|

|

市場調査レポート

商品コード

1438035

コンデンサ市場の2030年までの予測:製品タイプ別、実装タイプ別、電圧別、用途別、エンドユーザー別、地域別の世界分析Capacitor Market Forecasts to 2030 - Global Analysis By Product, Mounting Type, Voltage, Application, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| コンデンサ市場の2030年までの予測:製品タイプ別、実装タイプ別、電圧別、用途別、エンドユーザー別、地域別の世界分析 |

|

出版日: 2024年02月02日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、コンデンサの世界市場は、2023年に243億2,000万米ドルとなり、2030年までには346億7,000万米ドルに達すると予測され、予測期間中に7.9%のCAGRで成長する見込みです。

コンデンサは、電界に電気エネルギーを蓄える電子部品です。絶縁材料で仕切られた2枚の導電性プレートで構成され、電荷を素早く蓄えたり放出したりすることができます。コンデンサは電子回路において、電圧変動の平滑化、信号のフィルタリング、タイミングアプリケーションに不可欠です。コンデンサは電圧を調整し、回路内の電気信号の流れを制御することで、安定性と適切な機能を保証します。

GSMA Mobile Economy 2021によると、IoT機器向けの積層セラミックコンデンサ需要では、北米が51億個で2025年まで市場をリードすると予想されています。

電子機器の小型化

電子機器の小型化により、メーカーは小型で効率的なコンデンサを製造する必要に迫られています。電子機器の小型化・高機能化に伴い、エネルギー密度が高く、フォームファクターが小さく、性能が向上したコンデンサへの需要が高まっています。この動向はコンデンサ技術の進歩につながり、小型化された電子機器の進化する要件を満たそうと各社が努力する中で、市場における技術革新と競争を促進しています。

原材料コストの変動

コンデンサ業界は、アルミニウム、タンタル、セラミックなどの原材料に大きく依存しています。これらの原材料の不安定な価格変動は製造費用に影響を与え、生産コストの不確実性につながります。こうした不確実性が、コンデンサ・メーカーが安定した生産コストと価格戦略を維持することを困難にしています。その結果、コンデンサ業界はリスクと不確実性の増大に直面し、利益率と市場全体の安定性に影響を及ぼしています。

拡大する5G技術展開

より高い周波数とより速いデータ転送速度を必要とする5Gネットワークのインフラを維持するために、先進的なコンデンサがますます必要になってきています。5G機器の信頼性と有効性を維持するために、コンデンサは電気信号のフィルタリングと安定化に不可欠です。そのため、5G技術の急速な世界展開が高性能コンデンサへの需要を押し上げ、コンデンサ業界に新たな成長機会を生み出しています。

偽造品の増加

偽造品は製品の信頼性、安全性、性能を損ない、電子機器に潜在的な不具合をもたらします。このようなコンデンサ偽造品の急増は、消費者の信頼を損なうだけでなく、正規メーカーにとっても経済的な課題となります。偽造コンデンサの増加は、業界内の品質基準と規制遵守を維持するための課題にもなっています。したがって、この側面が市場の成長を妨げています。

COVID-19の影響

COVID-19の流行は市場に大きな影響を与えています。サプライチェーンの混乱、労働力不足、原材料価格の変動、製造能力の低下がコスト増と生産の遅れにつながっています。世界の景気減速は、特に自動車や家電といった産業における需要に影響を及ぼしています。課題にもかかわらず、遠隔通信や医療機器への依存度の増加により、ヘルスケア機器や技術インフラにおけるコンデンサ需要が増加しています。

予測期間中、電気化学コンデンサ分野が最大になる見込み

電気化学コンデンサ分野は有利な成長を遂げると推定されます。電気化学コンデンサは、静電電荷分離によって電気エネルギーを貯蔵・放出するエネルギー貯蔵デバイスです。高い静電容量を得るために、電解質と高表面積電極を使用します。高電力密度、長サイクル寿命、急速充電機能という独自の組み合わせにより、他のエネルギー貯蔵技術とは一線を画し、さまざまな技術用途や産業用途に汎用性の高いソリューションを提供しています。

