|

|

市場調査レポート

商品コード

1324303

小型電気自動車(LEV)市場の2030年までの予測:車両タイプ別、車両カテゴリー別、出力別、コンポーネント別、用途別、地域別の世界分析Light Electric Vehicles Market Forecasts to 2030 - Global Analysis By Vehicle Type, Vehicle Category, Power Output, Component, Application and By Geography |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 小型電気自動車(LEV)市場の2030年までの予測:車両タイプ別、車両カテゴリー別、出力別、コンポーネント別、用途別、地域別の世界分析 |

|

出版日: 2023年08月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 175+ Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の小型電気自動車(LEV)市場は2023年に877億米ドルを占め、予測期間中にCAGR 11.74%で成長し、2030年には1,907億米ドルに達すると予測されています。

電動オートバイ、電動スクーター、電動自転車、その他類似の移動手段は、「小型電気自動車(LEV)」と呼ばれます。通常、従来の自動車よりも小型・軽量で、電気モーターと充電式バッテリーで駆動します。EVの例としては、水上・水中航行、道路・鉄道用自動車、電気航空機、電気宇宙船などがあります。中国やインドをはじめとするアジア諸国では、ラストワンマイル(最後の1キロメートル)接続のために従来型のEVが好まれ、EVが手ごろな価格の個人輸送手段として認識されているため、軽電気自動車が電化プロジェクトの中核を担うことになると思われます。

オーストラリア政府の独立法定機関であるオーストラリア統計局によると、オーストラリアでは電動バイクの登録台数が2020年の1,308台から2021年には2,706台に増加します。

電気自動車のバッテリー交換

LEVユーザーの時間を節約する新しい習慣として、LEV充電ステーションでのバッテリー交換があります。レベル3のEV充電と超急速充電は、それぞれ15分から30分で電気自動車をフル充電できるが、LEVでは一貫性がないです。つまり、バッテリー交換はLEVの代替手段として非常に有効なのです。NIOのような事業者は、2021年7月までに300カ所以上のバッテリー交換ステーションを設置し、2025年までにさらに約4,000カ所を設置したいとしています。中国国外で開発されたバッテリー交換ステーションは1,000カ所を超え、そのステーションは世界中で290万回近く利用されています。

互換性、互換性、標準化の欠如

軽電気自動車市場はまだ黎明期であるため、OEMは、モーター、バッテリー、エコシステム、その他の部品に関連する、より速く、より優れた技術に関する激しい競争と多数の特許のために、標準化され、互換性があり、普遍的な互換性のあるシステムと車両を開発することが困難であると感じています。インド政府の研究・諮問機関であるインド変革国家機構(NITI)アヨグは、この問題に対処するため、2022年8月にバッテリースワップ政策を起草しました。この政策は、バッテリー交換エコシステム全体の相互運用性を促進する標準化の技術的側面に言及しており、これが市場成長の妨げとなっています。

政府のインセンティブと補助金

従来の自動車に対する環境問題が高まり続けているため、世界中の政府が代替燃料で走る自動車の使用を推進しています。LEVは、インドや中国のような発展途上国において、地理的境界を利用した旅客輸送、ラストマイルデリバリー、その他の商業目的などの用途のために、運行車両の必須構成要素となっています。オランダのような先進国は、2025年末までに、すべての商用および政府用途でゼロエミッションの電気自動車を全面的に採用したいと考えています。また、メキシコなどの政府は、車両購入、充電、インフラ建設など、EV導入のいくつかの段階で税制優遇措置を講じています。

航続距離の制限とICE車より高い初期保有コスト

航続距離の制限により、小型電気自動車(LEV)の市場は拡大できていないです。LEVには、ICE車とは対照的に、燃料補給とエネルギー貯蔵を容易にするガソリンタンクがないです。ICE車と比較すると、フル充電されたバッテリーの航続距離は一般的に短いです。eスクーター、eモーターサイクル、eバイクなど、大半の電動二輪車の航続距離は最大100~120マイルであるため、1日に100マイル以上走る必要がある消費者はLEVの購入をためらっています。また、産業用車両はバッテリーの寿命が短く、充電時間が長いため、日常的な利用率が低下します。

