|

|

市場調査レポート

商品コード

1308573

自動車用データ管理材料の2030年までの市場予測-コンポーネント別、データタイプ別、車両タイプ別、展開別、用途別、地域別の世界分析Automotive Data Management Material Market Forecasts to 2030 - Global Analysis By Component, Data Type, Vehicle Type, Deployment, Application and By Geography |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 自動車用データ管理材料の2030年までの市場予測-コンポーネント別、データタイプ別、車両タイプ別、展開別、用途別、地域別の世界分析 |

|

出版日: 2023年07月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 175+ Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の自動車データ管理市場は2023年に22億1,000万米ドルを占め、予測期間中のCAGRは18.3%で成長し、2030年には71億7,000万米ドルに達すると予測されています。

自動車データ管理は、自動車とそのコンポーネントから生成されるデータを収集、保存、処理、分析するプロセスです。この情報には、自動車の操作方法、 促進要因の行動、環境、その他の重要な要素に関する詳細が含まれます。データは、性能の向上、メンテナンスコストの削減、全体的な運転体験の向上を目的として、車両に設置されたさまざまなセンサーやデバイスを使用して収集されます。

statista.comによると、2021年には米国で推定8,400万台のコネクテッド・ビークルが道路を走っているといいます。コネクテッドカーの市場は近年成長を続けており、今後も成長が見込まれます。

市場力学:

促進要因

コネクテッドカーと電気自動車の需要増加

コネクテッドカーに対する需要の高まりは、自動車データ管理の世界市場を牽引する重要な要因の一つです。コネクテッドカーの運転、位置情報、使用によって膨大な量のデータが生成されます。自動車メーカーやその他の利害関係者は、自動車データ管理システムを利用してこのデータを収集、処理、分析することで、 促進要因の安全性と車両性能を向上させることができます。さらに、電動化された自動車が受け入れられつつあることも、世界市場を牽引する要因となっています。電気自動車は、バッテリーの充電レベルやエネルギー使用量など、従来の内燃エンジン車と比較してさまざまなデータを生成します。軽量車両や電動モビリティといった自動車産業の進歩により、市場は前進しています。

抑制要因:

高い導入コストと熟練した専門家の不足

自動車データ管理ソリューションの導入は、特に中小企業にとっては高額になる可能性があり、市場の拡大を制限する可能性があります。さらに、自動車データ管理ソリューションの実装と保守ができる有資格の専門家の不足も、市場開拓を制約する可能性があります。

機会:

クラウドベースのソリューションとデータ分析への需要の高まり

データ分析に対する需要の高まりは、世界の自動車データ管理市場における主要なビジネスチャンスの1つです。自動車データ管理システムを活用することで、自動車メーカーやその他の利害関係者は膨大な量の車両データを分析して動向やパターンを特定し、データ主導の意思決定や車両性能の向上を実現できます。クラウドベースのソリューションは、柔軟性、拡張性、コスト効率が高く、あらゆる規模の企業に好まれています。したがって、自動車データ管理ソリューションは、リアルタイムのデータアクセスと洞察を可能にするクラウドベースのソリューションを提供することで、この傾向から利益を得ることができます。

脅威

サイバーセキュリティ問題の高まり

自動車データ管理市場の成長は、コネクテッドカーや自動運転車に関するサイバーセキュリティ問題の増加によって悪影響を受けると予想されます。他のコネクテッド・デバイスに影響を及ぼす同じサイバーセキュリティ・リスクが、コネクテッド車両にも影響を及ぼします。コネクテッド・ビークルはインターネットを介した広範なデータ伝送を行うため、ハッカーはデータへのアクセスや自動車のシステム乗っ取りを目的としてコネクテッド・ビークルを標的にする可能性があります。その結果、車両の物理的完全性と乗員の安全の両方が危険にさらされる可能性があります。さらに、自動車データ管理ソフトウェアのメンテナンスの問題は、市場の拡大をさらに遅らせる。

COVID-19の影響:

数多くのサプライチェーンの混乱と自動車需要の落ち込みにより、COVID-19の流行は自動車産業に大きな影響を及ぼしています。しかし、自動車業界が移り変わる業界情勢に適応する方法を模索する中、パンデミックはデジタル技術やデータ管理ソリューションへの注目度を高める結果ともなっています。企業がダウンタイムやメンテナンスコストを削減する方法を模索する中、パンデミックは遠隔診断や予知保全ソリューションの採用も加速させています。一般的に、パンデミックは自動車データ管理市場に機会と課題を与えています。

予測期間中はクラウドセグメントが最大になると予想される:

