|

|

市場調査レポート

商品コード

1351081

自動車エンジニアリングサービス市場の2030年までの予測- タイプ別、車両タイプ別、場所別、サービスタイプ別、推進力別、自然タイプ別、用途別、地域別の世界分析Automotive Engineering Services Market Forecasts to 2030 - Global Analysis By Type, Vehicle Type, Location, Service Type, Propulsion, Nature Type, Application and By Geography |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 自動車エンジニアリングサービス市場の2030年までの予測- タイプ別、車両タイプ別、場所別、サービスタイプ別、推進力別、自然タイプ別、用途別、地域別の世界分析 |

|

出版日: 2023年09月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 175+ Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、自動車エンジニアリングサービスの世界市場は2023年に1,656億米ドルを占め、予測期間中のCAGRは8.1%で2030年には2,856億6,000万米ドルに達すると予測されています。

自動車部品の作成、設計、試作は、自動車エンジニアリングサービスの主な用途です。これらのサービスには、システム統合、仮想テスト、乗用車や商用車の生産も含まれます。さらに、これらのサービスは製造を強化し、追加コストを削減するように設計されています。コンセプト段階から実際の生産段階に至るまで、特定のシステムや車両の特定の部分の開発、設計、プロトタイプ作成、システム統合、テストなどのサービスから構成されます。

ブルームバーグNEFの報告書によると、2020年には米国が300台であるのに対し、中国は42万1,000台の電気バスを保有します。2025年には60万台に達すると予想されています。保有台数が増えれば、電気、電子、車体制御の専門的なエンジニアリング・ソリューションが必要になります。

技術の進歩

電気自動車(EV)、自律走行、ADAS(先進運転支援システム)、コネクティビティなどは、自動車業界で進んだ技術革新のほんの一部に過ぎないです。複雑なシステムを設計し、統合するために、これらの進歩には専門的なエンジニアリング・スキルが必要です。EVを作るためには、エンジニアはパワーエレクトロニクス、充電インフラ、バッテリー技術に精通していなければならないです。さらに、自律走行にはリアルタイム制御システム、センサーフュージョン、機械学習の専門知識が必要です。コネクティビティの推進には、安全な通信プロトコル、エンターテインメント・プログラム、テレマティクス・ソリューションの構築が含まれます。

高額な初期投資

先進自動車技術の開発には多額の初期投資が必要です。小規模なエンジニアリング・サービス・プロバイダーや市場に新規参入する企業にとっては、インフラ、研究開発、その他の関連費用の捻出が困難となる可能性があります。さらに、成果が出る前に研究開発のために多額の資金を確保しなければならない場合、キャッシュフローに影響を与え、潜在的な参加者が革新的プロジェクトへの参加を躊躇する可能性もあります。

自律的技術の開発

エンジニアリング・サービス・プロバイダーは、自律走行車の開発によってもたらされるさまざまな機会を活用し、自動車産業の将来の進路に影響を与えることができます。これらの企業は、センサーの統合を進め、ライダーとレーダー技術を強化し、知覚と意思決定アルゴリズムを改善し、実際のシナリオを想定したシミュレーションベースのテストを実施し、厳格な安全性検証手順を通じて信頼できる自律走行ソリューションを確立するユニークな立場にあります。さらに、テクノロジーとイノベーションの接点でモビリティのパラメーターを再定義することで、車両が安全を確保しながら都市の複雑性をシームレスにナビゲートする未来を形作ろうとしています。

破壊的技術

電気自動車(EV)、自律走行システム、コネクティビティ・ソリューションは、その急速な融合が技術開発のペースを加速させ、従来の自動車事情を根本から変える可能性を秘めたイノベーションのほんの一例に過ぎないです。伝統的な調査手法に根ざしているエンジニアリング・サービス・プロバイダーにとっては、今が正念場です。しかし、より機敏で先見の明のある競合他社に駆逐されるという迫り来る脅威にさらされるだけでなく、こうした変革的な技術を迅速にピボットして自社の製品に取り入れることができないため、市場の関連性が薄れるリスクにもさらされています。

COVID-19の影響:

COVID-19の大流行は、自動車産業を含む多くの産業に大きな混乱をもたらしました。さらに、自動車市場は、操業停止、サプライチェーンの混乱、消費者需要の減少、操業上の困難によって深刻な影響を受けています。制限のため、自動車の生産と販売に後退が生じ、デジタル・ソリューションとリモートワークに焦点が変わっています。電気自動車や自律走行車の動向が加速したことに加え、パンデミックによって一部のプロジェクトが遅延し、コスト削減を余儀なくされました。回復にはワクチンの配布、経済成長、適応的な景観ナビゲーション技術などが必要です。

