|

|

市場調査レポート

商品コード

1363939

デジタル戦場の世界市場:2023-2030年Global Digital Battlefield Market 2023-2030 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| デジタル戦場の世界市場:2023-2030年 |

|

出版日: 2023年09月20日

発行: Orion Market Research

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

世界のデジタル戦場市場は、予測期間中(2023-2030年)に15.4%というかなりのCAGRで成長すると予測されています。デジタル戦場は、接続された監視、通信、武器、空中プラットフォームのネットワークです。戦略的意思決定のためにリアルタイムの状況認識情報を提供します。高度な通信・ネットワーク技術に対する需要の高まりが、デジタル戦場市場を牽引しています。先進的な通信・ネットワーキング技術が軍隊でどのように利用されているかの一例として、米国陸軍のJADC2(Joint All-Domain Command and Control)システムがあります。JADC2は、陸軍がすべての領域(陸、空、海、宇宙、サイバー)にまたがるセンサー、射撃手、意思決定者をリアルタイムで接続できるようにする戦争へのネットワーク中心アプローチです。JADC2は、5G、人工知能(AI)、機械学習(ML)など、さまざまな先進的通信・ネットワーク技術に依存しています。これらの技術により、陸軍は情報を共有し、より効果的に行動を調整できるようになり、同時に状況認識と意思決定能力も向上します。

デジタル戦場にはいくつかの制約もあり、そのひとつがコストです。デジタル戦場技術の開発と配備には非常に費用がかかります。これは一部の軍隊、特に予算が限られている軍隊にとっては障壁となり得ます。現実の例で言えば、5Gネットワークの開発と展開にかかるコストは、一部の軍にとって大きな障壁となっています。

セグメント別の展望

デジタルツインのサブセグメントが世界のデジタル戦場市場でかなりのシェアを占めると予想されます。

技術の中では、デジタルツインのサブセグメントが市場のかなりのシェアを占めると予想され、さらに予測期間中にかなりのCAGRで成長すると予測されています。デジタルツイン技術とは、複雑な技術データを統合して、物理的な製品を仮想的に表現する技術のことです。この技術は、デジタル戦場製品のライフサイクル全体を刺激し、その挙動を予測し、設計を最適化することができます。データ分析、AI、ML機能を組み込むことができます。また、リアルタイムの設計変更、使用条件、いくつかの性能変数の潜在的な影響を実証することもできます。例えば、2021年4月には、米国空軍の兵器専門部隊が、実物のコンピュータ化された表現を利用して、空軍の新型ジェット練習機を設計・試作しています。軍需企業がオンラインで互いの設計を競い合うことで、リアルタイムのデジタル・バーチャル・バージョン、つまりデジタルツインが作成され、空軍が兵器を開発・試験する際の助けとなります。

地域別展望

世界のデジタル戦場市場は、北米(米国、カナダ)、欧州(英国、イタリア、スペイン、ドイツ、フランス、その他欧州地域)、アジア太平洋地域(インド、中国、日本、韓国、その他アジア地域)、世界のその他の地域(中東とアフリカ、ラテンアメリカ)を含む地域別にさらに細分化されます。なかでも北米は、現代戦への需要の高まりと相まって研究開発活動が活発化していることから、世界のデジタル戦場市場で大きなシェアを占めています。

アジア太平洋地域はデジタル戦場の世界市場で大きなCAGRで成長する見込み

全地域の中で、アジア太平洋地域は予測期間中、世界的に顕著なCAGRで成長すると予想されています。アジア太平洋地域の成長を促進する主な要因の1つは、人工知能、クラウドコンピューティング、5Gなどの進歩の増加です。現代の戦争とともに、日常生活のあらゆるものとAIの統合が広範に利用されています。デジタル戦場に関する調査の増加も、デジタル戦場市場を牽引する要因の1つです。

目次

第1章 レポート概要

- 業界の現状分析と成長可能性の展望

- 調査方法とツール

- 市場内訳

- セグメント別

- 地域別

第2章 市場概要と洞察

- 調査範囲

- アナリストの洞察と現在の市場動向

- 主な調査結果

- 推奨事項

- 結論

第3章 競合情勢

- 主要企業分析

- BAE Systems plc.

- 概要

- 財務分析

- SWOT分析

- 最近の動向

- Lockheed Martin Corp.

- 概要

- 財務分析

- SWOT分析

- 最近の動向

- Northrop Grumman.

