|

|

市場調査レポート

商品コード

1348940

衛星D2D(Direct-to-Device)市場:第4版Satellite Direct-to-Device Market, 4th Edition |

||||||

|

|

|||||||

|

|||||||

| 衛星D2D(Direct-to-Device)市場:第4版 |

|

出版日: 2023年09月20日

発行: Analysys Mason

ページ情報: 英文 21 Slides

納期: 即日から翌営業日

|

- 全表示

- 概要

- 目次

レポートの概要

衛星D2D(Direct-to-Device)市場:第4版は、衛星D2Dの市場機会、市場促進要因、抑制要因、主要使用事例、戦略的洞察などを包括的に分析したレポートです。

市場機会と概要:

- 当レポートでは、衛星業界における重要な成長分野である衛星D2D市場について解説しています。

- NSRはこの市場機会を明らかにした最初の市場調査会社の1つであり、当レポートは4回目の更新となります。

重点分野:

- 「D2D4」は、衛星D2D市場の動向と戦略的選択肢の全体像を構築することを目的としています。

- サービス収益とトラフィックを地域別、市場セグメント別に予測します。

- 衛星通信事業者、移動体通信事業者(MNO)、機器・インフラベンダーに対して、この成長市場の一部を獲得する方法について提言を行っています。

主な質問:

- 新興の衛星D2D市場にはどのような収益の機会があるのか?

- MNOは、衛星D2Dを活用して、地上波を超えてどのような使用事例をターゲットにできるか?

- 衛星D2Dの限界と強みは何か?

- 市場の将来を形成する主要な技術開発とは何か、また参入企業はこの進化にどのように適応していくべきか?

- 主な参入企業とその様々な戦略(周波数、供給と能力、標準、ビジネスモデルなど)

対象読者

衛星D2D(Direct-to-Device)市場レポートは、以下のような衛星および通信業界の様々な利害関係者を対象としています:

- 収益の可能性とトラフィック予測、市場力学を理解しようとする衛星通信事業者。

- 成長と差別化の源泉として衛星D2Dに関心を持つMNOとCSP。

- 周波数帯、標準、ビジネスモデルの戦略的選択を評価したいチップセットおよび部品ベンダー、OEM、インフラベンダー(宇宙および地上)。

- D2Dを活用してイノベーションを促進し、デジタル・デバイドを解消しようとする規制当局や業界機関。

差別化要因

- 衛星D2D(Direct-to-Device)市場は、衛星業界におけるNSRの専門知識と通信動向に関するAnalysys Masonの知識のユニークな組み合わせでお届けします。

- 「D2D4」は、宇宙産業への理解と通信事業者の動向や消費者ニーズに関するAnalysys Masonの洞察を活用しています。

- 第4版は、主要な業界関係者へのインタビューを含む広範な1次調査と、強固な2次調査の基礎に基づいています。

- 第4版は、将来の戦略的意思決定のためのロードマップとして、読者がダイナミックな衛星D2Dの状況における様々な市場セグメント、地域、戦略的オプションをナビゲートするのに役立ちます。

衛星D2D(Direct-to-Device)市場:第4版は、新たな衛星D2D市場の機会を活用することに関心のある業界利害関係者に貴重な洞察と提言を提供します。当レポートは、NSRとAnalysys Masonの専門知識を活用し、進化する衛星D2D市場の包括的かつ公平な分析を提供しています。

主な特徴

本レポートの対象

- 衛星D2Dエコシステムに参加するための主な推奨事項

- 地域別およびセグメント別のサービス収益予測

- 地域別およびセグメント別のトラフィック予測

- 対応可能な市場の定義

- 衛星D2D機能の主要な強みと限界のレビュー

- 技術進化のタイミングと市場開発への影響

- 主要な戦略的選択の評価と意味:周波数、標準、ビジネスモデル

レポートのセグメンテーション

- コンシューマー

- トラフィック

- サービス収益

- IoT

- トラフィック

- サービス収益

- 政府および軍事

- トラフィック

- サービス収益

本レポートに含まれる企業

Airbus、Apple、AST SpaceMobile、AT&T、Bullitt、Echostar、Ericsson、Globalstar、Honor、Huawei、Inmarsat、Iridium、Lynk、Mediatek、Motorola、Nokia、Nothing、OmniSpace、Oppo、PNCC、Qualcomm、Rakuten、Sateliot、SCT、Skylo、SMART、Starlink、Telefónica、Thales Alenia Space、T-Mobile、vivo、Vodafone、Xiaomi。

