|

|

市場調査レポート

商品コード

1389865

人工呼吸器の世界市場:モビリティ別・種類別・インターフェース別・モード別・エンドユーザー別・地域別の評価、機会と予測 (2016年~2030年)Global Ventilator Market Assessment, By Mobility, By Type, By, Interface, By Mode, By End-user, By Region, Opportunities and Forecast, 2016-2030F |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 人工呼吸器の世界市場:モビリティ別・種類別・インターフェース別・モード別・エンドユーザー別・地域別の評価、機会と予測 (2016年~2030年) |

|

出版日: 2023年12月04日

発行: Market Xcel - Markets and Data

ページ情報: 英文 202 Pages

納期: 3~5営業日

|

- 全表示

- 概要

- 図表

- 目次

世界の人工呼吸器の市場規模は、2022年に43億5,000万米ドルと評価され、予測期間中 (2023年から2030年) に4.26%のCAGRで成長し、2030年には60億7,000万米ドルに達すると予測されています。近年、人工呼吸器技術の進歩や人工呼吸器に使用されるセンサー技術の向上により、世界市場は発展しています。昨今はCOVID-19やその他の慢性疾患による入院が増加しているため、人工呼吸器の需要が大幅に増加しており、世界の人工呼吸器市場をさらに押し上げています。人工呼吸器需要の増加は、各企業をアンメットニーズへの対応に駆り立てています。一部の国では、需要と供給の間に対処可能なギャップがあり、これが各企業のビジネスチャンスとなっています。このように、世界の人工呼吸器市場は、ICU入室の増加、慢性疾患の有病率の増加、有効性と患者のコンプライアンスを高めるための製品の進歩などによって成長しています。さらに、COVID-19の大流行により、重症患者の治療システムの欠点が露呈しました。このため政府は、需要と供給のギャップを埋めるため、病院内の重症患者ケア環境の整備と進化に一層力を入れるようになっています。パンデミック期間中、人工呼吸器設置の著しい急増が観察されました。訓練を受けた専門家の不足と人工呼吸器に関連する合併症が、市場の妨げとなる課題です。

当レポートでは、世界の人工呼吸器の市場について分析し、製品の概略や市場の基本構造、全体的な市場規模の動向見通し、セグメント別・地域別の詳細動向、市場の背景事情や主な影響要因、主要企業のプロファイル・市場シェアなどを調査しております。

目次

第1章 調査手法

第2章 プロジェクトの範囲と定義

第3章 新型コロナウイルス感染症 (COVID-19) が世界の人工呼吸器市場に与える影響

第4章 エグゼクティブサマリー

第5章 世界の人工呼吸器市場の将来展望 (2016年~2030年)

- 市場規模と予測

- 金額ベース

- 数量ベース

- モビリティ別

- 集中治療用人工呼吸器

- ハイエンドICU人工呼吸器

- ミッドエンドICU人工呼吸器

- ベーシックICU人工呼吸器

- ポータブル/可搬型人工呼吸器

- 集中治療用人工呼吸器

- 種類別

- 成人用人工呼吸器

- 小児用人工呼吸器

- 新生児/乳児用人工呼吸器

- インターフェース別

- 侵襲的人工呼吸器

- 非侵襲的人工呼吸器

- モード別

- 複合式人工呼吸器

- 従量式人工呼吸器

- 従圧式人工呼吸器

- その他

- エンドユーザー別

- 病院

- 外来診療センター

- クリニック

- 在宅医療

- その他

- 地域別

- 北米

- 欧州

- 南米

- アジア太平洋

- 中東・アフリカ

- 企業別市場シェア (%、2022年)

第6章 世界の人工呼吸器市場の見通し、2016~2030年

第8章 世界の人工呼吸器市場の将来展望:地域別 (2016年~2030年)