- 概要

- 財務分析

- SWOT分析

- 最近の動向

- RTX Corp.

- 概要

- 財務分析

- SWOT分析

- 最近の動向

- THALES

- 概要

- 財務分析

- SWOT分析

- 最近の動向

- 主要戦略分析

第4章 市場セグメンテーション

- 世界のデジタル戦場市場:ソリューション別

- ハードウェア

- ソフトウェア

- サービス

- 世界のデジタル戦場市場:技術別

- 人工知能(AI)

- モノのインターネット(IoT)

- ビッグデータ分析

- ロボティック・プロセス・オートメーション(RPA)

- デジタルツイン

- その他(5G、仮想・拡張現実(VR & AR)、ブロックチェーン)

- 世界のデジタル戦場市場:プラットフォーム別

- 陸上

- 海軍

- 航空

- 宇宙

- 世界のデジタル戦場市場:用途別

- 戦争プラットフォーム

- サイバーセキュリティ

- 監視・状況認識(SSA)

- 指揮統制(C2)

- その他(訓練・シミュレーション)

第5章 地域分析

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- イタリア

- スペイン

- フランス

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋

- 世界のその他の地域

第6章 企業プロファイル

- Airbus

- Amazon Web Services, Inc.

- Anduril Ind. , Inc.

- Atos SE

- Boeing Co.

- Cobham Ltd.

- Cognite AS

- Curtiss-Wright Corp.

- Databricks, Inc.

- Elbit Systems Ltd.

- General Dynamics Corp.

- Google Cloud Platform(Google LLC.)

- GreyCastle Security, LLC

- HENSOLDT AG

- Hexagon AB

- IBM Corp.

- Indra

- Israel Aerospace Industries(IAI)

- Kongsberg Gruppen ASA

- L3Harris Technologies, Inc.

- Leonardo S.p.A.

- Microsoft

- Microsoft Azure(Microsoft)

- Palantir Technologies Inc.

- Rafael Advanced Defense Systems Ltd.

- Rebellion Defense, Inc.

- Rheinmetall AG

- Saab

- Snowflake Inc.

- Textron Inc.

LIST OF TABLES

- 1. GLOBAL DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY SOLUTION, 2023-2030 ($ MILLION)

- 2. GLOBAL HARDWARE FOR DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 3. GLOBAL SOFTWARE FOR DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 4. GLOBAL SERVICES FOR DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 5. GLOBAL DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY TECHNOLOGY, 2023-2030 ($ MILLION)

- 6. GLOBAL AI IN DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 7. GLOBAL IOT IN DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 8. GLOBAL BIG DATA ANALYTICS IN DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 9. GLOBAL RPA IN DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 10. GLOBAL OTHER TECHNOLOGIES IN DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 11. GLOBAL DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY PLATFORM, 2023-2030 ($ MILLION)

- 12. GLOBAL DIGITAL BATTLEFIELD FOR LAND MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 13. GLOBAL DIGITAL BATTLEFIELD FOR NAVAL MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 14. GLOBAL DIGITAL BATTLEFIELD FOR AIR MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 15. GLOBAL DIGITAL BATTLEFIELD FOR SPACE MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 16. GLOBAL DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY APPLICATION, 2023-2030 ($ MILLION)

- 17. GLOBAL DIGITAL BATTLEFIELD IN WARFARE PLATFORMS MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 18. GLOBAL DIGITAL BATTLEFIELD IN CYBERSECURITY MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 19. GLOBAL DIGITAL BATTLEFIELD IN SURVEILLANCE AND SITUATIONAL AWARENESS (SSA) MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 20. GLOBAL DIGITAL BATTLEFIELD IN COMMAND AND CONTROL (C2) MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 21. GLOBAL DIGITAL BATTLEFIELD IN OTHER APPLICATIONS MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 22. GLOBAL DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2030 ($ MILLION)

- 23. NORTH AMERICAN DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY COUNTRY, 2023-2030 ($ MILLION)

- 24. NORTH AMERICAN DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY SOLUTION, 2023-2030 ($ MILLION)