予測期間中、社内セグメントが最大となる見込み

予測期間中、自動車エンジニアリングサービス市場では、社内セグメントが最大のシェアを占めると予想されます。同市場は、自動車メーカーが自社の資産やインフラを活用しながら、社内のエンジニアリングや調査業務を行うことを意味します。企業が設計、開発、イノベーションをよりコントロールできるようにすることで、この戦略はしばしば独自の進歩をもたらします。さらに、知識の保持を改善し、各部門間のシームレスなコラボレーションを可能にすることもできます。

予測期間中、設計分野のCAGRが最も高くなる見込み

予測期間中、設計分野のCAGRが最も高くなると予想されます。これは、メーカーが設計の研究開発への投資を増やし、エンジニアリング・サービス・プロバイダーと協力して、消費者向けに最先端の自動車機能を作り出そうとしている結果です。さらにメーカー各社は、パワーウェイトレシオのバランスを取るため、長くて広い室内空間を持つ自動車の生産に重点を置いています。

最もシェアの高い地域:

自動車エンジニアリングサービスに関しては、アジア太平洋地域が最大の市場シェアを占めると予想されます。これは、大規模な自動車OEMが存在することに加え、安価な労働力が利用できるため、インド、韓国、中国といった国々に生産や関連業務をアウトソーシングしていることに起因しています。さらに、自動車ESOプロバイダーはこの分野に力を注ぎ、その結果、アジア太平洋地域に事業拠点を移しました。低コスト国の総労働力の約30%はインドが供給しています。欧州、ラテンアメリカ、北米の国々と比べると、インドは15~26%のコスト優位性を持っています。世界中のさまざまなセグメントのニーズに応える世界なOEMは、インドが非常に競争力の高い市場であることに気づいています。

CAGRが最も高い地域:

予測期間中、CAGRが最も高くなると予想されるのは南米地域です。この地域では、好調な自動車産業と急成長する経済に牽引され、ブラジルの自動車エンジニアリングサービスの成長が顕著です。ブラジルは、大規模な消費者基盤、自動車需要の増加、電気自動車や持続可能なモビリティ・ソリューションへの関心の高まりにより、高い成長を遂げています。さらに、ブラジルは、技術革新、研究開発、外国投資の誘致に力を入れており、この地域の自動車業界において主要なプレーヤーとなっています。

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレーヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査ソース

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- アプリケーション分析

- 新興市場

- 新型コロナウイルス感染症(COVID-19)の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の自動車エンジニアリングサービス市場:タイプ別

- 機械式

- 埋め込み

- ソフトウェア

- その他のタイプ

第6章 世界の自動車エンジニアリングサービス市場:車両タイプ別

- 乗用車

- 小型商用車

- 大型商用車

- その他の車種

第7章 世界の自動車エンジニアリングサービス市場:場所別

- 社内

- 外注

- その他の場所

第8章 世界の自動車エンジニアリングサービス市場:サービスタイプ別

- コンセプト・調査

- テストと診断

- デザインする

- 接続性

- プロトタイピング

- システム統合

- テスト

- その他のサービスタイプ

第9章 世界の自動車エンジニアリングサービス市場:推進力別

- ICE

- 電気

- その他の推進力

第10章 世界の自動車エンジニアリングサービス市場:自然タイプ別

- ボディリース

- ターンキー

- 他の自然タイプ

第11章 世界の自動車エンジニアリングサービス市場:用途別

- 先進運転支援システム

- 電気、電子、車体制御

- シャーシ

- 接続サービス

- 内装・外装・車体エンジニアリング

- インフォテイメントシステム

- パワートレインとエキゾースト

- シミュレーション

- 電池の開発と管理

- 充電器のテスト

- モーター制御

- その他の用途

第12章 世界の自動車エンジニアリングサービス市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第13章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第14章 企業プロファイル

- HCL Technologies

- Onward Technologies Ltd.

- Tata Technologies Ltd.

- Altair Engineering Inc.

- Harman International Industries, Inc.

- Siemens AG

- EPAM Systems

- Capgemini

- Horiba, Ltd.

- Robert Bosch GmbH

- Pilot Systems International

- Magna International Inc.

