|

|

市場調査レポート

商品コード

1324361

タンタル市場の2030年までの予測:製品タイプ、製品形態、製品グレード、用途、エンドユーザー、地域別の世界分析Tantalum Market Forecasts to 2030 - Global Analysis By Product Type, Product Forms, Product Grade, Application, End User and By Geography |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| タンタル市場の2030年までの予測:製品タイプ、製品形態、製品グレード、用途、エンドユーザー、地域別の世界分析 |

|

出版日: 2023年08月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 175+ Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、タンタルの世界市場は2023年に48億2,000万米ドルを占め、予測期間中のCAGRは8.13%で成長し、2030年には83億3,000万米ドルに達すると予測されています。

タンタルは高い融点と強い耐食性を持つ遷移金属です。光沢のある青灰色をした化学元素で、見つけるのが非常に難しいです。硬岩鉱山がタンタルの一次情報であるが、職人鉱山、錫スラグ、タンタライト、コロンビン、コルトンのような鉱物にも含まれています。タンタルは化学的に不安定なためプラチナの代替品として使用され、実験機器、電子機器、医療機器、超合金の製造など幅広い用途があります。

インド・ブランド・エクイティ財団によると、2025年までにエレクトロニクス消費は、2020年度の330億米ドルから4,000億米ドルに増加します。

電子産業からの高い需要

航空宇宙産業や航空産業、電子機器やガジェットの生産におけるタンタルの高い需要が、タンタル市場を牽引しています。最も広く使用されているタンタルの形状はワイヤーと粉末です。その得意分野のひとつがコンデンサーの生産です。炭化タンタルは切削工具の製造に使用され、酸化タンタルはカメラレンズやX線装置の製造に使用されます。これらの要素も同様に市場拡大の原因となっています。

価格変動と需給の混乱

リチウム、モリブデン、インジウム、ニオブはすべてタンタルの成分であるため、価格変動が市場の拡大を妨げる可能性があります。タンタル業界の価格変動と市場の乱高下は、サプライチェーンの回復力と安定性に問題があることを示しています。このように、タンタル市場は、価格変動や需給不均衡といった市場の成長を妨げる要因の結果、多くの困難に直面しています。

ハイエンド技術の革新と採用

ここ数十年、世界中の産業界でハイエンド技術、自動化、コンピューターによるデータ記録・収集・検査、その他の高度な技術が開発・採用され、産業部門における電子機器の需要が増加しています。世界のサービス部門の成長は、LTE/4Gネットワークやモノのインターネット(IoT)サービスの展開など、技術主導の変革によって加速しています。このため、ノートパソコン、パソコン、エアコンなどの電子機器や電化製品の需要が増加しています。今後数年間は、エレクトロニクス産業の成長により、タンタルの需要が高まる可能性が高いです。

限られた供給量

タンタルは比較的珍しい金属であり、ルワンダやコンゴ民主共和国(DRC)を含む数カ国だけが重要な埋蔵量を有しています。タンタルは、用途によってはニオブやセラミックスなどの他の材料で代替できるため、需要と価格が低下する可能性があります。さらに、これらの地域での政情不安や紛争の結果、供給の変動が世界のタンタル市場に影響を及ぼしています。こうした変動は市場の妨げになる可能性があります。

COVID-19の影響:

生産量の制限、サプライチェーンの寸断、物流の課題、需要の減少により、COVID-19の流行はタンタル市場に大きな影響を与えました。しかし、需要が旺盛で、航空宇宙、電気・電子などの重要な分野での用途が盛んであることから、タンタル市場は予測期間中に急速に拡大すると予想されます。

予測期間中、電気・電子分野が最大になる見込み

高電力抵抗器やコンデンサーの生産におけるタンタルの需要が大きいため、予測期間中、電気・電子分野が最大の市場シェアを占めると予想されます。コンデンサにタンタルを使用することで、コンデンサは軽量化・小型化されます。このため、パソコン、携帯電話、車載用電子機器の製造において、コンデンサのニーズが高まっています。その結果、電気・電子産業が拡大し、市場を牽引しています。

