|

|

市場調査レポート

商品コード

1476302

チップレット市場の2030年までの予測: プロセッサ別、パッケージング技術別、用途別、地域別の世界分析Chiplets Market Forecasts to 2030 - Global Analysis By Processor, By Packaging Technologies, Application and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| チップレット市場の2030年までの予測: プロセッサ別、パッケージング技術別、用途別、地域別の世界分析 |

|

出版日: 2024年05月05日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、チップレットの世界市場は2023年に68億2,000万米ドルを占め、予測期間中のCAGRは81.9%で、2030年には4,494億6,000万米ドルに達する見込みです。

チップレットは、集積回路(IC)システム内で特定の機能を実行するモジュール型半導体部品です。これらの小型チップは、個別に設計、製造、テストされた後、より大きなICパッケージに組み込まれます。チップレットは柔軟でスケーラブルなシステム設計を可能にし、CPU、GPU、AIアクセラレータなどの複雑な電子機器の性能向上、開発コストの削減、市場投入までの時間の短縮を可能にします。

コンシューマー・テクノロジー協会によると、2020年10月のホリデーシーズンに米国では、ゲーム機、ノートパソコン、ウェアラブル端末、テレビなどのテクノロジー関連商品に平均約528米ドルが費やされました。

より高い性能と効率への需要

電子機器における絶え間ない技術革新の追求により、より高い性能と効率に対する需要がチップレット市場の主要な促進要因となっています。チップレットは、CPU、GPU、AIアクセラレータなど、性能特性が最適化された特殊なコンポーネントを1つのシステムに統合することを可能にします。このモジュール式アプローチにより、高性能製品をより柔軟に設計できるようになると同時に、エネルギー効率も向上します。より高速で高性能なデバイスに対する消費者の期待が高まり続ける中、チップレットベースのアーキテクチャの採用は大きく成長する見込みです。

標準化と相互運用性

普遍的に受け入れられている標準規格がないため、異なるベンダーのチップレット間で互換性の問題が生じ、シームレスな相互運用性と異種システムへの統合が妨げられます。このような標準化の欠如は、システム設計を複雑にし、開発時間を増加させ、メーカーのコストを上昇させます。さらに、標準化されたインターフェイスがないため、エコシステムの発展やコラボレーションの可能性が制限され、イノベーションと市場の成長が阻害されます。

エコシステム開発

半導体企業、ファウンドリ、パッケージングサプライヤ、システムインテグレータ間の協力的な取り組みにより、標準化されたインタフェースを確立し、リファレンスデザインを開発し、サプライチェーンパートナーシップを構築することができます。これにより、技術革新、相互運用性、拡張性が促進され、さまざまなアプリケーションでチップレットベースのソリューションの迅速な導入が可能になります。さらに、強固なエコシステムは知識の共有を促進し、技術的進歩を加速させ、投資を活性化させるため、チップレット市場の拡大を促進し、利害関係者が新たな動向や需要を活用する新たな機会を引き出します。

知的財産(IP)リスク

知的財産(IP)リスクは、技術開発と統合の複雑なエコシステムにより、チップレット市場に重大な脅威をもたらします。チップレットは複数の事業体によって開発され、さまざまなシステムに統合されているため、独自の設計、アルゴリズム、技術の知的財産権侵害、不正使用、不正流用のリスクがあります。これは法的紛争、競合優位性の喪失、ビジネス関係の毀損につながり、チップレット業界の技術革新と市場成長を阻害する可能性があります。

COVID-19の影響:

COVID-19パンデミックはチップレット市場を混乱させ、サプライチェーンの混乱、工場閉鎖、消費者需要の減少を引き起こしました。不確実性と景気後退により、製品の発売や半導体技術への投資が遅れました。しかし、デジタルインフラストラクチャやリモートワークソリューションに対する需要の高まりが、データセンターや通信ネットワークにおけるチップレットの採用を促進し、市場の低迷をある程度緩和しました。

予測期間中、中央処理装置(CPU)セグメントが最大となる見込み

チップレット市場では、電子機器においてCPUが重要な役割を果たしているため、予測期間中は中央処理装置(CPU)セグメントが優位を占めると予想されます。CPUは基本的な操作から複雑な計算まで幅広いタスクを処理するため、先進的なチップレットベースのCPU設計に対する需要が高まっています。データセンター、ゲーム、人工知能など、さまざまな用途で高性能コンピューティングのニーズが高まっていることから、CPU分野は市場シェアと収益でリードすると予想されます。