COVID-19の影響:

COVID-19の流行は、デジタルトランスフォーメーションのためのテクノロジー利用を加速させています。環境にやさしく安全な輸送手段を求める顧客の需要により、LEVの需要も急増しました。この流行は世界のサプライチェーンにも支障をきたし、部品の不足を招き、LEVの製造と納入が遅れています。その結果、モデルによっては価格が高くなり、出荷が遅れています。さらに、パンデミックの経済への影響により、一部の消費者は購入を先延ばしにせざるを得ず、市場の拡大を妨げています。

予測期間中は2輪車セグメントが最大になる見込み

2輪車は3輪車よりも機敏で操縦性に優れているため、混雑した大都市圏の対応に適しており、予測期間を通じて最大の市場シェアを占めました。また、従来の自動車よりも手頃な価格で環境に優しいため、コスト意識の高い消費者にアピールしています。さらに、大きな成長見通しを後押ししている主な理由は、環境問題に対する消費者の意識の高まりと燃料価格の上昇に伴い、環境に優しい輸送ソリューションに対する消費者の需要が高まっていることです。

予測期間中にCAGRが最も高くなると予想されるのは商業セグメント

商業セグメントは予測期間を通じて有利な成長が見込まれます。バンやトラックのような従来の配送車が交通渋滞や駐車規制のために利用できない都市部は、商用小型電気自動車(LEV)に適しています。電気自動車は、従来の配達用車両をより効果的かつ手頃な価格で代替できます。さらに、環境に優しく、二酸化炭素排出量を削減しようとする産業にとってますます重要になってきています。

最大のシェアを占める地域

対象期間中、北米が市場で最大のシェアを占めましたが、これは主に環境に優しい輸送手段に対する需要の高まりによるものです。この地域における市場拡大の主な貢献者は米国とカナダです。また、補助金や税制優遇措置といった形で電気自動車に対する政府の支援が高まっていることも、市場拡大を後押しすると予想されます。この地域では、交通渋滞が大きな問題となっている都市部を中心に、電動自転車や電動スクーターのニーズも高まっています。フォード、ゼネラル・モーターズ、その他の大手企業がこの地域での市場拡大を推進すると予想されます。

CAGRが最も高い地域:

安価で持続可能な交通手段への需要が高まっている結果、アジア太平洋地域は予測期間中に収益性の高い成長を遂げると予想されます。大きな市場シェアを持つ中国は、この地域で軽電気自動車市場が最も大きい国です。この地域での市場拡大は、補助金や税制上の優遇措置という形で電気自動車に対する政府の支援額が増加していることに後押しされています。また、消費者の可処分所得の増加と都市化が市場拡大に拍車をかけると予想されます。この地域では、特に駐車場の限られた混雑した都市部において、電動スクーターや電動自転車の需要が非常に高いです。

無料のカスタマイズサービス:

本レポートをご購読のお客様には、以下のいずれかの無料カスタマイズオプションをご提供いたします:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査ソース

- 仮定

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 用途分析

- 新興市場

- 新型コロナウイルス感染症(COVID-19)の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の小型電気自動車(LEV)市場:車両タイプ別

- Eバイク

- 電動ATV/UTV

- Eオートバイ

- Eスクーター

- E芝刈り機

- 手動

- ロボット

- 近所の電気自動車

- 産業用電気自動車

- 配送ロボット

- 無人フォークリフト

- 無人搬送車(AGV)