予測期間中、CAGRが最も高くなると予想されるコンデンサ分野

最終用途産業からの需要増加により、コンデンサ分野は予測期間中に急拡大すると予想されます。電解コンデンサを作るためには、コンデンサが使用されます。医療、航空宇宙、再生可能エネルギー分野は、これらの電解コンデンサを頻繁に使用するほんの一例です。さらに、単位面積当たりの静電容量がコンデンサの中で最も高いタンタルコンデンサは、小型電気機器に頻繁に使用されています。

最もシェアが高い地域:

予測期間中、アジア太平洋地域が最大の市場シェアを占めると予想されます。同市場は主に、電子機器、航空宇宙、医療機器などのエンドユーザー産業からの需要増加によって推進されています。アジア太平洋地域で最大のタンタル消費国は中国です。今後数年間は、アジア太平洋の急成長と相まって、国産タンタルコンデンサが市場シェアを拡大し続けると予想されます。

CAGRが最も高い地域:

予測期間中、北米は市場ベンダーに多くの拡大機会を提供すると予想されます。この地域のバイオ燃料市場の成長は、コンデンサ需要を押し上げているスマートフォン利用の増加から大きな影響を受けると思われます。この地域の主なタンタル市場は米国とカナダです。さらに、予測期間中、北米地域における採掘事業の増加が市場の堅調な拡大を支えることが予想されます。

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下のいずれかの無料カスタマイズオプションをご提供いたします:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査ソース

- 仮定

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 製品分析

- 用途分析

- エンドユーザー分析

- 新型コロナウイルス感染症(COVID-19)の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界のタンタル市場:製品タイプ別

- タンタル酸リチウム

- 炭化タンタル

- 酸化タンタル

- その他の製品タイプ

第6章 世界のタンタル市場:形態別

- 合金

- 炭化物

- 金属

- 粉末

- その他の形態

第7章 世界のタンタル市場:グレード別

- 医療グレードのタンタル

- 商用グレードのタンタル

第8章 世界のタンタル市場:用途別

- キャパシタ

- 化学処理装置

- エンジンタービンブレード

- 医療機器

- 半導体

- その他の用途

第9章 世界のタンタル市場:エンドユーザー別

- 航空宇宙

- ミサイル部品

- 超音速航空機

- 宇宙船

- 電気・電子

- 携帯電話

- コンピュータ

- カメラレンズ

- 医療とヘルスケア

- 化学および医薬品

- その他のエンドユーザー

第10章 世界のタンタル市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第11章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第12章 会社概要

- Admat Inc.

- Advanced Materials Inc.

- AMG Advanced Metallurgical Group NV

- Cabot Corp.

- China Minmetals Corporation

- CNMC Ningxia Orient Group Co. Ltd

- Ethiopia Mineral Development Share Company

- Fogang Jiata Metals Co. Ltd

- Global Advanced Metals Pty Ltd

- H.C. Starck GmbH

- High-Performance Alloys, Inc.

- Jiangxi Tungsten Industry Group Co. Ltd

- Mokawa Inc.

- Ningxia Orient Tantalum Industry Co. Ltd

- Talison Minerals Pvt. Ltd.

- Taniobis GmbH

- Tantec GmbH

- The USA Titanium Industry Inc.

- Ultra metal minor Limited

List of Tables

- Table 1 Global Tantalum Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Tantalum Market Outlook, By Product Type (2021-2030) ($MN)

- Table 3 Global Tantalum Market Outlook, By Lithium Tantalite (2021-2030) ($MN)

- Table 4 Global Tantalum Market Outlook, By Tantalum Carbide (2021-2030) ($MN)

- Table 5 Global Tantalum Market Outlook, By Tantalum Oxide (2021-2030) ($MN)

- Table 6 Global Tantalum Market Outlook, By Other Product Types (2021-2030) ($MN)

- Table 7 Global Tantalum Market Outlook, By Form (2021-2030) ($MN)

- Table 8 Global Tantalum Market Outlook, By Alloys (2021-2030) ($MN)

- Table 9 Global Tantalum Market Outlook, By Carbide (2021-2030) ($MN)

- Table 10 Global Tantalum Market Outlook, By Metal (2021-2030) ($MN)

- Table 11 Global Tantalum Market Outlook, By Powder (2021-2030) ($MN)

- Table 12 Global Tantalum Market Outlook, By Other Forms (2021-2030) ($MN)

- Table 13 Global Tantalum Market Outlook, By Grade (2021-2030) ($MN)

- Table 14 Global Tantalum Market Outlook, By Medical Grade Tantalum (2021-2030) ($MN)