クラウドセグメントは、予測期間全体を通じて市場を独占すると予測されます。コネクテッドカーや自律走行車では、クラウドコンピューティングが一般的になりつつあります。スケーラビリティの向上、市場投入までの時間の短縮、信頼性の向上、コスト効率の改善により、クラウド技術の採用は自動車産業を再構築しています。さらに、多くのソフトウェア開発者が自動車産業向けのクラウドベース技術に投資しており、これが同分野の成長を加速させています。

予測期間中、CAGRが最も高くなると予想されるのは非自律走行セグメントである:

非自律走行分野は予測期間中に急成長が見込まれます。非自律走行車は人間の介入なしでは走行できないです。連動しているが自律走行ではない自動車は、自動車データ管理の用途があります。さらに、コネクテッド・カーは、速度、モーターの状態、走行距離など、さまざまな変数に基づいてデータを生成します。自動車のエンターテインメント・システム、コントローラー・アクセス・ネットワーク、電気制御ユニットはすべて、運転体験を向上させる情報を提供します。こうした要因の結果、このセグメントは拡大しています。

最もシェアの高い地域:

予測期間中、北米はトップクラスの自動車メーカーやソフトウェア開発企業が広く存在し、自動車の生産と販売が継続的に伸びていること、最先端技術が広く採用されていること、可処分所得水準が高いことから、市場で大きなシェアを獲得すると予想されます。また、米国では、道路や高速道路での自律走行車の走行を許可する交通規制が整備され、自動運転車の試験や利用が急速に拡大していることも、今後の同地域の市場成長に拍車をかけると予想される重要な要因です。さらに、米国とカナダでUBI(利用者ベースの保険)が受け入れられつつあること、IT企業と自動車メーカーの戦略的提携が増加していることも、この地域の成長を促進すると予想される重要な要因です。

CAGRが最も高い地域:

欧州地域市場の有利な成長は、主に車両エレクトロニクス設計の進歩、車両生産の増加、車車間(V2V)および車車間インフラ(V2I)通信、連結車両販売の増加、重要なOEMの出現によるものです。欧州の影響もあり、コネクテッドカー市場は拡大しています。さらに、車両データ管理のための革新的で画期的な製品やサービスが、消費者向けに現地の事業者によって開発されており、この地域の成長を後押ししています。

主な発展:

2022年10月、マイクロソフトは、融資、リース、自動車定期購入、レンタカー、車両管理を提供するメルセデス・ベンツと提携しました。両社は、物理的な世界とデジタルの世界を融合させ、価値創造を推進することを目指しました。さらに、メルセデス・ベンツは、変化と不確実性が続く中、生産性を向上させ、生態系への影響を軽減するために、製造手順を現場に導入する前に、マイクロソフトのクラウド上で無限にシミュレーションし、改良することができます。

2022年10月、AWSは世界有数の自動車・オートバイのプレミアムメーカーであるBMWと手を組みました。この協業を通じて、両社はBMWの車両信号と車両インテリジェンス・データを含むソリューションを提供し、クラウド上でデータを安全に処理し、ルーティングすることを目指しました。さらに、AWSとBMWグループは、Software-Defined Transportationのコンセプトを実現し、道路を走る車両の能力を向上させることを熱望しています。

2022年3月、ACTIAとSibros Technologies Inc.は、ACU6テレマティクス技術に関する戦略的提携契約を締結しました。二輪車、大型運搬車、軽乗用車分野のOEM自動車メーカーにとって、この共同ソリューションは、連動した車両設計と技術革新の改善につながると期待されています。

レポート内容

- 地域レベルおよび国レベルの市場シェア評価

- 新規参入企業への戦略的提言

- 2021年、2022年、2023年、2026年、2030年の市場データを網羅

- 市場動向(推進要因、制約、機会、脅威、課題、投資機会、推奨事項)

- 市場推定に基づく主要ビジネスセグメントにおける戦略的提言

- 主要な共通トレンドをマッピングした競合情勢

- 詳細な戦略、財務、最近の動向を含む企業プロファイル

- 最新の技術的進歩をマッピングしたサプライチェーン動向

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下のいずれかの無料カスタマイズオプションをご提供いたします:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- エグゼクティブサマリー

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 一次調査情報源

- 二次調査情報源

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- アプリケーション分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