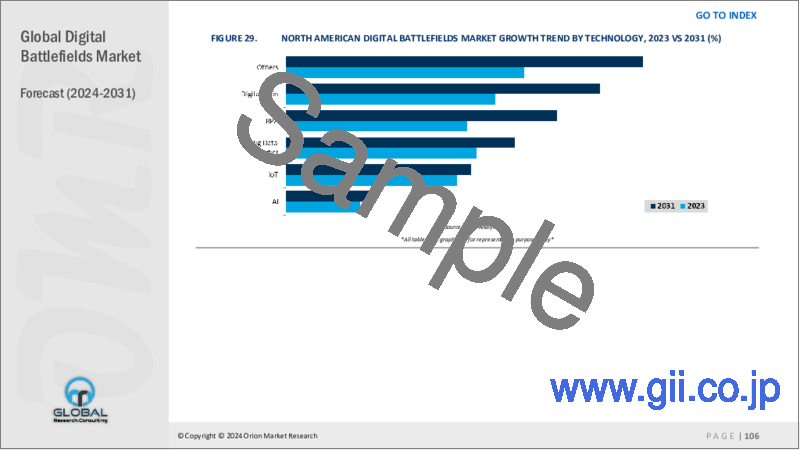

- 25. NORTH AMERICAN DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY TECHNOLOGY, 2023-2030 ($ MILLION)

- 26. NORTH AMERICAN DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY PLATFORM, 2023-2030 ($ MILLION)

- 27. NORTH AMERICAN DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY APPLICATION, 2023-2030 ($ MILLION)

- 28. EUROPEAN DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY COUNTRY, 2023-2030 ($ MILLION)

- 29. EUROPEAN DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY SOLUTION, 2023-2030 ($ MILLION)

- 30. EUROPEAN DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY TECHNOLOGY, 2023-2030 ($ MILLION)

- 31. EUROPEAN DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY PLATFORM, 2023-2030 ($ MILLION)

- 32. EUROPEAN DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY APPLICATION, 2023-2030 ($ MILLION)

- 33. ASIA- PACIFIC DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY COUNTRY, 2023-2030 ($ MILLION)

- 34. ASIA- PACIFIC DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY SOLUTION, 2023-2030 ($ MILLION)

- 35. ASIA- PACIFIC DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY TECHNOLOGY, 2023-2030 ($ MILLION)

- 36. ASIA- PACIFIC DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY PLATFORM, 2023-2030 ($ MILLION)

- 37. ASIA- PACIFIC DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY APPLICATION, 2023-2030 ($ MILLION)

- 38. REST OF THE WORLD DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY COUNTRY, 2023-2030 ($ MILLION)

- 39. REST OF THE WORLD DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY SOLUTION, 2023-2030 ($ MILLION)

- 40. REST OF THE WORLD DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY TECHNOLOGY, 2023-2030 ($ MILLION)

- 41. REST OF THE WORLD DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY PLATFORM, 2023-2030 ($ MILLION)

- 42. REST OF THE WORLD DIGITAL BATTLEFIELD MARKET RESEARCH AND ANALYSIS BY APPLICATION, 2023-2030 ($ MILLION)

LIST OF FIGURES

- 1. GLOBAL DIGITAL BATTLEFIELD MARKET SHARE BY SOLUTION, 2023 VS 2030 (%)

- 2. GLOBAL HARDWARE FOR DIGITAL BATTLEFIELD MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 3. GLOBAL SOFTWARE FOR DIGITAL BATTLEFIELD MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 4. GLOBAL SERVICES FOR DIGITAL BATTLEFIELD MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 5. GLOBAL DIGITAL BATTLEFIELD MARKET SHARE BY TECHNOLOGY, 2023 VS 2030 ($ MILLION)

- 6. GLOBAL AI IN DIGITAL BATTLEFIELD MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 7. GLOBAL IOT IN DIGITAL BATTLEFIELD MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 8. GLOBAL BIG DATA ANALYTICS IN DIGITAL BATTLEFIELD MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 9. GLOBAL RPA IN DIGITAL BATTLEFIELD MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 10. GLOBAL OTHER TECHNOLOGIES IN DIGITAL BATTLEFIELD MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 11. GLOBAL DIGITAL BATTLEFIELD MARKET SHARE BY PLATFORM, 2023 VS 2030 (%)

- 12. GLOBAL DIGITAL BATTLEFIELD FOR LAND MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 13. GLOBAL DIGITAL BATTLEFIELD FOR NAVAL MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 14. GLOBAL DIGITAL BATTLEFIELD FOR AIR MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 15. GLOBAL DIGITAL BATTLEFIELD FOR SPACE MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 16. GLOBAL DIGITAL BATTLEFIELD MARKET SHARE BY APPLICATION, 2023 VS 2030 (%)