予測期間中にCAGRが最も高くなると予測される自動車分野

自動車分野は、ADAS(先進運転支援システム)、電動化、コネクテッドビークル技術の採用が増加していることから、チップレット市場で最も高いCAGRが見込まれています。チップレットは、AIプロセッサ、センサ、通信モジュールなどの複雑な機能を自動車システムに統合し、自動車の安全性、効率性、接続性を向上させます。さらに、電気自動車や自律走行車への需要が、自動車分野でのチップレットの成長を促進しています。

最もシェアの高い地域:

予測期間中、アジア太平洋地域は、ファウンドリ、パッケージング施設、組立工場など、半導体製造のエコシステムが強固であることから、チップレット市場を独占する見通しです。また、中国、日本、韓国、台湾などの国々では、民生用電子機器、自動車、産業用オートメーションに対する需要が高まっており、チップレットの採用を後押ししています。さらに、政府の取り組み、技術インフラへの投資、熟練した労働力が、アジア太平洋地域のチップレット市場におけるリーダーシップをさらに強化しています。

CAGRが最も高い地域:

予測期間中、アジア太平洋地域はさまざまな要因により、チップレット市場の急速な拡大が見込まれています。この地域には、強固な半導体製造インフラ、研究開発投資の増加、民生用電子機器の需要拡大、人工知能や5Gなどの先端技術の採用増加などがあります。さらに、中国、日本、韓国、台湾などの主要市場プレイヤーの存在が、この地域のチップレット市場における有望な成長軌道に寄与しています。

無料のカスタマイズサービス:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 技術分析

- 用途分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界のチップレット市場:プロセッサ別

- フィールドプログラマブルゲートアレイ(FPGA)

- グラフィックスプロセッシングユニット(GPU)

- 中央処理装置(CPU)

- アプリケーション処理ユニット(APU)

- 人工知能特定用途向け集積回路(AI ASIC)

第6章 世界のチップレット市場:パッケージング技術別

- 2.5Dパッケージ

- 3Dパッケージング

- チップオンボード(COB)

- チップオンフレックス(COF)

- チップオングラス(COG)

- チップオンウェーハ(COW)

- ウェーハレベルパッケージング(WLP)

- ファンアウトウェーハレベルパッケージング(FO-WLP)

- その他のパッケージング技術

第7章 世界のチップレット市場:用途別

- 家電

- スマートフォン

- タブレット

- ウェアラブルデバイス

- ゲーム機

- パソコン

- スマートホームデバイス

- ヘルスケア

- 医療機器

- ウェアラブルヘルスモニター

- 埋め込み型医療機器

- 診断機器

- 自動車

- ADAS(先進運転支援システム)(ADAS)

- インフォテインメントシステム

- エンジン制御ユニット(ECU)

- 高度なセンサー

- 航空宇宙および防衛

- レーダーシステム

- 航空電子機器

- 通信システム

- 監視システム

- 産業

- 産業自動化

- ロボット工学

- プロセス制御システム

- モノのインターネット(IoT)デバイス

- 通信

- ネットワークスイッチ

- ルーター

- 基地局

- 光伝送システム

- 半導体

- チップレット開発

- SoCへの組み込み

- 異種統合

- その他の用途

第8章 世界のチップレット市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第9章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第10章 企業プロファイリング

- Advanced Micro Devices, Inc.(AMD)

- Applied Materials, Inc.

- ARM Holdings

- Broadcom Inc.

- GlobalFoundries Inc.

- IBM Corporation

- Infineon Technologies AG

- Intel Corporation

- Marvell Technology Group Ltd.

- MediaTek Inc.

- Micron Technology, Inc.

- NVIDIA Corporation

- Qualcomm Incorporated

- Renesas Electronics Corporation

- Samsung Electronics Co., Ltd.

- Synopsys, Inc.

- Taiwan Semiconductor Manufacturing Company Limited(TSMC)

- Texas Instruments Incorporated

- United Microelectronics Corporation(UMC)

- Xilinx, Inc.