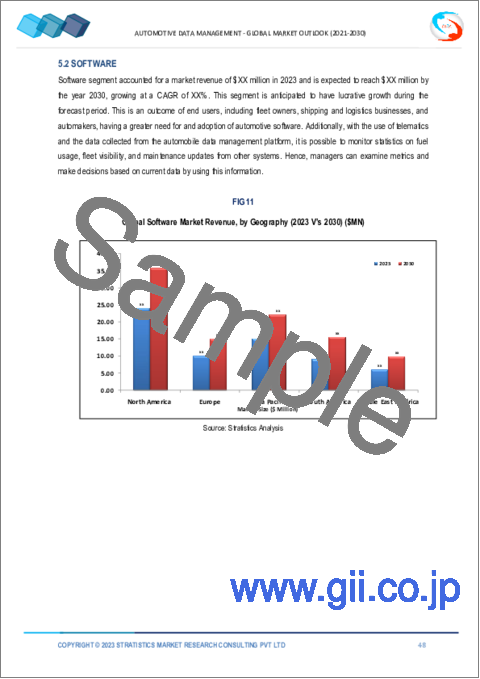

第5章 自動車データ管理の世界市場:コンポーネント別

- ソフトウェア

- データセキュリティ

- データ統合

- データ品質

- データ移行

- サービス

- プロフェッショナル

- マネージド

第6章 自動車データ管理の世界市場:データタイプ別

- 構造化

- 非構造化

第7章 自動車データ管理の世界市場:車両タイプ別

- 自律型

- 非自律型

第8章 自動車データ管理の世界市場:展開別

- オンプレミス

- クラウド

第9章 自動車データ管理の世界市場:用途別

- ディーラーパフォーマンス分析

- 促進要因とユーザーの行動分析

- 予知保全

- 安全・セキュリティ管理

- 利用ベースの保険(UBI)

- 保証分析

- その他の用途

第10章 自動車データ管理の世界市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第11章 主な発展

- 契約、パートナーシップ、提携、合弁事業

- 買収と合併

- 新製品の上市

- 事業拡大

- その他の主要戦略

第12章 企業プロファイル

- Acerta

- Agnik LLC

- Amazon Web Services, Inc.

- AMO Foundation

- Amodo

- Azuga

- Caruso Gmbh

- ETL Solution Ltd

- HEAVY.AI

- IBM Corporation

- Intellias

- Microsoft

- National Instrument Corp

- Netapp

- Otonomo Technologies Ltd

- Procon Analytics

- SAP SE

- Sibros Technologies Inc.

- Teradat Tech

- Vinli

- Xevo

List of Tables

- Table 1 Global Automotive Data Management Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Automotive Data Management Market Outlook, By Component (2021-2030) ($MN)

- Table 3 Global Automotive Data Management Market Outlook, By Software (2021-2030) ($MN)

- Table 4 Global Automotive Data Management Market Outlook, By Data Security (2021-2030) ($MN)

- Table 5 Global Automotive Data Management Market Outlook, By Data Integration (2021-2030) ($MN)

- Table 6 Global Automotive Data Management Market Outlook, By Data Quality (2021-2030) ($MN)

- Table 7 Global Automotive Data Management Market Outlook, By Data Migration (2021-2030) ($MN)

- Table 8 Global Automotive Data Management Market Outlook, By Service (2021-2030) ($MN)

- Table 9 Global Automotive Data Management Market Outlook, By Professional (2021-2030) ($MN)

- Table 10 Global Automotive Data Management Market Outlook, By Managed (2021-2030) ($MN)

- Table 11 Global Automotive Data Management Market Outlook, By Data Type (2021-2030) ($MN)

- Table 12 Global Automotive Data Management Market Outlook, By Structured (2021-2030) ($MN)

- Table 13 Global Automotive Data Management Market Outlook, By Unstructured (2021-2030) ($MN)

- Table 14 Global Automotive Data Management Market Outlook, By Vehicle Type (2021-2030) ($MN)

- Table 15 Global Automotive Data Management Market Outlook, By Autonomous (2021-2030) ($MN)

- Table 16 Global Automotive Data Management Market Outlook, By Non-autonomous (2021-2030) ($MN)

- Table 17 Global Automotive Data Management Market Outlook, By Deployment (2021-2030) ($MN)

- Table 18 Global Automotive Data Management Market Outlook, By On-premise (2021-2030) ($MN)

- Table 19 Global Automotive Data Management Market Outlook, By Cloud (2021-2030) ($MN)

- Table 20 Global Automotive Data Management Market Outlook, By Application (2021-2030) ($MN)

- Table 21 Global Automotive Data Management Market Outlook, By Dealer Performance Analysis (2021-2030) ($MN)

- Table 22 Global Automotive Data Management Market Outlook, By Driver & User Behavior Analysis (2021-2030) ($MN)

- Table 23 Global Automotive Data Management Market Outlook, By Predictive Maintenance (2021-2030) ($MN)

- Table 24 Global Automotive Data Management Market Outlook, By Safety & Security Management (2021-2030) ($MN)

- Table 25 Global Automotive Data Management Market Outlook, By Usage-Based Insurance (UBI) (2021-2030) ($MN)

- Table 26 Global Automotive Data Management Market Outlook, By Warranty Analytics (2021-2030) ($MN)

- Table 27 Global Automotive Data Management Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 28 North America Automotive Data Management Market Outlook, By Country (2021-2030) ($MN)

- Table 29 North America Automotive Data Management Market Outlook, By Component (2021-2030) ($MN)