- 17. GLOBAL DIGITAL BATTLEFIELD IN WARFARE PLATFORMS MARKET SHARE BY REGION, 2023 VS 2030 (%)

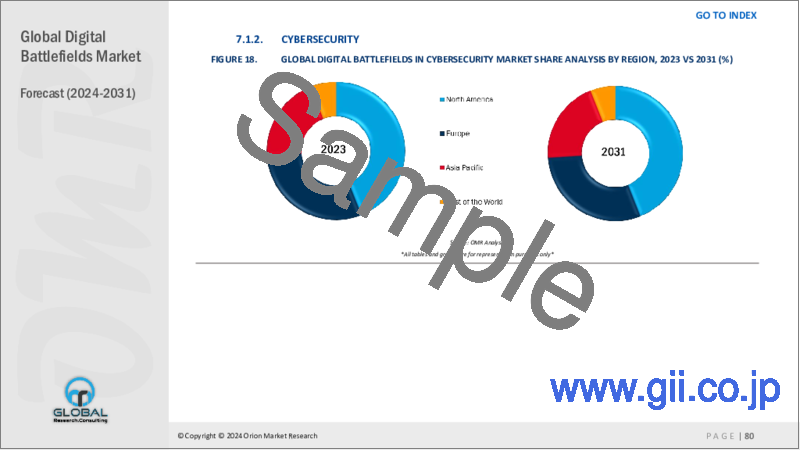

- 18. GLOBAL DIGITAL BATTLEFIELD IN CYBERSECURITY MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 19. GLOBAL DIGITAL BATTLEFIELD IN SURVEILLANCE AND SITUATIONAL AWARENESS (SSA) MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 20. GLOBAL DIGITAL BATTLEFIELD IN COMMAND AND CONTROL (C2) MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 21. GLOBAL DIGITAL BATTLEFIELD IN OTHER APPLICATIONS MARKET SHARE BY REGION, 2023 VS 2030 (%)

- 22. GLOBAL DIGITAL BATTLEFIELD MARKET SHARE BY REGION, 2022 VS 2030 (%)

- 23. US DIGITAL BATTLEFIELD MARKET SIZE, 2023-2030 ($ MILLION)

- 24. CANADA DIGITAL BATTLEFIELD MARKET SIZE, 2023-2030 ($ MILLION)

- 25. UK DIGITAL BATTLEFIELD MARKET SIZE, 2023-2030 ($ MILLION)

- 26. FRANCE DIGITAL BATTLEFIELD MARKET SIZE, 2023-2030 ($ MILLION)

- 27. GERMANY DIGITAL BATTLEFIELD MARKET SIZE, 2023-2030 ($ MILLION)

- 28. ITALY DIGITAL BATTLEFIELD MARKET SIZE, 2023-2030 ($ MILLION)

- 29. SPAIN DIGITAL BATTLEFIELD MARKET SIZE, 2023-2030 ($ MILLION)

- 30. REST OF EUROPE DIGITAL BATTLEFIELD MARKET SIZE, 2023-2030 ($ MILLION)

- 31. INDIA DIGITAL BATTLEFIELD MARKET SIZE, 2023-2030 ($ MILLION)

- 32. CHINA DIGITAL BATTLEFIELD MARKET SIZE, 2023-2030 ($ MILLION)

- 33. JAPAN DIGITAL BATTLEFIELD MARKET SIZE, 2023-2030 ($ MILLION)

- 34. SOUTH KOREA DIGITAL BATTLEFIELD MARKET SIZE, 2023-2030 ($ MILLION)

- 35. REST OF ASIA-PACIFIC DIGITAL BATTLEFIELD MARKET SIZE, 2023-2030 ($ MILLION)

- 36. REST OF THE WORLD DIGITAL BATTLEFIELD MARKET SIZE, 2023-2030 ($ MILLION)

Title: Global Digital Battlefields Market Size, Share & Trends Analysis Report by Solution (Hardware, Software, and Services), by Technology (Artificial Intelligence (AI), Internet of Things (IoT), Big Data Analytics, Robotics Process Automation (RPA), Digital Twin, and Others), by Platform (Land, Naval, Air, and Space), and by Application (Warfare Platforms, Cybersecurity, Surveillance and Situational Awareness (SSA), Command and Control (C2), and Others)Forecast Period (2023-2030).