- Table 15 Global Tantalum Market Outlook, By Commercial Grade Tantalum (2021-2030) ($MN)

- Table 16 Global Tantalum Market Outlook, By Application (2021-2030) ($MN)

- Table 17 Global Tantalum Market Outlook, By Capacitors (2021-2030) ($MN)

- Table 18 Global Tantalum Market Outlook, By Chemical Processing Equipment (2021-2030) ($MN)

- Table 19 Global Tantalum Market Outlook, By Engine Turbine Blades (2021-2030) ($MN)

- Table 20 Global Tantalum Market Outlook, By Medical Equipment (2021-2030) ($MN)

- Table 21 Global Tantalum Market Outlook, By Semiconductors (2021-2030) ($MN)

- Table 22 Global Tantalum Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 23 Global Tantalum Market Outlook, By End User (2021-2030) ($MN)

- Table 24 Global Tantalum Market Outlook, By Aerospace (2021-2030) ($MN)

- Table 25 Global Tantalum Market Outlook, By Missile Parts (2021-2030) ($MN)

- Table 26 Global Tantalum Market Outlook, By Supersonic Aircrafts (2021-2030) ($MN)

- Table 27 Global Tantalum Market Outlook, By Space Vehicles (2021-2030) ($MN)

- Table 28 Global Tantalum Market Outlook, By Electrical & Electronics (2021-2030) ($MN)

- Table 29 Global Tantalum Market Outlook, By Mobile Phones (2021-2030) ($MN)

- Table 30 Global Tantalum Market Outlook, By Computers (2021-2030) ($MN)

- Table 31 Global Tantalum Market Outlook, By Camera Lenses (2021-2030) ($MN)

- Table 32 Global Tantalum Market Outlook, By Medical & Healthcare (2021-2030) ($MN)

- Table 33 Global Tantalum Market Outlook, By Chemical & Pharmaceuticals (2021-2030) ($MN)

- Table 34 Global Tantalum Market Outlook, By Other End Users (2021-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Tantalum Market is accounted for $4.82 billion in 2023 and is expected to reach $8.33 billion by 2030 growing at a CAGR of 8.13% during the forecast period. Tantalum is a transition metal that has a high melting point and strong corrosion resistance. It is a chemical element that is lustrous and blue-grey in colour and extremely hard to find. Hard rock mines are the primary source of tantalum, but it is also present in artisanal mines, tin slag, and minerals like tantalite, columbine, and colton. Tantalum is used as a substitute for platinum due to its chemical immobility and has a wide range of uses in laboratory equipment, electronic devices, medical equipment, the production of superalloys, etc.

According to the India Brand Equity Foundation, By 2025, Electronics consumption will increase to US$400 billion by 2025, up from US$33 billion in FY20.

Market Dynamics:

Driver:

High demand from electronics industry

The high demand for tantalum in the aerospace and aviation industries, as well as in the production of electronic devices and gadgets, is what drives the tantalum market. The most widely used forms of tantalum are wire and powder. One of their areas of expertise is the production of capacitors. Tantalum carbide is used to make cutting tools, whereas tantalum oxide is used to make camera lenses and X-ray equipment. These elements are equally responsible for the market's expansion.

Restraint:

Price volatility and disruption in supply demand

As lithium, molybdenum, indium, and niobium are all components of tantalum, price fluctuations may hinder the market's expansion. The tantalum industry's price swings and market turbulence indicate issues with the supply chain's resiliency and stability. The tantalum market thus faces a number of difficulties as a result of factors like price volatility and a demand-supply imbalance, which hinder market growth.

Opportunity:

Innovation and adoption of high-end technologies

In the last few decades, there has been an increase in demand for electronic devices in the industrial sector due to the development and adoption of high-end technologies, automation, computerised data recording, collection, and inspection practises, and other such advanced techniques in industries around the world. Global service sector growth is being accelerated by technology-driven transformation, including the deployment of LTE/4G networks and Internet of Things (IoT) services. This has increased demand for electronic devices and appliances, including laptops, computers, air conditioners, and other items. In the upcoming years, the demand for tantalum is likely to rise due to the growth of the electronics industry.