- モビリティ別

- 種類別

- インターフェース別

- モード別

- エンドユーザー別

- 米国*

- モビリティ別

- 種類別

- インターフェース別

- モード別

- エンドユーザー別

- カナダ

- メキシコ

各セグメントの情報は、対象となる全ての地域・国について提供されます。

- 欧州

- ドイツ

- フランス

- イタリア

- 英国

- ロシア

- オランダ

- スペイン

- トルコ

- ポーランド

- 南米

- ブラジル

- アルゼンチン

- アジア太平洋

- インド

- 中国

- 日本

- オーストラリア

- ベトナム

- 韓国

- インドネシア

- フィリピン

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第7章 市場マッピング (2022年)

- モビリティ別

- 種類別

- インターフェース別

- モード別

- エンドユーザー別

- 地域別

第8章 マクロ環境と産業構造

- 需給分析

- 輸出入分析 (数量・金額ベース)

- サプライ/バリューチェーン分析

- PESTEL分析

- ポーターのファイブフォース分析

第9章 市場力学

- 成長促進要因

- 成長抑制要因 (課題、制約)

第10章 規制の枠組みとイノベーション

- 臨床試験

- 特許の情勢

- 規制当局の承認

- イノベーション/新興技術

第11章 主要企業の情勢

- 市場リーダー上位5社:競合マトリックス

- 市場リーダー上位5社:市場収益分析 (%、2022年)

- 企業合併・買収 (M&A)/合弁事業 (該当する場合)

- SWOT分析 (市場参入企業5社の場合)

- 特許分析 (該当する場合)

第12章 価格分析

第13章 ケーススタディ

第14章 主要企業の見通し

- Koninklijke Philips NV

- 企業概要

- 経営幹部

- 製品・サービス

- 財務状況 (報告どおり)

- 重点市場と地理的プレゼンス

- 最近の動向

- Getinge AB

- ResMed

- Medtronic

- Fisher &Paykel Healthcare Limited

- Avasarala Technologies Limited

- Allied Healthcare Products, Inc.

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd,

- Dragerwerk AG &CO. KGAA

- Nihon Kohden Corporation

上記企業は市場シェア順ではなく、調査作業中に入手した情報に従って変更される可能性があります。

第15章 戦略提言

第16章 Market Xcelについて、免責事項

List of Tables

- Table 1. Pricing Analysis of Products from Key Players

- Table 2. Competition Matrix of Top 5 Market Leaders

- Table 3. Mergers & Acquisitions/ Joint Ventures (If Applicable)

- Table 4. About Us - Regions and Countries Where We Have Executed Client Projects

List of Figures

- Figure 1. Global Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 2. Global Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 3. Global Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 4. Global Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 5. Global Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 6. Global Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 7. Global Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 8. Global Ventilator Market Share, By Region, In USD Billion, 2016-2030F

- Figure 9. North America Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 10. North America Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 11. North America Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 12. North America Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 13. North America Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 14. North America Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 15. North America Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 16. North America Ventilator Market Share, By Country, In USD Billion, 2016-2030F

- Figure 17. United States Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 18. United States Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 19. United States Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 20. United States Ventilator Market Share, By Type, In USD Billion, 2016-2030F

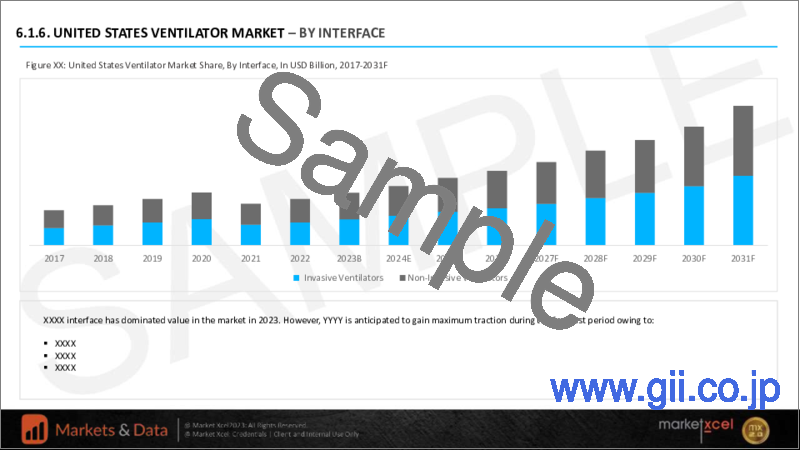

- Figure 21. United States Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 22. United States Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 23. United States Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 24. Canada Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 25. Canada Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 26. Canada Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 27. Canada Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 28. Canada Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 29. Canada Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 30. Canada Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 31. Mexico Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 32. Mexico Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 33. Mexico Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 34. Mexico Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 35. Mexico Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 36. Mexico Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 37. Mexico Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 38. Europe Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 39. Europe Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 40. Europe Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 41. Europe Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 42. Europe Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 43. Europe Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 44. Europe Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 45. Europe Ventilator Market Share, By Country, In USD Billion, 2016-2030F