- Tech Mahindra Limited

- Assystem Technologies

- L&T Technology

- T-NET JAPAN Co., Ltd.

- Altran Technologies SA

- EDAG Engineering GmbH

- Hunter Engineering Company

- DesignTech Systems.

List of Tables

- Table 1 Global Automotive Engineering Services Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Automotive Engineering Services Market Outlook, By Type (2021-2030) ($MN)

- Table 3 Global Automotive Engineering Services Market Outlook, By Mechanical (2021-2030) ($MN)

- Table 4 Global Automotive Engineering Services Market Outlook, By Embedded (2021-2030) ($MN)

- Table 5 Global Automotive Engineering Services Market Outlook, By Software (2021-2030) ($MN)

- Table 6 Global Automotive Engineering Services Market Outlook, By Other Types (2021-2030) ($MN)

- Table 7 Global Automotive Engineering Services Market Outlook, By Vehicle Type (2021-2030) ($MN)

- Table 8 Global Automotive Engineering Services Market Outlook, By Passenger Cars (2021-2030) ($MN)

- Table 9 Global Automotive Engineering Services Market Outlook, By Light Commercial Vehicles (2021-2030) ($MN)

- Table 10 Global Automotive Engineering Services Market Outlook, By Heavy Commercial Vehicles (2021-2030) ($MN)

- Table 11 Global Automotive Engineering Services Market Outlook, By Other Vehicle Types (2021-2030) ($MN)

- Table 12 Global Automotive Engineering Services Market Outlook, By Location (2021-2030) ($MN)

- Table 13 Global Automotive Engineering Services Market Outlook, By In-house (2021-2030) ($MN)

- Table 14 Global Automotive Engineering Services Market Outlook, By Outsource (2021-2030) ($MN)

- Table 15 Global Automotive Engineering Services Market Outlook, By Other Locations (2021-2030) ($MN)

- Table 16 Global Automotive Engineering Services Market Outlook, By Service Type (2021-2030) ($MN)

- Table 17 Global Automotive Engineering Services Market Outlook, By Concept/Research (2021-2030) ($MN)

- Table 18 Global Automotive Engineering Services Market Outlook, By Testing & Diagnostics (2021-2030) ($MN)

- Table 19 Global Automotive Engineering Services Market Outlook, By Designing (2021-2030) ($MN)

- Table 20 Global Automotive Engineering Services Market Outlook, By Connectivity (2021-2030) ($MN)

- Table 21 Global Automotive Engineering Services Market Outlook, By Prototyping (2021-2030) ($MN)

- Table 22 Global Automotive Engineering Services Market Outlook, By System Integration (2021-2030) ($MN)

- Table 23 Global Automotive Engineering Services Market Outlook, By Testing (2021-2030) ($MN)

- Table 24 Global Automotive Engineering Services Market Outlook, By Other Service Types (2021-2030) ($MN)

- Table 25 Global Automotive Engineering Services Market Outlook, By Propulsion (2021-2030) ($MN)

- Table 26 Global Automotive Engineering Services Market Outlook, By ICE (2021-2030) ($MN)

- Table 27 Global Automotive Engineering Services Market Outlook, By Electric (2021-2030) ($MN)

- Table 28 Global Automotive Engineering Services Market Outlook, By Other Propulsions (2021-2030) ($MN)

- Table 29 Global Automotive Engineering Services Market Outlook, By Nature Type (2021-2030) ($MN)

- Table 30 Global Automotive Engineering Services Market Outlook, By Body Leasing (2021-2030) ($MN)

- Table 31 Global Automotive Engineering Services Market Outlook, By Turnkey (2021-2030) ($MN)

- Table 32 Global Automotive Engineering Services Market Outlook, By Other Nature Types (2021-2030) ($MN)

- Table 33 Global Automotive Engineering Services Market Outlook, By Application (2021-2030) ($MN)

- Table 34 Global Automotive Engineering Services Market Outlook, By Advanced Driver-assistance Systems (2021-2030) ($MN)

- Table 35 Global Automotive Engineering Services Market Outlook, By Electrical, Electronics, and Body Controls (2021-2030) ($MN)

- Table 36 Global Automotive Engineering Services Market Outlook, By Chassis (2021-2030) ($MN)

- Table 37 Global Automotive Engineering Services Market Outlook, By Connectivity Services (2021-2030) ($MN)

- Table 38 Global Automotive Engineering Services Market Outlook, By Interior, Exterior, and Body Engineering (2021-2030) ($MN)