Threat:

Limited supply

Tantalum is a relatively uncommon metal, and only a few nations, including Rwanda and the Democratic Republic of the Congo (DRC), have significant reserves. Tantalum can be replaced with other materials, such as niobium or ceramics, in some applications, which can lower demand and prices. Additionally, supply fluctuations have had an impact on the global tantalum market as a result of political unrest and conflict in these areas. Such fluctuations may hinder the market.

COVID-19 Impact:

Due to limited production, a broken supply chain, logistical challenges, and a decline in demand, the COVID-19 pandemic had a significant impact on the tantalum market. However, with strong demand and flourishing applications in important sectors like aerospace, electrical and electronics, and others, it is anticipated that the tantalum market will expand quickly over the course of the forecast period.

The electrical & electronics segment is expected to be the largest during the forecast period

Due to the significant demand for tantalum in the production of high-power resistors and capacitors, the Electrical & Electronics segment is anticipated to hold the largest market share during the forecast period. Tantalum in capacitors makes them lighter and smaller. Because of this, there is an increasing need for capacitors in the production of personal computers, mobile phones, and automotive electronics. As a result, the electrical and electronics industry is expanding and driving the market.

The capacitors segment is expected to have the highest CAGR during the forecast period

Due to rising demand from end-use industries, the capacitors segment is anticipated to expand quickly during the forecast period. In order to make electrolytic capacitors, capacitors are used. The medical, aerospace, and renewable energy sectors are just a few that frequently use these electrolytic capacitors. Additionally, tantalum capacitors, which have the highest capacitance per unit space of any capacitor, are frequently used in compact electrical apparatus.

Region with largest share:

During the forecast period, Asia-Pacific is expected to hold the largest market share. The market is primarily being propelled by the rise in demand from end-user industries such as electronics, aerospace, and medical equipment. The largest tantalum consumer in the Asia-Pacific region is China. In the upcoming years, it is anticipated that domestic tantalum capacitors will continue to gain market share, combined with Asia-Pacific's rapid growth.

Region with highest CAGR:

During the projection timeframe, North America is anticipated to offer market vendors a number of expansion opportunities. The growth of the biofuels market in this region will be greatly impacted by the increase in smartphone use that is driving up capacitor demand. The region's main tantalum markets are in the US and Canada. Furthermore, over the course of the forecast period, it is expected that the growing number of mining operations in the North American region will support the market's robust expansion.

Key players in the market:

Some of the key players profiled in the Tantalum Market include: Admat Inc., Advanced Materials Inc., AMG Advanced Metallurgical Group NV, Cabot Corp., China Minmetals Corporation,CNMC Ningxia Orient Group Co. Ltd, Ethiopia Mineral Development Share Company, Fogang Jiata Metals Co. Ltd, Global Advanced Metals Pty Ltd, H.C. Starck GmbH, High-Performance Alloys, Inc., Jiangxi Tungsten Industry Group Co. Ltd, Mokawa Inc., Ningxia Orient Tantalum Industry Co. Ltd, Talison Minerals Pvt. Ltd., Taniobis GmbH, Tantec GmbH, The USA Titanium Industry Inc. and Ultra metal minor Limited.

Key Developments:

In April 2023, Cabot Corporation announced that it has acquired the Chiba solar farm from Shoko Co., Ltd. The solar farm adjoins Cabot's carbon black manufacturing facility in Chiba, Japan and will enable Cabot to export solar power as renewable energy to the electrical grid in the region. The Chiba solar farm generates up to 3,500 megawatt-hours (MWh) per year of electricity, which is equivalent to powering over 700 homes in Japan annually. The acquisition supports the company's sustainability strategy as the solar farm is an investment in renewable energy.

In April 2023, As part of the HVBatCycle (high voltage battery recycling) project, TANIOBIS has put the lithium-ion battery (LIB) recycling facility into operation. The project's objective was to develop sustainable, energy-efficient processes throughout the HV battery value chain, ultimately creating a closed battery materials loop. This has now been achieved.

In June 2022, H.C. Starck Tungsten Powders, a subsidiary of the Masan High-Tech Materials Group, and the Center for Solar Energy and Hydrogen Research Baden-Wurttemberg (ZSW) are jointly investigating the use of tungsten-based cathode coatings in lithium-ion batteries. After various tungsten precursors were first systematically examined for their suitability, the first coating tests have now started. This will be followed by electrochemical investigations.