- Figure 46. Germany Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 47. Germany Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 48. Germany Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 49. Germany Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 50. Germany Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 51. Germany Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 52. Germany Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 53. France Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 54. France Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 55. France Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 56. France Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 57. France Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 58. France Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 59. France Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 60. Italy Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 61. Italy Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 62. Italy Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 63. Italy Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 64. Italy Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 65. Italy Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 66. Italy Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 67. United Kingdom Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 68. United Kingdom Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 69. United Kingdom Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 70. United Kingdom Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 71. United Kingdom Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 72. United Kingdom Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 73. United Kingdom Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 74. Russia Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 75. Russia Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 76. Russia Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 77. Russia Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 78. Russia Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 79. Russia Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 80. Russia Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 81. Netherlands Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 82. Netherlands Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 83. Netherlands Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 84. Netherlands Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 85. Netherlands Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 86. Netherlands Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 87. Netherlands Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 88. Spain Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 89. Spain Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 90. Spain Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 91. Spain Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 92. Spain Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 93. Spain Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 94. Spain Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 95. Turkey Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 96. Turkey Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 97. Turkey Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 98. Turkey Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 99. Turkey Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 100. Turkey Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 101. Turkey Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 102. Poland Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 103. Poland Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 104. Poland Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 105. Poland Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 106. Poland Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 107. Poland Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 108. Poland Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 109. South America Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 110. South America Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 111. South America Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 112. South America Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 113. South America Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 114. South America Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 115. South America Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 116. South America Ventilator Market Share, By Country, In USD Billion, 2016-2030F

- Figure 117. Brazil Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 118. Brazil Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 119. Brazil Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 120. Brazil Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 121. Brazil Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 122. Brazil Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 123. Brazil Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 124. Argentina Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 125. Argentina Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 126. Argentina Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 127. Argentina Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 128. Argentina Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 129. Argentina Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 130. Argentina Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 131. Asia-Pacific Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 132. Asia-Pacific Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 133. Asia-Pacific Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 134. Asia-Pacific Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 135. Asia-Pacific Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 136. Asia-Pacific Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 137. Asia- Pacific Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 138. Asia-Pacific Ventilator Market Share, By Country, In USD Billion, 2016-2030F

- Figure 139. India Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 140. India Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 141. India Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 142. India Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 143. India Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 144. India Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 145. India Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 146. China Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 147. China Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 148. China Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 149. China Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 150. China Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 151. China Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 152. China Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 153. Japan Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 154. Japan Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 155. Japan Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 156. Japan Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 157. Japan Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 158. Japan Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 159. Japan Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 160. Australia Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 161. Australia Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 162. Australia Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 163. Australia Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 164. Australia Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 165. Australia Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 166. Australia Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 167. Vietnam Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 168. Vietnam Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 169. Vietnam Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 170. Vietnam Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 171. Vietnam Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 172. Vietnam Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 173. Vietnam Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 174. South Korea Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 175. South Korea Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 176. South Korea Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 177. South Korea Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 178. South Korea Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 179. South Korea Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 180. South Korea Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 181. Indonesia Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 182. Indonesia Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 183. Indonesia Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 184. Indonesia Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 185. Indonesia Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 186. Indonesia Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 187. Indonesia Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 188. Philippines Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 189. Philippines Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 190. Philippines Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 191. Philippines Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 192. Philippines Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 193. Philippines Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 194. Philippines Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 195. Middle East & Africa Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 196. Middle East & Africa Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 197. Middle East & Africa Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 198. Middle East & Africa Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 199. Middle East & Africa Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 200. Middle East & Africa Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 201. Middle East & Africa Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 202. Middle East & Africa Ventilator Market Share, By Country, In USD Billion, 2016-2030F