予測期間中、コンシューマーエレクトロニクス分野のCAGRが最も高くなると予想されます。

コンシューマーエレクトロニクス分野は、予測期間中に最も高いCAGR成長が見込まれます。コンデンサは、コンシューマーエレクトロニクスにおいて、電気エネルギーの蓄積と放出、デバイス性能の向上という重要な役割を果たしています。コンデンサは電圧を安定させ、ノイズをフィルタリングし、力率補正を改善し、一貫した効率的な動作を保証します。全体として、コンデンサはコンシューマーエレクトロニクスの効率的で信頼性の高い機能に貢献し、性能を向上させ、干渉を減らし、電子機器の寿命を延ばします。

最大のシェアを占める地域

アジア太平洋は、電子機器、自動車用途、再生可能エネルギープロジェクトにおける需要の増加により、予測期間中最大の市場シェアを占めると予測されます。同地域の工業化の拡大、急速な技術進歩、家電消費の増加が市場の上昇に寄与しています。中国、日本、韓国、インドなどの主要経済国で構成されるこの地域では、エネルギー貯蔵、パワーエレクトロニクス、電子機器向けのコンデンサ採用が急増しています。インフラへの投資増加や再生可能エネルギープロジェクトへの注目の高まりが、市場の拡大にさらに貢献しています。

CAGRが最も高い地域:

北米は、エレクトロニクス、自動車、通信の各産業で需要が増加していることから、予測期間中に最もCAGRが高くなると予測されています。この地域には、Murata Manufacturing Limited、Illinois Capacitor、Panasonic Corporation、Eaton Corporationといった主要企業があります。技術の進歩、家電消費の増加、自動車セクターの拡大といった要因が市場拡大に寄与しています。さらに、米国とカナダにおける電子機器の小型化と効率化の推進が需要をさらに押し上げています。

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査ソース

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 製品分析

- アプリケーション分析

- エンドユーザー分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界のコンデンサ市場:製品別

- 電解コンデンサ

- セラミックコンデンサ

- タンタルコンデンサ

- フィルムコンデンサ

- 電気化学コンデンサ

- 可変コンデンサ

- その他の製品

第6章 世界のコンデンサ市場:実装タイプ別

- 表面実装型

- スルーホール

第7章 世界のコンデンサ市場:電圧別

- 500V以下

- 501~1000V

- 1001~2000V

- 2000V以上

第8章 世界のコンデンサ市場:用途別

- コンシューマーエレクトロニクス

- カーエレクトロニクス

- 産業用電子機器

- 電源システム

- 医療機器

- 防衛・航空宇宙

- 再生可能エネルギー

- 電気通信

- その他の用途

第9章 世界のコンデンサ市場:エンドユーザー別

- OEM(相手先商標製品製造業者)

- 電子部品販売業者

- 電子機器製造サービス(EMS)プロバイダー

- その他のエンドユーザー

第10章 世界のコンデンサ市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東・アフリカ

第11章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第12章 企業プロファイル

- Murata Manufacturing Limited

- TDK Corporation

- Nichicon Corporation

- Vishay Intertechnology Inc

- KEMET Corporation

- Panasonic Corporation

- AVX Corporation

- Rubycon Corporation

- Wurth Elektronik Group

- Nippon Chemi-Con Corporation

- Kyocera Corporation

- Cornell Dubilier Electronics Inc

- Yageo Corporation

- Samsung Electro-Mechanics Limited

- Illinois Capacitor Inc

- Rohm Semiconductor

- Tantalum Corporation

- CapXon International Electronic Limited

- Honeywell International

- Lelon Electronics Corporation

List of Tables

- Table 1 Global Capacitor Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Capacitor Market Outlook, By Product (2021-2030) ($MN)

- Table 3 Global Capacitor Market Outlook, By Electrolytic Capacitors (2021-2030) ($MN)

- Table 4 Global Capacitor Market Outlook, By Ceramic Capacitors (2021-2030) ($MN)

- Table 5 Global Capacitor Market Outlook, By Tantalum Capacitors (2021-2030) ($MN)

- Table 6 Global Capacitor Market Outlook, By Film Capacitors (2021-2030) ($MN)

- Table 7 Global Capacitor Market Outlook, By Electrochemical Capacitors (2021-2030) ($MN)

- Table 8 Global Capacitor Market Outlook, By Variable Capacitors (2021-2030) ($MN)

- Table 9 Global Capacitor Market Outlook, By Other Products (2021-2030) ($MN)

- Table 10 Global Capacitor Market Outlook, By Mounting Type (2021-2030) ($MN)