- Table 39 Global Automotive Engineering Services Market Outlook, By Infotainment Systems (2021-2030) ($MN)

- Table 40 Global Automotive Engineering Services Market Outlook, By Powertrain and Exhaust (2021-2030) ($MN)

- Table 41 Global Automotive Engineering Services Market Outlook, By Simulation (2021-2030) ($MN)

- Table 42 Global Automotive Engineering Services Market Outlook, By Battery Development and Management (2021-2030) ($MN)

- Table 43 Global Automotive Engineering Services Market Outlook, By Charger Testing (2021-2030) ($MN)

- Table 44 Global Automotive Engineering Services Market Outlook, By Motor Controls (2021-2030) ($MN)

- Table 45 Global Automotive Engineering Services Market Outlook, By Other Applications (2021-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Automotive Engineering Services Market is accounted for $165.60 billion in 2023 and is expected to reach $285.66 billion by 2030 growing at a CAGR of 8.1% during the forecast period. Creating, designing, and prototyping automotive parts are the main use of automotive engineering services. These services also include system integration, virtual testing, and the production of passenger cars and commercial vehicles. Additionally, these services are designed to enhance manufacturing and lower additional costs. It consists of services such as developing, designing, prototyping, system integration, and testing a specific system or a specific part of a vehicle from the concept stage to the actual production stage.

According to a report by Bloomberg NEF, China has a fleet of 421,000 electric buses compared to 300 in the US in 2020. The number is expected to reach 600,000 by 2025. More fleets would require specialized engineering solutions for electric, electronics, and body controls.

Market Dynamics:

Driver:

Advancements in technology

Electric cars (EVs), autonomous driving, advanced driver assistance systems (ADAS), connectivity, and other innovations are just a few of the technological innovations that have been made in the automotive industry. In order to design and integrate complex systems, these advancements call for specialized engineering skills. Engineers must be knowledgeable about power electronics, charging infrastructure, and battery technology in order to create EVs. Moreover, real-time control systems, sensor fusion, and machine learning expertise are necessary for autonomous driving. The drive for connectivity includes the creation of safe communication protocols, entertainment programs, and telematics solutions.

Restraint:

High initial expenditure

Large initial investments are necessary to develop advanced automotive technologies. Smaller engineering services providers or newcomers to the market may find it difficult to afford the costs of infrastructure, R&D, and other related expenses. Additionally, it can affect cash flow and possibly deter potential participants from taking part in innovative projects if significant funding must be set aside for R&D before seeing results.

Opportunity:

Development of autonomous technology

Engineering service providers can take advantage of the wide range of opportunities presented by the development of autonomous vehicles to influence the future course of the automotive industry. These companies are in a unique position to advance sensor integration, enhance lidar and radar technology, improve perception and decision-making algorithms, carry out simulation-based testing for actual scenarios, and establish trustworthy autonomous solutions through rigorous safety validation procedures. Moreover, they are shaping a future where vehicles seamlessly navigate through urban complexity while ensuring safety, redefining the parameters of mobility at the nexus of technology and innovation.

Threat:

Disruptive technologies

Electric vehicles (EVs), autonomous systems, and connectivity solutions are just a few examples of the innovations whose rapid convergence are accelerating the pace of technological development and have the potential to fundamentally alter the conventional automotive landscape. Now is a crucial time for engineering service providers who are rooted in traditional methodologies. However, in addition to exposing them to the looming threat of being eclipsed by more nimble and visionary competitors, their inability to quickly pivot and incorporate these transformative technologies into their offerings exposes them to the risk of fading market relevance.

COVID-19 Impact:

The COVID-19 pandemic has significantly disrupted many industries, including the automotive industry. Moreover, the automotive market has been severely impacted by lockdowns, supply chain disruptions, decreased consumer demand, and operational difficulties. Due to limitations, there were setbacks in vehicle production and sales, which changed the focus to digital solutions and remote work. In addition to accelerating trends in electric and autonomous vehicles, the pandemic also delayed some projects and forced cost-cutting measures. Distribution of vaccines, economic growth, and adaptive landscape navigation techniques are all necessary for recovery.

The In-house segment is expected to be the largest during the forecast period

During the forecast period, it is anticipated that the In-House segment will hold the largest share in the automotive engineering services market. The market alludes to the practice of automakers conducting internal engineering and research tasks while utilizing their own assets and infrastructure. By allowing businesses to exercise more control over design, development, and innovation, this strategy frequently results in proprietary advancements. Additionally, it can improve knowledge retention and enable seamless collaboration between various departments.