- Figure 203. Saudi Arabia Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 204. Saudi Arabia Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 205. Saudi Arabia Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 206. Saudi Arabia Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 207. Saudi Arabia Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 208. Saudi Arabia Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 209. Saudi Arabia Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 210. UAE Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 211. UAE Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 212. UAE Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 213. UAE Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 214. UAE Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 215. UAE Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 216. UAE Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 217. South Africa Ventilator Market, By Value, In USD Billion, 2016-2030F

- Figure 218. South Africa Ventilator Market, By Volume, In Units, 2016-2030F

- Figure 219. South Africa Ventilator Market Share, By Mobility, In USD Billion, 2016-2030F

- Figure 220. South Africa Ventilator Market Share, By Type, In USD Billion, 2016-2030F

- Figure 221. South Africa Ventilator Market Share, By Interface, In USD Billion, 2016-2030F

- Figure 222. South Africa Ventilator Market Share, By Mode, In USD Billion, 2016-2030F

- Figure 223. South Africa Ventilator Market Share, By End-User, In USD Billion, 2016-2030F

- Figure 224. By Mobility Map-Market Size (USD Billion) & Growth Rate (%), 2022

- Figure 225. By Type Map-Market Size (USD Billion) & Growth Rate (%), 2022

- Figure 226. By Interface Map-Market Size (USD Billion) & Growth Rate (%), 2022

- Figure 227. By Mode Map-Market Size (USD Billion) & Growth Rate (%), 2022

- Figure 228. By End-User Map-Market Size (USD Billion) & Growth Rate (%), 2022

- Figure 229. By Region Map-Market Size (USD Billion) & Growth Rate (%), 2022

Global ventilator market was valued at USD 4.35 billion in 2022, expected to reach USD 6.07 billion in 2030 with a CAGR of 4.26% for the forecast period between 2023 and 2030F. The global market has evolved in recent years owing to technological advances in ventilator technology and improved sensor technologies utilized in ventilators. With increasing hospitalization due to COVID-19 and other chronic diseases in recent years, the demand for ventilators has increased significantly, further boosting the global ventilator market. The increased demand for ventilators is pushing the market players to cater to the unmet needs. Several nations have an addressable gap between supply and demand that can serve as an opportunity for market players. Thus, the global ventilator market is growing due to increasing ICU admissions, increased chronic disease prevalence, advancements in products to enhance effectiveness and patient compliance, and so on. Moreover, the COVID-19 pandemic exposed the shortcomings of the critical care system. This led governments to focus more on developing and evolving the critical care settings in hospitals to bridge the demand and supply gap. A notable surge in ventilator installations has been observed during the pandemic period. Lack of trained professionals and complications associated with ventilators are the challenges that can hinder the market.

Increasing ICU Admissions Due to COVID-19 and Growing Burden of Chronic Disease

The global ventilator market is undergoing a significant transformation due to the simultaneous increase in ICU admissions and the growing burden of chronic diseases. The surge in ICU admissions, especially during the COVID-19 pandemic, has placed immense pressure on healthcare systems worldwide. This increased demand for ventilators as a critical tool in managing severe respiratory conditions led to a substantial increase in production and distribution. The rising prevalence of chronic diseases, such as chronic obstructive pulmonary disease (COPD) and cardiovascular disease, is contributing to a consistent requirement for ventilatory support in non-ICU settings. As a result, the global ventilator market is expanding to meet these evolving healthcare needs, with technological advancements and an increased focus on developing more accessible and advanced ventilator solutions. This dual impact of surging ICU admissions and the increasing chronic disease burden is reshaping the ventilator market, making it an important sector for innovation and investment in the healthcare industry.

Introduction Of Cutting-Edge Technologies in Ventilators

Technological advancements are playing a significant role in driving the global ventilator market. These innovations are not only enhancing the performance and capabilities of ventilators but also addressing critical issues related to patient comfort, ease of use, and remote monitoring. Smart ventilators equipped with sophisticated sensors and connectivity features are becoming increasingly prevalent, allowing healthcare providers to monitor patients' respiratory status and adjust settings remotely, thereby improving patient care and reducing the workload on healthcare staff. Furthermore, the integration of artificial intelligence and machine learning enables ventilators to adapt to real-time to fulfil individual patient needs, optimizing treatment and reducing the risk of complications.