- Table 11 Global Capacitor Market Outlook, By Surface Mounted (2021-2030) ($MN)

- Table 12 Global Capacitor Market Outlook, By Through-Hole (2021-2030) ($MN)

- Table 13 Global Capacitor Market Outlook, By Voltage (2021-2030) ($MN)

- Table 14 Global Capacitor Market Outlook, By Up To 500 V (2021-2030) ($MN)

- Table 15 Global Capacitor Market Outlook, By 501 To 1000 V (2021-2030) ($MN)

- Table 16 Global Capacitor Market Outlook, By 1001 To 2000 V (2021-2030) ($MN)

- Table 17 Global Capacitor Market Outlook, By Above 2000 V (2021-2030) ($MN)

- Table 18 Global Capacitor Market Outlook, By Application (2021-2030) ($MN)

- Table 19 Global Capacitor Market Outlook, By Consumer Electronics (2021-2030) ($MN)

- Table 20 Global Capacitor Market Outlook, By Automotive Electronics (2021-2030) ($MN)

- Table 21 Global Capacitor Market Outlook, By Industrial Electronics (2021-2030) ($MN)

- Table 22 Global Capacitor Market Outlook, By Power Supply Systems (2021-2030) ($MN)

- Table 23 Global Capacitor Market Outlook, By Medical Devices (2021-2030) ($MN)

- Table 24 Global Capacitor Market Outlook, By Defense & Aerospace (2021-2030) ($MN)

- Table 25 Global Capacitor Market Outlook, By Renewable Energy (2021-2030) ($MN)

- Table 26 Global Capacitor Market Outlook, By Telecommunications (2021-2030) ($MN)

- Table 27 Global Capacitor Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 28 Global Capacitor Market Outlook, By End User (2021-2030) ($MN)

- Table 29 Global Capacitor Market Outlook, By Original Equipment Manufacturers (OEMs) (2021-2030) ($MN)

- Table 30 Global Capacitor Market Outlook, By Electronic Component Distributors (2021-2030) ($MN)

- Table 31 Global Capacitor Market Outlook, By Electronics Manufacturing Services (EMS) Providers (2021-2030) ($MN)

- Table 32 Global Capacitor Market Outlook, By Other End Users (2021-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Capacitor Market is accounted for $24.32 billion in 2023 and is expected to reach $34.67 billion by 2030 growing at a CAGR of 7.9% during the forecast period. A capacitor is an electronic component that stores electrical energy in an electric field. Comprising two conductive plates separated by an insulating material, it can store and release charge rapidly. Capacitors are vital in electronic circuits for smoothing voltage fluctuations, filtering signals, and timing applications. Capacitors ensures stability and proper functioning by regulating voltage and controlling the flow of electrical signals within circuits.

According to GSMA Mobile Economy 2021, in terms of multilayer ceramic capacitor demand for IoT devices, North America is expected to lead the market through 2025 with 5.1 billion.

Market Dynamics:

Driver:

Miniaturization of electronic devices

The miniaturization of electronic devices has been compelling manufacturers to produce compact and efficient capacitors. As electronic devices become smaller and more sophisticated, there is an increasing demand for capacitors with higher energy density, smaller form factors, and improved performance. This trend has led to advancements in capacitor technology, fostering innovation and competition in the market as companies strive to meet the evolving requirements of miniaturized electronics.

Restraint:

Fluctuations in raw material costs

The capacitor industry heavily relies on materials like aluminum, tantalum, and ceramics. Volatile price movements in these raw materials impact manufacturing expenses, leading to uncertain production costs. These uncertainties make it challenging for capacitor manufacturers to maintain stable production costs and pricing strategies. Consequently, the capacitor industry faces increased risks and uncertainties, impacting profit margins and overall market stability.

Opportunity:

Growing 5G technology deployment

Advanced capacitors are becoming more and more necessary to sustain the infrastructure of 5G networks, which require higher frequencies and quicker data transfer rates. In order to maintain the dependability and effectiveness of 5G equipment, capacitors are essential for filtering and stabilizing electrical signals. Thereby, the rapid global rollout of 5G technology is driving up demand for high-performance capacitors, creating new growth opportunities in the capacitor industry.