The global digital battlefields market is anticipated to grow at a considerable CAGR of 15.4% during the forecast period (2023-2030). The digital battlefield is a network of connected surveillance, communication, weapon, and aerial platforms. It provides real-time situational awareness information for strategic decision-making. The increasing demand for advanced communication and networking technologies is driving the digital battlefields market. One example of how advanced communication and networking technologies are being used by militaries is the US Army's Joint All-Domain Command and Control (JADC2) system. JADC2 is a network-centric approach to warfare that enables the Army to connect its sensors, shooters, and decision-makers across all domains (land, air, sea, space, and cyber) in real-time. JADC2 relies on a variety of advanced communication and networking technologies, including 5G, artificial intelligence (AI), and machine learning (ML). These technologies enable the Army to share information and coordinate its actions more effectively, while also improving its situational awareness and decision-making capabilities.

The digital battlefields also has some constraints with it, one of which is the cost. Developing and deploying digital battlefield technologies can be very expensive. This can be a barrier for some militaries, especially those with limited budgets. If we take a real-life example then the cost of developing and deploying 5G networks has been a major barrier for some militaries.

Segmental Outlook

The global digital battlefields market is segmented based on solution, technology, platform, and application. Based on the solution, the market is sub-segmented into hardware, software, and services. Based on the technology, the market is sub-segmented into AI, IoT, big data analytics, RPA, and others. Based on the platform, the market is bifurcated into land, air, naval, and space. Based on the application, the market is sub-segmented into warfare platforms, cybersecurity, SSA, C2, and others.

Digital Twin Sub-Segment is Anticipated to Hold a Considerable Share of the Global Digital Battlefield Market

Among the technology, the digital twin sub-segment is expected to hold a considerable share of the market and is further anticipated to grow at a considerable CAGR over the forecast period. Digital twin technology refers to a complex collection of technical data is merged to make a virtual representation of a physical product. This technology can stimulate the entire life cycle of the digital battlefield product, predict its behavior, and optimize its design. It can incorporate data analytics, AI, and ML capabilities. It can also demonstrate the potential impact of real-time designs changes, usage conditions, and several performance variables. For instance, in April 2021, the new jet trainer aircraft for the Air force is being designed and prototyped by the US Air Force weapons specialties utilizing computerized representations of actual objects. By allowing military corporations to compete with one other's designs online, creating a digital virtual version of a real time, or a digital twin, which will aid the Air force in developing and testing weapons.

Regional Outlook

The global digital battlefields market is further segmented based on geography including North America (the US, and Canada), Europe (UK, Italy, Spain, Germany, France, and the Rest of Europe), Asia-Pacific (India, China, Japan, South Korea, and Rest of Asia), and the Rest of the World (the Middle East & Africa, and Latin America). Among these, North America holds a significant share of the global digital battlefields market owing to the surging R&D activities coupled with the increasing demand for modern warfare.

The Asia-Pacific Region is Expected to Grow at a Significant CAGR in the Global Digital Battlefields Market

Among all regions, the Asia-Pacific region is expected to grow at a prominent CAGR over the forecast period, globally. One of the primary factors driving the growth of the Asia-Pacific region is the increase in advancements in Artificial Intelligence, Cloud computing, 5G, etc. The integration of AI with everything in our daily life along with modern warfare is being used extensively. The increase in research on the digital battlefield is also one of the factors driving the digital battlefields market.

Market Players Outlook

The major companies serving the global digital battlefields market include BAE Systems plc., Lockheed Martin Corp., Northrop Grumman., RTX Corp., THALES, and others. The market players are considerably contributing to the market growth by the adoption of various strategies including mergers and acquisitions, partnerships, collaborations, funding, and new product launches, to stay competitive in the market. For instance, in June 2022, U.S. and Indian defense officials announced the creation of a joint technology accelerator aimed at increasing collaboration and interoperability between the two nations. Along with, the collaboration aims to establish AI & ML Unmanned Battlefield Tech Space Electronic Warfare Cyber Industry.

The Report Covers:

- Market value data analysis of 2023 and forecast to 2030.

- Annualized market revenues ($ million) for each market segment.

- Country-wise analysis of major geographical regions.

- Key companies operating in the global digital battlefields market. Based on the availability of data, information related to new product launches, and relevant news is also available in the report.

- Analysis of business strategies by identifying the key market segments positioned for strong growth in the future.

- Analysis of market-entry and market expansion strategies.

- Competitive strategies by identifying 'who-stands-where' in the market.