List of Tables

- Table 1 Global Chiplets Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Chiplets Market Outlook, By Processor (2021-2030) ($MN)

- Table 3 Global Chiplets Market Outlook, By Field-Programmable Gate Array (FPGA) (2021-2030) ($MN)

- Table 4 Global Chiplets Market Outlook, By Graphics Processing Unit (GPU) (2021-2030) ($MN)

- Table 5 Global Chiplets Market Outlook, By Central Processing Unit (CPU) (2021-2030) ($MN)

- Table 6 Global Chiplets Market Outlook, By Application Processing Unit (APU) (2021-2030) ($MN)

- Table 7 Global Chiplets Market Outlook, By Artificial Intelligence Application-specific Integrated Circuit (AI ASIC) (2021-2030) ($MN)

- Table 8 Global Chiplets Market Outlook, By Packaging Technology (2021-2030) ($MN)

- Table 9 Global Chiplets Market Outlook, By 2.5D Packaging (2021-2030) ($MN)

- Table 10 Global Chiplets Market Outlook, By 3D Packaging (2021-2030) ($MN)

- Table 11 Global Chiplets Market Outlook, By Chip-on-Board (COB) (2021-2030) ($MN)

- Table 12 Global Chiplets Market Outlook, By Chip-on-Flex (COF) (2021-2030) ($MN)

- Table 13 Global Chiplets Market Outlook, By Chip-on-Glass (COG) (2021-2030) ($MN)

- Table 14 Global Chiplets Market Outlook, By Chip-on-Wafer (COW) (2021-2030) ($MN)

- Table 15 Global Chiplets Market Outlook, By Wafer-Level Packaging (WLP) (2021-2030) ($MN)

- Table 16 Global Chiplets Market Outlook, By Fan-Out Wafer-Level Packaging (FO-WLP) (2021-2030) ($MN)

- Table 17 Global Chiplets Market Outlook, By Other Packaging Technologies (2021-2030) ($MN)

- Table 18 Global Chiplets Market Outlook, By Application (2021-2030) ($MN)

- Table 19 Global Chiplets Market Outlook, By Consumer Electronics (2021-2030) ($MN)

- Table 20 Global Chiplets Market Outlook, By Smartphones (2021-2030) ($MN)

- Table 21 Global Chiplets Market Outlook, By Tablets (2021-2030) ($MN)

- Table 22 Global Chiplets Market Outlook, By Wearable Devices (2021-2030) ($MN)

- Table 23 Global Chiplets Market Outlook, By Gaming Consoles (2021-2030) ($MN)

- Table 24 Global Chiplets Market Outlook, By Personal Computers (2021-2030) ($MN)

- Table 25 Global Chiplets Market Outlook, By Smart Home Devices (2021-2030) ($MN)

- Table 26 Global Chiplets Market Outlook, By Healthcare (2021-2030) ($MN)

- Table 27 Global Chiplets Market Outlook, By Medical Devices (2021-2030) ($MN)

- Table 28 Global Chiplets Market Outlook, By Wearable Health Monitors (2021-2030) ($MN)

- Table 29 Global Chiplets Market Outlook, By Implantable Medical Devices (2021-2030) ($MN)

- Table 30 Global Chiplets Market Outlook, By Diagnostic Equipment (2021-2030) ($MN)

- Table 31 Global Chiplets Market Outlook, By Automotive (2021-2030) ($MN)

- Table 32 Global Chiplets Market Outlook, By Advanced Driver Assistance Systems (ADAS) (2021-2030) ($MN)

- Table 33 Global Chiplets Market Outlook, By Infotainment Systems (2021-2030) ($MN)

- Table 34 Global Chiplets Market Outlook, By Engine Control Units (ECUs) (2021-2030) ($MN)

- Table 35 Global Chiplets Market Outlook, By Advanced Sensors (2021-2030) ($MN)

- Table 36 Global Chiplets Market Outlook, By Aerospace and Defense (2021-2030) ($MN)

- Table 37 Global Chiplets Market Outlook, By Radar Systems (2021-2030) ($MN)

- Table 38 Global Chiplets Market Outlook, By Avionics (2021-2030) ($MN)

- Table 39 Global Chiplets Market Outlook, By Communication Systems (2021-2030) ($MN)

- Table 40 Global Chiplets Market Outlook, By Surveillance Systems (2021-2030) ($MN)

- Table 41 Global Chiplets Market Outlook, By Industrial (2021-2030) ($MN)

- Table 42 Global Chiplets Market Outlook, By Industrial Automation (2021-2030) ($MN)

- Table 43 Global Chiplets Market Outlook, By Robotics (2021-2030) ($MN)

- Table 44 Global Chiplets Market Outlook, By Process Control Systems (2021-2030) ($MN)

- Table 45 Global Chiplets Market Outlook, By Internet of Things (IoT) Devices (2021-2030) ($MN)

- Table 46 Global Chiplets Market Outlook, By Telecommunications (2021-2030) ($MN)