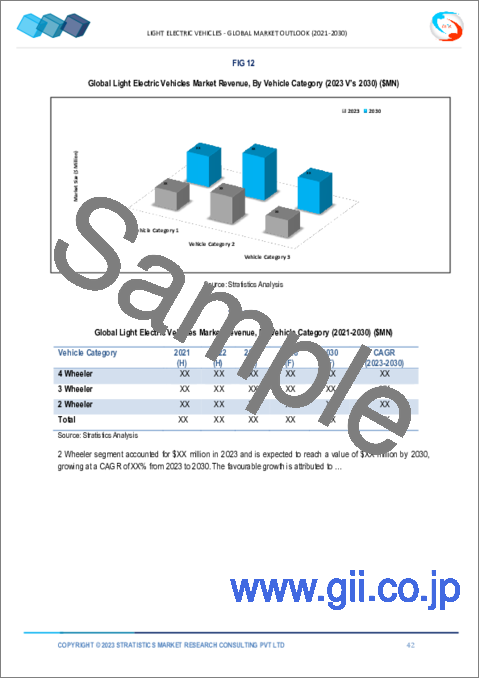

第6章 世界の小型電気自動車(LEV)市場:車両カテゴリー別

- 4輪車

- 3輪車

- 2輪車

第7章 世界の小型電気自動車(LEV)市場:出力別

- 9~15KW

- 6~9KW

- 6KW未満

第8章 世界の小型電気自動車(LEV)市場:コンポーネント別

- パワーエレクトロニクス

- Eブレーキブースター

- パワーコントローラー

- インバーター

- モーターコントローラー

- 電気モーター

- バッテリーパック

第9章 世界の小型電気自動車(LEV)市場:用途別

- 商業

- レクリエーション・スポーツ

- シェアードモビリティ

- パーソナルモビリティ

第10章 世界の小型電気自動車(LEV)市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第11章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第12章 会社概要

- Borgwarner Inc.

- BMW AG

- Balkancar Record

- Auto Rennen India

- Auro Robotics

- Ari Motors

- Alke, American Landmaster

- Addax Motors

- Aisin Corporation

- Accelerated Systems Inc.

List of Tables

- Table 1 Global Light Electric Vehicles Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Light Electric Vehicles Market Outlook, By Vehicle Type (2021-2030) ($MN)

- Table 3 Global Light Electric Vehicles Market Outlook, By E Bike (2021-2030) ($MN)

- Table 4 Global Light Electric Vehicles Market Outlook, By Electric ATV/UTV (2021-2030) ($MN)

- Table 5 Global Light Electric Vehicles Market Outlook, By E Motorcycle (2021-2030) ($MN)

- Table 6 Global Light Electric Vehicles Market Outlook, By E Scooter (2021-2030) ($MN)

- Table 7 Global Light Electric Vehicles Market Outlook, By E Lawn Mower (2021-2030) ($MN)

- Table 8 Global Light Electric Vehicles Market Outlook, By Manual (2021-2030) ($MN)

- Table 9 Global Light Electric Vehicles Market Outlook, By Robotic (2021-2030) ($MN)

- Table 10 Global Light Electric Vehicles Market Outlook, By Neighborhood Electric Vehicle (2021-2030) ($MN)

- Table 11 Global Light Electric Vehicles Market Outlook, By Electric Industrial Vehicle (2021-2030) ($MN)

- Table 12 Global Light Electric Vehicles Market Outlook, By Delivery Robot (2021-2030) ($MN)

- Table 13 Global Light Electric Vehicles Market Outlook, By Autonomous Forklift (2021-2030) ($MN)

- Table 14 Global Light Electric Vehicles Market Outlook, By Automated Guided Vehicle (2021-2030) ($MN)

- Table 15 Global Light Electric Vehicles Market Outlook, By Vehicle Category (2021-2030) ($MN)

- Table 16 Global Light Electric Vehicles Market Outlook, By 4 Wheeler (2021-2030) ($MN)

- Table 17 Global Light Electric Vehicles Market Outlook, By 3 Wheeler (2021-2030) ($MN)

- Table 18 Global Light Electric Vehicles Market Outlook, By 2 Wheeler (2021-2030) ($MN)

- Table 19 Global Light Electric Vehicles Market Outlook, By Power Output (2021-2030) ($MN)

- Table 20 Global Light Electric Vehicles Market Outlook, By 9-15 KW (2021-2030) ($MN)

