|

|

市場調査レポート

商品コード

1447103

発電機の2030年までの市場予測: タイプ別、燃料タイプ別、技術別、用途別、エンドユーザー別、地域別の世界分析Genset Market Forecasts to 2030 - Global Analysis By Type, Fuel Type (Diesel, Natural Gas, Biogas, Liquid Petroleum Gas and Other Fuel Types), Technology, Application, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 発電機の2030年までの市場予測: タイプ別、燃料タイプ別、技術別、用途別、エンドユーザー別、地域別の世界分析 |

|

出版日: 2024年03月03日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の発電機市場は2023年に214億8,000万米ドルを占め、予測期間中のCAGRは8.2%で成長し、2030年には373億1,000万米ドルに達する見込みです。

発電機セットの略である発電機は、エンジンと発電機で構成されるコンパクトなユニットです。停電時や系統電力が利用できない場合にバックアップ電力を供給するために設計されています。発電機には、ディーゼル、天然ガス、プロパンなど、さまざまなサイズと燃料の種類があります。電源が遮断されると自動的に始動し、通常の電力が回復するまで電力を供給します。

中央電力局によると、2022-23年度の再生可能エネルギー発電量は2,035億5,200万ユニット(MU)で、前年度比年率19%増でした。

急速な工業化と都市化

急速な工業化と都市化は、信頼性の高い電力バックアップソリューションへの需要を増大させています。産業界は操業を維持するために中断のない電力供給を必要とし、バックアップ電源としての発電機セットの採用を促進しています。都市化によってインフラ整備が進み、病院、データセンター、通信などの必要不可欠なサービスのバックアップ電源が必要となります。さらに、都市部では送電網が不安定になることが多く、発電機の必要性がさらに高まっています。その結果、産業界や都市部では、活動を支えるために信頼性の高い電力供給が優先されるため、市場は安定した成長を遂げています。

環境への懸念

ジェット機に関する環境上の懸念は、主に窒素酸化物(NOx)、一酸化炭素(CO)、粒子状物質などの汚染物質の排出に関連しています。これらの排出物は大気汚染の原因となり、健康被害をもたらします。さらに、ジェット機は化石燃料に依存することが多く、温室効果ガスの排出につながり、気候変動を悪化させる。厳しい規制はジェット機メーカーにコンプライアンス負担を課し、製造コストと価格設定に影響を与えます。環境意識が高まるにつれて、消費者は環境に優しい代替品をますます好むようになっており、そのため従来の発電機市場の成長を妨げています。

インフラプロジェクトへの投資の増加

建設や輸送からエネルギーや通信に至るまで、インフラプロジェクトでは、中断のない操業を確保するために信頼性の高いバックアップ電源ソリューションが必要とされます。発電機は、送電網が停止している間や、送電網へのアクセスが制限されている遠隔地において、信頼できる電力源を提供します。政府や民間企業がインフラ整備に多額の資金を割く中、発電機の需要は急増を続けています。メーカー各社は、進化する顧客ニーズに対応するため、技術革新と効率強化に注力しており、この動向はジェット機市場の拡大を維持すると予想されます。

高いイニシャルコスト

信頼性、効率性、厳格な規制への適合を確保するために必要な高度なエンジニアリングと製造が主要理由で、ジェット機には高い初期コストがかかります。これらのコストには、高品質の部品の購入、高度な制御システム、さまざまな条件下での性能を保証するための厳格なテストが含まれます。このような初期費用は、特に価格に敏感な市場や、財源が限られている地域では、潜在的な購買意欲をそぐことになります。高い初期費用は参入障壁となり、市場の成長を制限する可能性があります。

COVID-19の影響

COVID-19の大流行は、産業や企業が操業やサプライチェーンの混乱に直面したため、発電機市場に大きな影響を与えました。当初は、経済の不確実性と封鎖措置により需要が減少しました。しかし、企業が遠隔地での業務に適応し、中断のない電力供給を求めるようになると、特に医療、データセンター、通信といった必要不可欠なセグメントで、発電機に対する需要が復活しました。このため、将来の混乱がもたらすリスクを軽減するために、信頼性の高い電源バックアップソリューションへの投資が増加する方向にシフトしました。