- Table 30 North America Automotive Data Management Market Outlook, By Software (2021-2030) ($MN)

- Table 31 North America Automotive Data Management Market Outlook, By Data Security (2021-2030) ($MN)

- Table 32 North America Automotive Data Management Market Outlook, By Data Integration (2021-2030) ($MN)

- Table 33 North America Automotive Data Management Market Outlook, By Data Quality (2021-2030) ($MN)

- Table 34 North America Automotive Data Management Market Outlook, By Data Migration (2021-2030) ($MN)

- Table 35 North America Automotive Data Management Market Outlook, By Service (2021-2030) ($MN)

- Table 36 North America Automotive Data Management Market Outlook, By Professional (2021-2030) ($MN)

- Table 37 North America Automotive Data Management Market Outlook, By Managed (2021-2030) ($MN)

- Table 38 North America Automotive Data Management Market Outlook, By Data Type (2021-2030) ($MN)

- Table 39 North America Automotive Data Management Market Outlook, By Structured (2021-2030) ($MN)

- Table 40 North America Automotive Data Management Market Outlook, By Unstructured (2021-2030) ($MN)

- Table 41 North America Automotive Data Management Market Outlook, By Vehicle Type (2021-2030) ($MN)

- Table 42 North America Automotive Data Management Market Outlook, By Autonomous (2021-2030) ($MN)

- Table 43 North America Automotive Data Management Market Outlook, By Non-autonomous (2021-2030) ($MN)

- Table 44 North America Automotive Data Management Market Outlook, By Deployment (2021-2030) ($MN)

- Table 45 North America Automotive Data Management Market Outlook, By On-premise (2021-2030) ($MN)

- Table 46 North America Automotive Data Management Market Outlook, By Cloud (2021-2030) ($MN)

- Table 47 North America Automotive Data Management Market Outlook, By Application (2021-2030) ($MN)

- Table 48 North America Automotive Data Management Market Outlook, By Dealer Performance Analysis (2021-2030) ($MN)

- Table 49 North America Automotive Data Management Market Outlook, By Driver & User Behavior Analysis (2021-2030) ($MN)

- Table 50 North America Automotive Data Management Market Outlook, By Predictive Maintenance (2021-2030) ($MN)

- Table 51 North America Automotive Data Management Market Outlook, By Safety & Security Management (2021-2030) ($MN)

- Table 52 North America Automotive Data Management Market Outlook, By Usage-Based Insurance (UBI) (2021-2030) ($MN)

- Table 53 North America Automotive Data Management Market Outlook, By Warranty Analytics (2021-2030) ($MN)

- Table 54 North America Automotive Data Management Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 55 Europe Automotive Data Management Market Outlook, By Country (2021-2030) ($MN)

- Table 56 Europe Automotive Data Management Market Outlook, By Component (2021-2030) ($MN)

- Table 57 Europe Automotive Data Management Market Outlook, By Software (2021-2030) ($MN)

- Table 58 Europe Automotive Data Management Market Outlook, By Data Security (2021-2030) ($MN)

- Table 59 Europe Automotive Data Management Market Outlook, By Data Integration (2021-2030) ($MN)

- Table 60 Europe Automotive Data Management Market Outlook, By Data Quality (2021-2030) ($MN)

- Table 61 Europe Automotive Data Management Market Outlook, By Data Migration (2021-2030) ($MN)

- Table 62 Europe Automotive Data Management Market Outlook, By Service (2021-2030) ($MN)

- Table 63 Europe Automotive Data Management Market Outlook, By Professional (2021-2030) ($MN)

- Table 64 Europe Automotive Data Management Market Outlook, By Managed (2021-2030) ($MN)

- Table 65 Europe Automotive Data Management Market Outlook, By Data Type (2021-2030) ($MN)

- Table 66 Europe Automotive Data Management Market Outlook, By Structured (2021-2030) ($MN)

- Table 67 Europe Automotive Data Management Market Outlook, By Unstructured (2021-2030) ($MN)

- Table 68 Europe Automotive Data Management Market Outlook, By Vehicle Type (2021-2030) ($MN)

- Table 69 Europe Automotive Data Management Market Outlook, By Autonomous (2021-2030) ($MN)

- Table 70 Europe Automotive Data Management Market Outlook, By Non-autonomous (2021-2030) ($MN)

- Table 71 Europe Automotive Data Management Market Outlook, By Deployment (2021-2030) ($MN)

- Table 72 Europe Automotive Data Management Market Outlook, By On-premise (2021-2030) ($MN)

- Table 73 Europe Automotive Data Management Market Outlook, By Cloud (2021-2030) ($MN)

- Table 74 Europe Automotive Data Management Market Outlook, By Application (2021-2030) ($MN)