Additionally, advancements in materials and design are making ventilators more compact and portable, facilitating their use in various healthcare settings. These technological advancements are increasing the efficiency of ventilators and expanding their application. Pune's medical device company, Noccarc, launched Noccarc V730i Smart ICU Ventilator in June 2023. The Noccarc V730i, uses smart technology to enhance critical care. This ventilator can access cloud capabilities through its internet connectivity, enabling remote software updates.

Government Initiatives

Governments around the globe have provided financial incentives and regulatory support to encourage research, development, and manufacturing of ventilators, leading to innovations in design, functionality, and accessibility. Ventilators are an essential part of critical healthcare systems and several government initiatives in different countries have provided cost-efficient and effective solutions to the public. During the COVID-19 pandemic, the demand for ventilators in hospitals grew exponentially, which led the governments to take immediate action to facilitate critical care management of patients. Governments provided financial incentives and regulatory support to encourage research, development, and manufacturing of ventilators. The government of the United States, under the Defense Production Act, paid Philips USD 646.7 million to deliver 2,500 ventilators to the Strategic National Stockpile by the end of May 2020. This was part of a larger initiative aiming to provide 43,000 ventilators by the end of 2020. In India, the PM CARES fund allocated USD 280 million to supply 50,000 "made in India" ventilators to government-run COVID-19 hospitals in all states and union territories.

Impact of COVID-19

The global ventilator market experienced a significant impact due to the COVID-19 pandemic. With the rapid and widespread transmission of the virus, the need for ventilators surged dramatically, particularly during the initial stages of the pandemic when hospitals faced unprecedented patient loads. This sudden surge in demand led to shortages in many regions, prompting governments and healthcare providers to bolster their ventilator supplies. Italy witnessed a significant growth of 66.42% in the number of ICU units. There were 5179 ICU units before the pandemic, reaching 8619 post COVID-19 pandemic.

Consequently, there was a significant increase in the production and procurement of ventilators worldwide, with numerous companies and industries pivoting to address the urgent need. The pandemic also accelerated innovations in ventilator technology, focusing on improved patient monitoring and portability. While the initial demand has subsided, the pandemic highlighted the importance of ventilator infrastructure and readiness for future health crisis.

Portable Ventilators will Grow at a Faster Pace

The future of portable ventilators will witness rapid growth in the forecasted period. Several factors drive this surge in demand for portable ventilators. Firstly, technological advancements have made it possible to develop compact, lightweight, and battery-powered ventilators that offer mobility and flexibility, allowing patients greater freedom and independence. As healthcare trends increasingly shift towards home-based and outpatient care, the need for portable ventilators will keep growing by allowing patients to manage their respiratory conditions in familiar and comfortable settings. Additionally, the ongoing emphasis on telemedicine and remote monitoring further underscores the importance of portable ventilators, which healthcare professionals can remotely control and monitor.

In October 2021, Movair announced the commercial launch of Luisa Life Supporting Ventilator with high-flow oxygen therapy in the United States. Luisa is equipped with a 10-inch display that can be rotated, along with adaptable connectivity features, allowing patients to seamlessly incorporate the ventilator into their everyday routines, including aligning it with their preferred side of the bed for sleeping. Additionally, Luisa offers multi-language programming capabilities, guaranteeing that a wide array of patients, families, and caregivers can easily understand the alarm notifications.

Key Players Landscape and Outlook

The global ventilator market features a landscape dominated by key players such as Koninklijke Philips N.V., Getinge AB, ResMed, Medtronic, Fisher & Paykel Healthcare Limited, Avasarala Technologies Limited, Allied Healthcare Products, Inc., Shenzhen Mindray Bio-Medical Electronics Co. Ltd and many others. Companies are introducing ventilators with additional features and organizations are also focusing on portable ventilators. Market players are developing partnerships to reach emerging and underdeveloped economies.