予測期間中、ハイブリッド発電機セグメントが最大になる見込み

ハイブリッド発電機セグメントは、その効率性、燃料消費の削減、低排出ガスにより、有利な成長を遂げると推定されます。ソーラーパネル、風力タービン、バッテリーなどのコンポーネントを統合することで、ハイブリッド発電機は、利用可能な場合は再生可能エネルギーを利用し、必要な場合は従来の燃料源に頼ることで発電を最適化します。この柔軟性により、オフグリッド用途、遠隔地、または信頼性の低い送電網インフラがある場所に最適です。環境の持続可能性としなやかさにより、人気の高い選択肢となっています。

予測期間中にCAGRが最も高くなると予想される産業用セグメント

送電網の停止中や不安定な電力供給中も操業を維持できることから、産業用セグメントは予測期間中に最も高いCAGRの成長が見込まれています。中断のない電力が生産プロセスに不可欠な産業では、発電機が継続性を確保し、コストのかかるダウンタイムを防止します。さらに、主電力網へのアクセスが制限されている遠隔地や非電化地域では、発電機は柔軟性を提供します。その使用は、操業効率を高め、中断による経済的損失から守り、産業運営の全体的な回復力を強化し、持続的な生産性と競合を支えます。

最大のシェアを占める地域

アジア太平洋は、工業化、都市化の進展、信頼性の高い電源バックアップソリューションの必要性から、予測期間中最大の市場シェアを占めると予測されます。中国、インド、日本などの国々が、急速なインフラ整備と無停電電源装置に対する需要の高まりによって、この成長を牽引しています。市場は、様々なエンドユーザー・セグメントに対応する多様な製品ポートフォリオを提供する幅広い参入企業によって特徴付けられます。技術の進歩、政府の取り組み、エネルギー効率に関する意識の高まりが、アジア太平洋における発電機市場の拡大にさらに拍車をかけています。

CAGRが最も高い地域:

北米は、バックアップ電源ソリューションの需要増加、排出ガスに関する厳しい規制、無停電電源の必要性に関する意識の高まりにより、予測期間中CAGRが最も高くなると予測されます。米国とカナダは、強固な産業インフラと商業施設によって市場を独占しています。これらの要因は、継続的な技術の進歩や革新と相まって、北米地域における発電機市場の成長軌道を維持すると予想されます。

無料のカスタマイズサービス

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます。

- 企業プロファイル

- 追加市場参入企業の包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推定・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データ鉱業

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査ソース

- 前提条件

第3章 市場動向分析

- イントロダクション

- 促進要因

- 抑制要因

- 機会

- 脅威

- 技術分析

- 用途分析

- エンドユーザー分析

- 新興市場

- 新型コロナウイルス感染症(COVID-19)の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の発電機市場:タイプ別

- イントロダクション

- ポータブル発電機

- 定置式発電機

- ハイブリッド発電機

- その他

第6章 世界の発電機市場:燃料タイプ別

- イントロダクション

- ディーゼル

- 天然ガス

- バイオガス

- 液体石油ガス(LPG)

- その他

第7章 世界の発電機市場:技術別

- イントロダクション

- 再生可能エネルギー一体型発電機

- マイクログリッド発電機セット

- スマート発電機

- その他

第8章 世界の発電機市場:用途別

- イントロダクション

- プライムパワー

- 待機発電

- ピークシェービング

- 継続発電

- その他

第9章 世界の発電機市場:エンドユーザー別

- イントロダクション

- 住宅用

- 商用

- 産業用

- 公共事業

- 政府と防衛

- その他

第10章 世界の発電機市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他の欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他のアジア太平洋

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他の中東・アフリカ

第11章 主要発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第12章 企業プロファイル

- Kohler Corporation

- Cummins Inc.

- Tata Motors

- MTU Onsite Energy

- Caterpillar Inc.

- Wartsila Corporation

- Yanmar Limited

- Mitsubishi Heavy Industries

- Himoinsa Limited

- Atlas Copco AB

- Doosan Corporation

- Kirloskar Electric Company Limited

- Briggs & Stratton Corporation

- Wacker Neuson SE

- Rolls-Royce Power Systems AG

- FG Wilson

- Ingersoll Rand Inc.