- Table 47 Global Chiplets Market Outlook, By Network Switches (2021-2030) ($MN)

- Table 48 Global Chiplets Market Outlook, By Routers (2021-2030) ($MN)

- Table 49 Global Chiplets Market Outlook, By Base Stations (2021-2030) ($MN)

- Table 50 Global Chiplets Market Outlook, By Optical Transport Systems (2021-2030) ($MN)

- Table 51 Global Chiplets Market Outlook, By Semiconductor (2021-2030) ($MN)

- Table 52 Global Chiplets Market Outlook, By Chiplet Development (2021-2030) ($MN)

- Table 53 Global Chiplets Market Outlook, By Incorporation into SoCs (2021-2030) ($MN)

- Table 54 Global Chiplets Market Outlook, By Heterogeneous Integration (2021-2030) ($MN)

- Table 55 Global Chiplets Market Outlook, By Other Applications (2021-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Chiplets Market is accounted for $6.82 billion in 2023 and is expected to reach $449.46 billion by 2030 growing at a CAGR of 81.9% during the forecast period. Chiplets are modular semiconductor components that perform specific functions within an integrated circuit (IC) system. These small, individual chips can be independently designed, manufactured, and tested before being assembled into a larger IC package. Chiplets enable flexible and scalable system designs, allowing for improved performance, reduced development costs, and faster time-to-market for complex electronic devices such as CPUs, GPUs, and AI accelerators.

According to Consumer Technology Association, in October 2020, the population in the U.S. in the holiday season spent about US$ 528, on average, on technology-based items, which included video game consoles, laptops, wearable's and television sets.

Market Dynamics:

Driver:

Demand for higher performance and efficiency

The demand for higher performance and efficiency is a key driver in the chiplets market due to the relentless pursuit of innovation in electronic devices. Chiplets enable manufacturers to integrate specialized components with optimized performance characteristics, such as CPUs, GPUs, and AI accelerators, into a single system. This modular approach allows for greater flexibility in designing high-performance products while also improving energy efficiency. As consumer expectations for faster and more powerful devices continue to rise, the adoption of chiplet-based architectures is poised for significant growth.

Restraint:

Standardization and interoperability

Without universally accepted standards, compatibility issues arise between chiplets from different vendors, hindering seamless interoperability and integration into heterogeneous systems. This lack of standardization complicates system design, increases development time, and raises costs for manufacturers. Furthermore, the absence of standardized interfaces limits the potential for ecosystem development and collaboration, stifling innovation and market growth.

Opportunity:

Ecosystem development

Collaborative efforts among semiconductor companies, foundries, packaging suppliers, and system integrators can establish standardized interfaces, develop reference designs, and create supply chain partnerships. This fosters innovation, interoperability, and scalability, enabling faster adoption of chiplet-based solutions across various applications. Additionally, a robust ecosystem promotes knowledge sharing, accelerates technological advancements, and stimulates investment, driving the expansion of the chiplets market and unlocking new opportunities for stakeholders to capitalize on emerging trends and demands.

Threat:

Intellectual property (IP) risks

Intellectual property (IP) risks pose a significant threat to the chiplets market due to the complex ecosystem of technology development and integration. With chiplets being developed by multiple entities and integrated into various systems, there's a risk of IP infringement, unauthorized use, or misappropriation of proprietary designs, algorithms, or technologies. This can lead to legal disputes, loss of competitive advantage, and damage to business relationships, potentially hampering innovation and market growth in the chiplets industry.

Covid-19 Impact:

The COVID-19 pandemic disrupted the chiplets market, causing supply chain disruptions, factory closures, and reduced consumer demand. Uncertainty and economic downturns led to delays in product launches and investments in semiconductor technologies. However, the increased demand for digital infrastructure and remote work solutions has driven the adoption of chiplets in data centers and telecommunication networks, mitigating some of the market's downturns.

The central processing unit (CPU) segment is expected to be the largest during the forecast period

In the chiplets market, the central processing unit (CPU) segment is anticipated to dominate during the forecast period due to the critical role CPUs play in electronic devices. CPUs handle tasks ranging from basic operations to complex computations, driving demand for advanced chiplet-based CPU designs. With the increasing need for high-performance computing in various applications such as data centers, gaming, and artificial intelligence, the CPU segment is expected to lead in market share and revenue.