Table of Contents

1. Report Summary

- Current Industry Analysis and Growth Potential Outlook

- 1.1. Research Methods and Tools

- 1.2. Market Breakdown

- 1.2.1. By Segments

- 1.2.2. By Region

2. Market Overview and Insights

- 2.1. Scope of the Report

- 2.2. Analyst Insight & Current Market Trends

- 2.2.1. Key Findings

- 2.2.2. Recommendations

- 2.2.3. Conclusion

3. Competitive Landscape

- 3.1. Key Company Analysis

- 3.2. BAE Systems plc.

- 3.2.1. Overview

- 3.2.2. Financial Analysis

- 3.2.3. SWOT Analysis

- 3.2.4. Recent Developments

- 3.3. Lockheed Martin Corp.

- 3.3.1. Overview

- 3.3.2. Financial Analysis

- 3.3.3. SWOT Analysis

- 3.3.4. Recent Developments

- 3.4. Northrop Grumman.

- 3.4.1. Overview

- 3.4.2. Financial Analysis

- 3.4.3. SWOT Analysis

- 3.4.4. Recent Developments

- 3.5. RTX Corp.

- 3.5.1. Overview

- 3.5.2. Financial Analysis

- 3.5.3. SWOT Analysis

- 3.5.4. Recent Developments

- 3.6. THALES

- 3.6.1. Overview

- 3.6.2. Financial Analysis

- 3.6.3. SWOT Analysis

- 3.6.4. Recent Developments

- 3.7. Key Strategy Analysis

4. Market Segmentation

- 4.1. Global Digital Battlefield Market by Solution

- 4.1.1. Hardware

- 4.1.2. Software

- 4.1.3. Services

- 4.2. Global Digital Battlefield Market by Technology

- 4.2.1. Artificial Intelligence (AI)

- 4.2.2. Internet of Things (IoT)

- 4.2.3. Big Data Analytics

- 4.2.4. Robotics Process Automation (RPA)

- 4.2.5. Digital Twin

- 4.2.6. Others (5G, Virtual & Augmented Reality (VR &AR), and Blockchain)

- 4.3. Global Digital Battlefield Market by Platform

- 4.3.1. Land

- 4.3.2. Naval

- 4.3.3. Air

- 4.3.4. Space

- 4.4. Global Digital Battlefield Market by Application

- 4.4.1. Warfare Platforms

- 4.4.2. Cybersecurity

- 4.4.3. Surveillance and Situational Awareness (SSA)

- 4.4.4. Command and Control (C2)

- 4.4.5. Others (Training and Simulation)

5. Regional Analysis

- 5.1. North America

- 5.1.1. United States

- 5.1.2. Canada

- 5.2. Europe

- 5.2.1. UK

- 5.2.2. Germany

- 5.2.3. Italy

- 5.2.4. Spain

- 5.2.5. France

- 5.2.6. Rest of Europe

- 5.3. Asia-Pacific

- 5.3.1. China

- 5.3.2. India

- 5.3.3. Japan

- 5.3.4. South Korea

- 5.3.5. Rest of Asia-Pacific

- 5.4. Rest of the World

6. Company Profiles

- 6.1. Airbus

- 6.2. Amazon Web Services, Inc.

- 6.3. Anduril Ind. , Inc.

- 6.4. Atos SE

- 6.5. Boeing Co.

- 6.6. Cobham Ltd.

- 6.7. Cognite AS

- 6.8. Curtiss-Wright Corp.

- 6.9. Databricks, Inc.

- 6.10. Elbit Systems Ltd.

- 6.11. General Dynamics Corp.

- 6.12. Google Cloud Platform (Google LLC.)

- 6.13. GreyCastle Security, LLC

- 6.14. HENSOLDT AG

- 6.15. Hexagon AB

- 6.16. IBM Corp.

- 6.17. Indra

- 6.18. Israel Aerospace Industries (IAI)

- 6.19. Kongsberg Gruppen ASA

- 6.20. L3Harris Technologies, Inc.

- 6.21. Leonardo S.p.A.

- 6.22. Microsoft

- 6.23. Microsoft Azure (Microsoft)

- 6.24. Palantir Technologies Inc.

- 6.25. Rafael Advanced Defense Systems Ltd.

- 6.26. Rebellion Defense, Inc.

- 6.27. Rheinmetall AG

- 6.28. Saab

- 6.29. Snowflake Inc.

- 6.30. Textron Inc.