- Sterling Generators Private Limited

- John Deere

- Generac Power Systems

List of Tables

- Table 1 Global Genset Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Genset Market Outlook, By Type (2021-2030) ($MN)

- Table 3 Global Genset Market Outlook, By Portable Generators (2021-2030) ($MN)

- Table 4 Global Genset Market Outlook, By Stationary Generators (2021-2030) ($MN)

- Table 5 Global Genset Market Outlook, By Hybrid Generators (2021-2030) ($MN)

- Table 6 Global Genset Market Outlook, By Other Types (2021-2030) ($MN)

- Table 7 Global Genset Market Outlook, By Fuel Type (2021-2030) ($MN)

- Table 8 Global Genset Market Outlook, By Diesel (2021-2030) ($MN)

- Table 9 Global Genset Market Outlook, By Natural Gas (2021-2030) ($MN)

- Table 10 Global Genset Market Outlook, By Biogas (2021-2030) ($MN)

- Table 11 Global Genset Market Outlook, By Liquid Petroleum Gas (LPG) (2021-2030) ($MN)

- Table 12 Global Genset Market Outlook, By Other Fuel Types (2021-2030) ($MN)

- Table 13 Global Genset Market Outlook, By Technology (2021-2030) ($MN)

- Table 14 Global Genset Market Outlook, By Renewable Energy Integrated Gensets (2021-2030) ($MN)

- Table 15 Global Genset Market Outlook, By Microgrid Gensets (2021-2030) ($MN)

- Table 16 Global Genset Market Outlook, By Smart Gensets (2021-2030) ($MN)

- Table 17 Global Genset Market Outlook, By Other Technologies (2021-2030) ($MN)

- Table 18 Global Genset Market Outlook, By Application (2021-2030) ($MN)

- Table 19 Global Genset Market Outlook, By Prime Power (2021-2030) ($MN)

- Table 20 Global Genset Market Outlook, By Standby Power (2021-2030) ($MN)

- Table 21 Global Genset Market Outlook, By Peak Shaving (2021-2030) ($MN)

- Table 22 Global Genset Market Outlook, By Continuous Power (2021-2030) ($MN)

- Table 23 Global Genset Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 24 Global Genset Market Outlook, By End User (2021-2030) ($MN)

- Table 25 Global Genset Market Outlook, By Residential (2021-2030) ($MN)

- Table 26 Global Genset Market Outlook, By Commercial (2021-2030) ($MN)

- Table 27 Global Genset Market Outlook, By Industrial (2021-2030) ($MN)

- Table 28 Global Genset Market Outlook, By Utilities (2021-2030) ($MN)

- Table 29 Global Genset Market Outlook, By Government & Defense (2021-2030) ($MN)

- Table 30 Global Genset Market Outlook, By Other End Users (2021-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Genset Market is accounted for $21.48 billion in 2023 and is expected to reach $37.31 billion by 2030 growing at a CAGR of 8.2% during the forecast period. A genset, short for generator set, is a compact unit comprising an engine and an electric generator. It's designed to provide backup power during electricity outages or where grid power is unavailable. Gensets come in various sizes and fuel types, including diesel, natural gas, and propane. Gensets automatically start when power is interrupted, supplying electricity until regular power is restored.

According to Central Electricity Authority, in FY 2022-23, the country's total renewable energy generation accounted for 203,552 million units (MU), with an annual growth rate of 19% compared to the previous year.

Market Dynamics:

Driver:

Rapid industrialization and urbanization

Rapid industrialization and urbanization augments the demand for reliable power backup solutions. Industries require uninterrupted power supply to sustain operations, driving the adoption of generator sets as backup power sources. Urbanization leads to increased infrastructure development, necessitating backup power for essential services like hospitals, data centers, and telecommunications. Moreover, urban areas often face grid instability, further emphasizing the need for gensets. Consequently, the market experiences steady growth as industries and urban centers prioritize reliable power supply to support their activities.

Restraint:

Environmental concerns

Environmental concerns regarding gensets primarily revolve around emissions of pollutants such as nitrogen oxides (NOx), carbon monoxide (CO), and particulate matter. These emissions contribute to air pollution and pose health risks. Additionally, gensets often rely on fossil fuels, leading to greenhouse gas emissions and exacerbating climate change. Stringent regulations impose compliance burdens on genset manufacturers, impacting production costs and pricing. As environmental consciousness grows, consumers increasingly favour eco-friendly alternatives, thus hindering market growth for traditional gensets.