Product Types Covered:

- Lithium Tantalite

- Tantalum Carbide

- Tantalum Oxide

- Other Product Types

Forms Covered:

- Alloys

- Carbide

- Metal

- Powder

- Other Forms

Grades Covered:

- Medical Grade Tantalum

- Commercial Grade Tantalum

Applications Covered:

- Capacitors

- Chemical Processing Equipment

- Engine Turbine Blades

- Medical Equipment

- Semiconductors

- Other Applications

End Users Covered:

- Aerospace

- Electrical & Electronics

- Medical & Healthcare

- Chemical & Pharmaceuticals

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026 and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Product Analysis

- 3.7 Application Analysis

- 3.8 End User Analysis

- 3.9 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Tantalum Market, By Product Type

- 5.1 Introduction

- 5.2 Lithium Tantalite

- 5.3 Tantalum Carbide

- 5.4 Tantalum Oxide

- 5.5 Other Product Types

6 Global Tantalum Market, By Form

- 6.1 Introduction

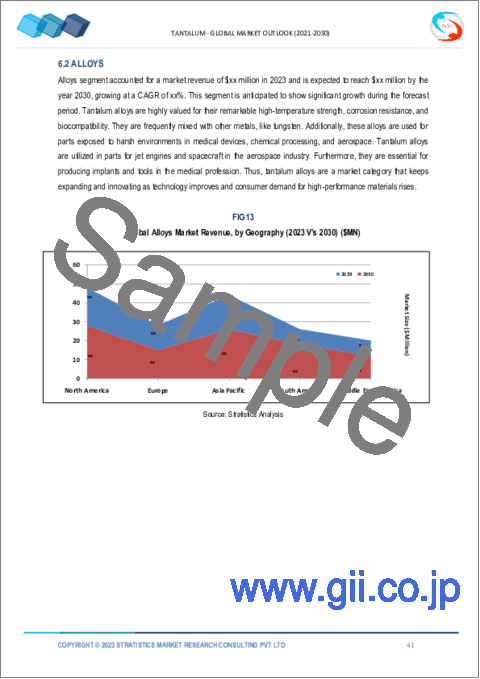

- 6.2 Alloys

- 6.3 Carbide

- 6.4 Metal

- 6.5 Powder

- 6.6 Other Forms

7 Global Tantalum Market, By Grade

- 7.1 Introduction

- 7.2 Medical Grade Tantalum

- 7.3 Commercial Grade Tantalum

8 Global Tantalum Market, By Application

- 8.1 Introduction

- 8.2 Capacitors

- 8.3 Chemical Processing Equipment

- 8.4 Engine Turbine Blades

- 8.5 Medical Equipment

- 8.6 Semiconductors

- 8.7 Other Applications

9 Global Tantalum Market, By End User

- 9.1 Introduction

- 9.2 Aerospace

- 9.2.1 Missile Parts

- 9.2.2 Supersonic Aircrafts

- 9.2.3 Space Vehicles

- 9.3 Electrical & Electronics

- 9.3.1 Mobile Phones

- 9.3.2 Computers

- 9.3.3 Camera Lenses

- 9.4 Medical & Healthcare

- 9.5 Chemical & Pharmaceuticals

- 9.6 Other End Users

10 Global Tantalum Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.5 South America

- 10.5.1 Argentina

- 10.5.2 Brazil

- 10.5.3 Chile

- 10.5.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 Admat Inc.

- 12.2 Advanced Materials Inc.

- 12.3 AMG Advanced Metallurgical Group NV

- 12.4 Cabot Corp.

- 12.5 China Minmetals Corporation

- 12.6 CNMC Ningxia Orient Group Co. Ltd

- 12.7 Ethiopia Mineral Development Share Company

- 12.8 Fogang Jiata Metals Co. Ltd

- 12.9 Global Advanced Metals Pty Ltd

- 12.10 H.C. Starck GmbH

- 12.11 High-Performance Alloys, Inc.

- 12.12 Jiangxi Tungsten Industry Group Co. Ltd

- 12.13 Mokawa Inc.

- 12.14 Ningxia Orient Tantalum Industry Co. Ltd

- 12.15 Talison Minerals Pvt. Ltd.

- 12.16 Taniobis GmbH

- 12.17 Tantec GmbH

- 12.18 The USA Titanium Industry Inc.

- 12.19 Ultra metal minor Limited