- Table 75 Europe Automotive Data Management Market Outlook, By Dealer Performance Analysis (2021-2030) ($MN)

- Table 76 Europe Automotive Data Management Market Outlook, By Driver & User Behavior Analysis (2021-2030) ($MN)

- Table 77 Europe Automotive Data Management Market Outlook, By Predictive Maintenance (2021-2030) ($MN)

- Table 78 Europe Automotive Data Management Market Outlook, By Safety & Security Management (2021-2030) ($MN)

- Table 79 Europe Automotive Data Management Market Outlook, By Usage-Based Insurance (UBI) (2021-2030) ($MN)

- Table 80 Europe Automotive Data Management Market Outlook, By Warranty Analytics (2021-2030) ($MN)

- Table 81 Europe Automotive Data Management Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 82 Asia Pacific Automotive Data Management Market Outlook, By Country (2021-2030) ($MN)

- Table 83 Asia Pacific Automotive Data Management Market Outlook, By Component (2021-2030) ($MN)

- Table 84 Asia Pacific Automotive Data Management Market Outlook, By Software (2021-2030) ($MN)

- Table 85 Asia Pacific Automotive Data Management Market Outlook, By Data Security (2021-2030) ($MN)

- Table 86 Asia Pacific Automotive Data Management Market Outlook, By Data Integration (2021-2030) ($MN)

- Table 87 Asia Pacific Automotive Data Management Market Outlook, By Data Quality (2021-2030) ($MN)

- Table 88 Asia Pacific Automotive Data Management Market Outlook, By Data Migration (2021-2030) ($MN)

- Table 89 Asia Pacific Automotive Data Management Market Outlook, By Service (2021-2030) ($MN)

- Table 90 Asia Pacific Automotive Data Management Market Outlook, By Professional (2021-2030) ($MN)

- Table 91 Asia Pacific Automotive Data Management Market Outlook, By Managed (2021-2030) ($MN)

- Table 92 Asia Pacific Automotive Data Management Market Outlook, By Data Type (2021-2030) ($MN)

- Table 93 Asia Pacific Automotive Data Management Market Outlook, By Structured (2021-2030) ($MN)

- Table 94 Asia Pacific Automotive Data Management Market Outlook, By Unstructured (2021-2030) ($MN)

- Table 95 Asia Pacific Automotive Data Management Market Outlook, By Vehicle Type (2021-2030) ($MN)

- Table 96 Asia Pacific Automotive Data Management Market Outlook, By Autonomous (2021-2030) ($MN)

- Table 97 Asia Pacific Automotive Data Management Market Outlook, By Non-autonomous (2021-2030) ($MN)

- Table 98 Asia Pacific Automotive Data Management Market Outlook, By Deployment (2021-2030) ($MN)

- Table 99 Asia Pacific Automotive Data Management Market Outlook, By On-premise (2021-2030) ($MN)

- Table 100 Asia Pacific Automotive Data Management Market Outlook, By Cloud (2021-2030) ($MN)

- Table 101 Asia Pacific Automotive Data Management Market Outlook, By Application (2021-2030) ($MN)

- Table 102 Asia Pacific Automotive Data Management Market Outlook, By Dealer Performance Analysis (2021-2030) ($MN)

- Table 103 Asia Pacific Automotive Data Management Market Outlook, By Driver & User Behavior Analysis (2021-2030) ($MN)

- Table 104 Asia Pacific Automotive Data Management Market Outlook, By Predictive Maintenance (2021-2030) ($MN)

- Table 105 Asia Pacific Automotive Data Management Market Outlook, By Safety & Security Management (2021-2030) ($MN)

- Table 106 Asia Pacific Automotive Data Management Market Outlook, By Usage-Based Insurance (UBI) (2021-2030) ($MN)

- Table 107 Asia Pacific Automotive Data Management Market Outlook, By Warranty Analytics (2021-2030) ($MN)

- Table 108 Asia Pacific Automotive Data Management Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 109 South America Automotive Data Management Market Outlook, By Country (2021-2030) ($MN)

- Table 110 South America Automotive Data Management Market Outlook, By Component (2021-2030) ($MN)

- Table 111 South America Automotive Data Management Market Outlook, By Software (2021-2030) ($MN)

- Table 112 South America Automotive Data Management Market Outlook, By Data Security (2021-2030) ($MN)

- Table 113 South America Automotive Data Management Market Outlook, By Data Integration (2021-2030) ($MN)

- Table 114 South America Automotive Data Management Market Outlook, By Data Quality (2021-2030) ($MN)

- Table 115 South America Automotive Data Management Market Outlook, By Data Migration (2021-2030) ($MN)

- Table 116 South America Automotive Data Management Market Outlook, By Service (2021-2030) ($MN)

- Table 117 South America Automotive Data Management Market Outlook, By Professional (2021-2030) ($MN)