United Kingdom based manufacturer of anesthesia equipment OES Medical launched its new mains-powered ICU ventilator to support hospitals in managing oxygen demand at Arab Health 2022. The Gemini-G100, is an electrically operated piston ICU ventilator equipped with an integrated oxygen concentrator, tailored for intensive care applications. This device is specifically engineered for use in situations where a readily available supply of high-pressure oxygen gas is limited. The Gemini-G100 doesn't impose any oxygen supply burden on the hospital as it only requires electrical power. This feature greatly benefits hospitals by reducing their dependency on oxygen deliveries, particularly during periods of heightened demand.

Table of Contents

1. Research Methodology

2. Project Scope & Definitions

3. Impact of COVID-19 on Global Ventilator Market

4. Executive Summary

5. Global Ventilator Market Outlook, 2016-2030F

- 5.1. Market Size & Forecast

- 5.1.1. By Value

- 5.1.2. By Volume

- 5.2. By Mobility

- 5.2.1. Intensive Care Ventilators

- 5.2.1.1. High-End ICU Ventilators

- 5.2.1.2. Mid-End ICU Ventilators

- 5.2.1.3. Basic ICU Ventilators

- 5.2.2. Portable/Transportable Ventilators

- 5.2.1. Intensive Care Ventilators

- 5.3. By Type

- 5.3.1. Adult Ventilators

- 5.3.2. Pediatric Ventilators

- 5.3.3. Neonatal/Infant Ventilators

- 5.4. By Interface

- 5.4.1. Invasive Ventilators

- 5.4.2. Non-Invasive Ventilators

- 5.5. By Mode

- 5.5.1. Combined Mode Ventilators

- 5.5.2. Volume Mode Ventilators

- 5.5.3. Pressure Mode Ventilators

- 5.5.4. Others

- 5.6. By End-user

- 5.6.1. Hospitals

- 5.6.2. Ambulatory Care Centers

- 5.6.3. Clinics

- 5.6.4. Home Care Settings

- 5.6.5. Others

- 5.7. By Region

- 5.7.1. North America

- 5.7.2. Europe

- 5.7.3. South America

- 5.7.4. Asia-Pacific

- 5.7.5. Middle East and Africa

- 5.7 By Company Market Share (%), 2022

6. Global Ventilator Market Outlook, 2016-2030F

- 6.1. North America*

- 6.1.1. By Mobility

- 6.1.1.1. Intensive Care Ventilators

- 6.1.1.1.1. High-End ICU Ventilators

- 6.1.1.1.2. Mid-End ICU Ventilators

- 6.1.1.1.3. Basic ICU Ventilators

- 6.1.1.2. Portable/Transportable Ventilators

- 6.1.2. By Type

- 6.1.2.1. Adult Ventilators

- 6.1.2.2. Pediatric Ventilators

- 6.1.2.3. Neonatal/Infant Ventilators

- 6.1.3. By Interface

- 6.1.3.1. Invasive Ventilators

- 6.1.3.2. Non-Invasive Ventilators

- 6.1.4. By Mode

- 6.1.4.1. Combined Mode Ventilators

- 6.1.4.2. Volume Mode Ventilators

- 6.1.4.3. Pressure Mode Ventilators

- 6.1.4.4. Others

- 6.1.5. By End-user

- 6.1.5.1. Hospitals

- 6.1.5.2. Ambulatory Care Centers

- 6.1.5.3. Clinics

- 6.1.5.4. Home Care Settings

- 6.1.5.5. Others

- 6.1.6. United States*

- 6.1.6.1. By Mobility

- 6.1.6.1.1. Intensive Care Ventilators

- 6.1.6.1.1.1. High-End ICU Ventilators

- 6.1.6.1.1.2. Mid-End ICU Ventilators

- 6.1.6.1.1.3. Basic ICU Ventilators

- 6.1.6.1.2. Portable/Transportable Ventilators

- 6.1.6.2. By Type

- 6.1.6.2.1. Adult Ventilators

- 6.1.6.2.2. Pediatric Ventilators

- 6.1.6.2.3. Neonatal/Infant Ventilators