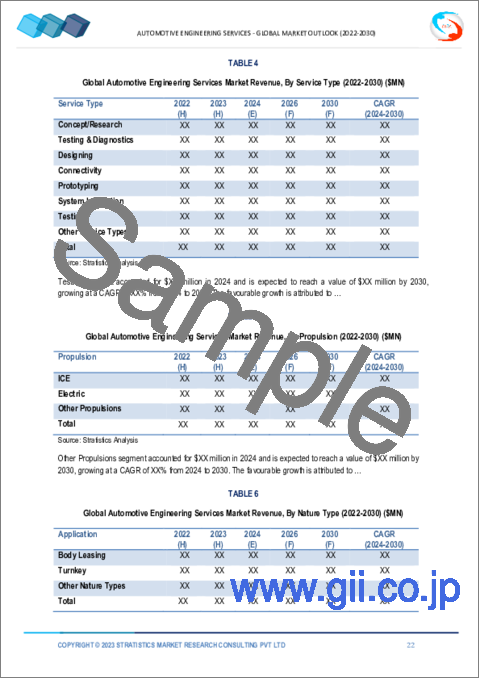

The designing segment is expected to have the highest CAGR during the forecast period

During the forecast period, the designing segment is anticipated to have the highest CAGR. This is a result of the manufacturers' increasing investments in designing R&D and working with engineering service providers to create cutting-edge automotive features for consumers. Moreover, manufacturers are placing a strong emphasis on producing vehicles with long and spacious interiors in order to balance power-to-weight ratios.

Region with largest share:

In terms of automotive engineering services, it is anticipated that the Asia-Pacific region will hold the largest market share. This is attributed to the existence of sizable auto OEMs as well as the outsourcing of production and related operations to nations like India, South Korea, and China due to the availability of cheap labor. Furthermore, automobile ESO providers have concentrated their efforts in this area and moved their operations to the Asia-Pacific region as a result. Around 30% of the total labor force in low-cost nations is supplied by India. Compared to nations in Europe, Latin America, and North America, India has a cost advantage of 15-26%. Global OEMs serving the needs of various segments around the world have found India to be a highly competitive market.

Region with highest CAGR:

The South American region is expected to have the highest CAGR over the course of the forecast period. In this region, Brazil's growth in automotive engineering services has been notable, driven by its strong automotive industry and burgeoning economy. The nation has experienced higher growth as a result of its sizable consumer base, rising vehicle demand, and growing interest in electric and sustainable mobility solutions. Moreover, Brazil has become a major player in the regional automotive landscape as a result of its emphasis on innovation, research, and development, as well as its efforts to draw in foreign investment.

Key players in the market:

Some of the key players in Automotive Engineering Services Market include: HCL Technologies, Onward Technologies Ltd, Tata Technologies Ltd., Altair Engineering Inc., Harman International Industries, Inc., Siemens AG, EPAM Systems, Capgemini, Horiba, Ltd., Robert Bosch GmbH, Pilot Systems International, Magna International Inc., Tech Mahindra Limited, Assystem Technologies, L&T Technology, T-NET JAPAN Co., Ltd., Altran Technologies SA, EDAG Engineering GmbH, Hunter Engineering Company and DesignTech Systems.

Key Developments:

In July 2023, Tata Technologies, an engineering and product development digital services company, has signed a 10-year Memorandum of Agreement (MoA) with the government of Chhattisgarh to modernise 36 government-owned ITIs in the state with a total project cost of Rs 1188.36 crore.

In June 2023, Robert Bosch GmbH has signed a PowerCell agreement with to manufacture the fuel cell stack S3 for PowerCell. PowerCell thereby increases its production capacity significantly and focuses on scaling up the assembly and deliveries of fuel cell systems as well as development of the next generation of fuel cell stacks.

In January 2023, Siemens Energy plans to boost its cooperation with Iraq in the coming years, the company said on Friday, as its CEO inked a deal with the Iraqi government to develop the country's power network. Siemens Energy CEO Christian Bruch signed a memorandum of understanding with Iraqi Electricity Minister Ziyad Ali to provide an additional 11 gigawatts for local power production, a statement from the German Economy Ministry said.

