソリューションの採用が増加していることも市場成長の原動力となっています。さらに、包装の環境に優しい性質は、欧州の厳しい環境規制とサステイナブル製品に対する消費者の嗜好に合致しています。さらに、サステイナブルパッケージングソリューションを推進する政府の取り組みが市場成長をさらに刺激しています。全体として、欧州のバッグインボックス市場は、技術革新と市場力学に後押しされ、成長を続けています。

無料のカスタマイズサービス

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます。

- 企業プロファイル

- 追加市場参入企業の包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推定・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携別の主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データ鉱業

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 前提条件

第3章 市場動向分析

- イントロダクション

- 促進要因

- 抑制要因

- 機会

- 脅威

- 用途分析

- エンドユーザー分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界のバッグインボックス市場:部品別

- イントロダクション

- バッグ

- ボックス

- 蛇口/栓

- キャップ/クロージャー

- ハンドル

- 装備

- その他

第6章 世界のバッグインボックス市場:材料別

- イントロダクション

- プラスチック

- 板紙/ダンボール

- アルミニウム

- 金属化フィルム

- その他

第7章 世界のバッグインボックス市場:容量別

- イントロダクション

- 5リットル以下

- 5~20リットル

- 20リットル以上

第8章 世界のバッグインボックス市場:用途別

- イントロダクション

- 液体製品

- 半液体製品

第9章 世界のバッグインボックス市場:エンドユーザー別

- イントロダクション

- 飲食品

- 産業

- 化粧品

- 医療

- 自動車

- 家庭消費者

- その他

第10章 世界のバッグインボックス市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他の欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他のアジア太平洋

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他の中東・アフリカ

第11章 主要開発

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第12章 企業プロファイリング

- Smurfit Kappa Group

- Scholle IPN

- Liqui-Box Corporation

- DS Smith PLC

- CDF Corporation

- Vine Valley Ventures Limited

- Amcor Limited

- Optopack Limited

- Arlington Packaging(英国)Limited

- Parish Manufacturing Inc.

- Zarcos America

- Aran Group

- TPS Rental Systems Limited

- International Dispensing Corporation(IDC)

List of Tables

- Table 1 Global Bag-in-Box Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Bag-in-Box Market Outlook, By Component (2021-2030) ($MN)

- Table 3 Global Bag-in-Box Market Outlook, By Bags (2021-2030) ($MN)

- Table 4 Global Bag-in-Box Market Outlook, By Boxes (2021-2030) ($MN)

- Table 5 Global Bag-in-Box Market Outlook, By Taps/Spigots (2021-2030) ($MN)

- Table 6 Global Bag-in-Box Market Outlook, By Caps/Closures (2021-2030) ($MN)

- Table 7 Global Bag-in-Box Market Outlook, By Handles (2021-2030) ($MN)

- Table 8 Global Bag-in-Box Market Outlook, By Fitments (2021-2030) ($MN)

- Table 9 Global Bag-in-Box Market Outlook, By Other Components (2021-2030) ($MN)

- Table 10 Global Bag-in-Box Market Outlook, By Material (2021-2030) ($MN)

- Table 11 Global Bag-in-Box Market Outlook, By Plastic (2021-2030) ($MN)

- Table 12 Global Bag-in-Box Market Outlook, By Paperboard/Cardboard (2021-2030) ($MN)

- Table 13 Global Bag-in-Box Market Outlook, By Aluminum (2021-2030) ($MN)

- Table 14 Global Bag-in-Box Market Outlook, By Metallized Films (2021-2030) ($MN)

- Table 15 Global Bag-in-Box Market Outlook, By Other Materials (2021-2030) ($MN)

- Table 16 Global Bag-in-Box Market Outlook, By Capacity (2021-2030) ($MN)

- Table 17 Global Bag-in-Box Market Outlook, By Less Than 5 Liters (2021-2030) ($MN)

- Table 18 Global Bag-in-Box Market Outlook, By 5 to 20 Liters (2021-2030) ($MN)

- Table 19 Global Bag-in-Box Market Outlook, By More Than 20 Liters (2021-2030) ($MN)

- Table 20 Global Bag-in-Box Market Outlook, By Application (2021-2030) ($MN)

- Table 21 Global Bag-in-Box Market Outlook, By Liquid Products (2021-2030) ($MN)

- Table 22 Global Bag-in-Box Market Outlook, By Semi-liquid Products (2021-2030) ($MN)

- Table 23 Global Bag-in-Box Market Outlook, By End User (2021-2030) ($MN)

- Table 24 Global Bag-in-Box Market Outlook, By Food & Beverage Industry (2021-2030) ($MN)