目次

このレポートについて

エグゼクティブサマリー

調査概要

- 課題:MNOの収益源と社会的影響は地上ネットワークの範囲により制限される

- ソリューション:衛星D2Dは、加入者のエンゲージメントを高め、新しいサービスを可能にし、地方のネットワーク展開コストを削減することで、MNOの機会を拡大

推奨事項

- 1. MNOの新たな差別化と成長の源としてのD2D

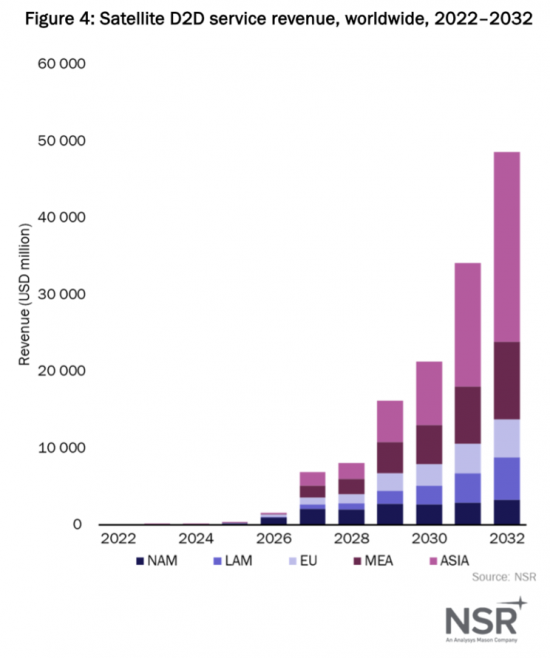

- 1.衛星D2Dサービスの収益は2032年までに486億米ドルに急増

- 2.D2Dは、消費者、IoT、政府/軍事の3つの主要セグメントから市場の関心を集める

- 3.消費者セグメントが収益シーンを支配しますが、IoTと政府/軍事が専門的な機会を提供

- 4.衛星D2DはMNOにとって競争上のリスクではないため、この技術は新たな収益源の実現手段として捉えられるべき。

- 2.急速に進化するテクノロジーとビジネスに適合

- 1.この分野の関係者は、テクノロジーとビジネスの驚異的な速さの進化に適応し続ける必要がある

- 2.供給のタイミングは、市場の準備と競争上の優位性のバランスをとるために重要。スペクトルは重要なリソースです。指数関数的な供給の増加が必要

- 3.バリューチェーンの調整

- 1.D2Dの複雑なソリューションを提供するには、適切なパートナーエコシステムの構築が重要

- 2.MNOのスペクトルを使用すると、後方互換性のおかげでより迅速な立ち上げが可能になる。規制の確実性とパフォーマンスの向上により、MSSの長期的な利点が生まれる。

- 3.独自のプロトコルは商用化へのより迅速な道を提供するが、拡張性を促進するためには標準ベースのソリューションが優先されるべき。

- 4.衛星サービスはMNOにとって魅力的な卸売モデルに重点を置くべき。

付録:調査手法

著者とAnalysys Masonについて

Report Summary:

“Satellite Direct to Device Markets, 4th Edition (D2D4) ” report provides a comprehensive analysis of the satellite D2D (Direct-to-Device) market opportunity, including market drivers and restraints, key use cases, and strategic insights.

Market Opportunity and Overview:

- The report describes the satellite D2D market opportunity, which represents a significant growth area within the satellite industry.

- NSR was one of the first market research firms to identify this opportunity, and this report represents the 4th annual update with a high level of maturity and in-depth analysis.

Key Focus Areas:

- “D2D4” aims to build a complete picture of trends and strategic choices within the satellite D2D market.

- It provides forecasts for service revenues and traffic broken down by region and market segment.

- Recommendations are offered for satellite operators, mobile network operators (MNOs), and equipment and infrastructure vendors on how to capture a portion of this growing market.

Key Questions Addressed:

- What is the revenue opportunity for the emerging satellite D2D market?

- What use cases can MNOs target beyond their terrestrial coverage leveraging satellite D2D?

- What are the limitations and strength of satellite D2D?

- Which are the key technology developments that will shape the future of the market and how should players stay adaptive to this evolution?

- Who are the main players and which are the different strategies (spectrum, supply and capabilities, standards, business models, etc.)?

Target Audience

“Satellite Direct to Device Markets” report is intended for various stakeholders in the satellite and telecommunications industries, including:

- Satellite operators seeking to understand revenue potential, traffic forecasts, and market dynamics.