Types Covered:

- Mechanical

- Embedded

- Software

- Other Types

Vehicle Types Covered:

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Other Vehicle Types

Locations Covered:

- In-house

- Outsource

- Other Locations

Service Types Covered:

- Concept/Research

- Testing & Diagnostics

- Designing

- Connectivity

- Prototyping

- System Integration

- Testing

- Other Service Types

Propulsions Covered:

- ICE

- Electric

- Other Propulsions

Nature Types Covered:

- Body Leasing

- Turnkey

- Other Nature Types

Applications Covered:

- Advanced Driver-assistance Systems

- Electrical, Electronics, and Body Controls

- Chassis

- Connectivity Services

- Interior, Exterior, and Body Engineering

- Infotainment Systems

- Powertrain and After-treatment

- Simulation

- Battery Development and Management

- Charger Testing

- Motor Controls

- Other Applications

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Automotive Engineering Services Market, By Type

- 5.1 Introduction

- 5.2 Mechanical

- 5.3 Embedded

- 5.4 Software

- 5.5 Other Types

6 Global Automotive Engineering Services Market, By Vehicle Type

- 6.1 Introduction

- 6.2 Passenger Cars

- 6.3 Light Commercial Vehicles

- 6.4 Heavy Commercial Vehicles

- 6.5 Other Vehicle Types

7 Global Automotive Engineering Services Market, By Location

- 7.1 Introduction

- 7.2 In-house

- 7.3 Outsource

- 7.4 Other Locations

8 Global Automotive Engineering Services Market, By Service Type

- 8.1 Introduction

- 8.2 Concept/Research

- 8.3 Testing & Diagnostics

- 8.4 Designing

- 8.5 Connectivity

- 8.6 Prototyping

- 8.7 System Integration

- 8.8 Testing

- 8.9 Other Service Types

9 Global Automotive Engineering Services Market, By Propulsion

- 9.1 Introduction

- 9.2 ICE

- 9.3 Electric

- 9.4 Other Propulsions

10 Global Automotive Engineering Services Market, By Nature Type

- 10.1 Introduction

- 10.2 Body Leasing

- 10.3 Turnkey

- 10.4 Other Nature Types

11 Global Automotive Engineering Services Market, By Application

- 11.1 Introduction

- 11.2 Advanced Driver-assistance Systems

- 11.3 Electrical, Electronics, and Body Controls

- 11.4 Chassis

- 11.5 Connectivity Services

- 11.6 Interior, Exterior, and Body Engineering

- 11.7 Infotainment Systems

- 11.8 Powertrain and Exhaust

- 11.9 Simulation

- 11.10 Battery Development and Management

- 11.11 Charger Testing

- 11.12 Motor Controls

- 11.13 Other Applications

12 Global Automotive Engineering Services Market, By Geography

- 12.1 Introduction

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.2.3 Mexico

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 Italy

- 12.3.4 France

- 12.3.5 Spain

- 12.3.6 Rest of Europe

- 12.4 Asia Pacific

- 12.4.1 Japan

- 12.4.2 China

- 12.4.3 India

- 12.4.4 Australia

- 12.4.5 New Zealand

- 12.4.6 South Korea

- 12.4.7 Rest of Asia Pacific

- 12.5 South America

- 12.5.1 Argentina

- 12.5.2 Brazil

- 12.5.3 Chile

- 12.5.4 Rest of South America

- 12.6 Middle East & Africa

- 12.6.1 Saudi Arabia

- 12.6.2 UAE

- 12.6.3 Qatar

- 12.6.4 South Africa

- 12.6.5 Rest of Middle East & Africa

13 Key Developments

- 13.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 13.2 Acquisitions & Mergers

- 13.3 New Product Launch

- 13.4 Expansions

- 13.5 Other Key Strategies

14 Company Profiling

- 14.1 HCL Technologies

- 14.2 Onward Technologies Ltd.

- 14.3 Tata Technologies Ltd.

- 14.4 Altair Engineering Inc.

- 14.5 Harman International Industries, Inc.

- 14.6 Siemens AG

- 14.7 EPAM Systems

- 14.8 Capgemini

- 14.9 Horiba, Ltd.

- 14.10 Robert Bosch GmbH

- 14.11 Pilot Systems International

- 14.12 Magna International Inc.

- 14.13 Tech Mahindra Limited

- 14.14 Assystem Technologies

- 14.15 L&T Technology

- 14.16 T-NET JAPAN Co., Ltd.

- 14.17 Altran Technologies SA

- 14.18 EDAG Engineering GmbH

- 14.19 Hunter Engineering Company

- 14.20 DesignTech Systems.