- Table 25 Global Bag-in-Box Market Outlook, By Industrial Applications (2021-2030) ($MN)

- Table 26 Global Bag-in-Box Market Outlook, By Cosmetics Industry (2021-2030) ($MN)

- Table 27 Global Bag-in-Box Market Outlook, By Healthcare Sector (2021-2030) ($MN)

- Table 28 Global Bag-in-Box Market Outlook, By Automotive Sector (2021-2030) ($MN)

- Table 29 Global Bag-in-Box Market Outlook, By Household Consumers (2021-2030) ($MN)

- Table 30 Global Bag-in-Box Market Outlook, By Other End Users (2021-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Bag-in-Box Market is accounted for $2.02 billion in 2023 and is expected to reach $3.01 billion by 2030 growing at a CAGR of 5.8% during the forecast period. Bag-in-Box (BiB) packaging revolutionizes liquid storage, offering a convenient and efficient alternative to traditional bottles and cans. Consisting of a flexible bag encased in a sturdy cardboard box, BiB extends shelf life, preserves freshness, and minimizes waste through its collapsible design. With customizable sizes, materials, and dispensing options, Bag-in-Box continues to gain popularity globally, catering to both consumer and commercial needs with its practicality and sustainability.

According to the European Food Safety Authority, Bag-in-box containers produce eight times less carbon dioxide during manufacture than conventional types of packaging.

Market Dynamics:

Driver:

Advancements in dispensing technologies

Advancements in dispensing technologies, such as improved valves and taps, offer precise pouring control, reducing waste and ensuring product freshness. These innovations enhance the user experience, making Bag-in-Box packaging more convenient and practical for consumers. Additionally, these systems enable easier integration of bag-in-box solutions into various dispensing equipment, expanding their applicability across different industries. As a result, the enhanced functionality and versatility provided by these technologies drive the adoption of Bag-in-Box packaging, contributing to its market growth.

Restraint:

Risk of leakage and contamination

The risk of leakage and contamination in bag-in-box packaging primarily stems from potential issues such as faulty seals, punctures during handling or transportation, and inadequate barrier properties of the packaging materials. These risks compromise product integrity, leading to quality deterioration and potential health hazards for consumers. Such incidents erode consumer trust, damage brand reputation, and result in product recalls. Consequently, concerns about product safety and reliability hinder the market growth.

Opportunity:

Shifts in consumer preferences towards customization

Bag-in-box packaging allows for customizable designs, sizes, and functionalities to meet specific consumer needs and preferences. This customization enables brands to differentiate their products, enhance brand visibility, and create unique consumer experiences. Additionally, the flexibility of bag-in-box packaging facilitates personalized branding and messaging, fostering stronger connections with consumers and ultimately driving market growth through increased demand for customizable packaging solutions.

Threat:

Competition from alternative packaging formats

Traditional packaging formats such as bottles and cans often have established consumer trust and market presence, making it difficult for bag-in-box packaging to penetrate certain segments. Additionally, the perception of prestige and quality associated with traditional formats may deter some consumers from adopting bag-in-box solutions. This intense competition necessitates innovative marketing strategies and differentiation to effectively capture market share.

Covid-19 Impact

The covid-19 pandemic significantly impacted the bag-in-box market. Lockdowns, restrictions, and economic uncertainties led to disruptions in supply chains, affecting production and distribution. Changes in consumer behaviour, including shifts towards online shopping and increased demand for packaged goods, influenced the market dynamics. Moreover, the closure of restaurants, bars, and other foodservice establishments reduced the demand for bag-in-box packaging in certain sectors. However, the pandemic also highlighted the importance of sustainable and hygienic packaging solutions, potentially driving long-term growth opportunities for bag-in-box packaging post-pandemic.

The paperboard/cardboard segment is expected to be the largest during the forecast period

The paperboard/cardboard segment is estimated to have a lucrative growth. Paperboard/cardboard material Bag-in-Boxes offer a sustainable and versatile packaging solution, catering to the growing demand for eco-friendly alternatives. Utilizing renewable resources, these Bag-in-Boxes reduce environmental impact by minimizing plastic usage. They provide excellent barrier properties, preserving product freshness and extending shelf life. Their lightweight and durable nature makes them convenient for storage and transportation, appealing to both consumers and businesses.

The food & beverage industry segment is expected to have the highest CAGR during the forecast period

The food & beverage industry segment is anticipated to witness the highest CAGR growth during the forecast period, due to its versatility and practicality. The packaging's aseptic design helps preserve product freshness and extends shelf life, ensuring quality and taste integrity. Its lightweight and stackable nature facilitates storage and transportation, reducing logistics costs. Moreover, bag-in-box packaging offers environmental benefits by minimizing material usage and waste, aligning with the industry's sustainability goals.