Opportunity:

Rising investments in infrastructure projects

The infrastructure projects, ranging from construction and transportation to energy and telecommunications, require reliable backup power solutions to ensure uninterrupted operations. Gensets offer a dependable source of electricity during grid outages or in remote locations where grid access is limited. As governments and private enterprises allocate significant funds towards infrastructure development, the demand for gensets continues to surge. This trend is expected to sustain the expansion of the genset market, with manufacturers focusing on innovation and efficiency enhancements to meet evolving customer needs.

Threat:

High initial costs

Gensets entail high initial costs primarily due to the sophisticated engineering and manufacturing required to ensure reliability, efficiency, and compliance with stringent regulations. These costs encompass the purchase of high-quality components, advanced control systems, and rigorous testing to guarantee performance under various conditions. Such upfront expenses can deter potential buyers, especially in price-sensitive markets or regions with limited financial resources. The high initial costs act as a barrier to entry, potentially limiting the market growth.

Covid-19 Impact

The covid-19 pandemic significantly impacted the genset market as industries and businesses faced disruptions in operations and supply chains. Initially, there was a decline in demand due to economic uncertainties and lockdown measures. However, as businesses adapted to remote work and sought uninterrupted power supply, there was resurgence in demand for gensets, particularly in essential sectors such as healthcare, data centers, and telecommunications. This led to a shift towards increased investment in reliable power backup solutions to mitigate the risks posed by future disruptions.

The hybrid generators segment is expected to be the largest during the forecast period

The hybrid generators segment is estimated to have a lucrative growth, due to its efficiency, reduced fuel consumption, and lower emissions. By integrating components like solar panels, wind turbines, or batteries, hybrid gensets optimize power generation by utilizing renewable energy when available and relying on conventional fuel sources when necessary. This flexibility makes them ideal for off-grid applications, remote areas, or locations with unreliable grid infrastructure. Its environmental sustainability and suppleness factors make it a popular choice.

The industrial segment is expected to have the highest CAGR during the forecast period

The industrial segment is anticipated to witness the highest CAGR growth during the forecast period, due to the sustaining operations during grid outages or unstable power supply. In industries where uninterrupted electricity is essential for production processes, gensets ensure continuity and prevent costly downtime. Additionally, gensets offer flexibility in remote or off-grid locations where access to the main power grid is limited. Their usage enhances operational efficiency, safeguards against financial losses due to disruptions, and reinforces the overall resilience of industrial operations, supporting sustained productivity and competitiveness.

Region with largest share:

Asia Pacific is projected to hold the largest market share during the forecast period owing to increasing industrialization, urbanization, and the need for reliable power backup solutions. Countries like China, India, and Japan are driving this growth with rapid infrastructure development and rising demand for uninterrupted power supply. The market is characterized by a wide range of players offering diverse product portfolios catering to various end-user segments. Technological advancements, government initiatives, and growing awareness about energy efficiency are further fueling the expansion of the genset market in the Asia Pacific region.

Region with highest CAGR:

North America is projected to have the highest CAGR over the forecast period, owing to increasing demand for backup power solutions, stringent regulations pertaining to emissions, and growing awareness regarding the need for uninterrupted power supply. The United States and Canada dominate the market, driven by robust industrial infrastructure and commercial establishments. These factors, coupled with ongoing technological advancements and innovations, are expected to sustain the growth trajectory of the genset market in the North American region.

Key players in the market

Some of the key players profiled in the Genset Market include Kohler Corporation, Cummins Inc., Tata Motors, MTU Onsite Energy, Caterpillar Inc., Wartsila Corporation, Yanmar Limited, Mitsubishi Heavy Industries, Himoinsa Limited, Atlas Copco AB, Doosan Corporation, Kirloskar Electric Company Limited, Briggs & Stratton Corporation, Wacker Neuson SE, Rolls-Royce Power Systems AG, FG Wilson, Ingersoll Rand Inc., Sterling Generators Private Limited, John Deere and Generac Power Systems.

Key Developments:

In September 2023, Kirloskar Oil Engines (KOEL) announced the launch of its range of CPCB IV+ compliant gensets. With a focus on delivering high-performance, fuel-efficient, and environmentally responsible solutions, the new gensets meet the latest emission norms set by the Central Pollution Control Board (CPCB).