Threat:

Rising availability of counterfeit products

Counterfeits undermine product reliability, safety, and performance, leading to potential malfunctions in electronic devices. This surge in counterfeit capacitor production not only jeopardizes consumer trust but also poses economic challenges for legitimate manufacturers. The rise in counterfeit capacitors also challenges efforts to maintain quality standards and regulatory compliance within the industry. Therefore, this aspect is hampering the market growth.

Covid-19 Impact

The covid-19 pandemic has significantly impacted the market. Supply chain disruptions, labor shortages, fluctuations in raw material prices and reduced manufacturing capacity have led to increased costs and delays in production. The global economic slowdown has affected demand, particularly in industries like automotive and consumer electronics. Despite challenges, there's a growing demand for capacitors in healthcare equipment and technology infrastructure, driven by increased reliance on remote communication and medical devices.

The electrochemical capacitors segment is expected to be the largest during the forecast period

The electrochemical capacitors segment is estimated to have a lucrative growth. Electrochemical capacitors are energy storage devices that store and release electrical energy through electrostatic charge separation. They use electrolytes and high surface area electrodes to achieve higher capacitance. Their unique combination of high power density, long cycle life, and fast charging capabilities distinguishes them from other energy storage technologies, providing versatile solutions for various technological and industrial applications.

The consumer electronics segment is expected to have the highest CAGR during the forecast period

The consumer electronics segment is anticipated to witness the highest CAGR growth during the forecast period. Capacitors play a crucial role in consumer electronics by storing and releasing electrical energy, enhancing device performance. They stabilize voltage, filter out noise, and improve power factor correction, ensuring consistent and efficient operation. Overall, capacitors contribute to the efficient and reliable functioning of consumer electronics, improving performance, reducing interference, and extending the lifespan of electronic devices.

Region with largest share:

Asia Pacific is projected to hold the largest market share during the forecast period owing to the increasing demand in electronic devices, automotive applications, and renewable energy projects. The region's expanding industrialization, rapid technological advancements, and rising consumer electronics consumption contribute to the market's upward trajectory. The region, comprising key economies like China, Japan, South Korea, and India, is witnessing a surge in capacitor adoption for energy storage, power electronics, and electronic devices. Rising investments in infrastructure and the growing focus on renewable energy projects further contribute to the market's expansion.

Region with highest CAGR:

North America is projected to have the highest CAGR over the forecast period, owing to the augmented demand across electronics, automotive, and telecommunications industries. The region is home to key players namely Murata Manufacturing, Illinois Capacitor, Panasonic Corporation and Eaton Corporation. Factors such as technological advancements, rising consumer electronics consumption, and the automotive sector's expansion contribute to market expansion. Additionally, the push towards miniaturization and increased efficiency in electronic devices in the US and Canada are further fuelling the demand.

Key players in the market

Some of the key players profiled in the Capacitor Market include Murata Manufacturing Limited, TDK Corporation, Nichicon Corporation, Vishay Intertechnology Inc, KEMET Corporation, Panasonic Corporation, AVX Corporation, Rubycon Corporation, Wurth Elektronik Group, Nippon Chemi-Con Corporation, Kyocera Corporation, Cornell Dubilier Electronics Inc, Yageo Corporation, Samsung Electro-Mechanics Limited, Illinois Capacitor Inc, Rohm Semiconductor, Tantalum Corporation, CapXon International Electronic Limited, Honeywell International and Lelon Electronics Corporation.

Key Developments:

In November 2023, ROHM has developed the BTD1RVFL series, a new line of silicon capacitors. By utilizing thin-film technology, their silicon capacitors offer a greater capacitance in a thinner form compared to the current multilayer ceramic capacitors (MLCCs) available in the market.

In April 2023, Kyocera Corporation announced that the company's Electronic Components Division developed a new capacitor (MLCC) with EIA 0201 size, with a capacitance of 10 microfarads, which the company claims to be the industry's highest among MLCCs in the 0201 case size. The dimensions of the capacitor are 0.6 mm x 0.3 mm.

In February 2022, Murata launched the NFM15HC435D0E3 MLCC, designed with 3 terminals to provide a capacitance of 4.3 F. The capacitor is designed for automotive applications to attain results on noise removal and superior decoupling that are required for high-performance processors employed in advanced driver assistance systems and autonomous driving functions.