- Table 118 South America Automotive Data Management Market Outlook, By Managed (2021-2030) ($MN)

- Table 119 South America Automotive Data Management Market Outlook, By Data Type (2021-2030) ($MN)

- Table 120 South America Automotive Data Management Market Outlook, By Structured (2021-2030) ($MN)

- Table 121 South America Automotive Data Management Market Outlook, By Unstructured (2021-2030) ($MN)

- Table 122 South America Automotive Data Management Market Outlook, By Vehicle Type (2021-2030) ($MN)

- Table 123 South America Automotive Data Management Market Outlook, By Autonomous (2021-2030) ($MN)

- Table 124 South America Automotive Data Management Market Outlook, By Non-autonomous (2021-2030) ($MN)

- Table 125 South America Automotive Data Management Market Outlook, By Deployment (2021-2030) ($MN)

- Table 126 South America Automotive Data Management Market Outlook, By On-premise (2021-2030) ($MN)

- Table 127 South America Automotive Data Management Market Outlook, By Cloud (2021-2030) ($MN)

- Table 128 South America Automotive Data Management Market Outlook, By Application (2021-2030) ($MN)

- Table 129 South America Automotive Data Management Market Outlook, By Dealer Performance Analysis (2021-2030) ($MN)

- Table 130 South America Automotive Data Management Market Outlook, By Driver & User Behavior Analysis (2021-2030) ($MN)

- Table 131 South America Automotive Data Management Market Outlook, By Predictive Maintenance (2021-2030) ($MN)

- Table 132 South America Automotive Data Management Market Outlook, By Safety & Security Management (2021-2030) ($MN)

- Table 133 South America Automotive Data Management Market Outlook, By Usage-Based Insurance (UBI) (2021-2030) ($MN)

- Table 134 South America Automotive Data Management Market Outlook, By Warranty Analytics (2021-2030) ($MN)

- Table 135 South America Automotive Data Management Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 136 Middle East & Africa Automotive Data Management Market Outlook, By Country (2021-2030) ($MN)

- Table 137 Middle East & Africa Automotive Data Management Market Outlook, By Component (2021-2030) ($MN)

- Table 138 Middle East & Africa Automotive Data Management Market Outlook, By Software (2021-2030) ($MN)

- Table 139 Middle East & Africa Automotive Data Management Market Outlook, By Data Security (2021-2030) ($MN)

- Table 140 Middle East & Africa Automotive Data Management Market Outlook, By Data Integration (2021-2030) ($MN)

- Table 141 Middle East & Africa Automotive Data Management Market Outlook, By Data Quality (2021-2030) ($MN)

- Table 142 Middle East & Africa Automotive Data Management Market Outlook, By Data Migration (2021-2030) ($MN)

- Table 143 Middle East & Africa Automotive Data Management Market Outlook, By Service (2021-2030) ($MN)

- Table 144 Middle East & Africa Automotive Data Management Market Outlook, By Professional (2021-2030) ($MN)

- Table 145 Middle East & Africa Automotive Data Management Market Outlook, By Managed (2021-2030) ($MN)

- Table 146 Middle East & Africa Automotive Data Management Market Outlook, By Data Type (2021-2030) ($MN)

- Table 147 Middle East & Africa Automotive Data Management Market Outlook, By Structured (2021-2030) ($MN)

- Table 148 Middle East & Africa Automotive Data Management Market Outlook, By Unstructured (2021-2030) ($MN)

- Table 149 Middle East & Africa Automotive Data Management Market Outlook, By Vehicle Type (2021-2030) ($MN)

- Table 150 Middle East & Africa Automotive Data Management Market Outlook, By Autonomous (2021-2030) ($MN)

- Table 151 Middle East & Africa Automotive Data Management Market Outlook, By Non-autonomous (2021-2030) ($MN)

- Table 152 Middle East & Africa Automotive Data Management Market Outlook, By Deployment (2021-2030) ($MN)

- Table 153 Middle East & Africa Automotive Data Management Market Outlook, By On-premise (2021-2030) ($MN)

- Table 154 Middle East & Africa Automotive Data Management Market Outlook, By Cloud (2021-2030) ($MN)

- Table 155 Middle East & Africa Automotive Data Management Market Outlook, By Application (2021-2030) ($MN)

- Table 156 Middle East & Africa Automotive Data Management Market Outlook, By Dealer Performance Analysis (2021-2030) ($MN)

- Table 157 Middle East & Africa Automotive Data Management Market Outlook, By Driver & User Behavior Analysis (2021-2030) ($MN)

- Table 158 Middle East & Africa Automotive Data Management Market Outlook, By Predictive Maintenance (2021-2030) ($MN)

- Table 159 Middle East & Africa Automotive Data Management Market Outlook, By Safety & Security Management (2021-2030) ($MN)