Region with largest share:

Asia Pacific is projected to hold the largest market share during the forecast period. Rapid urbanization, changing consumer lifestyles, and increasing disposable incomes are boosting demand for convenient and portable packaging solutions. Moreover, the region's expanding food and beverage industry, particularly in emerging economies like China and India, presents significant opportunities for Bag-in-Box manufacturers. Additionally, growing awareness of environmental sustainability and government initiatives promoting eco-friendly packaging further fuel market growth.

Region with highest CAGR:

Europe is projected to have the highest CAGR over the forecast period. The region's strong wine culture, coupled with increasing adoption of eco-friendly packaging solutions, drives market growth. Additionally, the packaging's eco-friendly nature aligns with Europe's stringent environmental regulations and consumer preferences for sustainable products. Moreover, government initiatives promoting sustainable packaging solutions further stimulate market growth. Overall, the bag-in-box market in Europe continues to thrive, propelled by innovation and market dynamics.

Key players in the market

Some of the key players profiled in the Bag-in-Box Market include Smurfit Kappa Group, Scholle IPN, Liqui-Box Corporation, DS Smith PLC, CDF Corporation, Vine Valley Ventures Limited, Amcor Limited, Optopack Limited, Arlington Packaging (UK) Limited, Parish Manufacturing Inc., Zacros America, Aran Group, TPS Rental Systems Limited and International Dispensing Corporation (IDC).

Key Developments:

In November 2023, Smurfit Kappa introduced a recyclable film to replace nylon which is used in bag in box container. The recyclable film is developed using polyethylene offering properties similar to nylon with benefit of recyclability.

In October 2023, Amcor Launched circular connector as part of sustainable packaging solution offerings which would enable the sourcing teams of Walmart and other retailers to lower its carbon footprint. It offers 70% lower carbon footprint compared with the existing products in the market.

Components Covered:

- Bags

- Boxes

- Taps/Spigots

- Caps/Closures

- Handles

- Fitments

- Other Components

Materials Covered:

- Plastic

- Paperboard/Cardboard

- Aluminum

- Metallized Films

- Other Materials

Capacities Covered:

- Less Than 5 Liters

- 5 to 20 Liters

- More Than 20 Liters

Applications Covered:

- Liquid Products

- Semi-liquid Products

End Users Covered:

- Food & Beverage Industry

- Industrial Applications

- Cosmetics Industry

- Healthcare Sector

- Automotive Sector

- Household Consumers

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 End User Analysis

- 3.8 Emerging Markets

- 3.9 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Bag-in-Box Market, By Component

- 5.1 Introduction

- 5.2 Bags

- 5.3 Boxes

- 5.4 Taps/Spigots

- 5.5 Caps/Closures

- 5.6 Handles

- 5.7 Fitments

- 5.8 Other Components

6 Global Bag-in-Box Market, By Material

- 6.1 Introduction

- 6.2 Plastic

- 6.3 Paperboard/Cardboard

- 6.4 Aluminum

- 6.5 Metallized Films

- 6.6 Other Materials

7 Global Bag-in-Box Market, By Capacity

- 7.1 Introduction

- 7.2 Less Than 5 Liters

- 7.3 5 to 20 Liters

- 7.4 More Than 20 Liters

8 Global Bag-in-Box Market, By Application

- 8.1 Introduction

- 8.2 Liquid Products

- 8.3 Semi-liquid Products

9 Global Bag-in-Box Market, By End User

- 9.1 Introduction

- 9.2 Food & Beverage Industry

- 9.3 Industrial Applications

- 9.4 Cosmetics Industry

- 9.5 Healthcare Sector

- 9.6 Automotive Sector

- 9.7 Household Consumers

- 9.8 Other End Users

10 Global Bag-in-Box Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.5 South America

- 10.5.1 Argentina

- 10.5.2 Brazil

- 10.5.3 Chile

- 10.5.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 Smurfit Kappa Group

- 12.2 Scholle IPN

- 12.3 Liqui-Box Corporation

- 12.4 DS Smith PLC

- 12.5 CDF Corporation

- 12.6 Vine Valley Ventures Limited

- 12.7 Amcor Limited

- 12.8 Optopack Limited

- 12.9 Arlington Packaging (UK)Limited

- 12.10 Parish Manufacturing Inc.

- 12.11 Zarcos America

- 12.12 Aran Group

- 12.13 TPS Rental Systems Limited

- 12.14 International Dispensing Corporation (IDC)