- MNOs and CSPs interested in satellite D2D as a source of growth and differentiation.

- Chipset and parts vendors, OEMs, and infrastructure vendors (both space and terrestrial) looking to assess strategic choices in terms of spectrum, standards, and business models.

- Regulators and industry agencies seeking to leverage D2D to foster innovation and bridge the digital divide.

Differentiating Factors:

- “Satellite Direct to Device Markets” stands out due to the unique combination of expertise from NSR in the satellite industry and Analysys Mason's knowledge of telecommunications trends.

- “D2D4” leverages understanding of the space industry and Analysys Mason's insights into telco trends and consumer needs.

- “Satellite Direct to Device 4” draws from extensive primary research, including interviews with key industry players, and is based on a solid foundation of secondary research.

- “D2D4” serves as a roadmap for future strategic decisions, helping readers navigate various market segments, regions, and strategic options in the dynamic satellite D2D landscape.

“Satellite Direct to Device Markets, 4th Edition” report offers valuable insights and recommendations for industry stakeholders interested in capitalizing on the emerging satellite D2D market opportunity. It leverages the expertise of NSR and Analysys Mason to provide a comprehensive and unbiased analysis of this evolving landscape.

Key Features:

Covered in this Report:

- Key recommendations for participating in the satellite D2D ecosystem

- Service revenues forecast by region and segment

- Traffic forecast by region and segment

- Addressable market definition

- Review of the key strength and limitations of the satellite D2D capabilities

- Timing of the technology evolution and implications for the development of the market

- Assessment and implications of key strategic choices: spectrum, standards and business models

Report Segmentation:

- Consumer

- Traffic

- Service Revenues

- IoT

- Traffic

- Service Revenues

- Government and Military

- Traffic

- Service Revenues

Companies included in this Report:

Airbus, Apple, AST SpaceMobile, AT&T, Bullitt, Echostar, Ericsson, Globalstar, Honor, Huawei, Inmarsat, Iridium, Lynk, Mediatek, Motorola, Nokia, Nothing, OmniSpace, Oppo, PNCC, Qualcomm, Rakuten, Sateliot, SCT, Skylo, SMART, Starlink, Telefónica, Thales Alenia Space, T-Mobile, vivo, Vodafone, Xiaomi.

Table of Contents

About this report

Executive summary

Research overview

- Challenge: MNOs' revenue sources and social impact are limited by the reach of terrestrial networks

- Solution: Satellite D2D extends MNOs' opportunities by boosting subscriber engagement, enabling new services and reducing rural network deployment costs

Recommendations

- 1. D2D as MNOs' new source of differentiation and growth

- 1. Satellite D2D service revenues to skyrocket to 48.6USD billion by 2032

- 2. D2D will attract market interest from 3 main segments: consumer, IoT and Gov/Mil

- 3. Consumer segment to dominate the revenue scene, but IoT and Gov/Mil present specialized opportunities

- 4. Satellite D2D does not represent a competitive risk for MNOs. The technology should be regarded as an enabler for new revenue streams

- 2. Fit for the fast-paced technology and business evolution

- 1. Actors in the field should stay adaptative to the extraordinarily fast evolution in technology and business

- 2. Timing of supply is critical to balance market readiness and competitive advantage. Spectrum is the key resource. Exponential supply growth needed

- 3. Aligning the value chain

- 1. Building the right ecosystem of partners is critical to deliver D2D's complex solution

- 2. Using MNOs' spectrum offers faster ramp-up thanks to backward compatibility. MSS long-term advantages due to regulatory certainty and enhanced performances

- 3. Standards-based solutions should be the preferred approach to facilitate scalability, albeit proprietary protocols offer a faster path to commercialization

- 4. Satellite offerings should focus on wholesale models that are attractive for MNOs

Appendix Methodology

About the authors and Analysys Mason

List of Exhibits

- Figure 1: Evolving Space enablers unlocking the opportunities in the satellite D2D market

- Figure 2: MNOs' limitations to create and capture value beyond their coverage

- Figure 3: Key segments enabled by satellite D2D

- Figure 4: Satellite D2D service revenues worldwide, 2022-2032

- Figure 5: share of service revenues per vertical worldwide

- Figure 6: satellite D2D cumulative service revenues (USD million) worldwide, 2022 to 2032

- Figure 7: Satellite D2D traffic with technology phases worldwide, 2022 to 2032

- Figure 8: generic legacy constellation supply case study