- Table 160 Middle East & Africa Automotive Data Management Market Outlook, By Usage-Based Insurance (UBI) (2021-2030) ($MN)

- Table 161 Middle East & Africa Automotive Data Management Market Outlook, By Warranty Analytics (2021-2030) ($MN)

- Table 162 Middle East & Africa Automotive Data Management Market Outlook, By Other Applications (2021-2030) ($MN)

According to Stratistics MRC, the Global Automotive Data Management Market is accounted for $2.21 billion in 2023 and is expected to reach $7.17 billion by 2030 growing at a CAGR of 18.3% during the forecast period. Automotive data management is the process of gathering, storing, processing, and analyzing data generated by vehicles and their components. This information includes details about how the car operated, the driver's actions, the environment, and other important factors. Data is gathered using a variety of sensors and devices that are installed in the vehicle in order to improve performance, reduce maintenance costs, and improve the overall driving experience.

According to statista.com, an estimated 84 million connected vehicles were found on the roads in the U.S. in 2021. The market for connected vehicles has been growing in recent years, which is expected to continue.

Market Dynamics:

Driver:

Increasing demand for connected and electric vehicles

The growing demand for connected vehicles is one of the key factors driving the global market for automotive data management. Huge amounts of data are generated by connected vehicles' operation, location, and use. Automobile manufacturers and other stakeholders can benefit from the collection, processing, and analysis of this data by using automotive data management systems to improve driver safety and vehicle performance. Furthermore, the growing acceptance of electrified cars is another factor driving the global market. Electric vehicles generate a variety of data compared to conventional internal combustion engine vehicles, such as battery charge level and energy usage. Due to advancements in the auto industry like lightweight vehicles and electric mobility, the market is advancing.

Restraint:

High implementation cost and lack of skilled professionals

Implementing automotive data management solutions can be expensive, particularly for small and medium-sized businesses, which could limit the market's expansion. Additionally, the development of the market may be constrained by a lack of qualified professionals who can implement and maintain automotive data management solutions.

Opportunity:

Growing demand for cloud-based solutions and data analytics

The growing demand for data analytics is one of the key business opportunities for the global automotive data management market. Utilizing automotive data management systems, automakers and other stakeholders can analyze enormous amounts of vehicle data to identify trends and patterns, enabling data-driven decision-making and vehicle performance improvement. The expanding use of cloud-based solutions also represents another significant area of business opportunity, as cloud-based solutions are more flexible, scalable, and cost-effective, and businesses of all sizes prefer them. Therefore, automotive data management solutions can benefit from this trend by offering cloud-based solutions that enable real-time data access and insights.

Threat:

Rising cybersecurity issues

Automotive data management market growth is anticipated to be negatively impacted by the rising number of cybersecurity issues with connected and self-driving vehicles. The same cybersecurity risks that affect other connected devices also affect connected vehicles. As a result of connected vehicles' extensive data transmission over the internet, hackers may target them in an effort to access that data or take over the systems of the car. Both the vehicle's physical integrity and the safety of the passengers may be at risk as a result of this. In addition, the maintenance problems with automotive data management software slow the market's expansion even more.

COVID-19 Impact:

With numerous supply chain disruptions and a drop in demand for vehicles, the COVID-19 pandemic has had a significant effect on the automotive industry. However, as the automotive industry searches for ways to adjust to the shifting landscape, the pandemic has also resulted in a greater focus on digital technologies and data management solutions. As businesses look for ways to cut downtime and maintenance costs, the pandemic has also accelerated the adoption of remote diagnostics and predictive maintenance solutions. In general, the pandemic has given the automotive data management market opportunities as well as challenges.

The cloud segment is expected to be the largest during the forecast period:

The cloud segment is anticipated to rule the market for the entire forecast period. In connected and autonomous vehicles, cloud computing is becoming more common. By facilitating greater scalability, quicker time-to-market, increased dependability, and enhanced cost-efficiency, the adoption of cloud technologies is reshaping the automotive industry. Moreover, numerous software developers are investing in cloud-based technologies for the automotive industry, which is accelerating the segment's growth.

The non-autonomous segment is expected to have the highest CAGR during the forecast period:

The non-autonomous sector is anticipated to experience rapid growth during the forecast period. Non-autonomous cars cannot run without human intervention. Automobiles that are linked but not autonomous have uses for automotive data management. Moreover, connected vehicles produce data based on a variety of variables, including speed, motor condition, and distance travelled. The entertainment system, controller access network, and electric control unit of the car all provide information that enhances the driving experience. As a result of such factors, the segment is expanding.