- Table 21 Global Light Electric Vehicles Market Outlook, By 6-9 KW (2021-2030) ($MN)

- Table 22 Global Light Electric Vehicles Market Outlook, By Less Than 6 KW (2021-2030) ($MN)

- Table 23 Global Light Electric Vehicles Market Outlook, By Component (2021-2030) ($MN)

- Table 24 Global Light Electric Vehicles Market Outlook, By Power Electronics (2021-2030) ($MN)

- Table 25 Global Light Electric Vehicles Market Outlook, By E Brake Booster (2021-2030) ($MN)

- Table 26 Global Light Electric Vehicles Market Outlook, By Power Controller (2021-2030) ($MN)

- Table 27 Global Light Electric Vehicles Market Outlook, By Inverter (2021-2030) ($MN)

- Table 28 Global Light Electric Vehicles Market Outlook, By Motor Controller (2021-2030) ($MN)

- Table 29 Global Light Electric Vehicles Market Outlook, By Electric Motor (2021-2030) ($MN)

- Table 30 Global Light Electric Vehicles Market Outlook, By Battery Pack (2021-2030) ($MN)

- Table 31 Global Light Electric Vehicles Market Outlook, By Application (2021-2030) ($MN)

- Table 32 Global Light Electric Vehicles Market Outlook, By Commercial (2021-2030) ($MN)

- Table 33 Global Light Electric Vehicles Market Outlook, By Recreation & Sports (2021-2030) ($MN)

- Table 34 Global Light Electric Vehicles Market Outlook, By Shared Mobility (2021-2030) ($MN)

- Table 35 Global Light Electric Vehicles Market Outlook, By Personal Mobility (2021-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Light Electric Vehicles Market is accounted for $87.7 billion in 2023 and is expected to reach $190.7 billion by 2030 growing at a CAGR of 11.74% during the forecast period. The electric motorcycles, electric scooters, electric bicycles, and other similar modes of mobility is referred to as the "light electric vehicles" (LEVs). Typically, smaller and lighter than conventional cars, these vehicles are propelled by electric motors and rechargeable batteries. Some instances of EVs include surface and underwater watercraft, cars for the road and rail, electric aircraft, and electric spacecraft. In China, India, and other Asian countries that favor their conventional counterparts for last-mile connectivity and perceive them as an affordable mode of personal transportation, light electric vehicles will be at the core of electrification projects.

According to the Australian Bureau of Statistics, an independent statutory agency of the Australian Government, in Australia, registrations for electric motorcycles increased from 1,308 in 2020 to 2,706 in 2021.

Market Dynamics:

Driver:

Use of battery swapping for electric utility vehicles

A new practice that saves LEV users time involves switching out batteries at the LEV charging stations. Although level 3 EV charging and ultra-fast charging can fully charge an electric vehicle in 15 to 30 minutes, respectively, they are inconsistent with LEVs. So, battery changing is a terrific LEV alternative. By July 2021, businesses like NIO had set up over 300 battery switching stations, and by 2025, they want to have built about 4,000 more. With over 1,000 battery-swapping stations developed outside of China, its stations have been utilized nearly 2.9 million times worldwide.

Restraint:

Lack of compatibility, interchangeability and standardization

Since the market for light electric vehicles is still in its infancy, OEMs find it challenging to develop standardized, interchangeable, and universally compatible systems and vehicles due to the intense competition and numerous patents for faster and better technologies related to motors, batteries, ecosystems, and other components. The National Institution for Transforming India (NITI) Ayog, a research and advisory body for the Indian government, drafted the Battery Swapping Policy in August 2022 to address this problem. This policy mentions the technical aspects of standardization that would promote interoperability throughout the battery swapping ecosystem, which leads to the hampering of the market growth.