The automotive segment is expected to have the highest CAGR during the forecast period

The automotive segment is poised for the highest CAGR in the chiplets market due to the increasing adoption of advanced driver assistance systems (ADAS), electrification, and connected vehicle technologies. Chiplets enable the integration of complex functionalities, such as AI processors, sensors, and communication modules, into automotive systems, enhancing vehicle safety, efficiency, and connectivity. Additionally, the demand for electric and autonomous vehicles further drives the growth of chiplets in the automotive sector.

Region with largest share:

Over the forecast period, Asia Pacific is poised to dominate the chiplets market due to the region's robust semiconductor manufacturing ecosystem, including foundries, packaging facilities, and assembly plants. Additionally, the growing demand for consumer electronics, automotive vehicles, and industrial automation in countries like China, Japan, South Korea, and Taiwan drives the adoption of chiplets. Moreover, government initiatives, investments in technology infrastructure, and a skilled workforce further bolster Asia Pacific's leadership in the chiplets market.

Region with highest CAGR:

During the forecast period, the Asia Pacific region is expected to experience rapid expansion in the chiplets market due to various factors. These include the region's robust semiconductor manufacturing infrastructure, increasing investments in research and development, growing demand for consumer electronics and rising adoption of advanced technologies such as artificial intelligence and 5G. Additionally, the presence of key market players in countries like China, Japan, South Korea, and Taiwan contribute to the region's promising growth trajectory in the chiplets market.

Key players in the market

Some of the key players in Chiplets Market include Advanced Micro Devices, Inc. (AMD), Applied Materials, Inc., ARM Holdings, Broadcom Inc., GlobalFoundries Inc., IBM Corporation, Infineon Technologies AG, Intel Corporation, Marvell Technology Group Ltd., MediaTek Inc., Micron Technology, Inc., NVIDIA Corporation, Qualcomm Incorporated, Renesas Electronics Corporation, Samsung Electronics Co., Ltd., Synopsys, Inc., Taiwan Semiconductor Manufacturing Company Limited (TSMC), Texas Instruments Incorporated, United Microelectronics Corporation (UMC) and Xilinx, Inc.

Key Developments:

In January 2024, Intel Corportion announced its intention to collaborate with an R&D hub named IMEC, to ensure Intel's advanced chiplet packaging technologies satisfy the stringent quality and reliability requirements required for automotive use cases.

In August 2023, Google Cloud (US) and NVIDIA Corporation (US) collaborated to offer advanced AI infrastructure and software for deploying large generative AI models and accelerating data science tasks. This partnership streamlines AI supercomputer deployment via Google Cloud's NVIDIA-powered solutions, leveraging the same technology utilized by Google DeepMind and research teams. The integration optimizes PaxML, Google's LLM framework, for NVIDIA, accelerated computing, enhancing experimentation and scalability with H100 and A100 Tensor Core GPUs.

In June 2023, Intel Corporation (US) announced a partnership with Taiwan Semiconductor Manufacturing Company Limited (Taiwan) to manufacture chips for Intel's high-performance computing and graphics products. The partnership would help Intel reduce its reliance on external foundries.

Processors Covered:

- Field-Programmable Gate Array (FPGA)

- Graphics Processing Unit (GPU)

- Central Processing Unit (CPU)

- Application Processing Unit (APU)

- Artificial Intelligence Application-specific Integrated Circuit (AI ASIC)

Packaging Technologies Covered:

- 2.5D Packaging

- 3D Packaging

- Chip-on-Board (COB)

- Chip-on-Flex (COF)

- Chip-on-Glass (COG)

- Chip-on-Wafer (COW)

- Wafer-Level Packaging (WLP)

- Fan-Out Wafer-Level Packaging (FO-WLP)

- Other Packaging Technologies

Applications Covered:

- Consumer Electronics

- Healthcare

- Automotive

- Aerospace and Defense

- Industrial

- Telecommunications

- Semiconductor

- Other Applications

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Technology Analysis

- 3.7 Application Analysis

- 3.8 Emerging Markets

- 3.9 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Chiplets Market, By Processor

- 5.1 Introduction

- 5.2 Field-Programmable Gate Array (FPGA)

- 5.3 Graphics Processing Unit (GPU)

- 5.4 Central Processing Unit (CPU)

- 5.5 Application Processing Unit (APU)

- 5.6 Artificial Intelligence Application-specific Integrated Circuit (AI ASIC)