Region with largest share:

Over the course of the prediction period, North America is anticipated to gain a significant share of the market due to the region's widespread presence of top automakers and software development firms, ongoing growth in vehicle production and sales, widespread adoption of cutting-edge technologies, and high levels of disposable income. Another significant factor anticipated to spur future regional market growth is the rapidly expanding testing and use of self-driving cars in the US due to favorable traffic regulations that permit autonomous vehicles to operate on roads and highways. Additionally, the growing acceptance of UBI (Usage-based Insurance) in the US and Canada, as well as the rise in IT companies' and automakers' strategic alliances, are other significant factors anticipated to propel growth in this region.

Region with highest CAGR:

The lucrative growth of the regional market in Europe is primarily due to advancements in vehicle electronics design, increased vehicle production, vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication, rising linked vehicle sales, and the emergence of significant OEMs. Due in large part to Europe, the market for connected cars is expanding. Additionally, innovative and ground-breaking products and services for vehicle data administration are being developed by local business players for consumers, aiding the region's growth.

Key players in the market

Some of the key players profiled in the Automotive Data Management Market include Acerta, Agnik LLC, Amazon Web Services, Inc., AMO Foundation, Amodo, Azuga, Caruso Gmbh, ETL Solution Ltd, HEAVY.AI, IBM Corporation, Intellias, Microsoft, National Instrument Corp, Netapp, Otonomo Technologies Ltd, Procon Analytics, SAP SE, Sibros Technologies Inc., Teradat Tech, Vinli and Xevo.

Key Developments:

In October 2022, Microsoft joined hands with Mercedes-Benz, which offers financing, leasing, car subscription and car rental, and fleet management. Together, the companies aimed to combine the physical and digital worlds to propel value creation. Moreover, Mercedes-Benz can simulate and refine manufacturing procedures infinitely in the Microsoft Cloud before getting them to the shop floor to improve productivity and reduce their ecological effect amid ongoing change and uncertainty.

In October 2022, AWS joined hands with BMW, the world's foremost premium manufacturer of automobiles and motorcycles. Through this collaboration, the companies aimed to provide a solution that contains BMW vehicle signals and fleet intelligence data, then securely procedures and route the data in the cloud. Moreover, AWS and BMW Group are eager to make the concept of software-defined transportation an existence and to improve the abilities of vehicles on the road.

In March 2022, ACTIA and Sibros Technologies Inc. signed a strategic collaboration agreement for the ACU6 telematics technology. For OEM automakers in the motorbike, heavy-duty haulage, and light passenger sectors, this joint solution is anticipated to improve linked vehicle design and innovation.

Components Covered:

- Software

- Service

Data Types Covered:

- Structured

- Unstructured

Vehicle Types Covered:

- Autonomous

- Non-autonomous

Deployments Covered:

- On-premise

- Cloud

Application Covered:

- Dealer Performance Analysis

- Driver & User Behavior Analysis

- Predictive Maintenance

- Safety & Security Management

- Usage-Based Insurance (UBI)

- Warranty Analytics

- Other Applications

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026 and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Automotive Data Management Market, By Component

- 5.1 Introduction

- 5.2 Software

- 5.2.1 Data Security

- 5.2.2 Data Integration

- 5.2.3 Data Quality

- 5.2.4 Data Migration

- 5.3 Service

- 5.3.1 Professional

- 5.3.2 Managed

6 Global Automotive Data Management Market, By Data Type

- 6.1 Introduction

- 6.2 Structured

- 6.3 Unstructured

7 Global Automotive Data Management Market, By Vehicle Type

- 7.1 Introduction

- 7.2 Autonomous

- 7.3 Non-autonomous

8 Global Automotive Data Management Market, By Deployment

- 8.1 Introduction

- 8.2 On-premise

- 8.3 Cloud

9 Global Automotive Data Management Market, By Application

- 9.1 Introduction

- 9.2 Dealer Performance Analysis

- 9.3 Driver & User Behavior Analysis

- 9.4 Predictive Maintenance

- 9.5 Safety & Security Management

- 9.6 Usage-Based Insurance (UBI)

- 9.7 Warranty Analytics

- 9.8 Other Applications

10 Global Automotive Data Management Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.5 South America

- 10.5.1 Argentina

- 10.5.2 Brazil

- 10.5.3 Chile

- 10.5.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 Acerta

- 12.2 Agnik LLC

- 12.3 Amazon Web Services, Inc.

- 12.4 AMO Foundation

- 12.5 Amodo

- 12.6 Azuga

- 12.7 Caruso Gmbh

- 12.8 ETL Solution Ltd

- 12.9 HEAVY.AI

- 12.10 IBM Corporation

- 12.11 Intellias

- 12.12 Microsoft

- 12.13 National Instrument Corp

- 12.14 Netapp

- 12.15 Otonomo Technologies Ltd

- 12.16 Procon Analytics

- 12.17 SAP SE

- 12.18 Sibros Technologies Inc.

- 12.19 Teradat Tech

- 12.20 Vinli

- 12.21 Xevo