Products Covered:

- Electrolytic Capacitors

- Ceramic Capacitors

- Tantalum Capacitors

- Film Capacitors

- Electrochemical Capacitors

- Variable Capacitors

- Other Products

Mounting Types Covered:

- Surface Mounted

- Through-Hole

Voltages Covered:

- Up To 500 V

- 501 To 1000 V

- 1001 To 2000 V

- Above 2000 V

Applications Covered:

- Consumer Electronics

- Automotive Electronics

- Industrial Electronics

- Power Supply Systems

- Medical Devices

- Defense & Aerospace

- Renewable Energy

- Telecommunications

- Other Applications

End Users Covered:

- Original Equipment Manufacturers (OEMs)

- Electronic Component Distributors

- Electronics Manufacturing Services (EMS) Providers

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Product Analysis

- 3.7 Application Analysis

- 3.8 End User Analysis

- 3.9 Emerging Markets

- 3.10 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Capacitor Market, By Product

- 5.1 Introduction

- 5.2 Electrolytic Capacitors

- 5.3 Ceramic Capacitors

- 5.4 Tantalum Capacitors

- 5.5 Film Capacitors

- 5.6 Electrochemical Capacitors

- 5.7 Variable Capacitors

- 5.8 Other Products

6 Global Capacitor Market, By Mounting Type

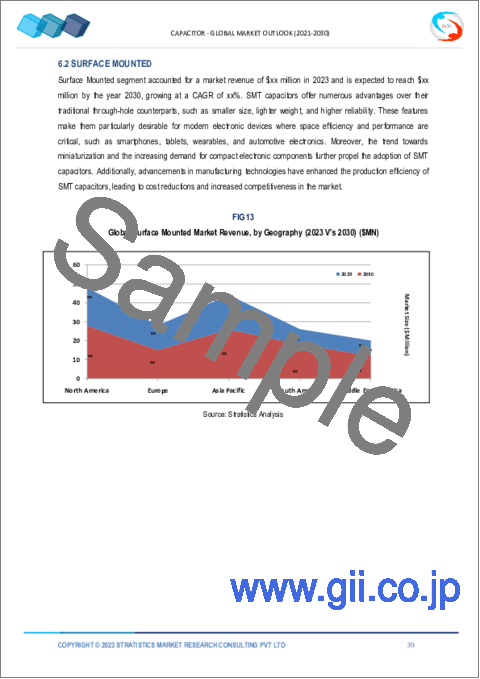

- 6.1 Introduction

- 6.2 Surface Mounted

- 6.3 Through-Hole

7 Global Capacitor Market, By Voltage

- 7.1 Introduction

- 7.2 Up To 500 V

- 7.3 501 To 1000 V

- 7.4 1001 To 2000 V

- 7.5 Above 2000 V

8 Global Capacitor Market, By Application

- 8.1 Introduction

- 8.2 Consumer Electronics

- 8.3 Automotive Electronics

- 8.4 Industrial Electronics

- 8.5 Power Supply Systems

- 8.6 Medical Devices

- 8.7 Defense & Aerospace

- 8.8 Renewable Energy

- 8.9 Telecommunications

- 8.10 Other Applications

9 Global Capacitor Market, By End User

- 9.1 Introduction

- 9.2 Original Equipment Manufacturers (OEMs)

- 9.3 Electronic Component Distributors

- 9.4 Electronics Manufacturing Services (EMS) Providers

- 9.5 Other End Users

10 Global Capacitor Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.5 South America

- 10.5.1 Argentina

- 10.5.2 Brazil

- 10.5.3 Chile

- 10.5.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 Murata Manufacturing Limited

- 12.2 TDK Corporation

- 12.3 Nichicon Corporation

- 12.4 Vishay Intertechnology Inc

- 12.5 KEMET Corporation

- 12.6 Panasonic Corporation

- 12.7 AVX Corporation

- 12.8 Rubycon Corporation

- 12.9 Wurth Elektronik Group

- 12.10 Nippon Chemi-Con Corporation

- 12.11 Kyocera Corporation

- 12.12 Cornell Dubilier Electronics Inc

- 12.13 Yageo Corporation

- 12.14 Samsung Electro-Mechanics Limited

- 12.15 Illinois Capacitor Inc

- 12.16 Rohm Semiconductor

- 12.17 Tantalum Corporation

- 12.18 CapXon International Electronic Limited

- 12.19 Honeywell International

- 12.20 Lelon Electronics Corporation