Opportunity:

Government incentives and subsidies

Governments all across the world are promoting the use of vehicles that run on alternative fuels as environmental worries about conventional automobiles continue to rise. LEVs are being made a required component of operational fleets in developing nations like India and China for uses including geofenced passenger carrying, last-mile delivery, and other commercial objectives. By the end of 2025, developed nations like the Netherlands want to entirely employ electric vehicles with zero emissions for all commercial and governmental uses. Tax incentives are also offered by governments, such as Mexico's, at several EV deployment stages, including vehicle purchase, charging, and infrastructure construction.

Threat:

Limited range and high initial ownership cost of LEVs than ICE Counterparts

Due to range restrictions, the market for light electric vehicles hasn't been able to expand. LEVs lack gasoline tanks for easy refueling and energy storage, in contrast to ICE vehicles. Compared to its ICE counterpart, a fully charged battery has a generally lower range. Consumers who need to go more than 100 miles per day are hesitant to buy LEVs because the majority of electric two-wheelers, such as e-scooters, e-motorcycles, and e-bikes, have a range of up to 100-120 miles. Industrial vehicles also experience short battery life and lengthy recharge times, which reduce their daily utilization.

COVID-19 Impact:

The COVID-19 epidemic has accelerated the use of technology for digital transformation. Due to customer demand for environmentally friendly and secure modes of transportation, LEV demand has also surged. The epidemic has also hampered the worldwide supply chain, which has led to a scarcity of parts and slowed down the creation and delivery of LEVs. As a result, some models cost more, and shipments are now delayed. Additionally, the pandemic's impact on the economy has forced some consumers to put off buying decisions, which has hampered the market's expansion.

The 2-wheelers segment is expected to be the largest during the forecast period

The 2-wheelers held the largest market share throughout the projection period, as they are more agile and maneuverable than three-wheelers and are therefore better suited for handling congested metropolitan areas. They appeal to consumers who are cost-conscious because they are also more affordable and environmentally friendly than conventional vehicles. Additionally, the key reason driving significant growth prospects is the rise in consumer demand for environmentally friendly transportation solutions, as their awareness of environmental issues grows and fuel prices rise.

The commercial segment is expected to have the highest CAGR during the forecast period

Commercial segment is expected to have lucrative growth throughout the projection period. Urban regions where traditional delivery vehicles like vans and trucks are unfeasible owing to traffic congestion and parking restrictions are suited for commercial light electric vehicles. They provide a more effective and affordable substitute for conventional delivery vehicles. Moreover, they are also environmentally friendly, which is becoming more and more crucial for industries trying to reduce their carbon footprint.

Region with largest share:

During the extended period, North America held the largest share of the market, primarily due to the rising demand for environmentally friendly transportation options. The main contributors to market expansion in this region are the United States and Canada. It is also anticipated that rising government support for electric vehicles in the form of subsidies and tax incentives will propel market expansion. In this region, there is a growing need for electric bicycles and scooters as well, particularly in urban areas where traffic congestion is a major problem. Ford, General Motors, and other significant companies are anticipated to propel market expansion in this area.

Region with highest CAGR:

As a result of the rising demand for inexpensive, sustainable modes of transport, Asia-Pacific is expected to have profitable growth during the forecast period. With a sizeable market share, China is the country in this region with the largest market for light electric vehicles. Market expansion in this area is being fueled by the growing amount of government support for electric vehicles in the form of subsidies and tax benefits. It is also anticipated that increased consumer disposable income and urbanization will fuel market expansion. This region has a very strong demand for electric scooters and bicycles, especially in congested urban areas with limited parking.

Key players in the market:

Some of the key players in Light Electric Vehicles market include: Borgwarner Inc., BMW AG, Balkancar Record, Auto Rennen India, Auro Robotics, Ari Motors, Alke, American Landmaster, Addax Motors, Aisin Corporation and Accelerated Systems Inc.

Key Developments:

In June 2022, Club Car announced the acquisition of Melex, which Garia bought in 2021 to help it expand its utility business, and Garia A/S, a maker of electric street-legal low-speed cars with a focus on the utility, consumer, and golf industries. Based in Poland, Melex is a producer of light utility vehicles.