6 Global Chiplets Market, By Packaging Technology

- 6.1 Introduction

- 6.2 2.5D Packaging

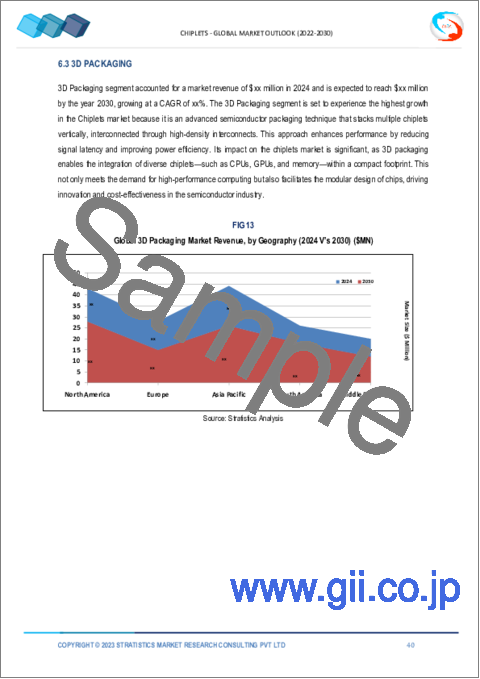

- 6.3 3D Packaging

- 6.4 Chip-on-Board (COB)

- 6.5 Chip-on-Flex (COF)

- 6.6 Chip-on-Glass (COG)

- 6.7 Chip-on-Wafer (COW)

- 6.8 Wafer-Level Packaging (WLP)

- 6.9 Fan-Out Wafer-Level Packaging (FO-WLP)

- 6.10 Other Packaging Technologies

7 Global Chiplets Market, By Application

- 7.1 Introduction

- 7.2 Consumer Electronics

- 7.2.1 Smartphones

- 7.2.2 Tablets

- 7.2.3 Wearable Devices

- 7.2.4 Gaming Consoles

- 7.2.5 Personal Computers

- 7.2.6 Smart Home Devices

- 7.3 Healthcare

- 7.3.1 Medical Devices

- 7.3.2 Wearable Health Monitors

- 7.3.3 Implantable Medical Devices

- 7.3.4 Diagnostic Equipment

- 7.4 Automotive

- 7.4.1 Advanced Driver Assistance Systems (ADAS)

- 7.4.2 Infotainment Systems

- 7.4.3 Engine Control Units (ECUs)

- 7.4.4 Advanced Sensors

- 7.5 Aerospace and Defense

- 7.5.1 Radar Systems

- 7.5.2 Avionics

- 7.5.3 Communication Systems

- 7.5.4 Surveillance Systems

- 7.6 Industrial

- 7.6.1 Industrial Automation

- 7.6.2 Robotics

- 7.6.3 Process Control Systems

- 7.6.4 Internet of Things (IoT) Devices

- 7.7 Telecommunications

- 7.7.1 Network Switches

- 7.7.2 Routers

- 7.7.3 Base Stations

- 7.7.4 Optical Transport Systems

- 7.8 Semiconductor

- 7.8.1 Chiplet Development

- 7.8.2 Incorporation into SoCs

- 7.8.3 Heterogeneous Integration

- 7.9 Other Applications

8 Global Chiplets Market, By Geography

- 8.1 Introduction

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 Italy

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 New Zealand

- 8.4.6 South Korea

- 8.4.7 Rest of Asia Pacific

- 8.5 South America

- 8.5.1 Argentina

- 8.5.2 Brazil

- 8.5.3 Chile

- 8.5.4 Rest of South America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 Qatar

- 8.6.4 South Africa

- 8.6.5 Rest of Middle East & Africa

9 Key Developments

- 9.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 9.2 Acquisitions & Mergers

- 9.3 New Product Launch

- 9.4 Expansions

- 9.5 Other Key Strategies

10 Company Profiling

- 10.1 Advanced Micro Devices, Inc. (AMD)

- 10.2 Applied Materials, Inc.

- 10.3 ARM Holdings

- 10.4 Broadcom Inc.

- 10.5 GlobalFoundries Inc.

- 10.6 IBM Corporation

- 10.7 Infineon Technologies AG

- 10.8 Intel Corporation

- 10.9 Marvell Technology Group Ltd.

- 10.10 MediaTek Inc.

- 10.11 Micron Technology, Inc.

- 10.12 NVIDIA Corporation

- 10.13 Qualcomm Incorporated

- 10.14 Renesas Electronics Corporation

- 10.15 Samsung Electronics Co., Ltd.

- 10.16 Synopsys, Inc.

- 10.17 Taiwan Semiconductor Manufacturing Company Limited (TSMC)

- 10.18 Texas Instruments Incorporated

- 10.19 United Microelectronics Corporation (UMC)

- 10.20 Xilinx, Inc.