In July 2023, Tata Motors, India's leading automobile company, has launched the new-generation, cutting edge range of gensets in India. Backed by the reliable and technologically advanced CPCB IV+ (Central Pollution Control Board IV+) compliant Tata Motors engines, the high-performance gensets are available in 25kVA to 125kVA configurations.

Types Covered:

- Portable Generators

- Stationary Generators

- Hybrid Generators

- Other Types

Fuel Types Covered:

- Diesel

- Natural Gas

- Biogas

- Liquid Petroleum Gas (LPG)

- Other Fuel Types

Technologies Covered:

- Renewable Energy Integrated Gensets

- Microgrid Gensets

- Smart Gensets

- Other Technologies

Applications Covered:

- Prime Power

- Standby Power

- Peak Shaving

- Continuous Power

- Other Applications

End Users Covered:

- Residential

- Commercial

- Industrial

- Utilities

- Government & Defense

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Technology Analysis

- 3.7 Application Analysis

- 3.8 End User Analysis

- 3.9 Emerging Markets

- 3.10 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Genset Market, By Type

- 5.1 Introduction

- 5.2 Portable Generators

- 5.3 Stationary Generators

- 5.4 Hybrid Generators

- 5.5 Other Types

6 Global Genset Market, By Fuel Type

- 6.1 Introduction

- 6.2 Diesel

- 6.3 Natural Gas

- 6.4 Biogas

- 6.5 Liquid Petroleum Gas (LPG)

- 6.6 Other Fuel Types

7 Global Genset Market, By Technology

- 7.1 Introduction

- 7.2 Renewable Energy Integrated Gensets

- 7.3 Microgrid Gensets

- 7.4 Smart Gensets

- 7.5 Other Technologies

8 Global Genset Market, By Application

- 8.1 Introduction

- 8.2 Prime Power

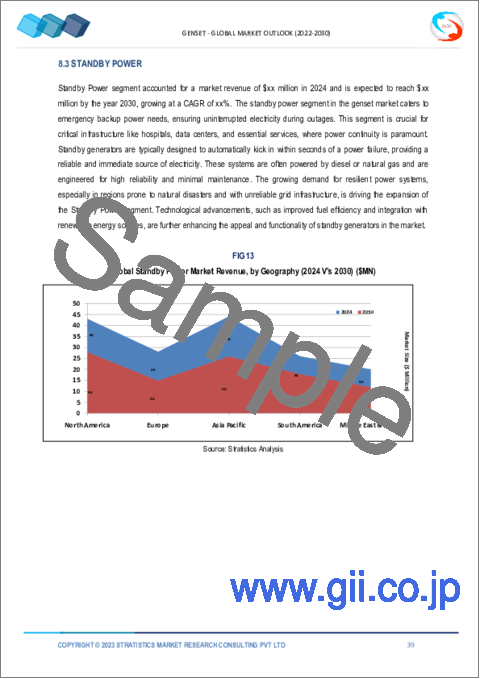

- 8.3 Standby Power

- 8.4 Peak Shaving

- 8.5 Continuous Power

- 8.6 Other Applications

9 Global Genset Market, By End User

- 9.1 Introduction

- 9.2 Residential

- 9.3 Commercial

- 9.4 Industrial

- 9.5 Utilities

- 9.6 Government & Defense

- 9.7 Other End Users

10 Global Genset Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.5 South America

- 10.5.1 Argentina

- 10.5.2 Brazil

- 10.5.3 Chile

- 10.5.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 Kohler Corporation

- 12.2 Cummins Inc.

- 12.3 Tata Motors

- 12.4 MTU Onsite Energy

- 12.5 Caterpillar Inc.

- 12.6 Wartsila Corporation

- 12.7 Yanmar Limited

- 12.8 Mitsubishi Heavy Industries

- 12.9 Himoinsa Limited

- 12.10 Atlas Copco AB

- 12.11 Doosan Corporation

- 12.12 Kirloskar Electric Company Limited

- 12.13 Briggs & Stratton Corporation

- 12.14 Wacker Neuson SE

- 12.15 Rolls-Royce Power Systems AG

- 12.16 FG Wilson

- 12.17 Ingersoll Rand Inc.

- 12.18 Sterling Generators Private Limited

- 12.19 John Deere

- 12.20 Generac Power Systems