- 6.1.6.3. By Interface

- 6.1.6.3.1. Invasive Ventilators

- 6.1.6.3.2. Non-Invasive Ventilators

- 6.1.6.4. By Mode

- 6.1.6.4.1. Combined Mode Ventilators

- 6.1.6.4.2. Volume Mode Ventilators

- 6.1.6.4.3. Pressure Mode Ventilators

- 6.1.6.4.4. Others

- 6.1.6.5. By End-user

- 6.1.6.5.1. Hospitals

- 6.1.6.5.2. Ambulatory Care Centers

- 6.1.6.5.3. Clinics

- 6.1.6.5.4. Home Care Settings

- 6.1.6.5.5. Others

- 6.1.7. Canada

- 6.1.8. Mexico

- 6.1.1. By Mobility

All segments will be provided for all regions and countries covered:

- 6.2. Europe

- 6.2.1. Germany

- 6.2.2. France

- 6.2.3. Italy

- 6.2.4. United Kingdom

- 6.2.5. Russia

- 6.2.6. Netherlands

- 6.2.7. Spain

- 6.2.8. Turkey

- 6.2.9. Poland

- 6.3. South America

- 6.3.1. Brazil

- 6.3.2. Argentina

- 6.4. Asia-Pacific

- 6.4.1. India

- 6.4.2. China

- 6.4.3. Japan

- 6.4.4. Australia

- 6.4.5. Vietnam

- 6.4.6. South Korea

- 6.4.7. Indonesia

- 6.4.8. Philippines

- 6.5. Middle East & Africa

- 6.5.1. Saudi Arabia

- 6.5.2. UAE

- 6.5.3. South Africa

7. Market Mapping, 2022

- 7.1. By Mobility

- 7.2. By Type

- 7.3. By Interface

- 7.4. By Mode

- 7.5. By End-user

- 7.6. By Region

8. Macro Environment and Industry Structure

- 8.1. Supply Demand Analysis

- 8.2. Import Export Analysis - Volume and Value

- 8.3. Supply/Value Chain Analysis

- 8.4. PESTEL Analysis

- 8.4.1. Political Factors

- 8.4.2. Economic System

- 8.4.3. Social Implications

- 8.4.4. Technological Advancements

- 8.4.5. Environmental Impacts

- 8.4.6. Legal Compliances and Regulatory Policies (Statutory Bodies Included)

- 8.5. Porter's Five Forces Analysis

- 8.5.1. Supplier Power

- 8.5.2. Buyer Power

- 8.5.3. Substitution Threat

- 8.5.4. Threat from New Entrant

- 8.5.5. Competitive Rivalry

9. Market Dynamics

- 9.1. Growth Drivers

- 9.2. Growth Inhibitors (Challenges, Restraints)

10. Regulatory Framework and Innovation

- 10.1. Clinical Trials

- 10.2. Patent Landscape

- 10.3. Regulatory Approvals

- 10.4. Innovations/Emerging Technologies

11. Key Players Landscape

- 11.1. Competition Matrix of Top Five Market Leaders

- 11.2. Market Revenue Analysis of Top Five Market Leaders (in %, 2022)

- 11.3. Mergers and Acquisitions/Joint Ventures (If Applicable)

- 11.4. SWOT Analysis (For Five Market Players)

- 11.5. Patent Analysis (If Applicable)

12. Pricing Analysis

13. Case Studies

14. Key Players Outlook

- 14.1. Koninklijke Philips N.V.

- 14.1.1. Company Details

- 14.1.2. Key Management Personnel

- 14.1.3. Products & Services

- 14.1.4. Financials (As reported)

- 14.1.5. Key Market Focus & Geographical Presence

- 14.1.6. Recent Developments

- 14.2. Getinge AB

- 14.3. ResMed

- 14.4. Medtronic

- 14.5. Fisher & Paykel Healthcare Limited

- 14.6. Avasarala Technologies Limited

- 14.7. Allied Healthcare Products, Inc.

- 14.8. Shenzhen Mindray Bio-Medical Electronics Co., Ltd,

- 14.9. Dragerwerk AG & CO. KGAA

- 14.10. Nihon Kohden Corporation

Companies mentioned above DO NOT hold any order as per market share and can be changed as per information available during research work.