In April 2022, Sansera Engineering Limited revealed that it has received orders from BMW Motorrad for two packages of 26 aluminum forged and machined parts totaling about USD 37.5 million over a ten-year period. Sansera has built a cutting-edge facility for aluminum forging and machining, including solution heat treatment and anodizing, at one of its sites in Bengaluru, where these parts will be produced.

In March 2022, A subsidiary of Textron Inc., Textron Ground Support Equipment Inc., has announced that it will work with General Motors (GM) and Powertrain Control Solutions (PCS) to electrify its broad range of products. For Textron GSE products alone, GM and PCS have created an integrated driveline that makes use of GM's lithium-ion battery systems. Textron GSE will be able to benefit from GM's expertise in electric propulsion systems thanks to the driveline.

In February 2022, In the United States and Canada, Wallbox N.V. and Polaris Inc. announced a new collaboration. Polaris will sell the 40 Amp version of Wallbox's best-selling charger, the Pulsar Plus, in order to make it even faster for customers to charge their electric vehicles. This revelation comes in the wake of Polaris' recent unveiling of the 2023 RANGER XP Kinetic. Off-road vehicles are a particular fit for Pulsar Plus 40 Amp because to its NEMA connection, which offers greater versatility for agricultural and rural charging areas.

Vehicle Types Covered:

- E Bike

- Electric ATV/UTV

- E Motorcycle

- E Scooter

- E Lawn Mower

- Neighborhood Electric Vehicle

- Electric Industrial Vehicle

- Delivery Robot

- Autonomous Forklift

- Automated Guided Vehicle

Vehicle Categories Covered:

- 4 Wheeler

- 3 Wheeler

- 2 Wheeler

Power Outputs Covered:

- 9-15 KW

- 6-9 KW

- Less Than 6 KW

Components Covered:

- Power Electronics

- E Brake Booster

- Power Controller

- Inverter

- Motor Controller

- Electric Motor

- Battery Pack

Applications Covered:

- Commercial

- Recreation & Sports

- Shared Mobility

- Personal Mobility

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Light Electric Vehicles Market, By Vehicle Type

- 5.1 Introduction

- 5.2 E Bike

- 5.3 Electric ATV/UTV

- 5.4 E Motorcycle

- 5.5 E Scooter

- 5.6 E Lawn Mower

- 5.6.1 Manual

- 5.6.2 Robotic

- 5.7 Neighborhood Electric Vehicle

- 5.8 Electric Industrial Vehicle

- 5.9 Delivery Robot

- 5.10 Autonomous Forklift

- 5.11 Automated Guided Vehicle

6 Global Light Electric Vehicles Market, By Vehicle Category

- 6.1 Introduction

- 6.2 4 Wheeler

- 6.3 3 Wheeler

- 6.4 2 Wheeler

7 Global Light Electric Vehicles Market, By Power Output

- 7.1 Introduction

- 7.2 9-15 KW

- 7.3 6-9 KW

- 7.4 Less Than 6 KW

8 Global Light Electric Vehicles Market, By Component

- 8.1 Introduction

- 8.2 Power Electronics

- 8.3 E Brake Booster

- 8.4 Power Controller

- 8.5 Inverter

- 8.6 Motor Controller

- 8.7 Electric Motor

- 8.8 Battery Pack

9 Global Light Electric Vehicles Market, By Application

- 9.1 Introduction

- 9.2 Commercial

- 9.3 Recreation & Sports

- 9.4 Shared Mobility

- 9.5 Personal Mobility

10 Global Light Electric Vehicles Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.5 South America

- 10.5.1 Argentina

- 10.5.2 Brazil

- 10.5.3 Chile

- 10.5.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 Borgwarner Inc.

- 12.2 BMW AG

- 12.3 Balkancar Record

- 12.4 Auto Rennen India

- 12.5 Auro Robotics

- 12.6 Ari Motors

- 12.7 Alke, American Landmaster

- 12.8 Addax Motors

- 12.9 Aisin Corporation

- 12.10 Accelerated Systems Inc.